Market Trends of Slovenia Property And Casualty Insurance Industry

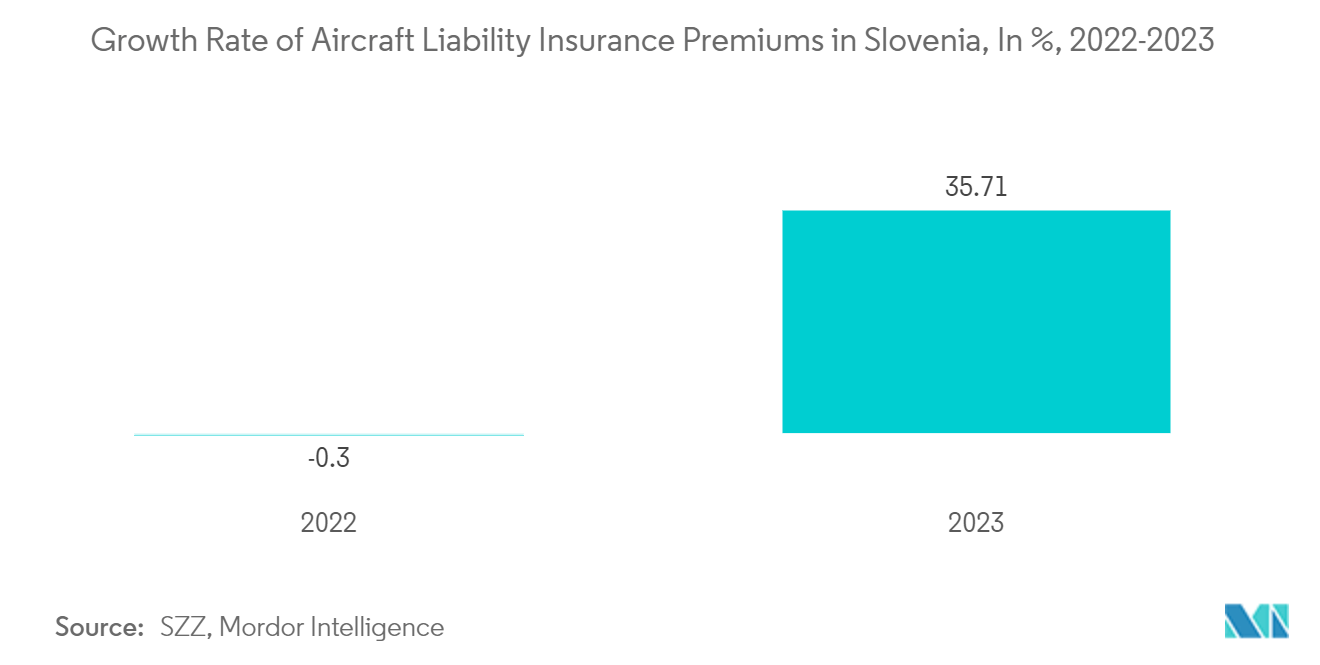

Unprecedented Surge in Demand for Aircraft Liability Insurance

Slovenia experienced a notable uptick in demand for aircraft liability insurance as numerous aviation operators and owners sought coverage. This surge was primarily fueled by a rebound in the country's economy post-COVID-19, leading to heightened air traffic and intensified activities in the aviation industry. Key drivers in the market include the expansion of commercial and private aviation fleets, an uptick in aircraft operations and flight hours, and the stringent regulatory mandates for liability insurance. In response, Slovenian insurance providers rolled out more comprehensive liability policies featuring elevated coverage limits and customized provisions to meet the dynamic needs of aircraft operators. These developments highlight a prevailing trend in the aviation insurance market, with providers consistently adjusting to the industry's changing demands and regulatory shifts.

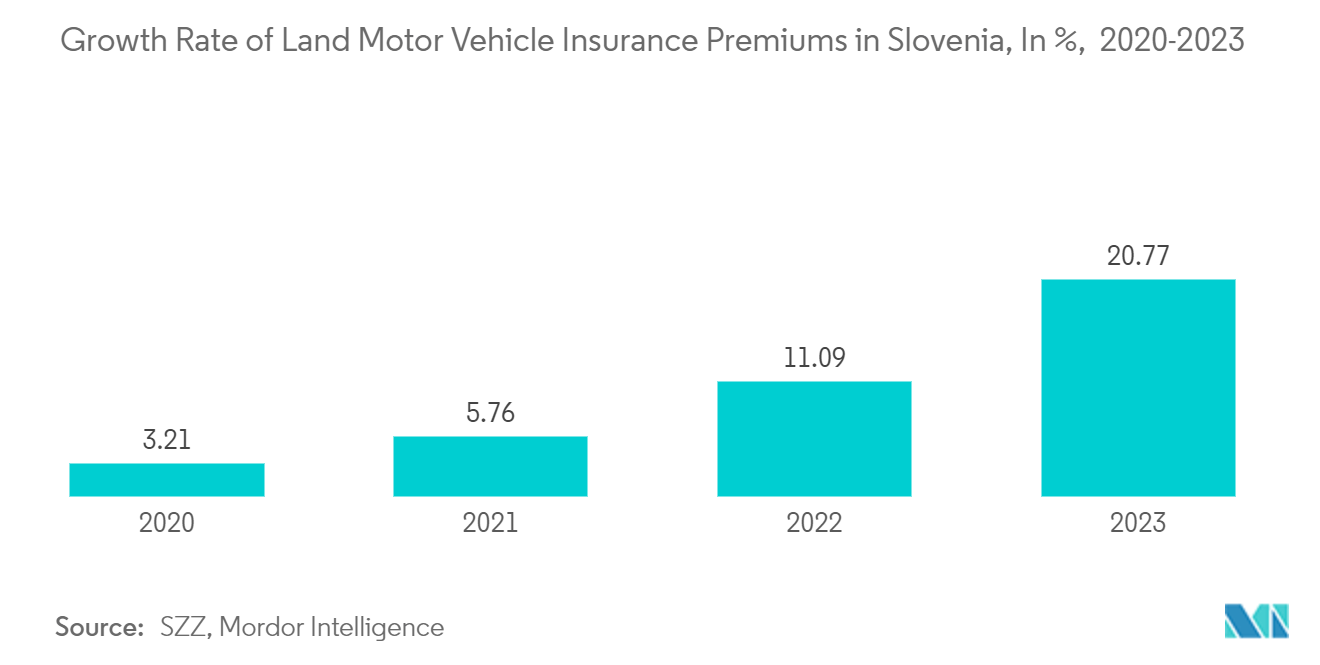

Increase in Land Motor Vehicle Insurance Claims Fueling the Market Growth

Slovenia's land motor vehicle insurance industry has seen robust growth, fueled by rising vehicle ownership and shifts in regulations. This momentum suggests a promising trajectory for the market in the years ahead. Insights from the Bank of Slovenia highlight that foreign direct investments (FDI) predominantly targeted the manufacturing sector (32.8%), trailed by financial and insurance activities (20.6%) and wholesale and retail trade, which encompasses motor vehicle and motorcycle repairs (19%). With these increasing rates, the trend of consumers comparing auto insurance options is expected to persist.

Additionally, interactions between customers and digital platforms, enhanced by AI, are witnessing a notable rise. The Slovenian government has implemented several regulatory changes aimed at improving road safety and insurance coverage, further driving market growth. Furthermore, advanced technologies like telematics and usage-based insurance (UBI) are increasingly being adopted, providing personalized insurance plans tailored to driving behavior.