Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

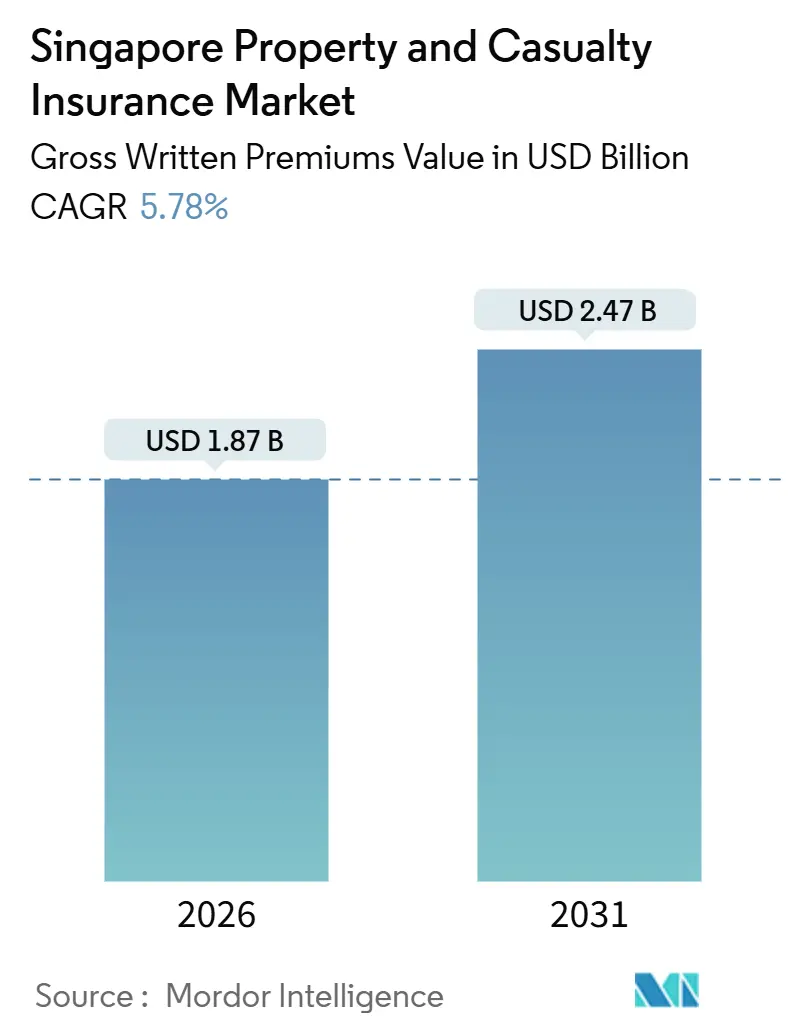

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

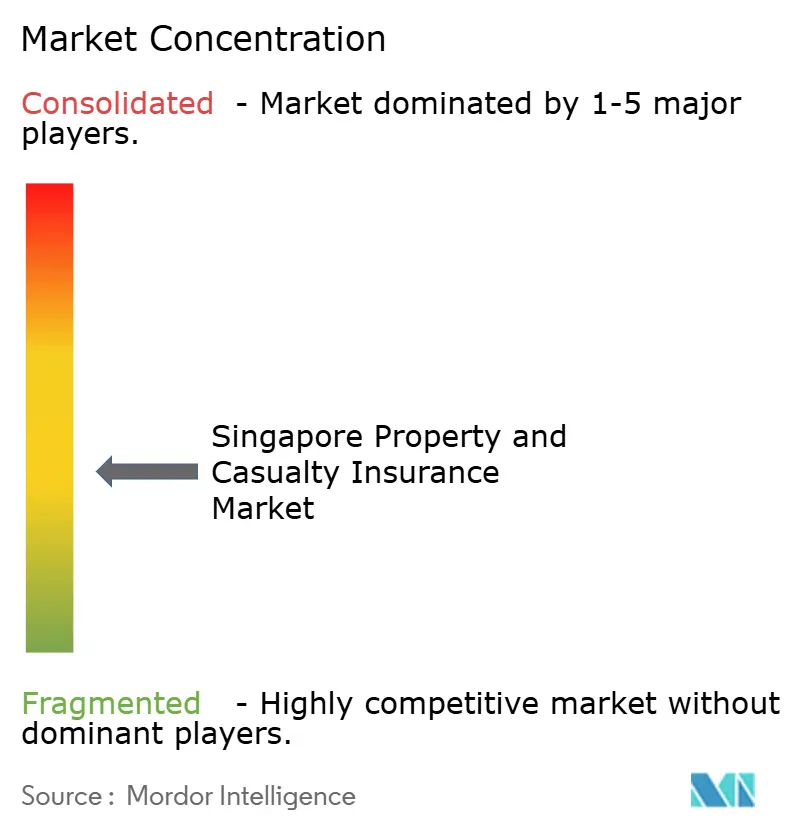

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Property And Casualty Insurance Market Analysis by Mordor Intelligence

The Singapore property and casualty insurance market size stands at USD 1.87 billion in 2026 and is forecast to reach USD 2.47 billion by 2031 at a 5.78% CAGR. The market’s growth rhythm reflects a shift from a decade of stronger expansion, as the general insurance sector averaged near 8% annual growth through 2024, setting the context for moderated gains as pricing becomes more competitive. Underwriting discipline is now central, after domestic underwriting profit fell 16.7% in 2024 even as gross written premiums increased 8.3%. Regulatory tightening under the Risk-Based Capital 2 framework reinforces capital quality, with updates effective January 1, 2026, on Additional Tier 1 and Tier 2 capital instruments to safeguard retail investors. Government-backed schemes for homes and mortgages, as well as the city-state’s hub role in marine and specialty risk, support diversified demand across lines.

Key Report Takeaways

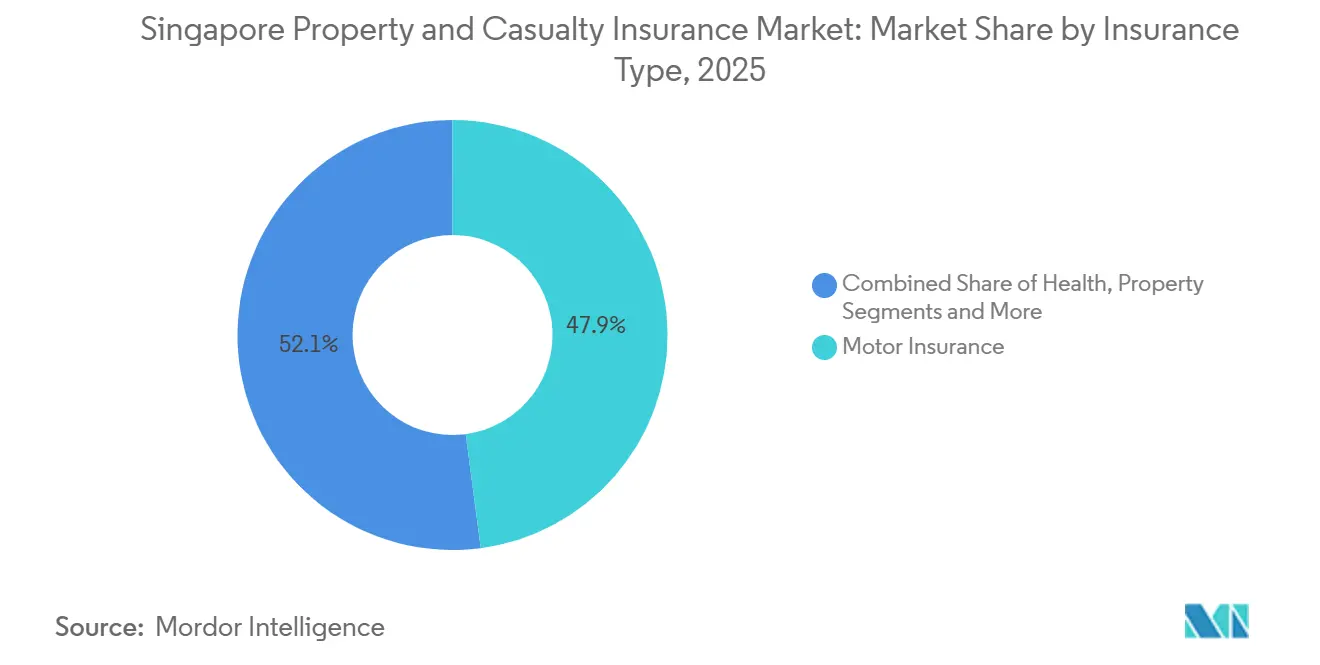

- By line of business, motor insurance led with 47.9% revenue share of the Singapore Property and Casualty insurance market size in 2025, while other insurance is projected to expand at an 8.95% CAGR through 2031.

- By customer type, the corporate segment held 56.5% of the Singapore Property and Casualty Insurance market size in 2025 and is forecast to record a 10.40% CAGR to 2031.

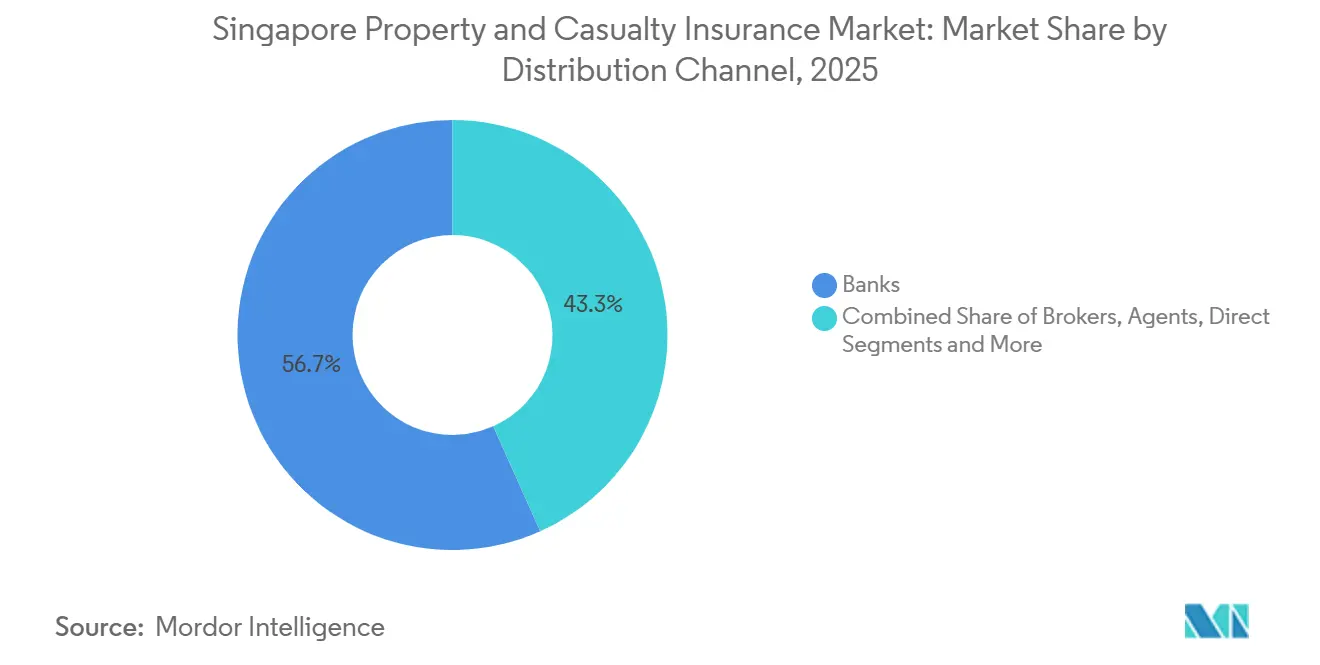

- By distribution channel, banks accounted for 56.7% of the Singapore Property and Casualty Insurance market size in 2025, while brokers and agents are projected to grow at a 7.65% CAGR through 2031.

- The Singapore Property and Casualty Insurance market is highly competitive, with share distribution spread across composite insurers, bancassurance players, and specialty-focused entities.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Property And Casualty Insurance Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strengthening Market Confidence Through Robust Regulation | +1.2% | Singapore domestic market | Medium term (2-4 years) |

| Leveraging Singapore's Role as a Regional Trade and Maritime Hub | +0.8% | Singapore and ASEAN corridors | Long term (≥ 4 years) |

| Driving P&C Uptake via Government-Backed Insurance Schemes | +1.5% | National, property and mortgage-linked lines | Short term (≤ 2 years) |

| Expanding Specialty Lines Through Rising Risk Awareness | +1.3% | Singapore with regional corporate spillovers | Medium term (2-4 years) |

| Bancassurance Scale and Embedded Distribution | +0.6% | National, retail and SME segments | Medium term (2-4 years) |

| Offshore Risk Aggregation and ILS or Parametric Market Development | +0.5% | Regional risks domiciled in Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strengthening Market Confidence Through Robust Regulation

Risk-Based Capital 2 enhancements that took effect January 1, 2026, require that Additional Tier 1 and Tier 2 instruments be sold only to non-retail investors to qualify as regulatory capital, which lifts the quality of capital and shields retail investors from complex structures. These measures improve solvency resilience and indirectly strengthen confidence in the Singapore property and casualty insurance market as risk sensitivity rises in underwriting and investment policies[1]Monetary Authority of Singapore, “Notice 133 Valuation and Capital Framework for Insurers,” MAS, mas.gov.sg. The regulatory environment remains active, and supervisors continue to refine guidance and expectations on governance, distribution, and conduct, signaling a durable compliance baseline that supports premium sustainability. Legislative oversight is also more assertive, evidenced by the Insurance (Amendment) Act 2024, which set the stage for ministerial intervention in transactions where public interest factors are significant. Together, these shifts boost the credibility of prudential safeguards and foster long-term stability that is supportive of orderly growth in the Singapore property and casualty insurance market.

Leveraging Singapore's Role as a Regional Trade and Maritime Hub

Singapore’s leading position as Asia’s second-largest marine hull underwriter and fourth worldwide anchors a steady flow of specialty risk, reinsurance placements, and complex coverage requirements that spill over into related lines. Hosting of major international marine insurance events underscores the city-state’s role in convening global markets, which benefits the Singapore property and casualty insurance market through knowledge transfer and deal origination. Regional risk pooling and parametric structures are also gaining traction, with the Southeast Asia Disaster Risk Insurance Facility operating from Singapore and delivering rapid post-disaster payouts in 2025 that demonstrate operational maturity[2]Global Asia Insurance Partnership, “Charting the path to close Asia’s $1tn insurance protection gap,” GAIP, gaip.global. Singapore's regulatory clarity and concentration of insurers, reinsurers, and brokers create a natural hub for complex risk financing that benefits specialty segments within the Singapore property and casualty insurance market. This hub dynamic remains a long-term structural advantage, especially as Southeast Asia’s infrastructure and logistics expansion continues to demand sophisticated coverage options.

Driving P&C Uptake via Government-Backed Insurance Schemes

The Home Protection Scheme is compulsory for eligible Housing & Development Board flat owners using CPF savings, which anchors penetrated mortgage-linked protection and reduces default risk tied to mortality and disability. Regulatory amendments in May 2025 expanded eligibility to members with certain pre-existing conditions, subject to premium loading caps, which enhances inclusion while preserving actuarial safeguards. The HDB Fire Insurance Scheme remains compulsory for HDB flat owners servicing HDB loans, which ensures baseline structural coverage and creates an upsell path to private plans for contents and renovations. These schemes provide recurring premium pools that stabilize the Singapore property and casualty insurance market, while complementary private plans build on the foundation created by mandatory coverage. Widespread protection adoption in health across Singapore further shapes demand for accident and riders, with the life sector reporting strong new business momentum in 2025 that signals robust household insurance engagement.

Expanding Specialty Lines Through Rising Risk Awareness

Corporate risk awareness is lifting demand in cyber, financial lines, and engineering, supported by evolving regulatory expectations on operational resilience and technology risk management across financial institutions. Specialty growth is reinforced by the availability of capacity and the broader hub ecosystem, where reinsurance, brokers, and carriers coordinate on coverage innovation and underwriting standards in Singapore. Directors and Officers liability conditions remain accommodative, with industry participants signaling adequate capacity and ongoing competition, which supports broader adoption among listed and private companies. The emergence of parametric structures for catastrophe risks, including regional facilities domiciled in Singapore, provides alternative protection options that reduce payout frictions and basis risk. These developments channel incremental growth to specialty across the Singapore property and casualty insurance market as corporate buyers seek limits and covers that traditional policies do not fully address.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Competition and Compressing Underwriting Margins | -0.9% | National, concentrated in mass retail lines | Short term (≤ 2 years) |

| Managing Heightened Catastrophe and Climate Risk Exposure | -1.2% | National with high-density property clusters | Medium term (2-4 years) |

| Capital and Compliance Burden Under RBC 2 and ORSA | -0.8% | National, all carriers | Short term (≤ 2 years) |

| M&A Scrutiny and Foreign Deal Uncertainty | -0.7% | National, inbound investors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition and Compressing Underwriting Margins

Profitability came under pressure in 2024, as domestic underwriting profit fell 16.7% to USD 170.54 million (SGD 219.04 million) even though gross written premiums rose 8.3%, highlighting a more competitive rate environment[3]SEADRIF, “Driving Climate Resilience Through Innovation,” SEADRIF, seadrif.org. Motor insurance posted an underwriting loss in 2024, reflecting claims severity and cost inflation that outpaced rate actions and underscored sensitivity to repair and parts trends. The shift in Singapore’s new-vehicle mix has implications for risk costs, with electric vehicles carrying higher repair complexity, which translates into higher premiums and tighter underwriting windows in motor insurance. Digitalization in claims and reporting curbs fraud and leakage, yet the same transparency heightens price comparisons and accelerates switching behavior in retail lines. These dynamics make measured growth and expense efficiency essential for sustainable returns in the Singapore property and casualty insurance market.

Managing Heightened Catastrophe and Climate Risk Exposure

Property segment net incurred claims increased 53.2% in 2024, with electrical fires up 8.3% and Active Mobility Device incidents up 25.7%, which raised the loss burden in dense residential clusters. Climate trends pose compounding risks, with Asia warming faster than the global average, elevating weather-related exposures in coastal and high-density urban zones relevant to Singapore[4]General Insurance Association of Singapore, “GIA Annual Report 2024,” GIA, gia.org.sg. Specialty marine lines experienced a tougher year in 2024, with marine hull premiums contracting 17.0%, reflecting broader volatility in shipping risk. Regulatory work on capital adequacy and catastrophe modeling remains a focal point to ensure insurers hold adequate buffers against correlated loss scenarios. Together, these factors make exposure management and reinsurance strategy central to the Singapore property and casualty insurance market.

Segment Analysis

By Line of Business: Specialty Lines Gain Momentum as Motor Dominance Persists

Motor commanded 47.9% of the Singapore property and casualty insurance market share in 2025, preserving its position as the largest line even as underwriting results softened in 2024. The segment’s profitability dipped due to higher claims severity, while the rate environment stayed competitive, which prompted underwriters to calibrate pricing and benefits more tightly. Health, property, and liability lines showed varied drivers, with property claims volatility in 2024 and liability steady demand from employers and commercial activity. Health-related cover continues to be shaped by system-wide cost management measures and household adoption of complementary protection, indicated by strong life-sector new business in 2025. Collectively, these patterns keep the Singapore property and casualty insurance market anchored by motor and supported by selective growth in other retail lines.

Other insurance, which includes cyber, engineering, surety, credit, and specialty liability, is projected to expand at an 8.95% CAGR within the Singapore property and casualty insurance market size between 2026 and 2031, setting the pace for the fastest growth across lines. Specialty momentum is supported by the city’s risk hub role and access to reinsurance and alternative structures demonstrated through regional risk pooling activity. Travel insurance logged a 2024 upswing in gross premiums alongside higher claims, reflecting normalization of mobility and evolving consumer protections. Marine hull experienced a difficult 2024 with a swing into underwriting loss, reinforcing the need for disciplined capacity and better risk differentiation. Going forward, specialty lines are positioned to absorb a meaningful share of incremental premium as corporates recalibrate risk budgets and seek bespoke limits, which supports diversification in the Singapore property and casualty insurance market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Customer Type: Corporate Segment Accelerates as SME Coverage Deepens

The corporate segment held 56.5% of the Singapore property and casualty insurance market share in 2025 and is projected to grow faster than retail through 2031, supported by demand for liability, property, and specialty covers. Larger firms and mid-market enterprises pursue coverage for cyber events, directors’ liabilities, and engineering risks as operational exposure becomes more technology-centric and compliance standards rise. Singapore’s position in logistics and trade routes adds to commercial lines depth, including marine and transit, which broadens the base of corporate policyholders across sectors. This trajectory aligns with the long-term opportunities in infrastructure, shipping, and services that concentrate in Singapore’s economy and the broader region.

The corporate portion of the Singapore property and casualty insurance market size is forecast to expand at a 10.40% CAGR to 2031 as risk financing becomes more sophisticated and coverage needs diversify. The strong pipeline of corporate risk appetite is complemented by evolving regulatory expectations on technology and governance, which encourage structured risk transfer. Retail demand remains supported by compulsory schemes for home and mortgage-linked exposures that ensure baseline protection across households. Amendments to the Home Protection Scheme in 2025 enhanced inclusion for members with certain pre-existing conditions, further stabilizing the retail pool while maintaining pricing discipline. Overall, corporate growth and retail stability together underpin a balanced demand outlook within the Singapore property and casualty insurance market.

By Distribution Channel: Bancassurance Dominates Yet Broker-Aggregator Models Gain Share

Banks accounted for a 56.7% share of gross written premiums in 2025, reflecting the sustained strength of bancassurance linkages and integration within broader wealth and lending journeys. Long-standing, multi-market alliances demonstrate the endurance of bank-insurer models, with high-volume cross-sell and enterprise-level coordination across products and client segments. As consumer engagement shifts to mobile banking, banks emphasize data-driven onboarding and claims support to preserve channel productivity. The Singapore property and casualty insurance market benefits from this high-touch, high-trust distribution mode that aligns with broader household financial planning.

Brokers and agents are projected to grow at a 7.65% CAGR within the Singapore property and casualty insurance market size to 2031, buoyed by digital intermediary portals and streamlined back-office flows. New portals launched by leading local players in 2025 improve turnarounds and reduce manual friction, which helps intermediaries remain competitive on service while competing on price transparency. Industry infrastructure has also advanced, including digital accident reporting and history checks that mitigate fraud risk and support fair pricing. The direct channel remains a complementary route, especially in commoditized covers, but intermediated advice continues to matter as coverage becomes more specialized in the Singapore property and casualty insurance market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Singapore is the sole geography covered for sizing and forecasts, and its domestic dynamics are shaped by a compact, high-density urban environment with concentrated residential and commercial exposures. The offshore dimension adds depth to the ecosystem, with offshore insurance funds contributing USD 4.03 billion (SGD 5.18 billion) of gross written premiums in 2024, while offshore property insurance totaled USD 2.39 billion (SGD 3.08 billion), reinforcing Singapore’s position as a risk hub. Marine specialization enhances the city-state’s profile, with a top-tier regional ranking in hull underwriting and a concentration of carriers and brokers that attract complex cases into Singapore placement markets. These elements together help the Singapore property and casualty insurance market draw in risks beyond its physical borders while maintaining a domestic core that is shaped by compulsory schemes and dense property clusters.

Market growth moderates from historical highs as the domestic base matures, yet the regional hub role offsets scale constraints by deepening specialty and reinsurance flows tied to trade, logistics, and infrastructure. Regional risk pooling and parametric solutions, demonstrated by fast payouts to ASEAN member states during 2025 events, confirm that Singapore-based platforms can deliver efficient protection beyond national risks. The regulatory regime underpins this role by offering clarity on capital and governance for insurers and reinsurers that domicile and transact in Singapore. The balance of domestic and regional business gives the Singapore property and casualty insurance market a diversified growth profile, even as it aligns with prudent underwriting and capital management.

Heightened fire and mobility-device incidents in 2024 lifted property claims in dense housing estates, a reminder of correlated risks in urban clusters that require careful pricing and prevention. Compulsory structural fire protection for HDB flat owners with HDB loans ensures baseline cover, while private policies extend to contents and renovations. Mortgage-linked protection through CPF also reduces household vulnerability to income shocks, and the 2025 HPS amendment broadened inclusion for members with certain pre-existing conditions. Climate trends heighten the importance of catastrophe modeling and capital buffers, reinforcing the prudential focus of the MAS framework that guides domestic and offshore risk-taking.

Competitive Landscape

Competition in the Singapore property and casualty insurance market reflects both scale and specialization, with many licensed insurers and registered brokers participating across consumer and commercial lines. Regulatory scrutiny over ownership and control is high, as shown by the Insurance (Amendment) Act 2024 framework that enabled ministerial intervention in transactions on public interest grounds. The MAS solvency regime also raises the bar on capital quality, which encourages prudent expansion and measured product launches by carriers competing on underwriting and service rather than pure price. GIA initiatives on data and claims reporting improve operational reliability, reduce fraud exposure, and narrow information asymmetry, which helps the market function more efficiently at scale. These conditions together favor players with strong risk selection, digital claims, and robust governance, while leaving room for niche specialists to differentiate in the Singapore property and casualty insurance market.

Strategic moves by leading firms in 2025 focus on digital acceleration and segment-specific propositions. A notable local player announced a significant investment plan to scale technology and talent, launched a digital intermediary portal, and digitized end-to-end journeys for selected retail products with broader rollouts planned. Bank-led distribution remains resilient, underpinned by long-running cross-border partnerships that continue to deliver new business through integrated wealth channels. The national association’s digital claims initiatives, including accident report pre-fill and history services, further standardize workflows that lower costs and support faster settlement. The Singapore property and casualty insurance market is therefore seeing competition shift toward experience and efficiency while capacity and capital guardrails remain central.

Capacity for specialty risks continues to organize around Singapore’s hub. Regional risk pooling demonstrated reliable disbursements in 2025, which builds confidence among corporate buyers in alternative and parametric structures. Life sector momentum in 2025 signals household protection engagement that often complements non-life covers, which sustains distribution productivity across bancassurance and intermediated channels. The broader regulatory environment continues to evolve on technology governance and operational resilience, which influences how carriers deploy data and automation in underwriting and claims. Against this backdrop, the Singapore property and casualty insurance market rewards firms that can combine risk expertise, digital scale, and channel partnerships to defend margins and grow selectively.

Singapore Property And Casualty Insurance Industry Leaders

AXA Singapore

Chubb Singapore

NTUC Income

MSIG Insurance (Singapore) Pte Ltd

AIG Asia Pacific Insurance Pte Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: MAS issued Circular ID 01/26, reminding insurers of Own Risk and Solvency Assessment expectations under MAS Notice 126, reinforcing supervisory intensity following 2025 submissions.

- April 2025: United Overseas Insurance unveiled a strategy to increase technology investments and talent, launched a digital intermediary portal, and digitized motor and travel journeys, with plans to extend digitization across all products by 2026.

- January 2025: Maybank’s insurance arm, Etiqa Insurance, introduced Invest future, a Shariah-compliant Takaful investment-linked plan distributed exclusively through Maybank Singapore

- August 2024: The General Insurance Association launched Myinfo Reporting under the Easy Accident Reporting System to enable online pre-fill for motor accident reports via Singpass, reducing manual errors and fraud risk.

Singapore Property And Casualty Insurance Market Report Scope

Property and Casualty Insurance is the type of coverage that protects the policyholder's property, such as home, car, and other belongings. It also includes liability coverage, which protects a person if found legally responsible for an accident that causes injuries to another person or damages to their property.

The Singapore Property and Casualty Insurance Market Report is Segmented by Line of Business (Motor Insurance, Health Insurance, Property Insurance, Liability Insurance, Other Insurance), Customer Type (Retail, Corporate), Distribution Channel (Brokers/Agents, Banks, Direct Sales, Other Channels), and Geography (Singapore). The Market Forecasts are Provided in Terms of Value (USD).

By Line of Business

| Motor Insurance |

| Health Insurance |

| Property Insurance |

| Liability Insurance |

| Other Insurance |

By Customer Type

| Retail |

| Corporate |

By Distribution Channel

| Brokers/Agents |

| Banks |

| Direct Sales |

| Other Channels |

| By Line of Business | Motor Insurance |

| Health Insurance | |

| Property Insurance | |

| Liability Insurance | |

| Other Insurance | |

| By Customer Type | Retail |

| Corporate | |

| By Distribution Channel | Brokers/Agents |

| Banks | |

| Direct Sales | |

| Other Channels |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the Singapore property and casualty insurance market?

The Singapore property and casualty insurance market size is USD 1.87 billion in 2026 and is projected to reach USD 2.47 billion by 2031 at a 5.78% CAGR.

Which lines contribute most to premiums in Singapore’s P&C space?

Motor remains the largest line, with a 47.9% share in 2025, while specialty categories grouped as “other insurance” are projected to grow the fastest to 2031.

How are banks and brokers positioned in Singapore’s non-life distribution?

Banks lead distribution with a 56.7% share in 2025, while brokers and agents are expected to grow at the fastest pace through 2031 due to the digitization of intermediary workflows.

What regulatory changes are most relevant to insurers in Singapore in 2026?

MAS’s RBC 2 enhancements, effective January 1, 2026, raise capital quality by limiting qualifying capital instruments to non-retail investors, reinforcing solvency resilience.

What risks weighed on Singapore’s P&C results in 2024?

Property claims rose sharply, and motor posted an underwriting loss, reflecting higher claims severity and incident patterns in dense urban settings.

How does Singapore’s hub role influence P&C growth?

Marine leadership, regional risk pooling, and a dense reinsurance ecosystem drive specialty demand and attract cross-border risk flows into Singapore.