Production Printer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

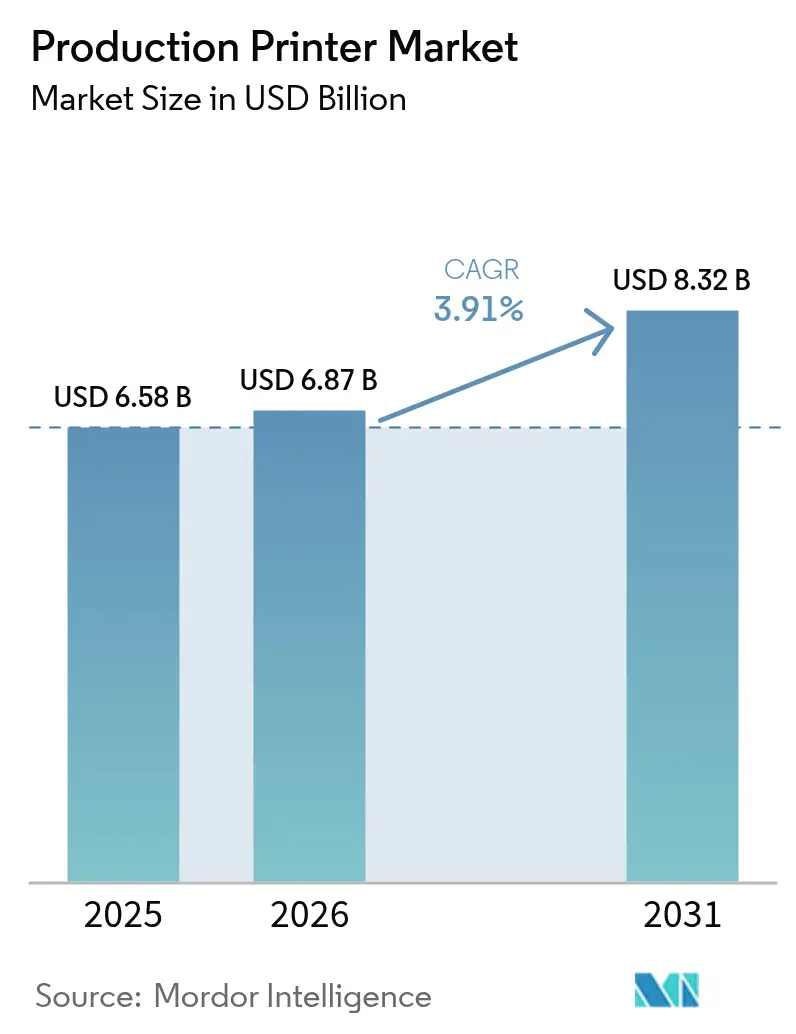

| Market Size (2026) | USD 6.87 Billion |

| Market Size (2031) | USD 8.32 Billion |

| Growth Rate (2026 - 2031) | 3.91% CAGR |

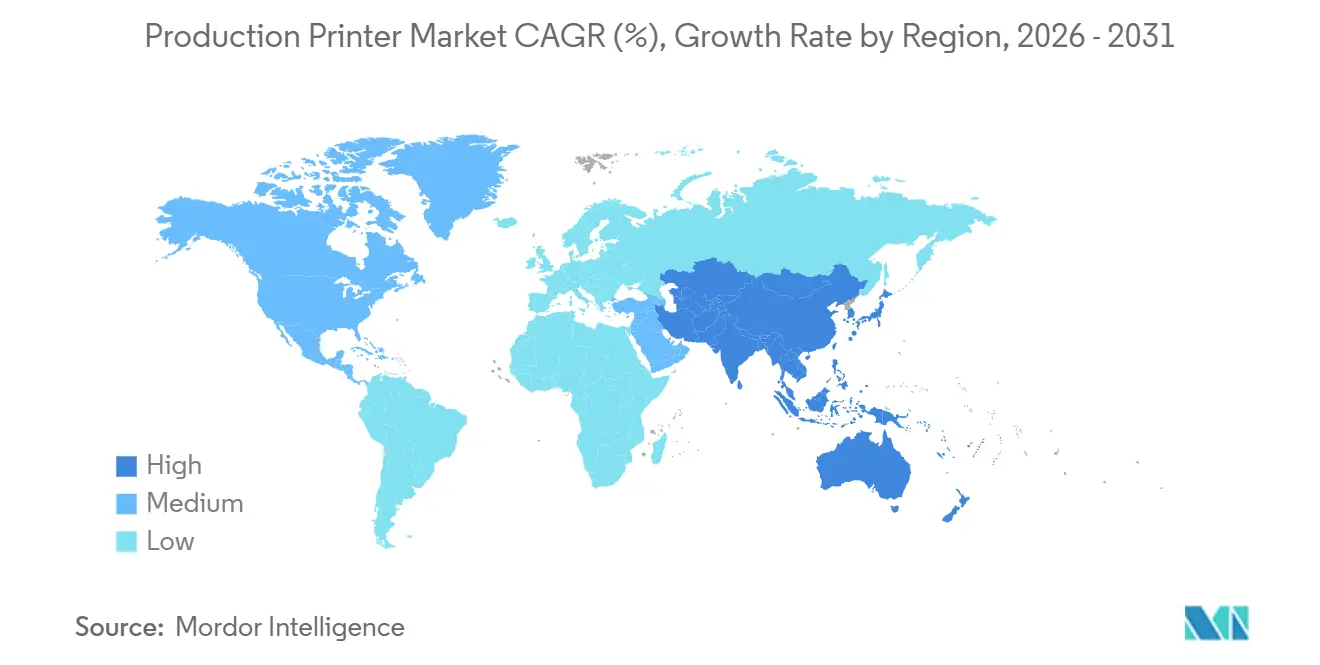

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Production Printer Market Analysis by Mordor Intelligence

The production printer market size is projected to expand from USD 6.58 billion in 2025 and USD 6.87 billion in 2026 to USD 8.32 billion by 2031, registering a 3.91% CAGR between 2026 and 2031. A shift away from legacy publishing and transactional mail toward packaging, labels, and on-demand commercial work is reshaping profit pools, with digital workflows enabling mass customization that offsets falling volumes in traditional segments. Brand owners are adopting variable-data workflows to launch limited-edition stock-keeping units, comply with complex labeling regulations, and manage shorter order cycles, all of which favor digitally driven presses over analog equipment. Capital spending is gradually recovering as semiconductor supply chains normalize, reducing the delivery lead times that constrained high-speed inkjet installations through mid-2024. Competitive intensity is increasing, yet service-contract economics and outcome-based pricing models are helping vendors defend margins even as equipment list prices come under pressure from low-cost Asian entrants.

Key Report Takeaways

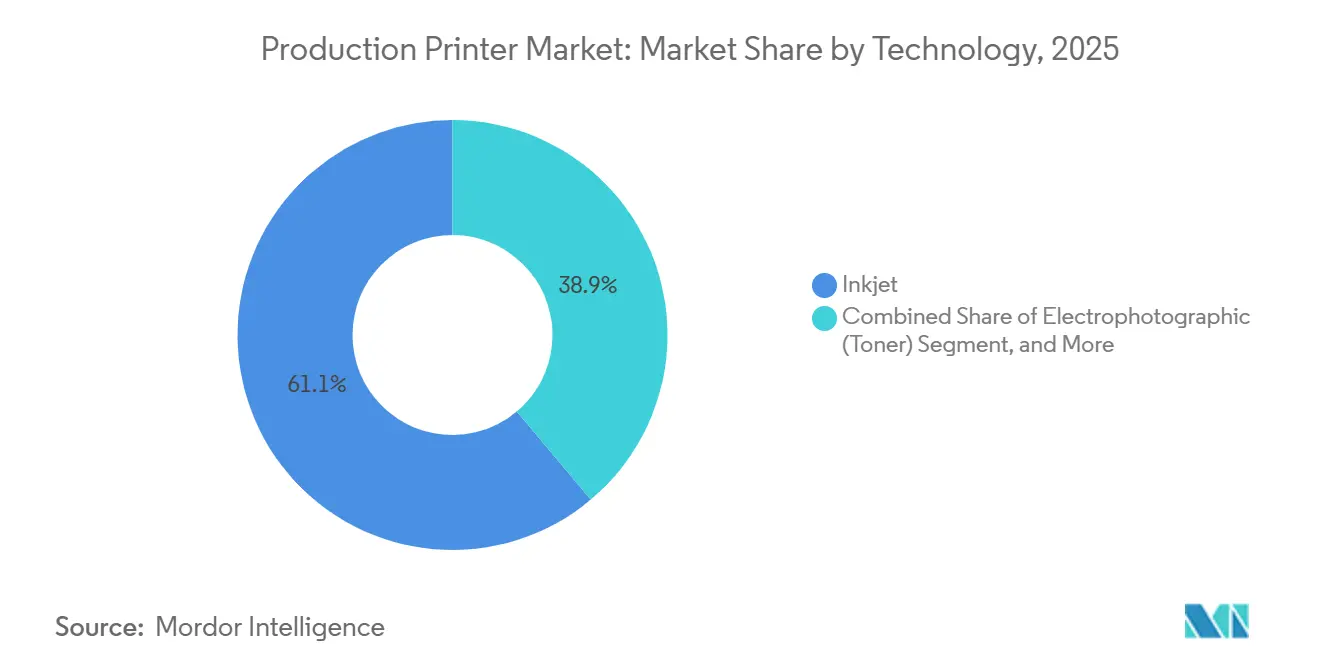

- By technology, inkjet captured 61.12% of 2025 revenue while electrophotographic platforms trailed at 38.88%.

- By production method, continuous-feed systems led with 57.12% of 2025 revenue, but cut-sheet platforms are advancing at a 4.31% CAGR through 2031.

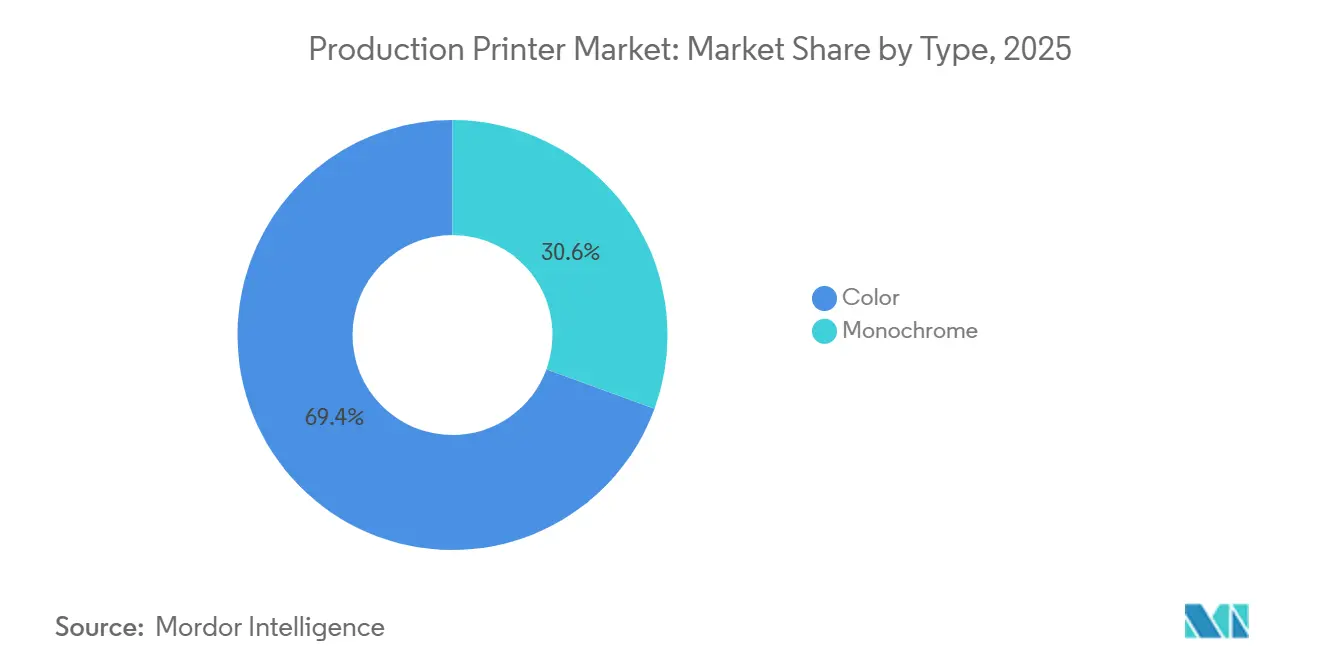

- By type, color printers commanded 69.42% of 2025 revenue; monochrome units constituted the remaining share.

- By application, packaging represented 26.23% of 2025 revenue and is projected to grow at a 4.88% CAGR to 2031.

- By geography, Asia-Pacific held 35.32% of 2025 revenue and will expand at a 4.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Production Printer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Printing Applications in Packaging | +1.8% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Short-Run, On-Demand Print Requirements | +1.2% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Advances in High-Speed Inkjet Technology | +1.0% | Global | Medium term (2-4 years) |

| Industrial-Grade Metallic and Functional Ink Demand | +0.6% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Digital Textile Microfactory Adoption | +0.4% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| AI-Driven Predictive Maintenance Reducing Downtime | +0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth Of Printing Applications In Packaging

Digital presses are penetrating flexible film, corrugated, and folding-carton lines as converters eliminate minimum order constraints that once favored long-run analog workflows. Ongoing European Union rules mandating recyclable mono-material structures by 2030 accelerate the shift toward water-based inkjet, especially for polyethylene and polypropylene films.[1]“Packaging and Packaging Waste Regulation,” European Commission, EC.EUROPA.EU Press makers that can certify food-contact inks and achieve color-consistency within Delta E 2.0 have become preferred suppliers, particularly in Germany and Italy where brand owners demand uniform shelf impact.[2]“The Future of Digital Printing to 2029,” Smithers, SMITHERS.COM Early adopters report material cost savings of up to 15% thanks to single-layer barrier coatings that replace multi-layer laminates.

Short-Run, On-Demand Print Requirements

Commercial printers now generate more than half of revenue from jobs under 5,000 impressions, a segment that has grown rapidly as retailers localize promotions and pharmaceutical firms comply with serialization codes. Cut-sheet inkjet platforms deliver profitable runs below 1,000 impressions because changeovers can occur in under 10 minutes, far quicker than continuous-feed setups. Faster turnaround raises margins despite smaller volumes, and premium pricing is attainable when 48-hour delivery is contractually guaranteed.

Advances In High-Speed Inkjet Technology

Throughput above 150 meters per minute on corrugated board and label stock has narrowed the historical cost gap with electrophotographic systems. Fujifilm’s J Press 750S demonstrated 1,200 dpi resolution on 3 mm substrates without offline priming, signaling that substrate versatility no longer requires productivity trade-offs.[3]“J Press 750S High-Speed Inkjet System,” Fujifilm Holdings, FUJIFILM.COM Recirculating printheads with piezoelectric actuators have extended maintenance windows to 18 months, cutting lifetime service spend by as much as 15%.

AI-Driven Predictive Maintenance

IoT sensors and machine-learning models flag nozzle misfires or color drift before visible defects occur, reducing emergency stoppages by roughly one-third. Heidelberg’s subscription program deploys remote diagnostics so parts arrive ahead of planned downtime, trimming mean time to repair from 8 hours to 2.5 hours. Vendors increasingly bundle analytics software with consumables, binding press uptime to service-contract revenue and strengthening customer lock-in.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to Digital Marketing and E-Reading | -1.5% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| High Capital Expenditure of Production Printers | -1.1% | Global, acute in South America and Africa | Medium term (2-4 years) |

| Semiconductor Supply-Chain Volatility | -0.5% | Global | Short term (≤ 2 years) |

| Regulatory Push for PFAS-Free Ink Formulations Raising R and D Costs | -0.6% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift To Digital Marketing And E-Reading

Programmatic advertising continues to capture budget share, cutting direct-mail volumes that once filled continuous-feed webs. E-book penetration above one-third of U.S. trade-book sales further compresses short-run publishing demand. While packaging and labels remain insulated, commercial printers must compete aggressively on the remaining work, and average operating margins have slid several points since 2020.

High Capital Expenditure Of Production Printers

Entry-level inkjet lines cost between USD 500,000 and USD 1.2 million, a hurdle for small operators in South America and Africa, where currency depreciation inflates effective prices. Proprietary inks represent nearly half of lifetime press spend, locking owners into vendor ecosystems. Leasing eases upfront cash needs yet lengthens payback periods and raises obsolescence risk as newer, faster models emerge every 24-30 months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Brand Differentiation Drives Color Dominance

Color devices generated 69.42% of 2025 revenue, and their share of the production printer market size is forecast to climb on a 4.28% CAGR through 2031. Brand owners willingly pay premiums for metallic finishes and precise spot-color matching that protect shelf identity across global supply chains. Metallic and functional inks, now printable on standard piezo heads, extend addressable applications from luxury spirits labels to RFID antennas.

Monochrome engines, with 30.58% revenue, persist in transactional mail and book interiors where cost-per-page below USD 0.01 outweighs color requirements. Even those niches are eroding as statements migrate online and publishers pivot to color-capable platforms that handle both text blocks and cover art without dual workflows. As inkjet consumable costs continue to fall, many commercial printers retire black-only fleets and route simple text work to color presses during off-peak shifts to maximize asset utilization.

By Production Method: Workflow Flexibility Favors Cut Sheet

Continuous-feed lines retained 57.12% of 2025 revenue, dominating jobs above 50,000 impressions thanks to low running costs per page and integrated finishing. Yet changeover complexity, multihour setup windows, and dedicated operators limit their suitability for today’s shorter orders. Cut-sheet lines, projected to outpace market growth at a 4.31% CAGR, have become the default choice for fast-turn commercial and packaging work below 5,000 impressions. They switch substrates in minutes, accept mixed media within a shift, and pair with inline die-cutting or lamination units to eliminate off-press handling.

Asset flexibility is particularly attractive to converters serving consumer goods brands that launch dozens of regional variants each year. These converters build schedules around multiple customers per day, a pattern incompatible with the continuous-feed economies of scale that presuppose multi-hour single-customer blocks. As postal regulators tighten automation-rate barcode rules, cut-sheet platforms capable of merging variable databases in line are winning direct-mail placements in the United States.

By Technology: Inkjet Captures Share Through Lower TCO

Inkjet systems accounted for 61.12% of 2025 sales, and their stake in the production printer market share is expanding by 4.47% annually to 2031. Water-based pigment chemistries now achieve Blue Wool ratings of 7-8, meeting long-term lightfastness targets while sidestepping the energy draw of UV curing. Electrophotography still leads pharmaceutical and secure-document niches, yet its higher consumable costs are eroding competitiveness in general commercial work.

Beyond consumables, inkjet’s substrate range unlocks corrugated, flexible film, and textured stocks that fuser rollers cannot handle. Screen’s Truepress Jet520HD NX demonstrates corrugated speeds of 150 m/min on 3 mm board, allowing converters to retire analog lines and reclaim up to 40% of floor space. Hybrid and nanography platforms remain niche, serving applications where extremely wide gamuts or minimal energy use trump capital costs.

By Application: Regulatory Tailwinds Propel Packaging Growth

Packaging represented 26.23% of 2025 turnover, the fastest-growing slice of the production printer market, with a 4.88% CAGR to 2031. Extended producer responsibility and mono-material recycling rules in the European Union reward converters that adopt food-safe, water-based inks compatible with polyethylene and polypropylene films. Commercial printing still contributes the largest absolute dollars but endures volume pressure as corporate communications migrate online.

Transactional mail volumes continue to slide as banks and utilities promote digital statements, whereas healthcare and legal mandates for audit-trail hard copies provide a partial offset. Niche growth avenues including textile microfactories and printed electronics are small today but tap the same drop-on-demand architectures as packaging inkjet, giving press makers a roadmap to diversify consumable streams without broad hardware redesign.

Geography Analysis

Asia-Pacific anchored 35.32% of 2025 revenue, and its contribution to the production printer market size is set to widen by a 4.93% CAGR through 2031. China’s USD 180 billion packaging sector is consolidating as regulators shutter solvent-based flexographic sites, prompting converters to fast-track inkjet installations that reduce water usage by 70-80%. India’s corrugated segment, posting double-digit growth, is likewise embracing digital workflows to serve e-commerce fulfillment that demands variable regional graphics. Vietnam’s label clusters ride supply-chain diversification, with multinational consumer-goods companies commissioning just-in-time runs near final assembly nodes.

North America ranks second in market size but faces structural volume erosion in direct mail and publishing as digital advertising and e-reading broaden reach. Packaging growth in food, beverage, and personal-care channels partially offsets those declines, and converters continue to invest in high-speed inkjet to comply with evolving state recycling mandates. The United States Postal Service’s barcode incentives further spur adoption of cut-sheet variable-data presses for targeted mailings.

Europe holds the third-largest slice of the production printer market. Adoption is driven by regulations targeting PFAS chemicals, compelling ink formulators to retool pigment dispersions and delaying press launches by up to one year in some cases. South America, the Middle East, and Africa collectively remain below one-quarter of worldwide revenue. Currency volatility and limited vendor financing lengthen capital payback, slowing equipment turnover, although regional packaging opportunities encourage gradual upgrades.

Competitive Landscape

The production printer market is moderately concentrated, with Xerox, HP, Canon, Ricoh, and Konica Minolta capturing 45% of 2025 revenue. Vendors compete on life-cycle cost rather than sticker price, bundling predictive maintenance, cloud workflow automation, and consumables in outcome-based contracts that generate up to 70% of lifetime value. Chinese manufacturers such as Founder and Tongfang price cut-sheet units 30-40% lower than incumbents, pressuring established players to guarantee uptime and Delta E color tolerances that new entrants struggle to match.

Screen Holdings and Fujifilm dominate the nascent high-speed packaging inkjet niche, where throughput above 150 m/min and compatibility with corrugated and flexible films raise barriers to entry. Heidelberg’s subscription model signals industry migration away from capex sales toward usage-based billing, aligning vendor revenue with customer uptime and lowering balance-sheet hurdles for printers wary of multi-million-dollar purchases.

Regulatory compliance is emerging as a competitive differentiator. Vendors that achieve ISO 12647 certification and validate PFAS-free inks gain preferred-supplier status with multinational consumer-goods firms navigating strict European packaging rules. Functional inks for printed electronics present white-space growth, leveraging existing CMYK jetting architectures to serve RFID, sensor, and display applications without major hardware redesigns.

Production Printer Industry Leaders

Xerox Holdings Corporation

HP Inc.

Canon Inc.

Ricoh Company, Ltd.

Konica Minolta, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Eli Lilly announced plans to eliminate 90 billion paper medicine inserts annually by switching to digital leaflets, aligning sustainability with patient accessibility.

- August 2025: Mimaki released the TS200-1600 dye-sublimation printer using water-based inks for textile and packaging applications.

- August 2025: Epson launched SureColor P7370 and P9370 wide-format printers with cloud fleet management targeting the graphic design and photography segments.

- January 2025: HP announced a USD 150 million expansion of its PageWide press plant in Barcelona to meet demand for PFAS-compliant packaging systems.

Global Production Printer Market Report Scope

The production printer, also known as a production-level printing machine or high-speed output printer, is designed to produce large volumes for high-speed output. In commercial printing environments where documents, brochures, catalogs, flyers, and similar materials must be produced in large quantities, it is normally utilized by print companies, publishing establishments, or marketing agencies.

The Production Printer Market Report is Segmented by Type (Monochrome, Color), Production Method (Cut Sheet, Continuous Feed), Technology (Inkjet, Electrophotographic, Other Technologies), Application (Commercial Printing, Publishing, Packaging, Transactional and Direct Mail, Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Monochrome |

| Color |

| Cut Sheet |

| Continuous Feed |

| Inkjet |

| Electrophotographic (Toner) |

| Other Technologies |

| Commercial Printing |

| Publishing |

| Packaging |

| Transactional and Direct Mail |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Type | Monochrome | |

| Color | ||

| By Production Method | Cut Sheet | |

| Continuous Feed | ||

| By Technology | Inkjet | |

| Electrophotographic (Toner) | ||

| Other Technologies | ||

| By Application | Commercial Printing | |

| Publishing | ||

| Packaging | ||

| Transactional and Direct Mail | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the production printer market in 2031?

The market is forecast to reach USD 8.32 billion by 2031, expanding at a 3.91% CAGR from 2026.

Which technology currently leads sales?

Inkjet systems captured 61.12% of 2025 revenue, leading all other technologies.

Why are color presses gaining share?

Brand owners pay premiums for spot-color accuracy and metallic finishes that differentiate packaging, lifting color devices to 69.42% of 2025 revenue.

Which region is expected to grow the fastest?

Asia-Pacific will expand at a 4.93% CAGR through 2031, driven by packaging demand in China, India, and Vietnam.

How are vendors addressing downtime?

Predictive maintenance platforms use IoT data and analytics to cut unplanned stoppages by roughly one-third and align service revenue with press uptime.

What regulatory trend most benefits digital printing?

European mandates for recyclable mono-material packaging favor water-based inkjet inks and accelerate digital press adoption in flexible-film and corrugated segments.

Page last updated on: