Private Cloud Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

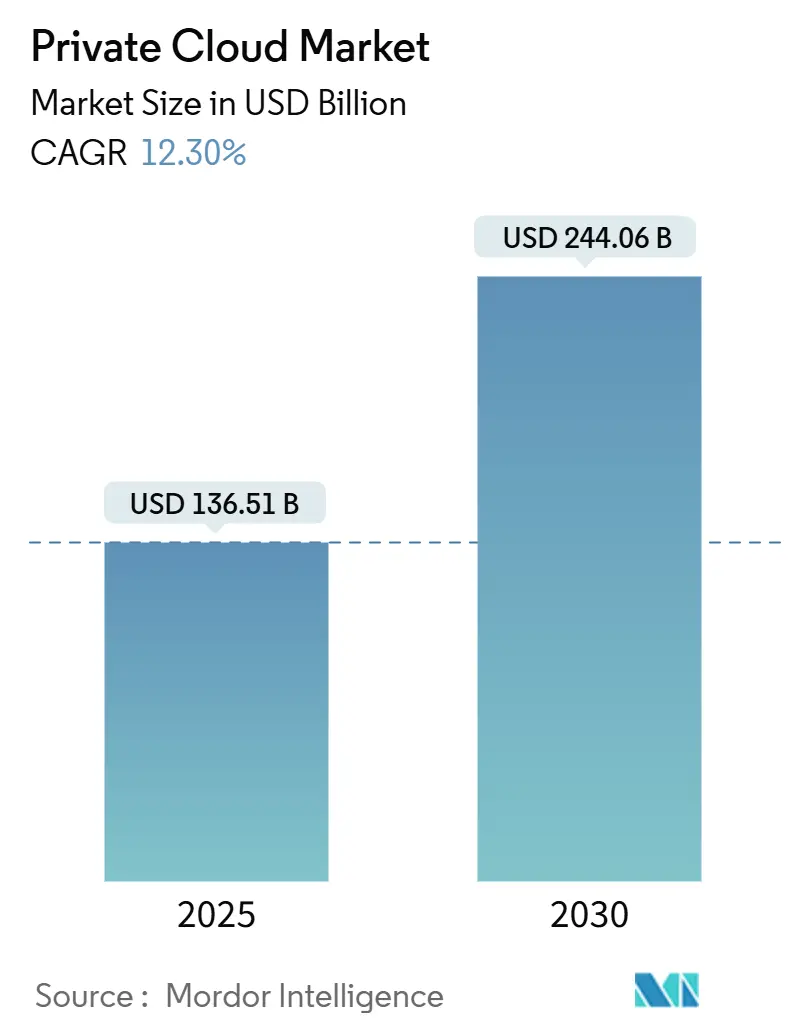

| Market Size (2025) | USD 136.51 Billion |

| Market Size (2030) | USD 244.06 Billion |

| Growth Rate (2025 - 2030) | 12.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Private Cloud Market Analysis by Mordor Intelligence

The private cloud market stands at USD 136.51 billion in 2025 and is forecast to reach USD 244.06 billion by 2030, advancing at a 12.30% CAGR. Adoption is accelerating as enterprises migrate AI workloads from public environments, comply with stricter data-sovereignty laws, and seek predictable infrastructure costs. Licensing upheavals after the Broadcom-VMware deal, which pushed prices up to six-times higher for some clients, have triggered rapid platform diversification. Infrastructure spending by hyperscalers and specialist providers already exceeds USD 150 billion, reflecting sustained demand for AI-ready capacity. Enterprises are also embracing managed private clouds that combine operational expertise with dedicated control, a trend reinforced by rising public-cloud egress fees and latency-sensitive Industry 4.0 deployments.

Key Report Takeaways

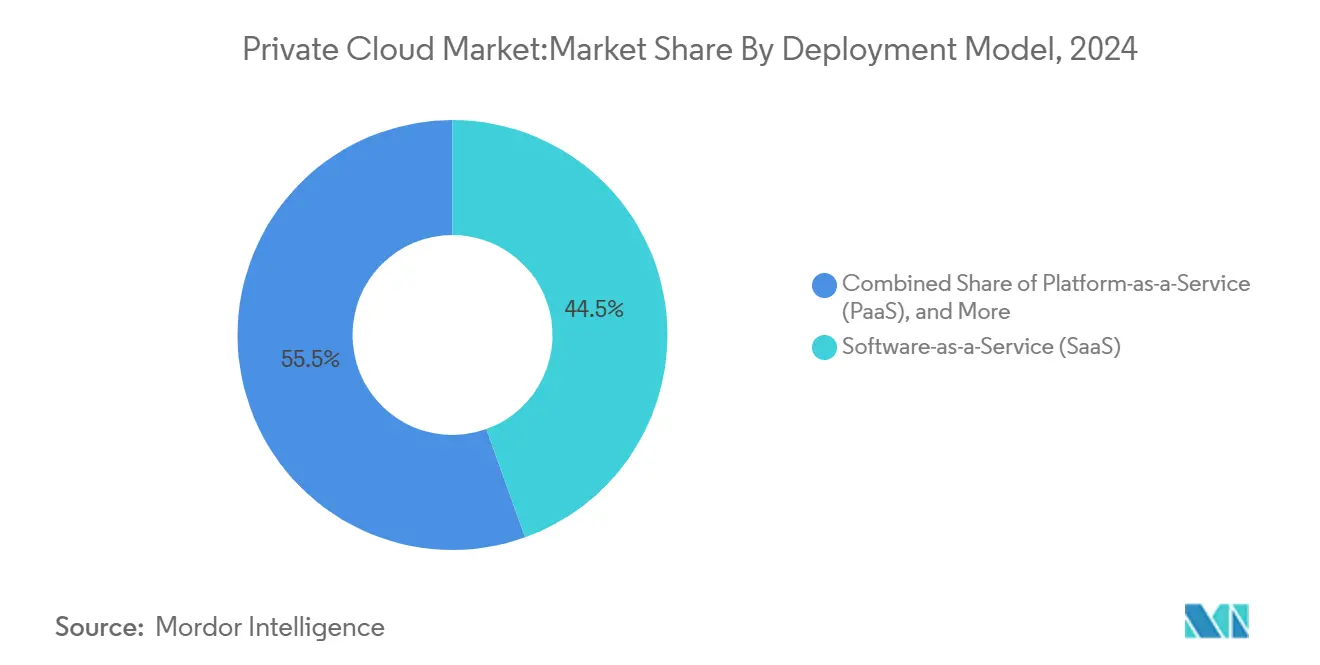

- By deployment model, Software-as-a-Service led with 44.50% of private cloud market share in 2024, while Services are on track for the fastest 13.90% CAGR through 2030.

- By end-user enterprise size, Large Enterprises held 60.50% of the private cloud market share in 2024; Small and Medium Enterprises are expanding at a 13.62% CAGR through 2030.

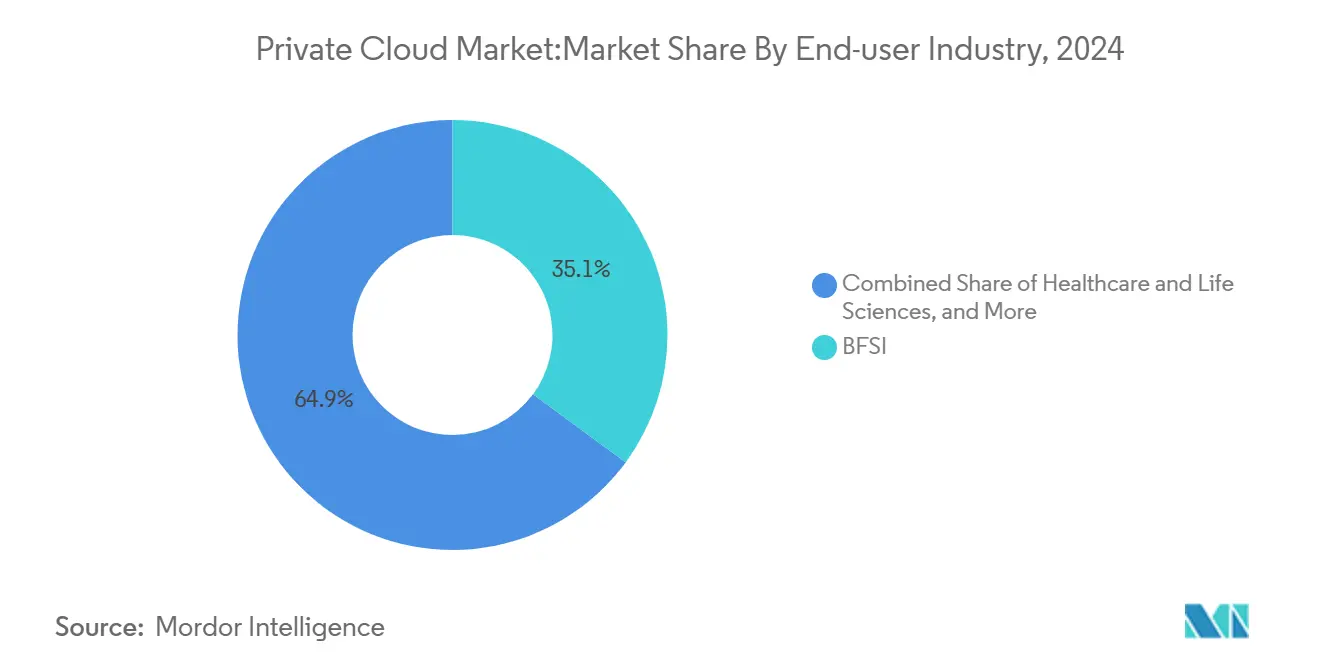

- By end-user industry, BFSI dominated with 35.10% revenue share in 2024; Healthcare is projected to grow at a 14.33% CAGR through 2030.

- By hosting type, On-premises Dedicated deployments accounted for 49.50% share of the private cloud market size in 2024, while Managed/Hosted solutions are advancing at a 13.80% CAGR through 2030.

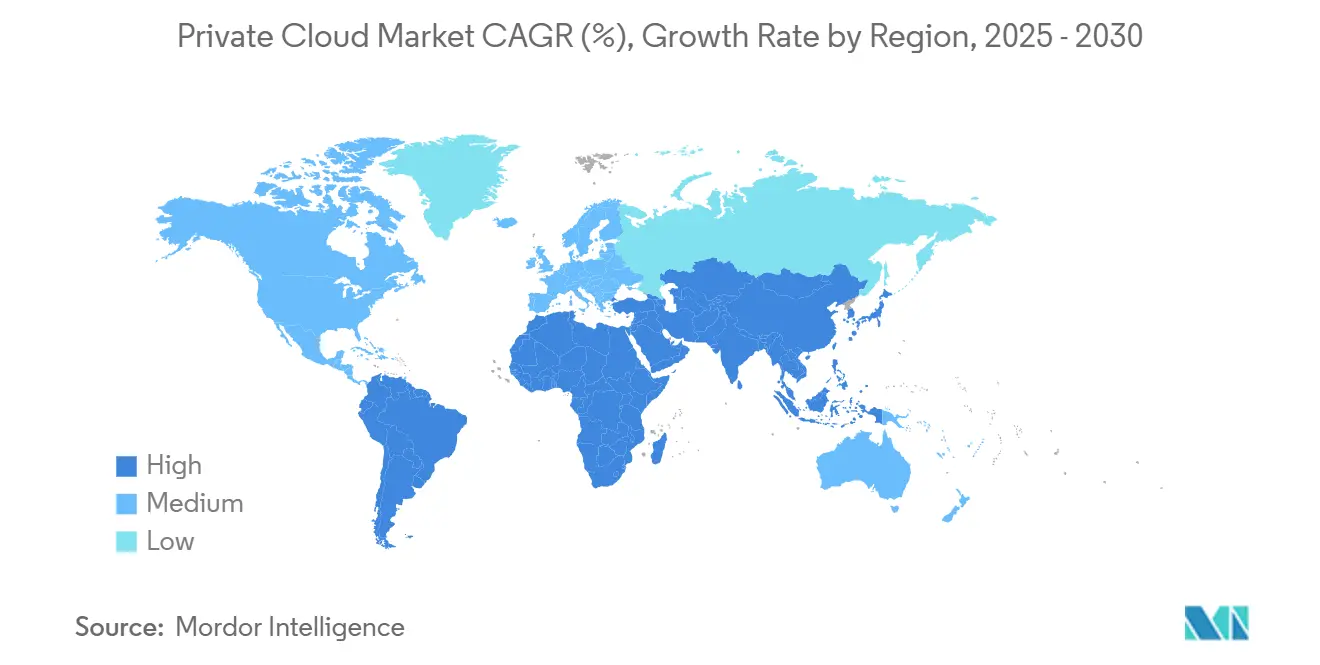

- By geography, North America retained 43.70% revenue share in 2024; Asia-Pacific is forecast to deliver the highest 16.45% CAGR through 2030.

Global Private Cloud Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating AI/Gen-AI workload repatriation to private clouds | +2.8% | North America, Europe, global corporations | Medium term (2-4 years) |

| Mandatory data-sovereignty rules (e.g., China, GCC, EU) | +2.1% | Asia-Pacific, European Union, Middle East | Long term (≥ 4 years) |

| Edge-to-core latency reduction needs in Industry 4.0 plants | +1.9% | Global manufacturing hubs in Asia-Pacific and North America | Medium term (2-4 years) |

| Cost-predictability versus escalating public-cloud egress fees | +1.7% | North America and Europe | Short term (≤ 2 years) |

| Kubernetes-native private PaaS bundles from server OEMs | +1.4% | Early adopters in North America | Medium term (2-4 years) |

| Telco 5G slicing driving on-prem hosted private-cloud demand | +1.2% | North America and Asia-Pacific telecom sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating AI/Gen-AI workload repatriation to private clouds

More than half of global IT leaders now default new AI projects to private infrastructure because data privacy and predictable performance outweigh public-cloud convenience. Broadcom reports that 69% of enterprises are actively pulling workloads back on-prem, noting cost reductions of up to 80% for intensive AI training tasks. Repatriation momentum is reinforced by licensing changes that penalize variable usage, motivating IT teams to consolidate compute in owned or hosted facilities where capacity can be right-sized.

Mandatory data-sovereignty rules

Regulators in the European Union, China, and Gulf Cooperation Council states now oblige companies in regulated sectors to store and process sensitive data within defined borders. China’s cross-border data flow regulation effective March 2024 and the EU’s Digital Operational Resilience Act create permanent demand for sovereign private clouds that guarantee jurisdictional control [1]European Commission, “Digital Operational Resilience Act,” ec.europa.eu. Enterprises therefore deploy region-specific instances to stay compliant across multiple legal regimes.

Edge-to-core latency reduction needs in Industry 4.0 plants

Industrial transformation programs require round-trip latencies below 5 ms between machinery and analytics engines. Ericsson found that private 5G paired with on-prem cloud improved real-time decision cycles at Toyota Material Handling and CJ Logistics by double-digit productivity margins. Partnerships, such as Verizon’s integration of NVIDIA GPUs with Mobile Edge Compute, knit together edge and core resources for factory AI, making local private cloud indispensable.

Cost-predictability versus escalating public-cloud egress fees

More than 90% of IT leaders identify preventable spending spikes in multi-cloud bills, with egress fees cited as a top reason. By relocating steady-state and data-intensive workloads to private clouds, finance teams regain budget certainty and can lock in three- to five-year depreciation cycles instead of facing fluctuating monthly invoices.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of multi-cloud FinOps and SRE talent | -1.8% | North America, Europe | Short term (≤ 2 years) |

| Rising software subscription costs post Broadcom-VMware | -1.5% | North America, Europe | Short term (≤ 2 years) |

| Vendor lock-in from single-stack appliances | -0.9% | Global | Medium term (2-4 years) |

| Complex overlap of PCI-DSS, HIPAA, GDPR | -0.7% | Highly regulated industries everywhere | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of multi-cloud FinOps and SRE talent

Organizations struggle to hire professionals who can optimize cost and reliability across hybrid estates. Nearly one-third of firms missed 2024 financial objectives due to cloud skills gaps [2]SoftwareOne, “Cloud Skills Report 2024,” softwareone.com. Resulting wage inflation and outsourcing fees lengthen ROI horizons and slow rollout schedules.

Rising software subscription costs after Broadcom-VMware deal

VMware customers now face minimum 72-core subscriptions instead of 16, plus a move from perpetual to annual billing. Some small firms report ten-fold cost jumps that delay or cancel refresh plans. The upheaval distorts expenditure forecasts, suppressing short-term upgrades while enterprises evaluate alternative hypervisors.

Segment Analysis

By Deployment Model: Services segment drives platform evolution

The Services category is expanding at a 13.90% CAGR, outperforming the broader private cloud market as firms outsource day-to-day operations to experts. Software-as-a-Service still delivered 44.50% revenue share in 2024, but buyers now expect bundled consulting, automation, and lifecycle management. Platform-as-a-Service adoption accelerates via Kubernetes-native suites such as Red Hat OpenShift, chosen by T-Mobile for a unified telco cloud. Infrastructure-as-a-Service continues to underpin legacy workloads yet is increasingly packaged with deployment toolchains.

Comprehensive services reduce complexity and lower the learning curve for AI-heavy environments. Kyndryl’s AI Private Cloud consulting practice illustrates demand for design-through-MLOps assistance. HPE’s Private Cloud Business Edition promises a 90% drop in VM license cost by decoupling hypervisors from hardware, underscoring how integrated offerings now deliver measurable TCO advantages.

Note: Segment shares of all individual segments available upon report purchase

By End-user Enterprise Size: SME adoption accelerates through simplified platforms

Large Enterprises captured 60.50% private cloud market share in 2024, leveraging scale to modernize data centers for AI training. Dell recorded USD 12.1 billion in AI-system orders in Q1 2025, led by Fortune 500 customers [3]Dell Technologies, “Q1 2025 Earnings Call Transcript,” dell.com. Yet Small and Medium Enterprises post the fastest 13.62% CAGR as turnkey solutions remove barriers. The private cloud market size for SMEs is projected to expand by double digits between 2025 and 2030.

SMEs reacted sharply to VMware price hikes, pivoting to Nutanix or Hyper-V alternatives and embracing managed service bundles that consolidate backup and disaster recovery. Hivelocity’s VMware-powered private cloud shows how providers offer enterprise-grade uptime without requiring deep in-house skills. Generative-AI assistants like Red Hat’s Lightspeed further streamline daily administration, letting lean IT teams control sophisticated clusters.

By End-user Industry: Healthcare compliance drives fastest growth

BFSI retained 35.10% revenue share in 2024 through stringent risk controls and core-banking modernizations. Healthcare, however, grows at 14.33% CAGR as HIPAA mandates encryption, auditing, and access segregation that suit private environments. The private cloud market size for Healthcare workloads is projected to scale rapidly through 2030. Solutions such as ClearDATA Automated Safeguards keep Kubernetes clusters compliant, enabling hospitals to deploy AI diagnostics while preventing data leakage.

Industry 4.0 manufacturing, public sector sovereign clouds, and telco 5G core functions also favor private architectures. TCS generated USD 2.6 billion in FY 2025 from India sovereign cloud projects. Retailers protect customer data against breach fines while mining real-time analytics onsite. Each vertical reflects unique regulatory and operational pressures that elevate the value proposition of dedicated infrastructure.

Note: Segment shares of all individual segments available upon report purchase

By Hosting Type: Managed services gain momentum

On-premises Dedicated deployments still delivered 49.50% revenue share in 2024. Even so, Managed/Hosted private clouds are growing 13.80% annually, signalling that control and convenience are no longer mutually exclusive. CME Group’s joint private region with Google Cloud combines sub-one-millisecond networking with cloud-native operations for electronic trading.

Investment flows confirm the trend. Vantage Data Centers secured USD 9.2 billion in new equity to build AI-optimized campuses, designed for managed private cloud tenants. Virtual private clouds remain important for enterprises that need isolated environments within shared facilities. Overall, host decisions now revolve around service scope and performance SLAs rather than simple physical location.

Geography Analysis

North America commands 43.70% of 2024 revenue, propelled by well-funded AI programs, regulatory clarity, and hyperscaler capital commitments. Amazon plans USD 30 billion for new U.S. data centers, expanding the private cloud supply chain for enterprises shifting from public consumption models. Verizon’s private 5G rollout at Cummins’ Jamestown plant highlights deep integration of edge compute and localized clouds.

Asia-Pacific posts the strongest 16.45% CAGR to 2030, underpinned by domestic data-sovereignty mandates and manufacturing digitalization. Nineteen percent of regional enterprises will lift sovereign cloud spending in 2025, while two-thirds of Australian firms already evaluate local-jurisdiction platforms. National programs in India, Korea, and Indonesia incentivize domestic hosting to retain economic value and strategic control.

Europe advances steadily as DORA and similar acts compel financial institutions to adopt resilient, region-based clouds. Organizations diversify away from U.S. public environments to mitigate extraterritorial access risks. Meanwhile, Middle East and Africa adopt sovereign frameworks, with Nigerian businesses preferring in-country providers over global giants. Geographic adoption therefore follows regulatory imperatives and industrial modernization priorities, giving rise to multiple regional private cloud ecosystems.

Competitive Landscape

Traditional virtualization leaders now compete alongside hardware OEMs, hyperscalers, and pure-play cloud software firms. Broadcom’s integration of VMware introduced price shocks of 300-600%, spurring customers to pilot Nutanix, Red Hat, and Microsoft stacks. IBM’s USD 6.4 billion bid for HashiCorp in 2025 underscores the race to bundle infrastructure automation into hybrid offerings.

Vendors differentiate through AI-optimized blueprints, Kubernetes automation, and integrated financial-operations toolchains. HPE collaborates with NVIDIA on Private Cloud AI, promising accelerated model training within controlled environments. Dell’s order backlog signals robust demand for turnkey GPU farms that stay inside company walls. These approaches fuse hardware, software, and services into cohesive platforms that reduce deployment friction.

Emerging opportunities center on sovereign cloud, industry-specific compliance, and edge-to-core orchestration. Red Hat’s work with Nokia and T-Mobile illustrates ecosystem-led expansion into telecom. Managed hosters invest heavily in liquid-cooled data centers to support power-dense AI nodes. Competitive intensity remains moderate, with a dozen vendors holding the majority of enterprise deployments yet leaving space for specialists focused on compliance, FinOps automation, or vertical integrations.

Private Cloud Industry Leaders

Microsoft Corporation

IBM Corporation

Amazon Web Services

Dell Technologies Inc.

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Broadcom announced general availability of VMware Cloud Foundation 9.0, offering a consistent operating model across data centers, edge sites, and managed infrastructure.

- May 2025: Alexi introduced Alexi Private Cloud, an isolated deployment of its legal AI platform for law firms.

- May 2025: HPE unveiled Private Cloud Business Edition with Morpheus VM Essentials, targeting 90% VM license cost reduction and 2.5× lower TCO.

- April 2025: Kyndryl launched AI Private Cloud services that span design, planning, and MLOps for regulated sectors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

The study defines the private cloud market as all revenue generated from software, infrastructure, and managed services that are provisioned for the exclusive use of one enterprise, whether hosted on-premises or in a dedicated third-party facility, and delivered through virtualization or container platforms.

Scope Exclusion: public multi-tenant clouds and pure colocation contracts fall outside this boundary.

Segmentation Overview

- By Deployment Model

- Software-as-a-Service (SaaS)

- Platform-as-a-Service (PaaS)

- Infrastructure-as-a-Service (IaaS)

- By End-user Enterprise Size

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Government and Public Sector

- Manufacturing and Industrial

- IT and Telecommunications

- Retail and E-commerce

- By Hosting Type

- On-premises Dedicated Private Cloud

- Virtual Private Cloud (VPC)

- Managed/Hosted Private Cloud

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor Intelligence interview teams spoke with cloud architects, procurement heads, and managed-service partners across North America, Europe, Asia-Pacific, and the Middle East to verify workload migration rates, price-performance thresholds, and regulatory triggers shaping private cloud adoption. These conversations helped us bridge data gaps around hybrid deployment mixes and refine the adoption curves surfaced during desk work.

Desk Research

Our analysts extracted baseline demand indicators from publicly available tier-1 sources such as the US National Institute of Standards and Technology (NIST) for cloud standards, International Telecommunication Union data on enterprise connectivity, Eurostat structural business statistics, the Uptime Institute's annual data-center survey, and regional trade association filings on IT spending patterns. Company 10-Ks, earnings transcripts, and technology vendor price lists were mined to gauge average selling prices, margin trends, and shipment volumes.

Subscription resources from D&B Hoovers and Dow Jones Factiva supplied historical revenue splits and strategic moves of major suppliers, while Questel patent records highlighted innovation pacing in hyper-converged nodes. The sources cited here are illustrative; many additional open datasets and archival materials support validation and context building.

Market-Sizing & Forecasting

A top-down construct starts with enterprise IT hardware and service expenditure, which is then filtered through workload virtualization ratios and private-cloud penetration by industry. Select bottom-up roll-ups, sampled rack shipments, hypervisor licence counts, and managed-hosting contract values are used to corroborate and adjust totals. Key variables modeled include x86 rack server ASPs, average core density, software-defined storage attach rates, sector-specific compliance spending, and regional electricity costs that influence TCO. Multivariate regression coupled with scenario analysis projects these drivers through 2030, while any residual data gaps are smoothed using weighted averages from primary interviews.

Data Validation & Update Cycle

Model outputs undergo multi-step variance checks versus external spend trackers and capacity-utilization polls. Senior analysts review anomalies before sign-off. We refresh every twelve months, and an interim sweep is triggered when sizable M&A, regulatory, or macro events occur, ensuring clients receive a living dataset.

Why Mordor's Private Cloud Baseline Commands Confidence

Published estimates often diverge because firms pick different deployment mixes, currency bases, or refresh cadences. Buyers can be left puzzled when numbers do not align.

Key gap drivers include whether hosted managed environments are pooled with on-premises builds, how aggressively future ASP erosion is baked in, and if shadow IT budgets are excluded. Our disciplined scoping, annual refresh rhythm, and dual-path validation keep Mordor's figure centered and reproducible, whereas others may lean on single-path extrapolations or wider workload umbrellas.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 136.51 B (2025) | Mordor Intelligence | - |

| USD 124.80 B (2024) | Global Consultancy A | Merges virtual private cloud with colocation, uses five-year-old price deck |

| USD 134.00 B (2025) | Research Firm B | Excludes managed-hosted offerings and applies flat regional growth factor |

| USD 107.28 B (2024) | Trade Journal C | Limits scope to infrastructure services, omits software and support layers |

In short, Mordor Intelligence delivers a balanced baseline grounded in transparent variables, cross-checked by industry voices and refreshed on a predictable cycle, letting decision-makers act with higher conviction.

Key Questions Answered in the Report

What is the current size of the private cloud market?

The market is valued at USD 136.51 billion in 2025.

How fast is the private cloud market expected to grow?

It is projected to expand at a 12.30% CAGR, reaching USD 244.06 billion by 2030.

Which deployment model is growing the quickest?

Managed Services within the Services segment are advancing at a 13.90% CAGR.

Why are enterprises repatriating AI workloads?

They aim to lower operational costs, improve data privacy, and secure predictable performance, factors not always achievable in public clouds.