| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 1.38 Billion |

| Market Size (2030) | USD 2.53 Billion |

| CAGR (2025 - 2030) | 12.90 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

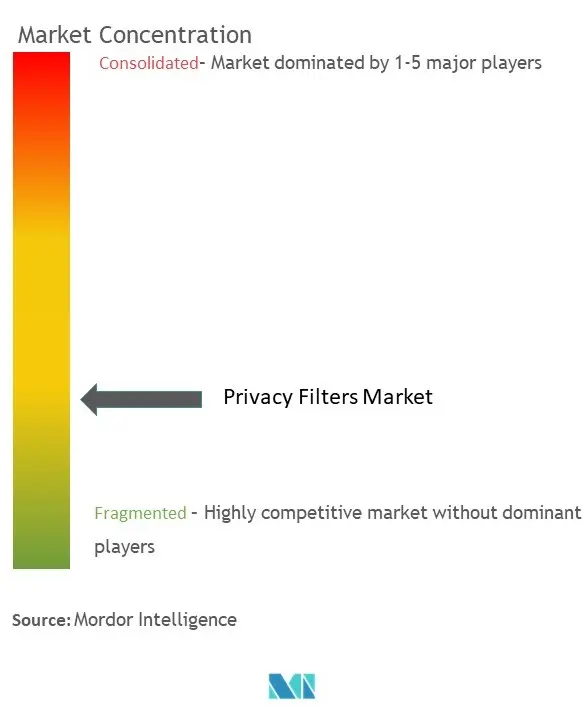

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Electronic Filters Market Analysis

The Privacy Filters Market size is estimated at USD 1.38 billion in 2025, and is expected to reach USD 2.53 billion by 2030, at a CAGR of 12.9% during the forecast period (2025-2030).

The privacy filters industry is experiencing significant transformation driven by the increasing digitalization of workplace environments and evolving security needs. According to Acuvue, office workers now spend approximately 6.5 hours daily in front of their computers, highlighting the critical need for enhanced screen protector solutions. This shift has prompted manufacturers to innovate beyond traditional privacy features, incorporating advanced technologies such as blue light filtering and anti-glare capabilities. The industry is witnessing a notable trend toward integrated solutions, with companies like TCL developing active privacy technology that allows users to switch privacy modes with a single click, moving away from conventional passive screen privacy filter protectors.

The market is seeing substantial technological advancements and product innovations that are reshaping user expectations and experiences. In August 2022, 3M launched COMPLY Magnetic Attach for Monitors, introducing a revolutionary quick-click bracket system that enables workers to easily attach and detach privacy filter solutions without compromising security. This development reflects the industry's response to the growing demand for flexible privacy solutions in hybrid work environments. According to Flexera Software, 49% of North American respondents anticipate increased IT spending, indicating strong potential for screen privacy filter adoption across various sectors.

The threat of visual hacking has emerged as a critical concern across industries, driving the adoption of sophisticated screen filter solutions. A recent Ponemon Institute study revealed alarming statistics: 52% of displays are vulnerable to visual hacking, with 91% of visual hacking attempts proving successful and 68% of visual intrusions going undetected. These findings have prompted organizations to reevaluate their physical security measures, particularly in high-risk sectors such as healthcare, finance, and legal services where data confidentiality is paramount.

The market is witnessing a shift toward more versatile and user-friendly solutions that accommodate various device types and usage scenarios. Major device manufacturers are increasingly integrating computer privacy screen features into their products, as evidenced by Fujitsu's launch of its LIFEBOOK U7 Series notebooks with built-in privacy filter solutions for hybrid work environments. This trend is further supported by the significant growth in device sales, with HP's notebook revenue reaching USD 30,522 million in 2021, indicating strong underlying demand for privacy-enhanced computing solutions. The industry is moving toward more sophisticated solutions that combine physical privacy protection with digital security features, creating a more comprehensive approach to data protection.

Electronic Filters Market Trends

Optical Comfort and Device Protection

Privacy filters serve a dual purpose by providing both visual privacy and significant optical comfort benefits for users. These filters incorporate advanced technology that reduces harmful blue light exposure by up to 30%, helping prevent eye strain and potential retinal damage from prolonged screen exposure. The anti-glare properties of privacy filters create an optimal viewing experience by eliminating mirror-like reflections from bright indoor lights while simultaneously protecting users' eyes from harmful UV rays, making them particularly valuable in various lighting conditions, whether working in offices, outdoors, or at home.

The protective capabilities of privacy filters extend beyond optical comfort to provide comprehensive device protection. These filters, typically constructed with high-grade materials and innovative micro-louver technology, serve as a physical barrier against obstinate debris and long-lasting scratches on device screens. The reversible nature of many privacy filters offers users the flexibility to choose between a matte finish that maximizes glare reduction and minimizes fingerprints, or a glossy surface that provides enhanced screen clarity. This versatility, combined with the filters' ultra-thin design (some as thin as 0.29mm), ensures that the protective benefits don't compromise device functionality or aesthetics while maintaining touchscreen compatibility and responsiveness. The integration of a screen protector enhances the durability and longevity of devices, making it a crucial accessory for modern technology.

Understand The Key Trends Shaping This Market

Download PDF

Rising Data Privacy and Security Concerns

The escalating concerns over visual hacking and data privacy have become significant drivers for privacy filter adoption across various sectors. According to recent studies by the Ponemon Institute, visual hacking attempts prove successful in 91% of cases, with 68% of visual intrusions going completely undetected, highlighting the severe vulnerability of unprotected screens. The risk is particularly pronounced in financial institutions, healthcare facilities, and corporate environments where sensitive information such as login credentials, financial records, and confidential documents are regularly displayed on screens, making them susceptible to unauthorized viewing from casual observers or intentional visual hackers.

The growing mobile workforce and flexible working arrangements have significantly amplified data privacy concerns, as employees increasingly access and process confidential information in non-secure locations such as cafes, airports, and public transportation. This shift in working patterns has created new challenges for organizations in maintaining visual privacy, especially when handling sensitive client data, internal financial statements, and proprietary information. The implementation of laptop privacy screen and monitor privacy screen solutions has become a critical component of comprehensive data protection strategies, providing a cost-effective solution to prevent visual hacking while ensuring compliance with increasingly stringent data protection regulations. These filters effectively narrow the field of vision to approximately 60 degrees, ensuring that sensitive information remains visible only to the intended user while appearing darkened to anyone viewing from side angles. Incorporating a screen privacy filter further enhances security measures, making it indispensable in today's data-driven environment.

Segment Analysis: By Application

Monitor Segment in Privacy Filters Market

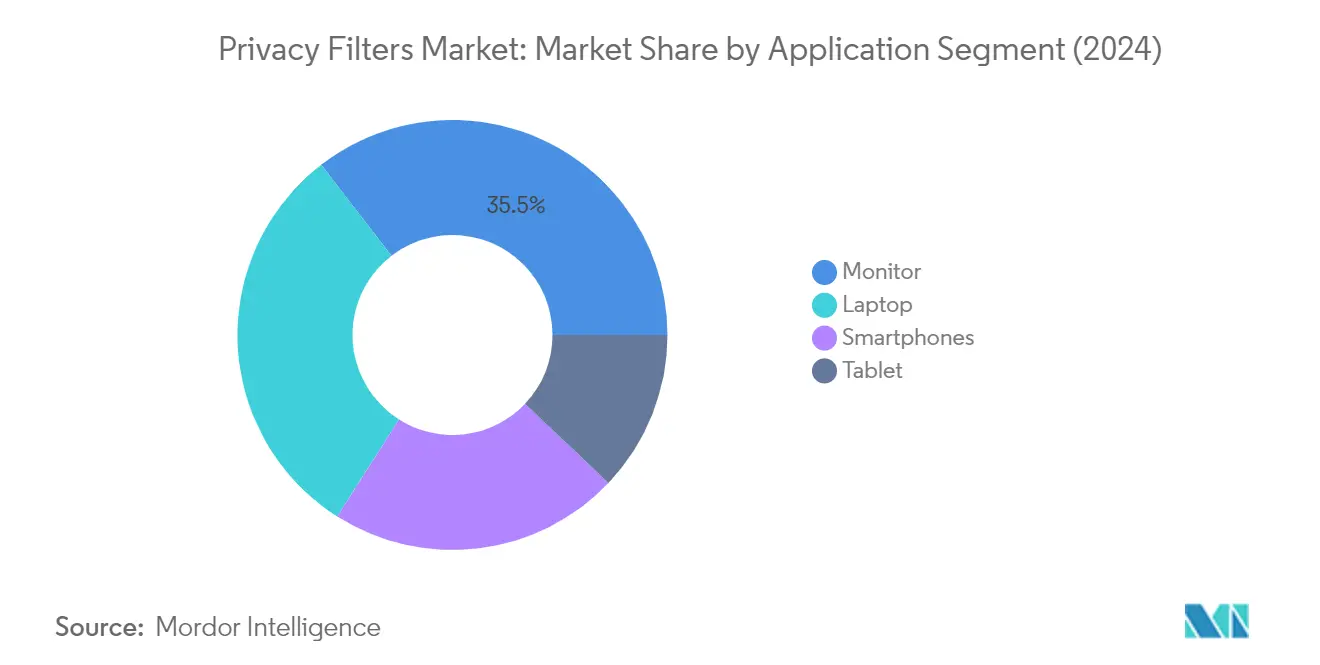

The monitor privacy screen segment continues to dominate the global privacy filters market, holding approximately 35% market share in 2024. This significant market position is primarily driven by the increasing adoption of screen privacy filter solutions in corporate offices, financial institutions, and healthcare facilities where protecting sensitive information displayed on monitors is crucial. The segment's growth is further supported by the rising implementation of visual privacy solutions in government organizations and educational institutions where multiple users often share workspace environments. Additionally, the increasing awareness about visual hacking in open office layouts and the need to comply with data protection regulations has led to widespread adoption of monitor privacy screen filters across various industries.

Smartphone Segment in Privacy Filters Market

The smartphone segment is emerging as the fastest-growing category in the privacy filters market for the period 2024-2029. This rapid growth is attributed to the increasing use of smartphones for accessing sensitive corporate data, banking applications, and personal information in public spaces. The segment's expansion is further fueled by the rising adoption of mobile banking solutions and the growing trend of remote work where professionals frequently access confidential information on their smartphones. The integration of advanced micro-louver technology in mobile privacy screen filters, which provides superior viewing angles and enhanced protection against visual hacking, is also contributing to the segment's accelerated growth trajectory.

Remaining Segments in Privacy Filters Market by Application

The laptop privacy screen and tablet segments complete the privacy filters market application landscape, each serving distinct user needs and preferences. The laptop privacy screen segment maintains a strong position due to the increasing mobility of the workforce and the growing need for visual privacy during business travel and remote work scenarios. Meanwhile, the tablet segment, though smaller in market share, continues to grow steadily driven by the increasing adoption of tablets in healthcare, education, and retail sectors where protecting sensitive information is paramount. Both segments benefit from technological advancements in privacy filter materials and mounting mechanisms, offering users enhanced flexibility and protection options.

Segment Analysis: By Feature

Adhesive Segment in Privacy Filters Market

The adhesive segment continues to dominate the global privacy filters market, commanding approximately 56% market share in 2024. This significant market position is attributed to the segment's superior screen clarity and comprehensive data protection capabilities. Adhesive privacy filters offer reliable attachment mechanisms that ensure the filter stays firmly in place while providing excellent touch sensitivity and screen visibility. These filters incorporate advanced ultra-fine vertical blinds technology that enables clear front viewing while blocking visibility from side angles. The washable adhesive variants have gained particular traction due to their reusability and ability to maintain effectiveness even after multiple applications. Additionally, these filters offer enhanced features such as blue light reduction, anti-glare properties, and scratch resistance, making them particularly appealing for professional and enterprise applications.

Magnetic Segment in Privacy Filters Market

The magnetic segment is emerging as the most dynamic category in the privacy filters market, projected to grow at approximately 14% during 2024-2029. This impressive growth trajectory is driven by the segment's unique value proposition of offering easy attachment and detachment capabilities without compromising device functionality. Magnetic privacy filters are particularly popular among users of premium devices like MacBooks and high-end monitors, as they allow for seamless integration with the device's design. The segment's growth is further bolstered by innovations in magnetic attachment mechanisms that enable users to quickly switch between privacy and sharing modes while ensuring the device can fully close and enter sleep mode with the filter attached. The versatility of magnetic filters, allowing users to choose between glossy and matte surfaces depending on lighting conditions, has significantly contributed to their increasing adoption across various professional environments.

Remaining Segments in Privacy Filters Market by Feature

The other features segment encompasses innovative attachment mechanisms such as flip-based privacy filters and double-sided tape solutions. These alternatives provide users with unique benefits such as built-in screen protection mechanisms and specialized mounting options for specific device types. The flip mechanism is particularly valuable in collaborative work environments where users frequently need to switch between private and shared viewing modes. Double-sided tape solutions offer a balance between permanent attachment and removability, catering to users who prefer a more traditional approach to screen protection. These alternative attachment methods continue to play an important role in meeting diverse user preferences and specific application requirements across different industries.

Segment Analysis: By End User Industry

Financial Institution Segment in Privacy Filters Market

The financial institution segment maintains its dominance in the privacy filters market, commanding approximately 27% market share in 2024. This significant market position is primarily driven by the critical need to protect sensitive financial data, customer information, and internal financial statements in banking environments. Financial institutions worldwide are implementing stringent security measures to safeguard confidential information displayed on screens, particularly as mobile and digital banking services continue to expand. The segment's prominence is further reinforced by increasing regulatory compliance requirements and the growing adoption of digital transformation initiatives in the banking sector, where visual privacy has become a crucial component of comprehensive data security strategies. Financial institutions are particularly focused on protecting various sensitive information including credit histories, loan applications, and customer financial records from visual hacking attempts, making privacy filters an essential tool in their security arsenal.

Healthcare Segment in Privacy Filters Market

The healthcare segment is emerging as the fastest-growing sector in the privacy filters market, with an expected growth rate of approximately 15% during 2024-2029. This remarkable growth is driven by the increasing digitization of patient records and the critical need to comply with stringent healthcare data protection regulations. Healthcare organizations are increasingly recognizing the importance of visual privacy in protecting sensitive patient information, particularly in shared workspaces and mobile healthcare environments. The adoption of privacy filters in healthcare settings is being fueled by the growing use of electronic health records (EHR) systems, telemedicine platforms, and mobile medical devices. Healthcare providers are implementing these solutions across various touchpoints, including nursing stations, mobile medical carts, and administrative areas, to prevent visual data breaches and maintain patient confidentiality in accordance with healthcare privacy regulations.

Remaining Segments in End User Industry

The privacy filters market encompasses several other significant segments including legal firms, government institutions, and educational institutions, each with unique privacy requirements and implementation needs. Legal firms utilize privacy filters to protect confidential client information and sensitive case details, while government organizations implement these solutions to safeguard classified information and citizen data. Educational institutions are increasingly adopting privacy filters to protect student records and administrative data, particularly with the rise of digital learning environments. These segments collectively contribute to the market's diversity, with each sector implementing privacy filters according to their specific security protocols and compliance requirements. The varying needs across these segments continue to drive innovation in privacy filter technology, leading to the development of more specialized solutions tailored to each sector's unique requirements.

Privacy Filters Market Geography Segment Analysis

Privacy Filters Market in North America

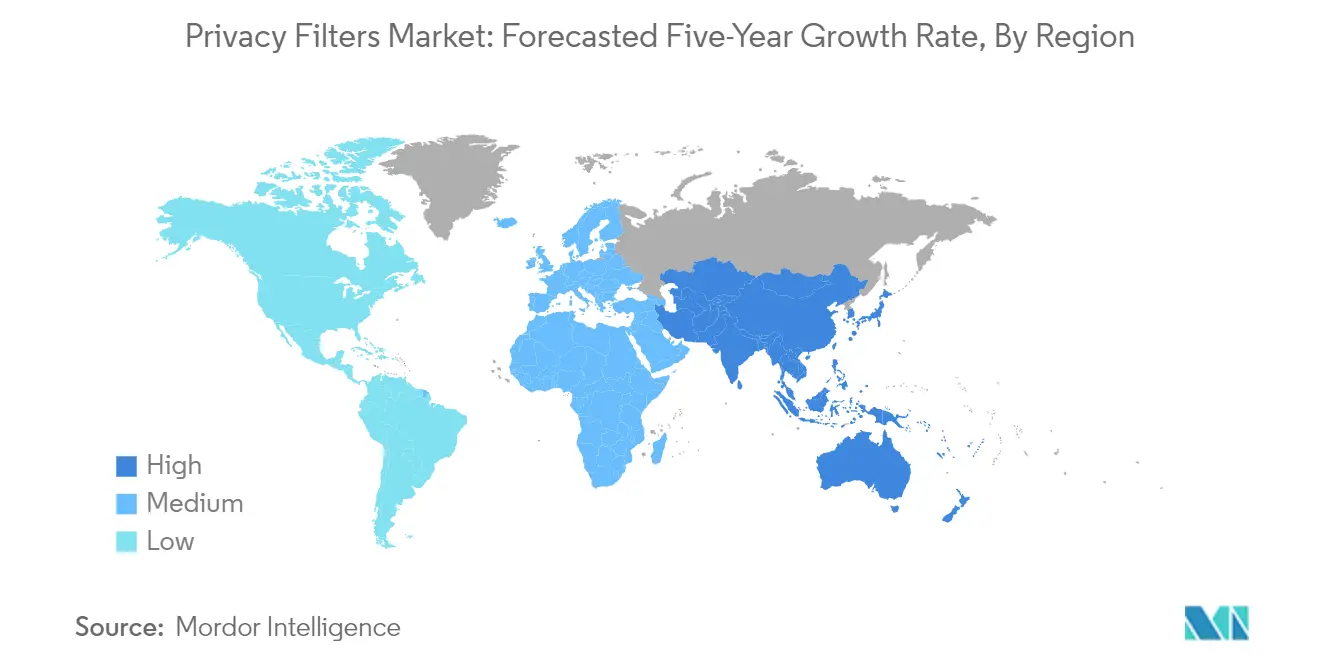

North America represents a dominant force in the global privacy filters market, holding approximately 31% market share in 2024. The region's leadership position is primarily driven by the extensive adoption of mobile devices in workspaces across major economies like the United States and Canada. The growing customer demand for connected devices and increasing penetration of electronic products continue to fuel market growth. The introduction of advanced technologies, including artificial intelligence, 5G, cloud computing, the Internet of Things, autonomous driving, and augmented and virtual reality, along with their incorporation into electronic products, is boosting the demand for new and innovative smart products. The region's robust information technology infrastructure and increasing corporate focus on data security have created a strong foundation for privacy filter adoption. Financial institutions, healthcare organizations, and government agencies in North America are particularly driving demand due to stringent data protection requirements and compliance needs. The region's emphasis on workplace privacy and information security, coupled with the high presence of major market players, continues to strengthen its position in the global privacy filters market.

Privacy Filters Market in Europe

Europe maintains a significant presence in the privacy filters market, demonstrating a robust growth trajectory with approximately a 13% growth rate from 2019 to 2024. The market's expansion is primarily driven by the increasing demand for smartphones, laptops, monitors, and other electronic devices across the region. The European market benefits from strong data protection regulations and a heightened focus on privacy concerns across various sectors. Financial institutions, particularly in countries like Germany, the United Kingdom, and France, are major adopters of privacy filters due to the critical nature of their operations and the need to protect sensitive client information. The region's emphasis on workplace privacy and data protection compliance, especially under GDPR requirements, has created a strong foundation for market growth. The presence of numerous multinational corporations and financial centers has further accelerated the adoption of privacy filters. European businesses' increasing focus on mobile workforce security and the growing awareness of visual hacking threats have also contributed to market expansion. The region's sophisticated IT infrastructure and strong emphasis on employee privacy protection continue to drive innovation in privacy filter technologies.

Privacy Filters Market in Asia-Pacific

The Asia-Pacific region represents the fastest-growing market for privacy filters, with a projected growth rate of approximately 15% from 2024 to 2029. This remarkable growth is attributed to the rapid digitalization across major economies like China, Japan, India, and South Korea. The region's expanding financial sector, particularly in emerging economies, has created substantial demand for privacy protection solutions. The increasing adoption of smartphones, tablets, and laptops in both corporate and educational sectors has heightened the need for visual privacy solutions. Major technology manufacturing hubs in countries like China, Japan, and South Korea are driving innovation in privacy filter technology, while also increasing local availability and adoption. The growing awareness of data privacy concerns and the implementation of stricter data protection regulations across various Asian countries have created a favorable environment for market expansion. The region's rapid economic growth, coupled with increasing corporate emphasis on data security, continues to drive the adoption of privacy filters across various sectors. The emergence of new business models and the growing remote workforce have further accelerated the need for visual privacy solutions in the Asia-Pacific region.

Privacy Filters Market in Rest of the World

The Rest of the World region, encompassing the Middle East, Africa, and Latin America, demonstrates growing potential in the privacy filters market. The increasing digitalization efforts across these regions, particularly in financial and government sectors, are driving the adoption of privacy filters. Countries in the Middle East, with their robust banking sector and increasing focus on cybersecurity, are showing significant interest in visual privacy solutions. The growing smartphone penetration and increasing awareness about data privacy in African nations are creating new opportunities for market expansion. The education sector across these regions is emerging as a significant consumer of privacy filters, driven by the increasing adoption of digital learning solutions. The healthcare sector's digital transformation in these regions has also contributed to the growing demand for privacy filters. The presence of multinational corporations and their emphasis on data protection compliance has further stimulated market growth. The region's evolving regulatory landscape regarding data protection and privacy is expected to create additional opportunities for privacy filter manufacturers and suppliers.

Get Analysis on Important Geographic Markets

Download PDF

Electronic Filters Industry Overview

Top Companies in Privacy Filters Market

The privacy filters market features established players like 3M Company, Targus, Dell Inc., Tech Armor, and Fellowes Brands leading the competitive landscape. Companies are focusing on developing advanced optical technologies and microlouver innovations to enhance visual privacy while maintaining screen clarity. Strategic product development includes features like blue light filtering, anti-glare properties, and compatibility with touchscreen devices. Operational agility is demonstrated through quick-response manufacturing and customization capabilities for different device specifications. Market leaders are expanding through partnerships with device manufacturers and establishing distribution networks across regions. Innovation trends show a shift towards magnetic attachment systems, reversible viewing options, and enhanced durability features. Companies are also emphasizing sustainability through eco-friendly packaging and materials while investing in antimicrobial protection technologies.

Mixed Market Structure with Regional Specialists

The screen protector market exhibits a mixed competitive structure with both global conglomerates and regional specialists maintaining significant market presence. Global players like 3M and Dell leverage their extensive distribution networks and brand recognition, while regional specialists such as EPHY Privacy and Kapsolo Europe focus on specific geographical markets with customized solutions. The market shows moderate consolidation with established players controlling major market share through their technological expertise and long-standing relationships with device manufacturers. These companies maintain their positions through extensive product portfolios covering various device types and sizes.

Recent market dynamics show increasing merger and acquisition activities, particularly involving technology companies seeking to expand their accessories portfolio. Companies are pursuing strategic partnerships with device manufacturers and distributors to strengthen their market position and expand geographical reach. The market structure is evolving with new entrants bringing specialized privacy solutions, while established players are expanding through acquisitions of smaller, innovative companies to enhance their technological capabilities and market coverage.

Innovation and Customization Drive Future Success

Success in the screen protector industry increasingly depends on technological innovation and the ability to adapt to rapidly evolving device specifications. Companies need to focus on developing advanced optical technologies while maintaining cost competitiveness and production efficiency. Market players must establish strong relationships with device manufacturers to ensure compatibility with new product launches and maintain market relevance. The ability to offer customized solutions for specific industry verticals, particularly in the financial and healthcare sectors, will become increasingly important for market success.

Future market share gains will require companies to balance product innovation with price competitiveness while addressing growing environmental concerns. Successful players will need to develop comprehensive distribution strategies covering both online and offline channels while providing superior customer support and warranty services. The market shows limited substitution risk due to the specific nature of privacy protection requirements, but regulatory compliance regarding data protection and workplace privacy standards will influence product development and marketing strategies. Companies must also focus on educating end-users about visual privacy risks and the benefits of privacy screen filters to drive market growth.

Electronic Filters Market Leaders

-

3M company

-

Targus

-

Dell Inc.

-

Tech Armor

-

Fellowes Brands

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Electronic Filters Market News

- May 2024: Autonivs launched the LSE3 Series LiDAR sensors for accurate object detection. This series supports up to four different channels for extended communication. To minimize communication errors, the sensors deploy different filter functions that help reduce noise for clean, accurate data transfer. An aluminum die-cast housing helps provide adequate protection from the harsh industrial environment and minimizes the chance of interference from 5G communication repeaters.

- November 2023: TDK Corporation announced the launch of noise suppression filters for the audio lines of high-sound quality devices. The company launched its noise suppression filters MAF1005FR series, designed to improve sound quality and reduce noise interference in smartphones' audio lines (sound lines) and other devices, including tablets, wearables, and portable games.

Electronic Filters Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Optical Comfort and Device Protection

- 5.1.2 Rising Data Privacy and Security Concerns

-

5.2 Market Restraints

- 5.2.1 Lack of Awareness about the Privacy Filters among the Users

- 5.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

6. MARKET SEGMENTATION

-

6.1 By Application

- 6.1.1 Laptops

- 6.1.2 Monitors

- 6.1.3 Smartphones

- 6.1.4 Tablets

-

6.2 By Feature

- 6.2.1 Adhesive

- 6.2.2 Magnetic

- 6.2.3 Other Features

-

6.3 By End-user Industry

- 6.3.1 Financial Institution

- 6.3.2 Educational Institution

- 6.3.3 Legal Firm

- 6.3.4 Government

- 6.3.5 Healthcare

- 6.3.6 Other End User Industries

-

6.4 By Geography***

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 3M Company

- 7.1.2 Targus

- 7.1.3 Dell Inc.

- 7.1.4 Tech Armor

- 7.1.5 Fellowes Brands

- 7.1.6 Kensington Computer Products Group (ACCO Brands)

- 7.1.7 MoniFilm (Right Group Co. Ltd)

- 7.1.8 EPHY Privacy (Advance Services & Solutions Ltd)

- 7.1.9 Upscreen (Bedifol GmbH)

- 7.1.10 KAPSOLO Europe ApS

- 7.1.11 Fujitsu Limited

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia-Pacific'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Electronic Filters Industry Segmentation

An electronic filter is a panel positioned over a display to make it difficult for somebody to read the screen without being straight in front of it. The misapplication of confidential information has become so extensive that new commandments were passed to guarantee privacy. Maintaining the safety of subtle details on the computer display is vital. Electronic filters help prevent casual spectators from observing confidential data on-screen.

The electronic filters market is segmented by application (laptops, monitors, smartphones, and tablets), feature (adhesive, magnetic, and other features), end-user industry (financial institution, educational institution, legal firm, government, healthcare, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Application | Laptops |

| Monitors | |

| Smartphones | |

| Tablets | |

| By Feature | Adhesive |

| Magnetic | |

| Other Features | |

| By End-user Industry | Financial Institution |

| Educational Institution | |

| Legal Firm | |

| Government | |

| Healthcare | |

| Other End User Industries | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Electronic Filters Market Research FAQs

How big is the Privacy Filters Market?

The Privacy Filters Market size is expected to reach USD 1.38 billion in 2025 and grow at a CAGR of 12.90% to reach USD 2.53 billion by 2030.

What is the current Privacy Filters Market size?

In 2025, the Privacy Filters Market size is expected to reach USD 1.38 billion.

Who are the key players in Privacy Filters Market?

3M company, Targus, Dell Inc., Tech Armor and Fellowes Brands are the major companies operating in the Privacy Filters Market.

Which is the fastest growing region in Privacy Filters Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Privacy Filters Market?

In 2025, the North America accounts for the largest market share in Privacy Filters Market.

What years does this Privacy Filters Market cover, and what was the market size in 2024?

In 2024, the Privacy Filters Market size was estimated at USD 1.20 billion. The report covers the Privacy Filters Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Privacy Filters Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Privacy Filters Market Research

Mordor Intelligence provides a comprehensive analysis of the privacy filter industry. We leverage our extensive expertise in technology market research to deliver this analysis. Our detailed report examines the evolving landscape of screen privacy filter solutions. This includes innovations in laptop privacy screen technologies, monitor privacy screen advancements, and mobile privacy screen developments. The analysis covers both traditional screen protector segments and advanced confidentiality screen solutions. These insights are available in an easy-to-read report PDF format for immediate download.

Our research benefits stakeholders across the screen protector industry by offering an in-depth analysis of computer privacy screen technologies and emerging trends in the screen filter segment. The report provides valuable insights for manufacturers, distributors, and end-users in the monitor filter space. It also examines growth opportunities in the expanding market for screen protectors. Mordor Intelligence's methodology ensures comprehensive coverage of market dynamics, competitive landscapes, and future growth projections. This delivers actionable intelligence for informed decision-making.