Premium Water Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

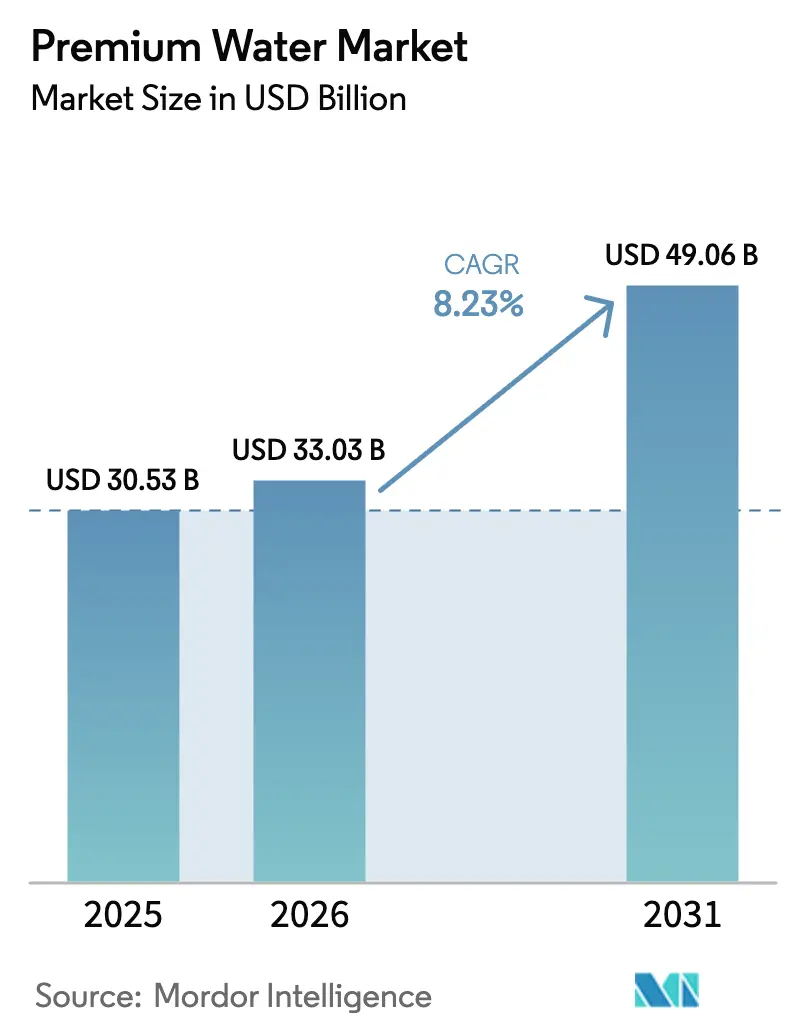

| Market Size (2026) | USD 33.03 Billion |

| Market Size (2031) | USD 49.06 Billion |

| Growth Rate (2026 - 2031) | 8.23% CAGR |

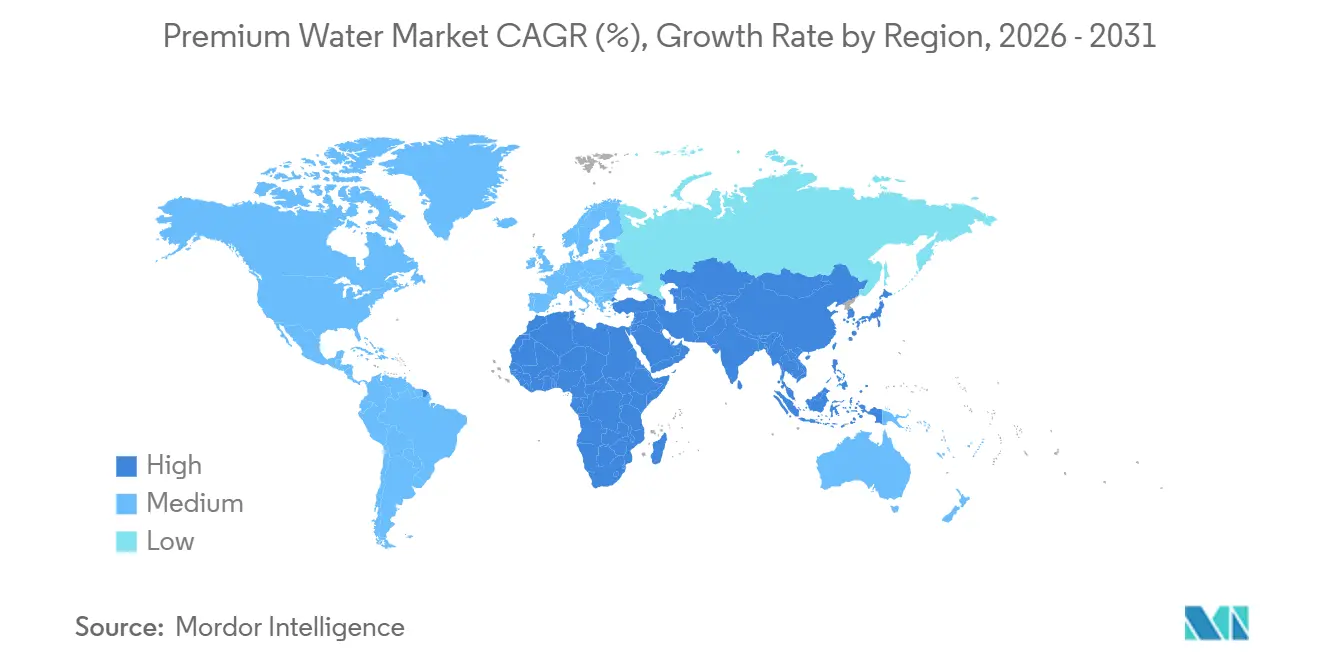

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

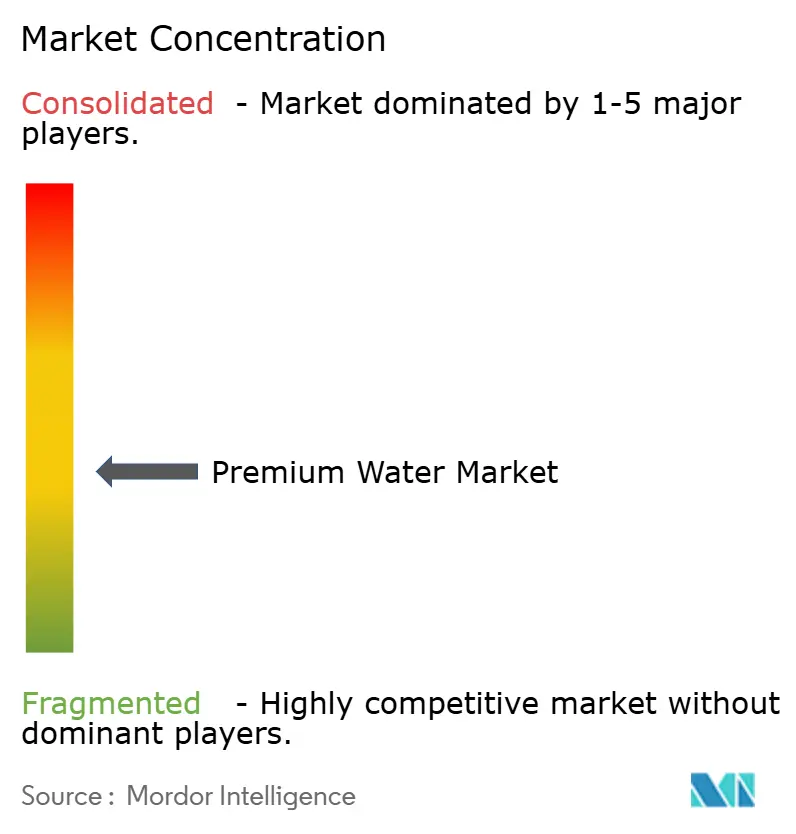

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Premium Water Market Analysis by Mordor Intelligence

The Premium Water market size was valued at USD 30.53 billion in 2025 and estimated to grow from USD 33.03 billion in 2026 to reach USD 49.06 billion by 2031, at a CAGR of 8.23% during the forecast period 2026-2031. Factors like heightened health awareness, lifestyle branding, and sustainability are elevating hydration to a premium status. While Europe dominated the regional landscape in 2025, the Asia-Pacific, buoyed by an expanding urban middle class and a focus on wellness, is poised to emerge as the fastest-growing region. Although still water remains the dominant choice, sparkling and functional variants are gaining traction, with consumers increasingly opting for zero-sugar, flavored, and electrolyte-rich alternatives over traditional soda. The packaging landscape is diversifying: while cost-effective plastic remains predominant, lightweight glass is gaining momentum, and aluminum is rising in popularity due to its recyclability and convenience for on-the-go consumers. The competitive landscape is moderately intense, with global giants streamlining their portfolios, while disruptors carve a niche through social media, direct-to-consumer logistics, and striking aesthetics.

Key Report Takeaways

- By product type, still water captured 62.17% of Premium Water market share in 2025, while sparkling water is set to post a 9.13% CAGR through 2031.

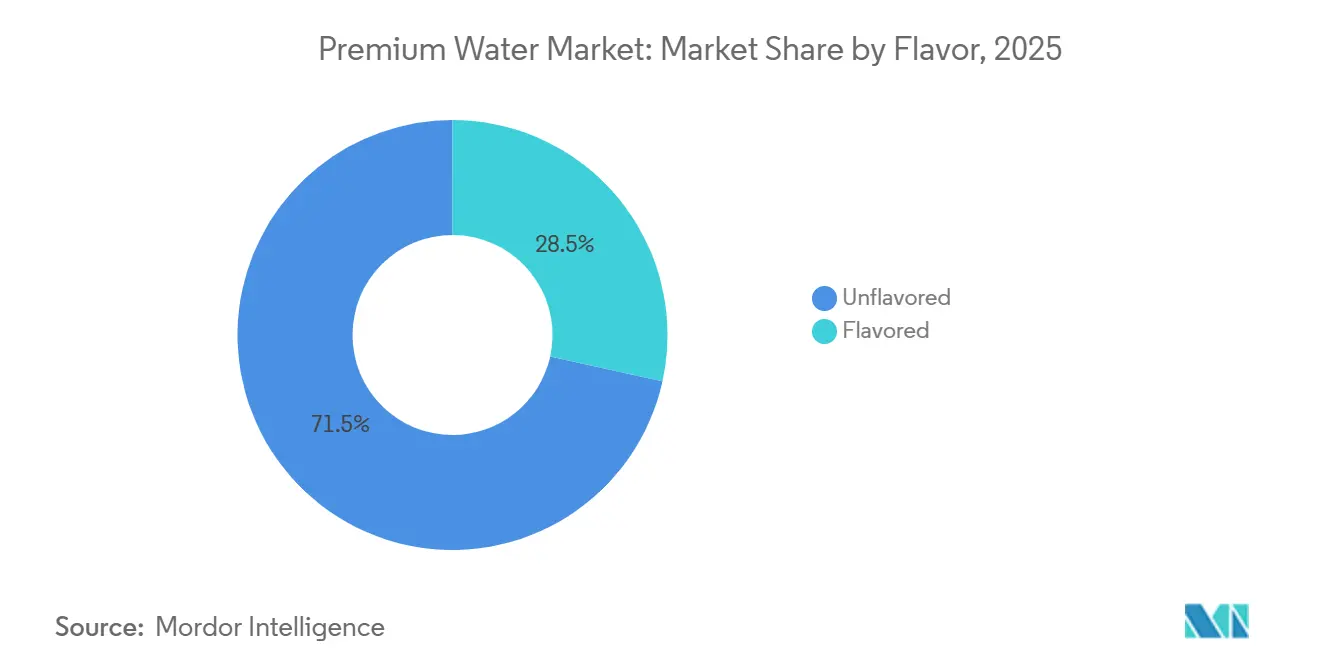

- By flavor, unflavored formats led with 71.54% revenue share in 2025; flavored variants are forecast to expand at a 7.56% CAGR over 2026-2031.

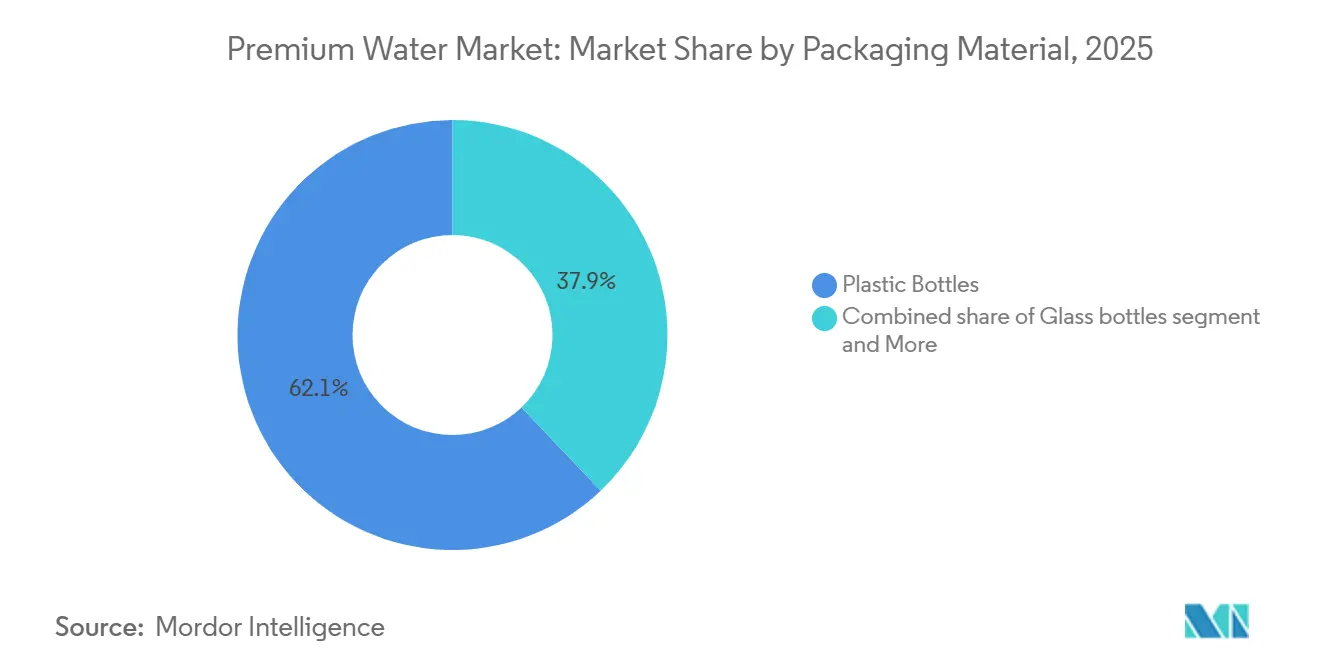

- By packaging, plastic bottles retained 62.11% of Premium Water market size in 2025, whereas glass bottles represent the fastest-growing format at a 10.48% CAGR.

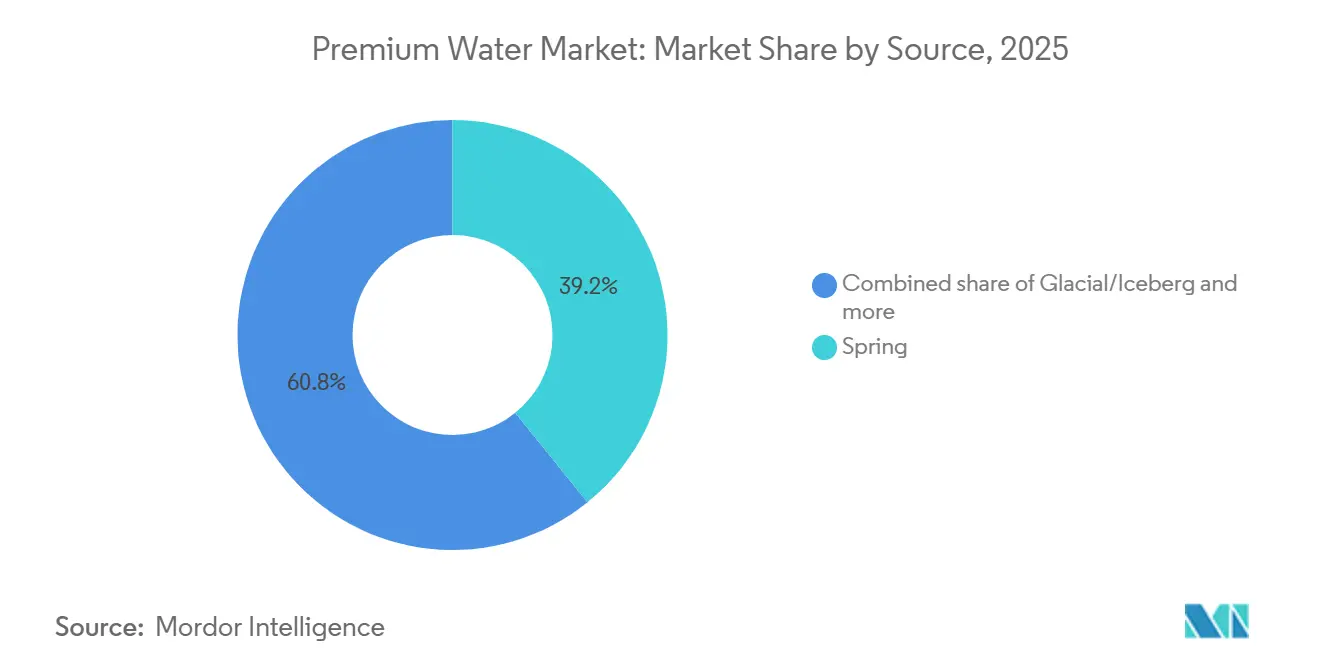

- By source, spring water commanded 39.25% share of the Premium Water market size in 2025 and glacial/iceberg water is projected to grow 7.35% CAGR during 2026-2031.

- By distribution, off-trade dominated with 66.13% share in 2025; on-trade channels are advancing at a 12.47% CAGR to 2031.

- By geography, Europe held 44.37% share of Premium Water market size in 2025; Asia-Pacific is anticipated to escalate at a 9.81% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Premium Water Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and wellness-driven shift toward functional hydration | +2.1% | Global, with strongest uptake in North America, Western Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Premiumization and lifestyle branding | +1.8% | North America, Europe, affluent urban centers in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Increasing tourism boosts demand for premium bottled water | +1.3% | Europe (France, Italy, Spain), Asia-Pacific (Thailand, Singapore), Middle East (UAE, Saudi Arabia) | Short term (≤ 2 years) |

| Social media trends influence premium water choices | +1.5% | North America, Western Europe, urban Asia (China, Japan, South Korea) | Short term (≤ 2 years) |

| Expansion of luxury retail channels supports premium water | +1.2% | Global, concentrated in Tier-1 cities and premium grocery/specialty retail | Medium term (2–4 years) |

| Product innovation with flavors enhances consumer interest | +1.1% | North America, Europe, Asia-Pacific urban markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Health and wellness-driven shift toward functional hydration

The increasing consumer focus on hydration as a means to achieve specific health benefits is driving the growth of the premium water market. Products such as alkaline, electrolyte, and vitamin-infused waters are gaining traction. In 2024, the European Commission introduced technical guidelines for the standardized measurement of ‘PFAS Total’ and ‘Sum of PFAS’ in drinking water, enhancing safety and quality standards across the EU and fostering consumer trust in functional water products[1]Source: European Commission, "New EU-wide protections against PFAS in drinking water come into effect", environment.ec.europa.eu. Essentia Hydroboost, containing 400 mg of electrolytes per bottle, has successfully penetrated mainstream U.S. retail channels, reflecting consumer acceptance of premium pricing. Similarly, Coca-Cola's Power Water, which delivers 50% more electrolytes than Propel, highlights the growing interest of major beverage companies in this segment. In India, Booster Black Water has reported sales exceeding 1 million cans by 2026, indicating the rising demand for functional water in emerging markets. The functional claims associated with these products support higher price points and strengthen brand differentiation, reducing direct price comparisons with standard bottled water.

Premiumization and lifestyle branding

Consumers increasingly associate premium water with superior taste and values, elevating its status as a lifestyle product. Brands like Realm Artesian, priced at USD 6.50 for a 16 oz glass, leverage origin stories, such as its Adirondack roots, to justify their premium positioning. Similarly, Liquid Death has effectively utilized counterculture branding, combining distinctive design with aluminum tallboys, achieving a valuation of USD 1.4 billion and projected 2024 revenues of USD 333 million. Celebrity-backed products, such as Caliwater, are also contributing to market expansion by enhancing brand appeal and pricing power. Additionally, shifting consumer preferences toward healthier and more wellness-focused lifestyles are influencing purchasing decisions. A growing number of consumers are opting for non-alcoholic beverages, particularly in restaurant settings, reflecting a broader movement toward health-conscious choices and experiential consumption.

Social media trends influence premium water choices

Social media trends are becoming a major force in the premium water market, shaping both consumer preferences and brand visibility. UK adults now average four and a half hours online daily, marking a 10-minute increase from last year. Additionally, 95% of the UK population aged 16 and above have access to the internet at home, and the average time spent online daily on personal devices (smartphones, tablets, and computers) in May 2025 was 4 hours and 30 minutes[2]Source: Online Nations Report, "Online Landscape", ofcom.org.uk. In August 2025, fitness influencer Ashton Hall highlighted Saratoga Spring Water's cobalt-blue bottles in a popular morning-routine video. This endorsement not only boosted sales but also caused a temporary spike in the brand's stock prices. The resulting organic social sharing and meme creation emphasized the influential power of such endorsements. Similarly, in February 2026, Altitude Water appointed sustainability influencer Luke Hillman as its brand ambassador. Hillman promoted the company's atmospheric water generation technology, aiming to connect with a younger, eco-conscious demographic. Given the rapid trend cycles and micro-virality on social media, brands are increasingly adopting real-time monitoring, agile content strategies, and limited-edition product launches to capitalize on fleeting opportunities. Additionally, striking packaging, such as Liquid Death's skull-themed tallboy cans and Icelandic Glacial's frosted glass bottles, not only enhances user-generated content and unboxing experiences but also cements a premium market position, driving growth.

Product innovation with flavors enhances consumer interest

Product innovation with flavors is emerging as a significant driver in the premium water market, enhancing consumer interest and supporting market growth. Flavored water offerings effectively address the gap between plain water and high-calorie soft drinks, catering to evolving consumer preferences. For instance, PepsiCo introduced “bubly drops,” a customizable solution that allows consumers to add zero-calorie flavors to sparkling water. Similarly, in 2023, Coca-Cola Company expanded its premium sparkling water portfolio with Topo Chico Sabores, featuring flavors such as lime, grapefruit, and tangerine, aimed at health-conscious consumers seeking refreshing alternatives[3]Source: The Coca‑Cola Company, "Topo Chico Launches Line of Fruit-Flavored Sparkling Waters With Herbal Extracts", coca-colacompany.com.The use of natural extracts and essential oils aligns with the growing demand for clean-label products, further increasing the appeal of these offerings in the premium segment. However, the risk of commoditization due to similar flavor profiles across brands underscores the importance of continuous innovation. Overall, flavor-driven product differentiation is playing a pivotal role in attracting consumers and driving the expansion of the premium water market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product pricing limits mass consumer adoption | -1.4% | Developing markets (India, Southeast Asia, Latin America, Sub-Saharan Africa); price-sensitive segments in developed markets | Medium term (2–4 years) |

| At-home filtration/dispense tech cannibalizes bottled demand | -1.1% | North America, Western Europe, urban Asia-Pacific (Japan, South Korea, Singapore) | Long term (≥ 4 years) |

| Counterfeit or low-quality products undermine consumer trust | -0.7% | Emerging markets (China, India, Southeast Asia); online retail channels globally | Short term (≤ 2 years) |

| Slow adoption in developing countries hinders growth | -0.9% | Sub-Saharan Africa, rural South Asia, parts of Latin America and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High product pricing limits mass consumer adoption

High price points act as a significant restraint on the penetration of premium water products into middle-income demographics. For instance, Evian is priced higher than standard bottled water in European supermarkets, limiting its appeal to cost-sensitive consumers. Similarly, Realm Artesian's positioning at USD 6.50 confines its distribution to luxury channels, which, while ensuring high margins, restricts unit sales and overall market reach. In China, the market exhibits polarization, with standard PET bottles priced at USD 0.18 per unit, while premium SKUs priced above USD 1.40 cater to a small but growing niche. This bifurcated market landscape highlights the challenges of balancing affordability with premium positioning. To mitigate the risk of volume erosion, companies must focus on strategies such as offering smaller pack sizes or incorporating functional benefits to make premium products more accessible without diluting their brand value.

At-home filtration/dispense tech cannibalizes bottled demand

The increasing adoption of at-home filtration and dispensing technologies, such as Elkay's ezH2O bottle-filling stations, is emerging as a significant restraint on the premium bottled water market. These systems are designed for ease of use and often incorporate advanced filtration mechanisms. Features like hands-free operation, antibacterial materials to reduce germ transmission, and energy-efficient components, including power compressors and high-efficiency insulation, enhance their appeal. Additionally, smart connectivity, automated filter reordering, and app-based contamination alerts provide added convenience and cost-effectiveness over time, making them a viable alternative to single-serve bottled water. While premium bottled water brands attempt to differentiate through portability, occasion-specific consumption, and functional additives not found in tap water, the growing preference for at-home solutions poses a structural challenge to market growth.

Segment Analysis

By Source: Spring Water Leadership Amid Glacial Premium Growth

Spring water emerged as the largest segment in the premium water market in 2025, contributing 39.25% to the market share. This segment's dominance is driven by strong consumer trust in its naturally mineralized profile and its scalability. Sustainable extraction practices, adhering to environmental flow thresholds, ensure a consistent supply while maintaining ecological balance. Companies leveraging spring water benefit from its broad consumer appeal and ability to cater to diverse preferences. The perception of spring water as a "natural and untouched" source enhances its premium positioning. Additionally, its widespread geographic availability supports steady supply chains and market penetration. Investments in sustainable sourcing and eco-friendly packaging further strengthen consumer confidence and drive long-term demand within this segment.

Glacial and iceberg water represent the fastest-growing segment, with an expected CAGR of 7.35%, driven by their ultra-premium positioning. This segment commands luxury pricing due to its low mineral content and remote origins. However, climate-driven challenges, such as glacier retreats and volume constraints, necessitate adaptive sourcing strategies and rigorous quality testing. Companies are diversifying their source portfolios by incorporating artesian, purified, or locally filtered options to mitigate environmental risks and meet varying consumer preferences. The exclusivity of glacial and iceberg water appeals to high-income consumers seeking rare and unique products. Branding strategies that emphasize purity, origin narratives, and limited availability further enhance their premium perception. However, increasing environmental scrutiny and regulatory pressures may require companies to adopt transparent sourcing practices and sustainability certifications to maintain credibility in this segment.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Functional Sparkling Gains Velocity

In 2025, still water dominated the Premium Water market, seizing a 62.17% share. This segment's dominance was largely attributed to its strong value positioning and the prevalence of household bulk purchases, which continue to drive steady demand. Despite a slowdown in volume growth as consumers increasingly explore enhanced benefits and flavor options, still water remains a cornerstone for portfolio stability among brands in the global premium water market. Its affordability and widespread availability make it an essential hydration choice, appealing to a broad spectrum of consumer demographics and ensuring consistent market performance.

Sparkling water is set to outpace all others, boasting a projected CAGR of 9.13% through 2031. This segment's rapid growth is driven by the growing popularity of zero-sugar formulations and nostalgic flavor tie-ins, positioning it as a healthier alternative to soda. The use of aluminum cans enhances their shelf visibility while aligning with the growing consumer preference for environmentally friendly packaging. Additionally, innovative product launches, such as Coca-Cola's electrolyte-rich Power Water and Spindrift's flavor-forward SKUs, which achieved a 30% year-over-year revenue increase in 2025, underscore the segment's strong growth trajectory. Aggressive marketing strategies and the continuous expansion of flavor portfolios are further accelerating the global adoption of sparkling water, solidifying its position as a key growth driver in the premium water market.

By Flavor: Unflavored Dominates, Flavored Accelerates

Unflavored bottles were the largest segment in the Premium Water market in 2025, with 71.54% market share. This segment's dominance in the market is primarily due to its perceived purity and adaptability, making it suitable for diverse consumption scenarios such as cooking and medication. The unflavored category also plays a critical role in ensuring supply-chain efficiency and maintaining consistent core volume, which reinforces its position as a staple choice among consumers. Furthermore, the neutral taste and the absence of additives align with consumers' growing inclination toward clean-label, minimally processed products, driving sustained demand in this segment.

Flavored water emerged as the fastest-growing segment, with a 7.56% CAGR projected during the forecast period. In the global premium water market, this growth is attributed to rising consumer interest in calorie-free flavor options and innovative product offerings. Leading brands, including Waterloo with its Banana Berry Bliss and Melon Medley flavors, and Sparkling Ice through its LIFE SAVERS collaboration, have effectively utilized advanced research and development and co-branding strategies to capture consumer attention. Additionally, the inclusion of functional claims, such as electrolytes and antioxidants, has broadened the segment's appeal, enabling premium pricing and encouraging trial rates. The introduction of limited-edition flavors and seasonal variants further enhances consumer engagement, fostering repeat purchases and driving growth in this segment.

By Packaging Type: Glass Surges, Aluminum Emerges

Plastic bottles accounted for the largest share of the premium water market in 2025, at 62.11%. The segment's dominance is driven by factors such as low unit costs and lightweight properties, which minimize logistics challenges. Their extensive availability and affordability make them ideal for large-scale distribution. Despite increasing environmental concerns, the segment continues to thrive due to its practicality and well-established supply chain. Additionally, advancements in recyclable PET materials and improved waste management practices are enabling companies to address sustainability challenges while maintaining cost-effectiveness. The segment also benefits from the convenience of on-the-go consumption and compatibility with high-volume production processes.

Glass packaging is projected to be the fastest-growing segment, with a forecasted CAGR of 10.48%. The segment's growth is attributed to the rising preference among eco-conscious consumers for glass, which they associate with purity and reusability. Innovations such as Vetropack’s Rezon lightweight glass, designed to reduce CO₂ emissions through optimized weight and reuse cycles, are enhancing its market appeal. While challenges such as breakage and higher freight emissions persist, advancements in lightweight engineering and the segment's premium positioning are driving its adoption. Furthermore, the increasing use of glass packaging by luxury hotels and fine-dining establishments reinforces its high-end brand perception. Regulatory pressures against single-use plastics are also encouraging brands to adopt glass as a sustainable alternative.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Off-Trade Dominates, On-Trade Premiumizes

In 2025, the off-trade segment remained the largest in the Premium Water market, accounting for 66.13% of the market share. The segment's growth is primarily driven by the widespread availability of premium water across supermarkets, convenience stores, and e-commerce platforms. Factors such as multi-pack promotions and the convenience of online shopping, particularly through platforms like Amazon and quick-commerce apps, have further supported its dominance. Additionally, exclusive flavors offered by convenience stores, such as Sparkling Ice’s Cherry Cola, have driven impulse purchases, strengthening the segment's position. Enhanced shelf visibility and effective in-store branding strategies significantly influence consumer purchasing behavior in retail settings. Furthermore, the introduction of private-label premium water products by major retailers has intensified competition while contributing to the overall growth of the category.

The on-trade segment is anticipated to be the fastest-growing in the Premium Water market, with a projected CAGR of 12.47%. This growth is driven by the increasing focus on positioning water as a curated element in dining experiences within the hospitality sector. For example, BE WTR’s reusable glass loops in Singapore exemplify the integration of sustainability with premium dining. High-end restaurants are capitalizing on this by offering water pairings priced as high as USD 115 per guest, highlighting the segment's revenue potential. The on-trade segment also enhances brand value through engaging storytelling, which reinforces premium perceptions and impacts retail channels. Collaborations between premium water brands and luxury hospitality chains are further elevating the experiential aspect of consumption, encouraging consumers to view water as a lifestyle choice and a symbol of status.

Geography Analysis

Europe emerged as the largest segment in the Premium Water market in 2025, accounting for 44.37% of the market share. This dominance is attributed to the region's established mineral-water traditions and strict quality standards. Leading brands such as S.Pellegrino and Perrier benefit from strong demand in the on-trade sector. The implementation of PFAS monitoring in 2026 is expected to increase manufacturers' compliance costs. Additionally, consumer preferences for sustainability and product provenance are driving the adoption of glass packaging and localized bottling, which also helps reduce transport emissions. Heritage branding and geographical indications further strengthen consumer trust, encouraging higher spending on premium products. The region's advanced distribution networks and a well-developed hospitality sector ensure steady demand across both retail and on-trade channels.

Asia-Pacific is projected to be the fastest-growing segment, with a robust CAGR of 9.81% forecasted through 2031. The region's rapid growth is driven by rising disposable incomes, urbanization, and increasing wellness, particularly in China and India, where social media plays a significant role in influencing consumer behavior. Functional water products, such as alkaline, protein, and black waters, are gaining popularity among health-conscious millennial consumers. The expansion of omnichannel logistics is improving last-mile delivery efficiency in densely populated urban areas, supporting the segment's growth. Furthermore, investments by global and regional players are enhancing product availability and brand visibility in emerging markets. The growing influence of Western consumption patterns and aspirations for premium lifestyles is further accelerating the adoption of high-end water products in the region.

Other regions, including North America, the Middle East and Africa, and South America, exhibit varied growth dynamics. North America remains a key market for scale and innovation, with Smartwater achieving USD 1.4 billion in sales in 2025 and the BlueTriton–Primo merger creating a nationwide network of premium brands. In the Middle East and Africa, arid climates and a growing hospitality sector are driving demand for premium imports and localized bottling, although detailed data for 2025-2026 is limited. South America presents significant opportunities, but regulatory and infrastructure challenges continue to hinder the widespread adoption of premium water products. However, increasing consumer awareness and urbanization are gradually supporting the growth of premium product adoption in these regions. Strategic partnerships and infrastructure development initiatives are expected to improve market accessibility and foster long-term growth potential.

Competitive Landscape

The premium water market is moderately fragmented, with competition between global brands and numerous regional and niche players. Prominent companies in the market include Nestlé S.A., Danone S.A., Primo Brands Corporation, The Wonderful Company LLC (recognized for FIJI Water), and PepsiCo, Inc. Global players utilize their strong brand equity, extensive distribution networks, and premium positioning to maintain a competitive edge. In contrast, smaller brands differentiate themselves by focusing on sustainability, unique water sourcing methods, and health-oriented product attributes. This competitive landscape fosters innovation and drives varied pricing strategies. Despite some regional consolidations, the global market remains highly competitive, with no single entity achieving dominance.

Market trends indicate a strategic shift toward vertical integration and ecosystem development. Companies are diversifying their portfolios by venturing into functional beverages, introducing innovative packaging solutions, and implementing sustainability initiatives. These strategies enhance competitive differentiation and align with evolving consumer preferences for environmentally responsible and health-focused products. Additionally, mergers and acquisitions are becoming more frequent as companies aim to expand their geographic presence and strengthen supply chain control. Partnerships with hospitality players and premium retail channels are also helping brands enhance visibility and reinforce their premium positioning in the market.

Emerging opportunities in the market include advancements in functional water products, sustainable packaging solutions, and direct-to-consumer subscription models. These subscription models bypass traditional retail channels, reducing markups while fostering stronger customer relationships. Additionally, the adoption of technology is accelerating across the industry. Innovations such as smart packaging, water generation systems, and digital marketing platforms enable personalized consumer engagement and improve operational efficiencies. These advancements support premium pricing strategies and position companies to meet the growing demand for high-quality, sustainable water products.

Premium Water Industry Leaders

-

Nestlé S.A.

-

Danone S.A.

-

Clear Water

-

Primo Brands Corporation

-

The Wonderful Company LLC (Fiji Water)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Tehuacán Brillante Mineral Water, originating from the Tehuacán Valley in Mexico, expanded its presence in the U.S. market. By partnering with national distributors KEHE and UNFI, the brand targeted prominent national and regional grocery chains. The water, naturally mineralized and carbonated, was marketed as a premium import, highlighting its protected source and well-balanced mineral profile.

- February 2026: Waterloo Sparkling Water, in a bid to energize its brand, had made Banana Berry Bliss and Melon Medley permanent flavors. The company also reinstated Lemon Italian Ice as a year-round offering. Tying its promotional efforts to the 2026 Winter Games, Waterloo had launched the "Wake Up With Waterloo" campaign. Additionally, in collaboration with The Bagel Nook, the brand had introduced exclusive limited-time bagel creations. Notably, Waterloo had boasted a remarkable achievement, claiming to have tripled its growth in the category in 2025.

- February 2026: Keurig Dr Pepper had unveiled Bai Barù Blood Orange, branding it as WonderWater. This offering, infused with antioxidants, tapped into the younger demographic's preference for citrus flavors, contributing to the introduction of over 35 new beverage varieties in their portfolio.

- October 2025: Powerade, a brand under Coca-Cola, launched a zero-sugar, electrolyte-infused functional water. This launch marked the brand's strategic entry into the hydration market, aiming to cater to the growing consumer demand for healthier and functional beverage options.

Global Premium Water Market Report Scope

Premium water is characterized by its premium pricing, emphasis on purity, distinctive sources, wellness benefits, and upscale packaging. They are consumed directly or used as mixers in beverages. The global premium water market is segmented by product type into still, sparkling, and functional water. By flavor segment, the market is segmented into flavored and unflavored. By packaging material, it is segmented into glass bottles, plastic bottles, aluminum cans, and other formats. By source segment, it is segmented into spring, glacial/iceberg, and other premium sources such as artesian or purified water. By distribution channel, it is segmented into on-trade and off-trade segments, with off-trade further segmented into supermarkets/hypermarkets, convenience stores, online retailers, and other off-trade channels. By geography, the premium water market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. Market sizing and forecasts are provided for each segment in terms of value (USD) and volume (liters) over the study period.

| Spring |

| Glacial/Iceberg |

| Others (Artesian, Purified/Distilled, etc.) |

| Still |

| Sparkling |

| Functional |

| Flavored |

| Unflavored |

| Glass Bottles |

| Plastic Bottles |

| Aluminum Bottles/Cans |

| Others (Bag-in-Box, Pouches) |

| On-trade (Hotels, Restaurants, Cafe's) | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others (Gas Stations) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Spring | |

| Glacial/Iceberg | ||

| Others (Artesian, Purified/Distilled, etc.) | ||

| By Product Type | Still | |

| Sparkling | ||

| Functional | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Packaging Type | Glass Bottles | |

| Plastic Bottles | ||

| Aluminum Bottles/Cans | ||

| Others (Bag-in-Box, Pouches) | ||

| By Distribution Channel | On-trade (Hotels, Restaurants, Cafe's) | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others (Gas Stations) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the Premium Water market expected to grow through 2031?

The Premium Water market is projected to advance at an 8.23% CAGR over 2026-2031 based on Mordor Intelligence estimates.

Which region will contribute the most incremental value by 2031?

Asia-Pacific is forecast to post the highest CAGR at 9.81%, outpacing all other regions as disposable incomes and wellness trends drive premium adoption.

What packaging formats are gaining traction in premium segments?

Lightweight glass bottles and aluminum cans are accelerating, with glass growing at 10.48% CAGR.

Why are functional and flavored waters becoming popular?

Consumers seek zero-sugar taste variety and added benefits such as electrolytes, vitamins, or protein, prompting rapid uptake of sparkling and functional sub-segments.

How are companies addressing sustainability concerns?

Strategies include recyclable or reusable packaging, localized bottling to cut transport emissions, and carbon-neutral operations as showcased by Icelandic Glacial and BE WTR.