Precision Oncology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

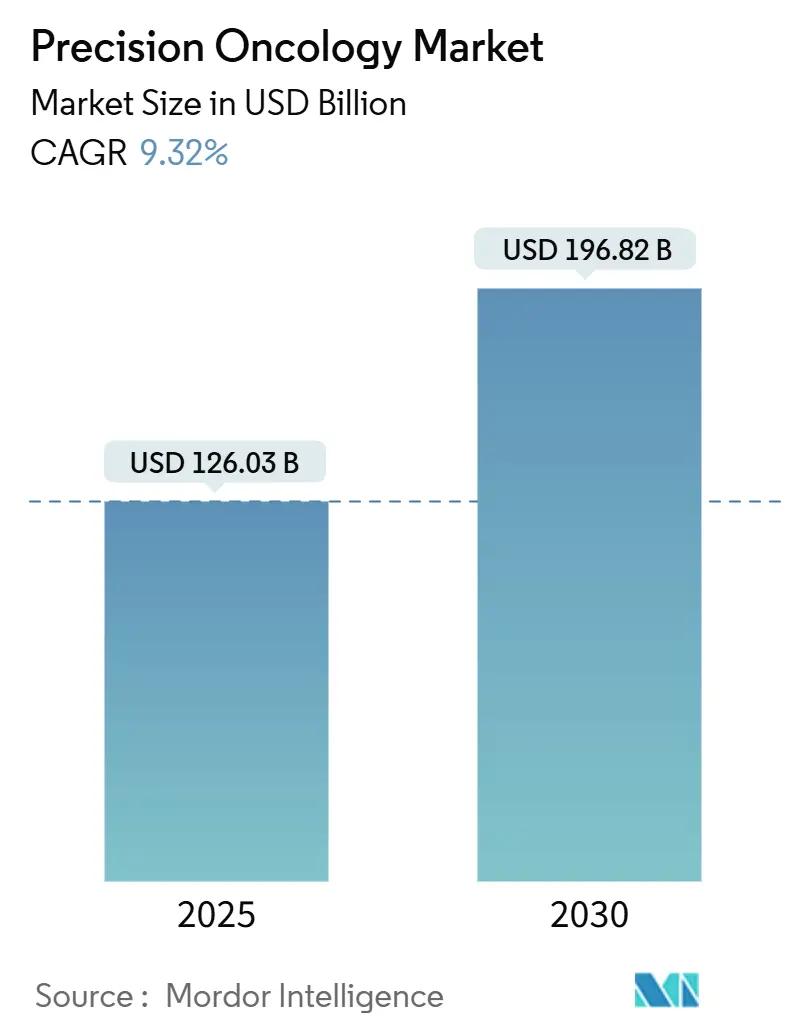

| Market Size (2025) | USD 126.03 Billion |

| Market Size (2030) | USD 196.82 Billion |

| Growth Rate (2025 - 2030) | 9.32% CAGR |

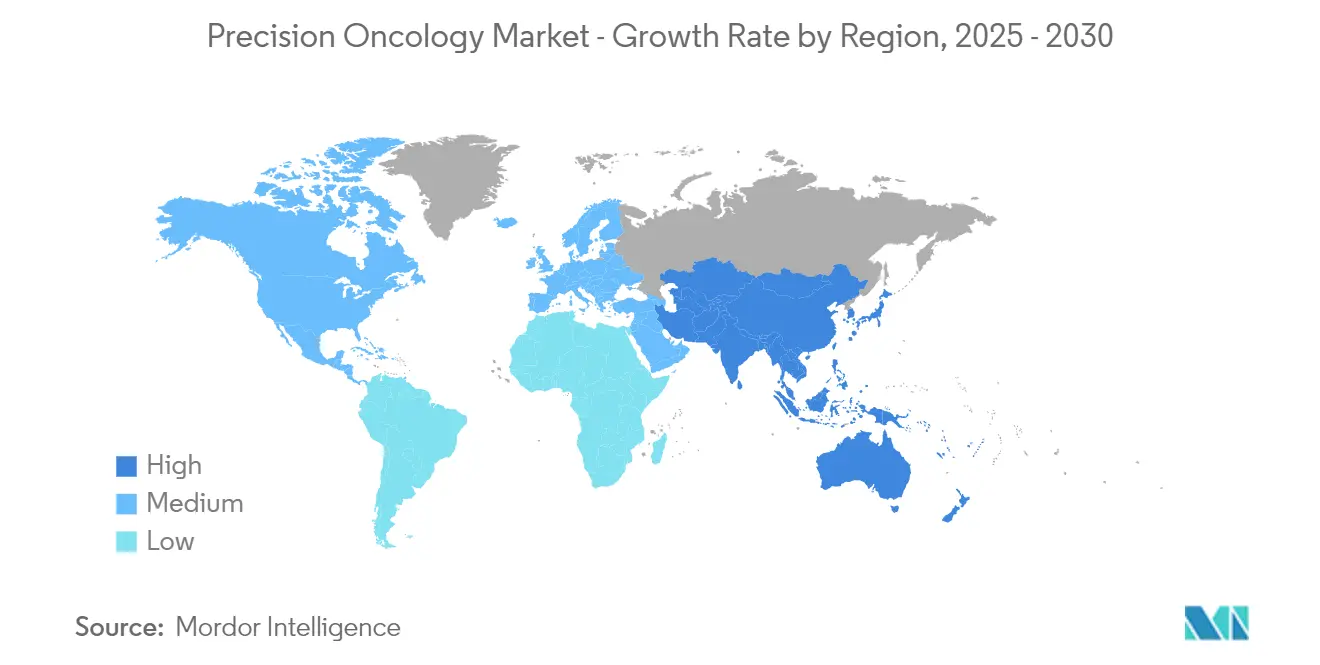

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Precision Oncology Market Analysis by Mordor Intelligence

The Precision Oncology Market size is estimated at USD 126.03 billion in 2025, and is expected to reach USD 196.82 billion by 2030, at a CAGR of 9.32% during the forecast period (2025-2030).

Precision Oncology Market Overview

The precision oncology landscape is experiencing a transformative shift driven by the convergence of multiple technologies and treatment modalities. The integration of artificial intelligence, nanotechnology, and digital health tools has revolutionized cancer diagnosis and treatment planning, with predictive analytics playing an increasingly crucial role in identifying high-risk patients. According to an article published in January 2025 in the Digital Medicine journal, new technologies, combined with artificial intelligence (AI) and machine learning (ML) techniques, are swiftly propelling precision oncology forward, enhancing both diagnostic methods and treatment strategies for cancer patients. The growing demand for precision oncology is driven by the need for more accurate, personalized cancer care solutions, which are increasingly prioritized by healthcare providers and pharmaceutical companies aiming to improve patient outcomes and optimize resource allocation.

The field has witnessed significant advancement in biomarker research and molecular diagnostics, with academic institutions and clinical practitioners increasingly collaborating on biomarker discovery initiatives. In July 2023, Australia launched PrOSPeCT (Precision Oncology Screening Platform Enabling Clinical Trials), which stands as Australia's largest cancer genomics initiative, aiming to transform cancer treatment and offer renewed hope to patients facing challenging cancers. By championing precision medicine, the program brings together Australia's leading cancer institutes, researchers, industry stakeholders, and government entities. It also extends free genomic profiling to 23,000 Australians grappling with advanced or incurable cancers, such as sarcomas, ovarian, and pancreatic cancers. Initiated by OMICO, PrOSPeCT is a groundbreaking endeavor that aims to meld genomic technology with pioneering clinical trials, making precision oncology accessible across population.

This trend has accelerated the translation of research findings into clinical applications, with diagnostic companies developing more sophisticated testing panels that can simultaneously analyze multiple genetic markers. The integration of these comprehensive molecular profiling capabilities into routine clinical practice has substantially improved treatment selection and patient outcomes.

International collaborations and cross-border research initiatives have emerged as key drivers of innovation in the precision oncology sector. For instance, in November 2024, the establishment of the LC-SCRUM-Asia network, comprising over 150 hospitals, has created an extensive genomic screening infrastructure that facilitates rapid patient enrollment in clinical trials and accelerates the development of targeted therapies. This collaborative approach has led to more efficient drug development processes and faster commercialization of novel treatments, with approximately 40% reduction in traditional drug development timelines reported by leading pharmaceutical companies in 2024.

The evolution of healthcare delivery systems has significantly influenced the precision oncology landscape, with integrated care models becoming increasingly prevalent. Modern hospitals and diagnostic centers are investing heavily in advanced molecular diagnostic capabilities and digital infrastructure to support precision oncology programs. The implementation of sophisticated data analytics platforms has enabled healthcare providers to better interpret complex genomic data and make more informed treatment decisions.

Global Precision Oncology Market Trends and Insights

Advancements in Genomic Sequencing and Artificial Intelligence

The precision oncology market is experiencing significant growth driven by revolutionary advances in genomic sequencing technologies and artificial intelligence applications. The integration of AI-powered diagnostic tools has dramatically improved cancer detection accuracy and treatment planning capabilities, as evidenced by innovations like Ataraxis AI's diagnostic tool launched in October 2024, which demonstrated a 30% higher accuracy rate compared to current standards in breast cancer care. These technological breakthroughs are enabling healthcare providers to analyze complex genomic data more efficiently and accurately, leading to more precise treatment recommendations and improved patient outcomes. The convergence of next-generation sequencing technologies with machine learning algorithms has created powerful platforms for identifying specific genetic mutations and predicting treatment responses.

The continuous evolution of AI applications in precision oncology has expanded beyond diagnostics into drug discovery and clinical trial optimization. Major technology companies and healthcare institutions are investing heavily in developing sophisticated AI models that can process vast amounts of genomic data and identify novel therapeutic targets. For instance, in April 2024, Illumina Inc.'s FDA approval of its TruSight Oncology comprehensive test, which analyzes over 500 genes in solid tumors, represents a significant advancement in making comprehensive genomic profiling more accessible to clinicians. These technological innovations are not only accelerating the drug development process but also enabling more personalized treatment approaches by helping clinicians match patients with the most effective targeted therapies based on their unique genetic profiles.

Increasing Cancer Prevalence and Supportive Government Initiatives

The rising global cancer burden has prompted governments worldwide to increase their support for precision oncology research and implementation. As per the American Cancer Society's 2025 projections, the United States is set to witness a rise in new cancer cases, with estimates jumping to 2.04 million from 1.9 million in 2023. This increasing cancer incidence is expected to drive the demand for precision oncology solutions, as healthcare providers and stakeholders focus on personalized treatment approaches to improve patient outcomes and address the growing burden of cancer effectively.

Government support extends beyond funding to include policy frameworks and healthcare infrastructure development that facilitate the adoption of precision oncology approaches. For instance, the National Institutes of Health's launch of the Cancer Screening Research Network in February 2024 demonstrates the commitment to evaluating emerging technologies, including multi-cancer detection blood tests. This initiative, which will involve 24,000 participants in the Vanguard Study, aims to validate new screening methods that could transform early cancer detection capabilities. Such comprehensive government support is essential in overcoming barriers to implementation and ensuring broader access to precision oncology solutions across different healthcare settings and patient populations.

Strategic Collaborations and Regulatory Approvals

The precision oncology landscape is being transformed by an increasing number of strategic collaborations between pharmaceutical companies, biotechnology firms, and diagnostic companies. These partnerships are accelerating the development and commercialization of innovative precision oncology solutions. A notable example is the April 2023 collaboration between Flare Therapeutics and Caris Life Sciences, which focuses on advancing precision oncology pipeline approaches across five therapeutic programs through innovative molecular profiling techniques. These strategic alliances are crucial in combining complementary expertise and resources to address complex challenges in cancer treatment and accelerate the development of targeted therapies.

The regulatory landscape has also evolved to support rapid advancement in precision oncology, with authorities demonstrating increased efficiency in reviewing and approving novel treatments. In August 2024, the FDA approved several groundbreaking therapies and combination treatments, including dostarlimab-gxly for advanced endometrial cancer and trastuzumab deruxtecan-nxki for HER2-positive solid tumors. The establishment of expedited review pathways for precision oncology products has been instrumental in bringing innovative treatments to market more quickly. For instance, Agilent Technologies' launch of the SureSelect Cancer CGP Assay in April 2023, designed for somatic variant profiling across multiple solid tumor types, exemplifies how regulatory support for advanced diagnostic tools is enabling more precise patient stratification and treatment selection.

Precision Oncology Market Type Segment Analysis

Therapeutics Segment in Precision Oncology Market

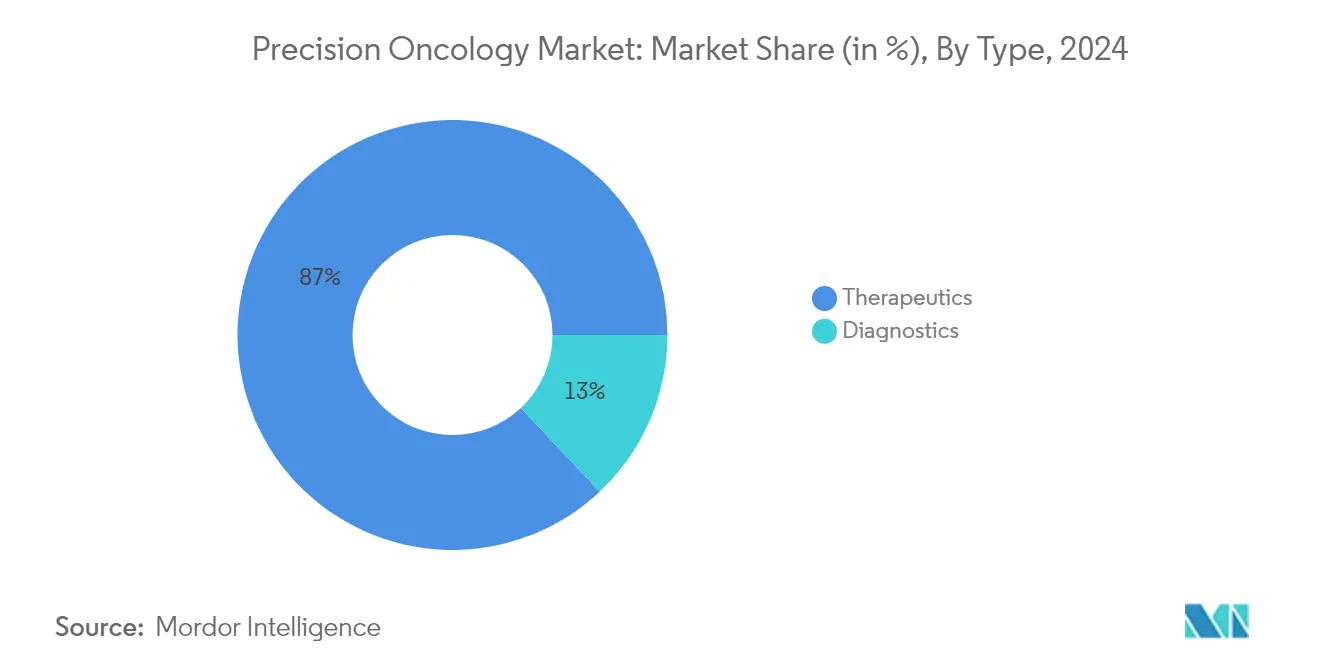

The therapeutics segment dominates the precision oncology market, commanding approximately 87% of the market share in 2024. This substantial market position is primarily driven by the increasing adoption of targeted therapy approaches and personalized treatment protocols in cancer care. The segment's prominence is further strengthened by continuous technological advancements in drug development and delivery systems, particularly in areas such as immunotherapy and molecular targeted agents. Strategic collaborations between pharmaceutical companies and research institutions have resulted in an expanded pipeline of precision therapeutics, contributing to the segment's market leadership. The integration of artificial intelligence and machine learning in drug discovery processes has accelerated the development of novel therapeutic solutions, while regulatory approvals for innovative treatment options have sustained market growth. Additionally, the rising prevalence of various cancer types and supportive government initiatives have created a favorable environment for therapeutic advancement in precision oncology.

Diagnostics Segment in Precision Oncology Market

The diagnostics segment emerges as the fastest-growing segment in the precision oncology market and is projected to expand at a significant CAGR over the forecast period. This remarkable growth trajectory is fueled by rapid advancements in genomic sequencing technologies and the increasing emphasis on early cancer detection. The integration of artificial intelligence and machine learning algorithms has revolutionized diagnostic accuracy and efficiency, making precision diagnostics more accessible and reliable. Growing awareness about the benefits of early cancer detection and personalized treatment planning has significantly boosted the adoption of diagnostic solutions. The segment's expansion is further supported by increasing investments in research and development of novel diagnostic tools, particularly in liquid biopsy and molecular testing. Technological innovations in companion diagnostics and the development of more sophisticated biomarker testing methods have created new opportunities for market growth. Moreover, the rising demand for non-invasive diagnostic procedures and the increasing focus on preventive healthcare have contributed to the segment's accelerated growth rate.

Precision Oncology Market Cancer Type Segment Analysis

Lung Cancer Segment in Precision Oncology Market

In 2024, the breast cancer segment has established itself as the dominant contributor within the precision oncology market, capturing a significant market share. This remarkable position is fueled by increasing awareness of personalized medicine approaches and the development of innovative targeted therapies. The segment's expansion is particularly driven by advances in genomic profiling technologies and the growing adoption of companion diagnostic tests for breast cancer treatment selection. Recent breakthroughs in identifying novel biomarkers and the development of more effective targeted therapies have significantly contributed to this growth momentum. The segment is further bolstered by strong research initiatives and clinical trials focusing on precision medicine approaches for various breast cancer subtypes. The integration of artificial intelligence and machine learning in breast cancer diagnostics and treatment planning has also emerged as a key growth catalyst.

Breast Cancer Segment in Precision Oncology Market

The lung cancer segment is projected to exhibit the highest growth rate in the precision oncology market. This growth trajectory underscores the growing focus on targeted therapies and advancements in precision medicine tailored to address the complexities of lung cancer. This substantial market position is primarily driven by the high global prevalence of lung cancer and the increasing adoption of targeted therapies. The segment's leadership is further strengthened by significant technological advancements in biomarker testing and companion diagnostics specifically designed for lung cancer treatments. Recent developments in liquid biopsy technologies have particularly enhanced the segment's position by enabling early detection and monitoring of lung cancer progression. The segment has also benefited from the introduction of novel precision therapeutics targeting specific genetic mutations common in lung cancer, such as EGFR, ALK, and ROS1. Additionally, the increasing success rates of immunotherapy treatments in lung cancer patients have contributed to the segment's market dominance.

Precision Oncology Market End User Segment Analysis

Hospital Segment in Precision Oncology Market

The hospital segment maintains its dominant position in the precision oncology market, commanding a significant share in 2024. This leadership position is primarily attributed to hospitals' comprehensive infrastructure for cancer treatment, including dedicated oncology departments and specialized care units. The segment's strength is further reinforced by hospitals' ability to integrate various precision oncology services, from diagnostic testing to treatment administration, under one roof. Advanced hospital systems have increasingly adopted precision medicine approaches, implementing molecular tumor boards and specialized precision oncology programs. The segment's robust performance is also supported by hospitals' established partnerships with pharmaceutical companies and diagnostic laboratories, enabling access to cutting-edge precision oncology solutions. Additionally, hospitals serve as primary points of care for cancer patients, managing both initial diagnosis and ongoing treatment protocols. The segment's market position is further strengthened by hospitals' capability to handle complex precision oncology procedures and maintain sophisticated electronic health record systems that facilitate personalized treatment approaches.

Pharmaceutical & Biotechnology Companies Segment in Precision Oncology Market

The pharmaceutical and biotechnology companies segment is emerging as the fastest-growing sector in the precision oncology market. This remarkable growth is driven by increasing investments in precision medicine research and development, particularly in targeted therapies and biomarker-driven drug development. The segment's expansion is fueled by strategic collaborations between pharmaceutical companies and diagnostic manufacturers, creating integrated precision oncology solutions. Companies are increasingly focusing on developing companion diagnostics alongside targeted therapies, enhancing treatment efficacy and patient outcomes. The segment's growth is further accelerated by advancements in artificial intelligence and machine learning applications in drug discovery and development. Rising adoption of precision medicine approaches in clinical trials and drug development programs contributes significantly to the segment's rapid expansion. Additionally, pharmaceutical and biotech companies are actively expanding their precision oncology portfolios through mergers, acquisitions, and licensing agreements, further driving segment growth.

Precision Oncology Market Geography Analysis

Precision Oncology Market in North America

North America maintains its dominant position in the global precision oncology market, commanding approximately 45% of the market share in 2024. The region's leadership is underpinned by its robust healthcare infrastructure and extensive network of research institutions. The presence of major pharmaceutical companies and biotechnology firms has created a fertile ground for innovation in precision oncology treatments. The region benefits from sophisticated diagnostic capabilities, advanced genomic sequencing facilities, and well-established clinical trial networks. Additionally, favorable reimbursement policies and increasing adoption of personalized medicine approaches by healthcare providers have accelerated market growth. The strong focus on research and development, coupled with substantial investment in oncology-focused startups, continues to drive technological advancement in the field. Furthermore, the region's regulatory framework, particularly the FDA's support for breakthrough designations and accelerated approvals, has facilitated faster market entry for innovative precision oncology solutions.

Precision Oncology Market in Europe

Europe represents a significant market for precision oncology, demonstrating robust growth over the forecast period. The region's market expansion is driven by strong healthcare systems and increasing government support for precision medicine initiatives. The European market benefits from extensive collaboration between academic institutions, healthcare providers, and pharmaceutical companies, fostering innovation in personalized cancer treatments. Countries like Germany, France, and the UK lead the regional market with their advanced healthcare infrastructure and significant investments in genomic research. The region's commitment to healthcare digitalization and the integration of artificial intelligence in cancer diagnostics has enhanced the adoption of precision oncology solutions. Furthermore, the presence of well-established biotech clusters and research centers has created an ecosystem conducive to developing innovative cancer treatments. The European Union's initiatives to standardize genetic testing and biomarker analysis across member states have also contributed to market growth.

Precision Oncology Market in Asia Pacific

The Asia Pacific precision oncology market is poised for remarkable expansion and is projected to grow at a notable pace. The region's growth trajectory is supported by rapidly evolving healthcare infrastructure and increasing investment in advanced medical technologies. Countries like Japan, China, and South Korea are leading the regional market with their significant investments in healthcare technology and research facilities. The large patient population and increasing healthcare awareness have created substantial opportunities for market expansion. Growing private sector participation and government initiatives to promote precision medicine have strengthened the market foundation. The region's emerging economies are witnessing increased adoption of next-generation sequencing technologies and molecular diagnostics. Additionally, the rising number of cancer research centers and clinical laboratories has enhanced the accessibility of precision oncology solutions. The growing collaboration between international pharmaceutical companies and local healthcare providers has further accelerated market development.

Precision Oncology Market in Middle East and Africa

The Middle East and Africa region presents an emerging market for precision oncology, characterized by growing healthcare investments and increasing focus on advanced medical technologies. The region's market is driven by significant healthcare infrastructure development, particularly in GCC countries. Major medical hubs in countries like Saudi Arabia and the UAE are leading the adoption of precision oncology solutions through substantial investments in healthcare technology and research facilities. The region benefits from increasing government initiatives to improve cancer care and rising private sector participation in healthcare delivery. Growing awareness about personalized medicine and improving access to advanced diagnostic facilities have created new opportunities for market expansion. The establishment of specialized cancer treatment centers and partnerships with international healthcare providers has enhanced the quality of cancer care. Additionally, medical tourism initiatives and improving healthcare insurance coverage have contributed to market growth.

Precision Oncology Market in South America

South America's precision oncology market is experiencing steady growth, driven by improving healthcare infrastructure and increasing awareness about personalized medicine approaches. The region is witnessing a gradual shift towards more sophisticated cancer treatment methodologies, supported by growing investment in healthcare technology. Countries like Brazil and Argentina are leading the regional market with their expanding healthcare facilities and increasing adoption of advanced diagnostic technologies. The region benefits from growing partnerships between international pharmaceutical companies and local healthcare providers, facilitating knowledge transfer and technology adoption. Rising healthcare expenditure and improving access to advanced cancer treatments have created new opportunities for market expansion. Furthermore, the increasing focus on medical tourism and the establishment of specialized cancer treatment centers have contributed to market development. The region's growing middle class and improving insurance coverage for advanced treatments are also driving market growth.

Competitive Landscape

Top Companies in the Precision Oncology Market

The precision oncology market is led by several prominent players, including Thermo Fisher Scientific Inc., Labcorp (Invitae Corporation), Illumina Inc., Qiagen, Novartis AG, and F. Hoffmann-La Roche AG, among others. These companies are focusing on continuous product innovation through significant investments in research and development of novel diagnostic tools and therapeutic solutions. Strategic collaborations and partnerships, particularly between pharmaceutical companies and diagnostic manufacturers, have become increasingly common to develop comprehensive precision medicine solutions. Companies are expanding their geographical presence through distribution agreements and regional partnerships while simultaneously working on operational optimization through digital transformation and automation. The industry has also witnessed a strong focus on developing AI and machine learning capabilities to enhance diagnostic accuracy and treatment effectiveness.

Market Dominated by Global Research Leaders

The precision oncology market exhibits a moderately consolidated structure dominated by large multinational corporations with extensive research capabilities and global distribution networks. These established players possess significant advantages in terms of technological expertise, regulatory compliance capabilities, and established relationships with healthcare providers and research institutions. The market has witnessed increasing consolidation through strategic acquisitions, particularly of innovative biotech startups and specialized diagnostic companies, as larger players seek to expand their technological capabilities and product portfolios.

The competitive dynamics are characterized by a mix of large pharmaceutical conglomerates and specialized biotech firms, with regional players maintaining strong positions in specific geographic markets or therapeutic areas. Market entry barriers are substantial due to high research and development costs, stringent regulatory requirements, and the need for extensive clinical validation. The industry has seen a trend toward vertical integration, with companies seeking to control multiple aspects of the precision oncology value chain, from diagnostic testing to therapeutic development and delivery.

Innovation and Integration Drive Future Success

Success in the precision oncology market increasingly depends on companies' ability to integrate multiple technologies and deliver comprehensive solutions that combine diagnostic accuracy with therapeutic effectiveness. Market leaders are focusing on developing platform technologies that can support multiple cancer types and treatment modalities, while also investing in data analytics capabilities to better understand treatment outcomes and patient responses. Companies are also emphasizing the development of companion diagnostics and biomarker-driven approaches to enhance treatment precision and effectiveness, while building stronger relationships with healthcare providers and payers to ensure market access and reimbursement.

For new entrants and smaller players, success lies in identifying and focusing on specific market niches where they can develop distinctive capabilities and competitive advantages. This includes specializing in particular cancer types, developing novel biomarker approaches, or creating innovative delivery mechanisms for precision therapies. Companies must also navigate evolving regulatory frameworks, particularly around genetic testing and data privacy, while building robust evidence generation capabilities to demonstrate clinical utility and cost-effectiveness. The ability to form strategic partnerships with larger players, while maintaining technological independence and innovation capabilities, will be crucial for long-term success in this dynamic market.

Precision Oncology Industry Leaders

-

F. Hoffmann-La Roche AG

-

Illumina Inc.

-

Labcorp (Invitae Corporation)

-

Novartis AG

-

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Omico, a not-for-profit leader in genomics, unveiled a pioneering model aimed at making cutting-edge cancer treatments accessible and routine for Australians grappling with rare and complex cancers. The Precision Oncology Health System Incubator (PrO-HSI) charts a strategic investment route, leveraging multi-sector funding and existing policy frameworks. Its goal is to seamlessly weave advanced therapies into current cancer care, all while safeguarding public resources in light of a shrinking taxpayer base and an ageing demographic.

- December 2024: At the Aster Cancer Conclave 2024, Aster DM Healthcare, an integrated healthcare provider in India, unveiled three significant initiatives: Precision Oncology Clinics, the Aster Cancer Grid, and Onco Collect. These initiatives signify a major leap forward in India's cancer treatment landscape. The conclave, which drew prominent oncologists, researchers, and industry experts from both national and international arenas, showcased the forefront of advancements in cancer care and treatment.

- March 2024: Bayer and Aignostics GmbH unveiled a strategic partnership, harnessing artificial intelligence (AI) for precision oncology drug research and development. Aignostics, a spin-off from the renowned Charité-Universitätsmedizin Berlin hospital, stands at the forefront of computational pathology, adeptly translating intricate biomedical data into actionable biological insights.

Global Precision Oncology Market Report Scope

As per the scope of the report, precision oncology involves profiling tumors at the molecular level to pinpoint alterations that can be targeted. It is the practice of tailoring treatment plans based on a patient's genetic structure and the specific molecular traits of their cancer.

The precision oncology market is segmented by type, cancer type, end user, and geography. By type, the market is segmented into therapeutics and diagnostics. By cancer type, the market is segmented into breast cancer, lung cancer, colorectal cancer, prostate cancer, and other types of cancer. By end user, the market is segmented into hospitals, diagnostic laboratories, pharmaceutical & biotechnology companies, and research & academic institutes. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD) for the above segments.

| Therapeutics |

| Diagnostics |

| Breast Cancer |

| Lung Cancer |

| Colorectal Cancer |

| Prostate Cancer |

| Other Cancer Types |

| Hospitals |

| Diagnostic Laboratories |

| Pharmaceutical & Biotechnology Companies |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Therapeutics | |

| Diagnostics | ||

| By Cancer Type | Breast Cancer | |

| Lung Cancer | ||

| Colorectal Cancer | ||

| Prostate Cancer | ||

| Other Cancer Types | ||

| By End-user | Hospitals | |

| Diagnostic Laboratories | ||

| Pharmaceutical & Biotechnology Companies | ||

| Research & Academic Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Precision Oncology Market?

The Precision Oncology Market size is expected to reach USD 126.03 billion in 2025 and grow at a CAGR of 9.32% to reach USD 196.82 billion by 2030.

What is the current Precision Oncology Market size?

In 2025, the Precision Oncology Market size is expected to reach USD 126.03 billion.

Which is the fastest growing region in Precision Oncology Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Precision Oncology Market?

In 2025, the North America accounts for the largest market share in Precision Oncology Market.

What years does this Precision Oncology Market cover, and what was the market size in 2024?

In 2024, the Precision Oncology Market size was estimated at USD 114.28 billion. The report covers the Precision Oncology Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Precision Oncology Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: