| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 56.87 Billion |

| Market Size (2030) | USD 72.34 Billion |

| CAGR (2025 - 2030) | 4.93 % |

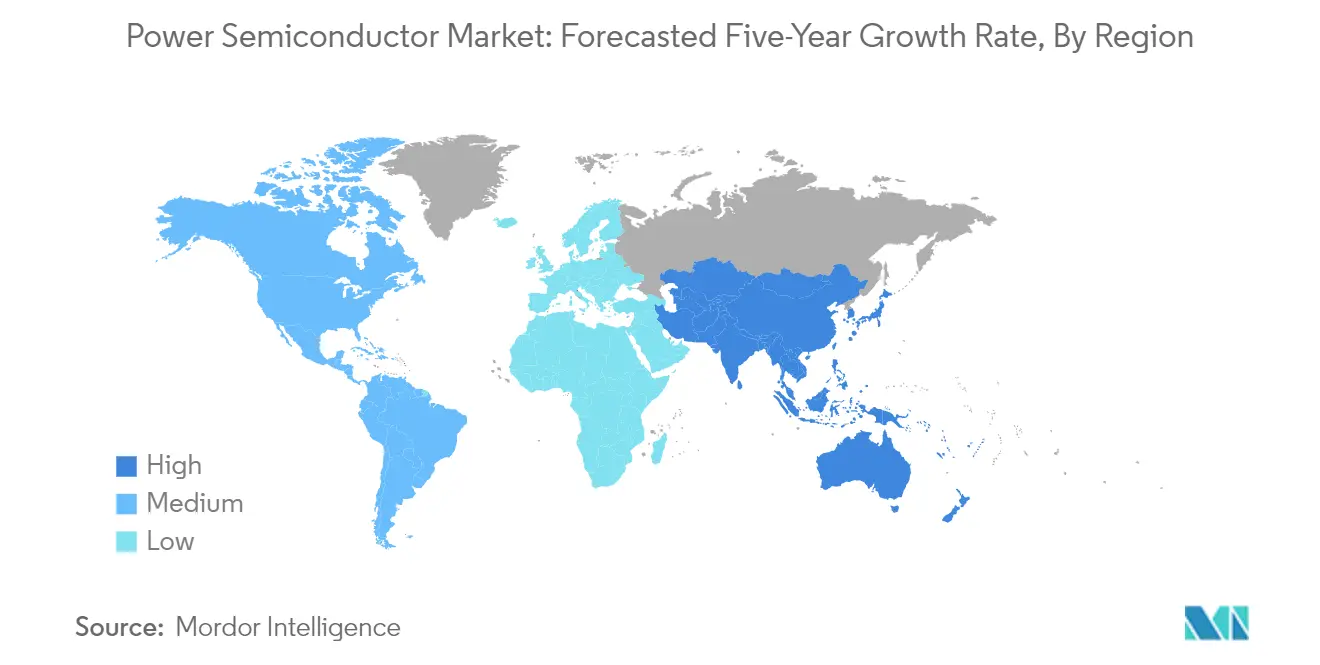

| Fastest Growing Market | Asia |

| Largest Market | Asia |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Power Semiconductor Market Analysis

The Power Semiconductor Market size is estimated at USD 56.87 billion in 2025, and is expected to reach USD 72.34 billion by 2030, at a CAGR of 4.93% during the forecast period (2025-2030).

The power semiconductor industry is experiencing significant transformation driven by increasing defense spending and technological advancements in semiconductor manufacturing. According to the US Congressional Budget Office, defense outlays reached USD 746 billion in 2023 and are projected to increase to USD 1.1 trillion by 2033, representing 6% of the country's GDP by 2024. This substantial increase in defense spending is driving investments in advanced power semiconductor technologies for military applications, including radar systems, communication equipment, and aerospace applications. The industry is witnessing a shift toward more sophisticated power electronics solutions to meet the demanding requirements of modern defense systems.

The industry is facing challenges in silicon wafer supply, which has led to increased focus on manufacturing efficiency and alternative materials. According to SEMI Silicon Manufacturers Group, global silicon wafer shipments declined to 2,834 million square inches in Q1 2024, representing a 13.2% decrease compared to the same quarter of the previous year. This supply constraint has accelerated the development of advanced manufacturing processes and the exploration of alternative semiconductor materials, pushing manufacturers to innovate and optimize their production capabilities.

Wide bandgap semiconductors, particularly silicon carbide semiconductors (SiC) and gallium nitride semiconductors (GaN), are emerging as game-changing technologies in the power semiconductor landscape. These materials offer superior properties compared to traditional silicon, including higher efficiency, faster switching speeds, and better thermal conductivity. The industry is witnessing increased adoption of these materials in high-power applications, with manufacturers investing heavily in research and development to improve their performance and reduce production costs.

The telecommunications sector is driving significant innovation in power semiconductor technologies, particularly with the expansion of 5G networks. According to Ericsson's mobility report, global 5G subscriptions are projected to exceed 5.3 billion by 2029, accounting for 58% of all mobile subscriptions. This rapid expansion of 5G infrastructure is creating substantial demand for advanced power electronics capable of handling high-frequency operations while maintaining energy efficiency. The industry is responding with new generations of power devices specifically designed to meet the demanding requirements of 5G base stations and related telecommunications equipment.

Power Semiconductor Market Trends

Increasing Demand for Consumer Electronics and Wireless Communications

The surge in consumer electronics adoption and wireless communication technologies is driving significant demand for power semiconductors across multiple applications. Power semiconductors play a crucial role in electric vehicles, with components like power MOSFETs and IGBTs serving as power electronic switches in vehicle powertrains. This is evidenced by the robust growth in electric vehicle markets, which saw sales approaching 14 million units in 2023, with market share surging from 4% in 2020 to 18% by 2023. The first quarter of 2024 has already witnessed global electric car sales exceeding 3 million units, marking a 25% increase compared to 2023, with projections indicating approximately 17 million electric vehicles will be sold by the end of 2024.

The expansion of 5G infrastructure has emerged as another significant driver for power semiconductor demand. The deployment of 5G technology requires efficient power management IC solutions, particularly in base stations and communication equipment. For instance, China's deployment of 5G infrastructure has reached a critical stage, with the number of 5G base stations amounting to 3.38 million by the end of 2023. Power semiconductors are essential in these applications for managing high-frequency operations, controlling power consumption, and ensuring reliable performance in wireless communication systems. The increasing integration of advanced driver-assistance systems (ADAS), including adaptive cruise control, lane assistance, and collision avoidance systems, further amplifies the demand for power semiconductors in automotive electronics applications.

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand for Energy-Efficient Battery-Powered Portable Devices

The escalating demand for energy-efficient, battery-powered portable devices is driving innovation in power semiconductor technology, particularly in power management ICs and battery management systems. These semiconductors are crucial for extending battery life and improving overall device efficiency in applications ranging from smartphones and tablets to wearable devices and portable medical equipment. Power management ICs play a vital role in stabilizing and converting variable voltage outputs from power sources into consistent and usable power, while also enhancing energy storage efficiency and facilitating power distribution across various portable applications.

The trend toward miniaturization and increased functionality in portable devices has intensified the need for advanced power semiconductor solutions that can deliver improved power density while maintaining high efficiency. Power semiconductors, such as MOSFETs and IGBTs, are being optimized for lower power consumption and enhanced thermal performance in battery-powered applications. These components are particularly crucial in managing power requirements for features like high-resolution displays, multiple sensors, and wireless connectivity in portable devices. The integration of power semiconductors enables sophisticated power management features, including dynamic voltage scaling and power gating, which are essential for maximizing battery life while maintaining optimal performance in modern portable devices.

Segment Analysis: By Component

Power IC Segment in Power Semiconductor Market

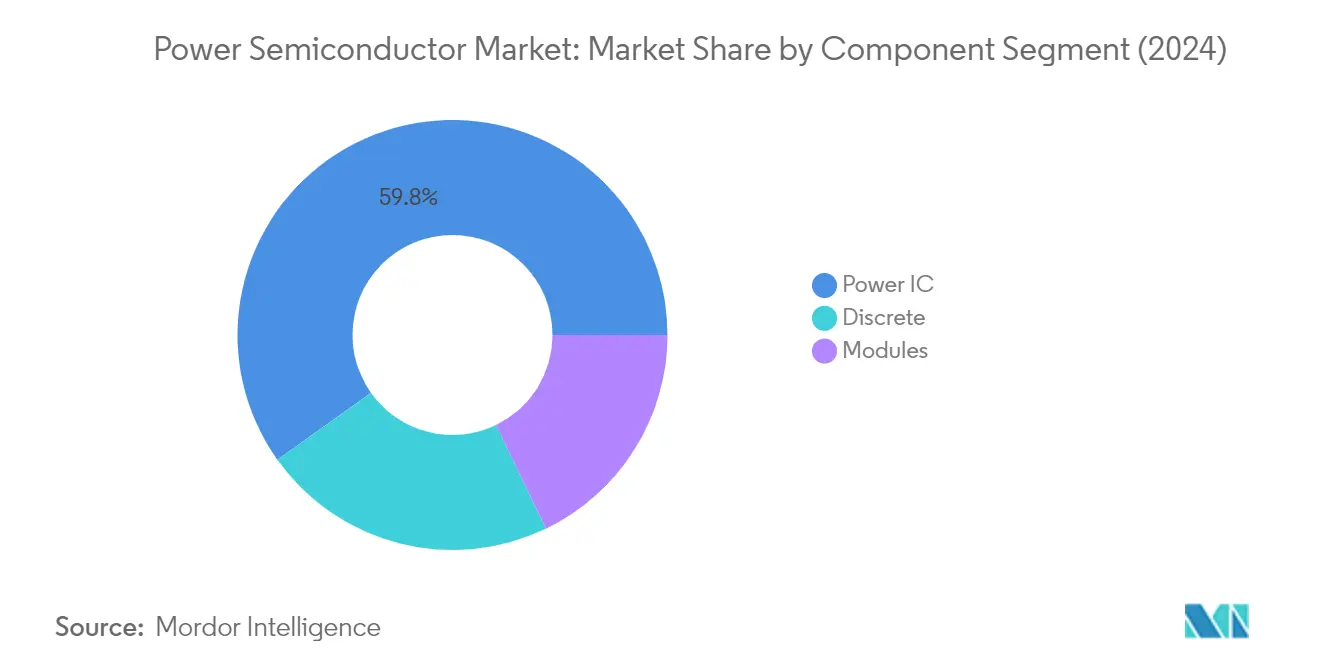

The Power IC segment dominates the global power semiconductor market, commanding approximately 60% of the market share in 2024. This significant market position is attributed to the segment's crucial role in various applications, including voltage regulation, battery management, and power conversion across multiple industries. Power ICs have become increasingly important in modern electronic devices, offering integrated solutions that combine multiple power management IC functions into single chips. The segment's prominence is particularly evident in consumer electronics, automotive applications, and industrial systems, where these components enable efficient power distribution and management. The growing demand for sophisticated power management solutions in smartphones, tablets, and other portable devices continues to drive the segment's dominance, while the increasing adoption of electric vehicles and renewable energy systems further reinforces its market leadership.

Modules Segment in Power Semiconductor Market

The Power Modules segment is emerging as the fastest-growing segment in the power semiconductor market, projected to grow at approximately 7% during the forecast period 2024-2029. This robust growth is primarily driven by the increasing adoption of power modules in electric vehicles, renewable energy systems, and industrial applications. The segment's growth is further accelerated by technological advancements in module design, particularly in IGBT and power MOSFET modules, which offer improved thermal management and higher power density. The automotive sector's transition towards electrification has created a substantial demand for power modules, as they are essential components in electric vehicle powertrains and charging systems. Additionally, the expansion of renewable energy infrastructure and the growing need for efficient power conversion in industrial applications continue to fuel the segment's rapid growth trajectory.

Remaining Segments in Power Semiconductor Market by Component

The Power Discrete segment represents a significant portion of the power semiconductor market, playing a vital role in various applications requiring individual power management components. This segment includes essential components such as rectifiers, bipolar transistors, power MOSFETs, and IGBTs, each serving specific functions in power control and conversion applications. Discrete components are particularly valued in applications where customized power solutions are required, offering flexibility in design and implementation. The segment maintains its importance in industrial applications, consumer electronics, and automotive systems, where individual components are preferred for their reliability and specific performance characteristics. The continued innovation in discrete component technology, particularly in areas such as silicon carbide and gallium nitride-based devices, ensures the segment's ongoing relevance in the power semiconductor landscape.

Segment Analysis: By Material

Silicon/Germanium Segment in Power Semiconductor Market

The Silicon/Germanium segment continues to dominate the global power semiconductor market, commanding approximately 84% market share in 2024. This segment's prominence is attributed to silicon's widespread availability, cost-effectiveness, and established manufacturing processes. Silicon's remarkable versatility as a semiconductor material, coupled with its highly effective semiconducting capabilities and inherent strength and stability, makes it particularly suitable for power electronics applications. The segment's dominance is further reinforced by its extensive application across various sectors, including consumer electronics, automotive, and industrial applications. Silicon power semiconductors are extensively utilized in smartphones, tablets, laptops, and other portable devices, contributing to power efficiency and enabling longer battery life and faster charging capabilities.

Gallium Nitride (GaN) Segment in Power Semiconductor Market

The Gallium Nitride (GaN) segment is experiencing remarkable growth in the power semiconductor market, projected to expand at an impressive CAGR of approximately 29% during 2024-2029. GaN's superior characteristics, including high electron mobility, a wide bandgap of 3.5eV, and exceptional switching capabilities, are driving its adoption across various applications. The technology's ability to operate at elevated temperatures exceeding 200°C, combined with its capacity to handle high power levels with low electrical losses, positions it as a transformative force in the industry. The segment's growth is particularly accelerated by its increasing implementation in power conversion systems, electric vehicles, renewable energy applications, and RF power amplifiers, where its unique properties enable significant improvements in system efficiency and performance.

Remaining Segments in Power Semiconductor Market by Material

The Silicon Carbide (SiC) segment represents a crucial component of the power semiconductor market, bridging the gap between traditional silicon-based devices and emerging GaN technology. SiC technology offers significant advantages in high-power and high-temperature applications, making it particularly valuable in electric vehicles, renewable energy systems, and industrial motor drives. The material's superior thermal conductivity and lower on-state resistance have made it increasingly popular in applications requiring efficient power conversion and management. The segment's growth is driven by its ability to enable smaller, more efficient power systems while maintaining high reliability and performance standards.

Segment Analysis: By End-User Industry

Consumer Electronics Segment in Power Semiconductor Market

The consumer electronics segment dominates the global power semiconductor market, commanding approximately 29% market share in 2024. This significant market position is driven by the increasing integration of power semiconductors in smartphones, tablets, laptops, home appliances, and smart home devices. The segment's growth is further bolstered by the rising demand for efficient power management solutions in portable electronic devices, where power semiconductors like power MOSFETs and PMICs play crucial roles in battery management and power optimization. The adoption of advanced technologies such as GaN semiconductors in consumer electronics has enabled the development of sleeker designs, enhanced wireless charging capabilities, and improved thermal management systems. Major manufacturers are continuously introducing innovative power semiconductor products specifically designed for consumer electronics applications, focusing on reducing power consumption while improving overall device performance and reliability.

Automotive Segment in Power Semiconductor Market

The automotive segment is emerging as the fastest-growing sector in the power semiconductor market, projected to grow at a CAGR of approximately 7% during 2024-2029. This remarkable growth is primarily attributed to the accelerating adoption of electric vehicles (EVs) and the increasing integration of advanced driver assistance systems (ADAS). The segment's expansion is further driven by the automotive industry's shift towards electrification, with power semiconductors playing a crucial role in various applications including powertrain systems, battery management, and motor control. The development of SiC semiconductors and gallium nitride (GaN) based power semiconductors has revolutionized EV design, enabling higher efficiency and improved thermal performance. Major automotive manufacturers are forming strategic partnerships with semiconductor companies to ensure stable supply chains and develop innovative power solutions for next-generation vehicles.

Remaining Segments in End-User Industry

The power semiconductor market encompasses several other significant segments including industrial, power, IT and telecommunication, military and aerospace, and other end-user industries. The industrial segment plays a vital role in applications such as factory automation, robotics, and uninterruptible power supplies. The power sector utilizes these semiconductors in renewable energy systems, smart grids, and power distribution networks. In the IT and telecommunication sector, power semiconductors are essential for data centers, 5G infrastructure, and communication equipment. The military and aerospace segment employs these components in defense systems, avionics, and satellite communications. Each of these segments contributes uniquely to the market's dynamics, driven by specific technological requirements and regulatory standards that shape their adoption and implementation patterns.

Power Semiconductor Market Geography Segment Analysis

Power Semiconductor Market in China

China dominates the global power semiconductor market landscape, commanding approximately 36% of the market share in 2024 while demonstrating remarkable growth potential with a projected CAGR of nearly 6% from 2024 to 2029. The nation's prominence is largely attributed to its position as a global powerhouse for consumer electronics and household appliances manufacturing. China's proactive policies emphasizing technological progress and innovation have spurred significant investments in R&D from both public and private entities. The country's automotive sector, particularly its leadership in electric vehicle adoption, has been a crucial driver of market growth. The government's push toward carbon neutrality by 2060 has catalyzed the demand for power electronics, especially in the electric vehicle segment. Furthermore, China's aggressive expansion of 5G infrastructure, with over 3.38 million base stations by the end of 2023, has created substantial demand for power semiconductors in telecommunications applications. The nation's data center sector has also emerged as a significant consumer of power semiconductors, with China maintaining its position as the fourth-largest data center market globally.

Power Semiconductor Market in the United States

The United States maintains its position as a crucial hub in the global power semiconductor industry, driven by its extensive automotive and electronics manufacturing base. The nation's semiconductor manufacturing industry benefits from a robust infrastructure supporting manufacturing, design, and research activities. The implementation of the CHIPS Act has catalyzed significant investments in semiconductor manufacturing capabilities, with major initiatives including the establishment of new fabrication facilities and research centers. The country's strong focus on electric vehicle adoption, supported by government incentives and infrastructure development, has created substantial demand for power semiconductors in automotive applications. The rapid expansion of renewable energy infrastructure, particularly in solar and wind power installations, has further boosted market growth. The United States has also witnessed significant advancement in data center development and cloud computing infrastructure, driving demand for efficient power management solutions. Additionally, the country's leadership in technological innovation, particularly in wide bandgap semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN), has positioned it at the forefront of next-generation power semiconductor development.

Power Semiconductor Market in Japan

Japan's power semiconductor market is characterized by its strong foundation in electronic products manufacturing and technological innovation. The country's robust manufacturing landscape, anchored by industry giants like Sony and Panasonic, continues to drive significant demand for power semiconductors in consumer electronics applications. Japan's aggressive pursuit of carbon neutrality has led to substantial investments in renewable energy infrastructure, creating new opportunities for power semiconductor applications. The nation's automotive industry has been particularly active in electric vehicle development, with major manufacturers increasing their focus on electrification technologies. Japan's commitment to industrial automation and robotics, supported by initiatives like Society 5.0, has created additional demand for power semiconductors in industrial applications. The country's emphasis on energy efficiency and power management in electronic devices has driven innovation in power semiconductor technologies. Furthermore, Japan's strong research and development capabilities, coupled with its established semiconductor manufacturing infrastructure, have enabled the development of advanced power semiconductor solutions for emerging applications.

Power Semiconductor Market in Other Countries

The power semiconductor market demonstrates significant diversity across other regions, each with unique drivers and characteristics. South Korea has established itself as a prominent player, leveraging its advanced communication technology infrastructure and strong presence in consumer electronics manufacturing. Taiwan's market is distinguished by its world-leading semiconductor manufacturing capabilities and comprehensive ecosystem. European countries, particularly Germany and France, have shown strong growth potential driven by their automotive and industrial sectors. The rest of Asia-Pacific, including countries like India, Singapore, and Malaysia, is experiencing rapid growth fueled by increasing electronics manufacturing activities and digital infrastructure development. Latin American countries, particularly Mexico and Brazil, are emerging as significant markets due to their growing automotive manufacturing base. The Middle East and African regions are gradually developing their semiconductor capabilities, focusing on applications in renewable energy and industrial automation. These diverse markets collectively contribute to the global power semiconductor ecosystem, each bringing unique strengths and opportunities for growth.

Get Analysis on Important Geographic Markets

Download PDF

Power Semiconductor Industry Overview

Top Companies in Power Semiconductor Market

The power semiconductor market is led by established players like Infineon, OnSemi, STMicroelectronics, Mitsubishi, and Fuji Electric, who are driving innovation through continuous research and development investments. These power semiconductor companies are focusing on expanding their product portfolios with advanced technologies like Silicon Carbide (SiC) and Gallium Nitride (GaN) to meet the growing demand for efficient power management solutions. Strategic facility expansions and manufacturing capacity increases are being undertaken to strengthen market presence, particularly in high-growth regions like Asia-Pacific. Companies are also emphasizing partnerships and collaborations to enhance their technological capabilities and market reach, while simultaneously investing in digital infrastructure to improve customer experience and operational efficiency. The industry leaders are particularly targeting emerging applications in automotive electrification, renewable energy, and industrial automation sectors through dedicated product development initiatives.

Consolidated Market with Strong Regional Players

The power semiconductor market exhibits a relatively consolidated structure, dominated by global conglomerates with extensive manufacturing capabilities and robust distribution networks. These major players leverage their integrated operations, spanning from research and development to end-user distribution, while regional specialists maintain strong positions in specific geographic markets or product niches. The market has witnessed significant merger and acquisition activities, particularly aimed at expanding technological capabilities and geographic reach, with companies seeking to strengthen their positions in emerging technologies like wide-bandgap semiconductors. The formation of strategic alliances and joint ventures has become increasingly common, especially for developing next-generation power semiconductor solutions.

The competitive landscape is characterized by a mix of diversified electronics manufacturers and specialized semiconductor companies, each bringing unique strengths to the market. While global leaders maintain their dominance through extensive product portfolios and strong customer relationships, specialized players are carving out niches in specific applications or regions. The industry has seen increased collaboration between established players and technology startups, particularly in developing innovative solutions for emerging applications. Manufacturing capabilities and intellectual property portfolios play crucial roles in determining competitive positions, with companies investing heavily in both areas to maintain their market standing.

Innovation and Adaptability Drive Market Success

Success in the power semiconductor market increasingly depends on companies' ability to innovate while maintaining operational efficiency and supply chain resilience. Market leaders are strengthening their positions through continuous investment in research and development, focusing on both product innovation and manufacturing process improvements. Companies are also expanding their presence in high-growth application areas like electric vehicles and renewable energy, while simultaneously maintaining strong positions in traditional markets. The ability to offer comprehensive solutions, rather than individual components, has become increasingly important, with successful companies developing integrated product ecosystems and application-specific solutions.

For new entrants and smaller players, success lies in identifying and focusing on specific market niches where they can establish strong competitive positions. This includes developing specialized solutions for emerging applications or focusing on specific geographic markets where they can build strong customer relationships. Companies must also navigate complex regulatory environments, particularly regarding environmental standards and energy efficiency requirements, while managing concentration risk in their customer base. The ability to maintain flexible manufacturing capabilities and robust supply chains has become crucial, particularly in light of recent global disruptions. Success also increasingly depends on developing strong partnerships across the value chain, from raw material suppliers to end-users.

Power Semiconductor Market Leaders

-

Infineon Technologies AG

-

Texas Instruments Inc.

-

STMicroelectronics NV

-

NXP Semiconductors NV

-

Qorvo Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Power Semiconductor Market News

- June 2024 - Infineon Technologies AG unveiled the CoolGaN Transistor 700 V G4 product family. These devices excel in power conversion, specifically in the 700 V voltage range. These transistors boast a 20% performance boost in input and output figures-of-merit. This enhancement translates to heightened efficiency, minimized power losses, and more economical solutions. The applications span from consumer chargers and notebook adapters to data center power supplies, renewable energy inverters, and battery storage solutions.

- June 2024 - Elliott, a USD 65 billion hedge fund renowned for its shareholder activism, injected USD 2.5 billion into Texas Instruments. The fund advocates a more flexible approach to capital expenditures to boost the company's free cash flow. In a detailed 13-page letter obtained by CNBC, Elliott suggested Texas Instruments implement a "dynamic capacity-management strategy." As per Elliott, this strategy could potentially elevate the company's free cash flow to USD 9 per share by 2026.

Power Semiconductor Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain/supply Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.5 Technology Snapshot

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Demand for Consumer Electronics and Wireless Communications

- 5.1.2 Growing Demand for Energy-Efficient Battery-powered Portable Devices

-

5.2 Market Restraints

- 5.2.1 Shortage of Silicon Wafers and Variable Driving Requirement

6. MARKET SEGMENTATION

-

6.1 By Component

- 6.1.1 Discrete

- 6.1.1.1 Rectifier

- 6.1.1.2 Bipolar

- 6.1.1.3 MOSFET

- 6.1.1.4 IGBT

- 6.1.1.5 Other Discrete Components (Thyristor and HEMT)

- 6.1.2 Modules

- 6.1.2.1 Thyristor

- 6.1.2.2 IGBT

- 6.1.2.3 MOSFET

- 6.1.3 Power IC

- 6.1.3.1 Multichannel PMICS

- 6.1.3.2 Switching Regulators (AC/DC, DC/DC, Isolated and Non-isolated)

- 6.1.3.3 Linear Regulators

- 6.1.3.4 BMICs

- 6.1.3.5 Other Components

-

6.2 By Material

- 6.2.1 Silicon/Germanium

- 6.2.2 Silicon Carbide (SiC)

- 6.2.3 Gallium Nitride (GaN)

-

6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Consumer Electronics

- 6.3.3 IT and Telecommunication

- 6.3.4 Military and Aerospace

- 6.3.5 Power

- 6.3.6 Industrial

- 6.3.7 Other End-user Industries

-

6.4 By Geography***

- 6.4.1 United States

- 6.4.2 Europe

- 6.4.3 Japan

- 6.4.4 China

- 6.4.5 South Korea

- 6.4.6 Taiwan

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Infineon Technologies AG

- 7.1.2 Texas Instruments Inc.

- 7.1.3 Qorvo Inc.

- 7.1.4 STMicroelectronics NV

- 7.1.5 NXP Semiconductors NV

- 7.1.6 ON Semiconductor Corporation

- 7.1.7 Renesas Electronics Corporation

- 7.1.8 Broadcom Inc.

- 7.1.9 Toshiba Corporation

- 7.1.10 Mitsubishi Electric Corporation

- 7.1.11 Fuji Electric Co. Ltd

- 7.1.12 Semikron International

- 7.1.13 Wolfspeed Inc.

- 7.1.14 Rohm Co. Ltd

- 7.1.15 Vishay Intertechnology Inc.

- 7.1.16 Nexperia Holding BV (Wingtech Technology Co. Ltd)

- 7.1.17 Alpha & Omega Semiconductor

- 7.1.18 Magnachip Semiconductor Corp.

- 7.1.19 Microchip Technology Inc.

- 7.1.20 Littlefuse Inc.

8. VENDORS MARKET SHARE ANALYSIS

9. INVESTMENT ANALYSIS

10. FUTURE OF THE MARKET

**Subject to Availability

***The Geography segment in the Final Report will also include 'Rest of the World' subsegment

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Power Semiconductor Industry Segmentation

A power semiconductor is used as a switch or rectifier in power electronics. It plays a crucial role in controlling and converting electrical power in electronic circuits. The market is defined by the revenue generated from sales of various components of power semiconductors like discrete, module, and power IC, using various materials like silicon/germanium, silicon carbide (SiC), and gallium nitride (GaN). They are employed in a diverse range of global end-user industries like automotive, consumer electronics, IT and telecommunication, military and aerospace, power, industrial, and others.

The power semiconductor market is segmented by component (discrete [rectifier, bipolar, MOSFET, IGBT, and other discrete components], modules [thyristor, IGBT, and MOSFET], power IC [multichannel PMICs, switching regulators (AC/DC, DC/DC, isolated and non-isolated), linear regulators, BMICs, other components]), material (silicon/ germanium, silicon carbide (SiC), gallium nitride (GaN)), end-user industry (automotive, consumer electronics, IT & telecommunications, military and aerospace, power, industrial, and other end-user industries), and geography (United States, Europe, Japan, China, South Korea, Taiwan, Rest of the World). The market sizes and value (USD) forecasts for all segments are provided.

| By Component | Discrete | Rectifier | |

| Bipolar | |||

| MOSFET | |||

| IGBT | |||

| Other Discrete Components (Thyristor and HEMT) | |||

| Modules | Thyristor | ||

| IGBT | |||

| MOSFET | |||

| Power IC | Multichannel PMICS | ||

| Switching Regulators (AC/DC, DC/DC, Isolated and Non-isolated) | |||

| Linear Regulators | |||

| BMICs | |||

| Other Components | |||

| By Material | Silicon/Germanium | ||

| Silicon Carbide (SiC) | |||

| Gallium Nitride (GaN) | |||

| By End-user Industry | Automotive | ||

| Consumer Electronics | |||

| IT and Telecommunication | |||

| Military and Aerospace | |||

| Power | |||

| Industrial | |||

| Other End-user Industries | |||

| By Geography*** | United States | ||

| Europe | |||

| Japan | |||

| China | |||

| South Korea | |||

| Taiwan | |||

Need A Different Region or Segment?

Customize Now

Power Semiconductor Market Research FAQs

How big is the Power Semiconductor Market?

The Power Semiconductor Market size is expected to reach USD 56.87 billion in 2025 and grow at a CAGR of 4.93% to reach USD 72.34 billion by 2030.

What is the current Power Semiconductor Market size?

In 2025, the Power Semiconductor Market size is expected to reach USD 56.87 billion.

Who are the key players in Power Semiconductor Market?

Infineon Technologies AG, Texas Instruments Inc., STMicroelectronics NV, NXP Semiconductors NV and Qorvo Inc. are the major companies operating in the Power Semiconductor Market.

Which is the fastest growing region in Power Semiconductor Market?

Asia is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Power Semiconductor Market?

In 2025, the Asia accounts for the largest market share in Power Semiconductor Market.

What years does this Power Semiconductor Market cover, and what was the market size in 2024?

In 2024, the Power Semiconductor Market size was estimated at USD 54.07 billion. The report covers the Power Semiconductor Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Power Semiconductor Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Power Semiconductor Market Research

Mordor Intelligence offers a comprehensive analysis of the power semiconductor industry. We leverage decades of expertise in power electronics research and consulting. Our extensive coverage includes crucial technologies such as IGBT, power MOSFET, and power module solutions. Additionally, we explore emerging wide bandgap semiconductor innovations, including silicon carbide semiconductor and gallium nitride semiconductor technologies. The report provides detailed insights into power management IC developments, power converter applications, and power discrete components. This information is available in an easy-to-download report PDF format.

Our analysis benefits stakeholders across the power electronics industry. It serves manufacturers of power transistor and power diode components, as well as developers of smart power device solutions. The report examines automotive semiconductor trends and power integrated circuit advancements. It also covers the evolution of power device technologies. Comprehensive coverage includes detailed analysis of SiC semiconductor and GaN semiconductor applications, power rectifier developments, and emerging opportunities in the power IC sector. This provides actionable insights for strategic decision-making across the value chain.