| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 2.74 Billion |

| Market Size (2030) | USD 4.38 Billion |

| CAGR (2025 - 2030) | 9.78 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Power Module Packaging Market Analysis

The Power Module Packaging Market size is estimated at USD 2.74 billion in 2025, and is expected to reach USD 4.38 billion by 2030, at a CAGR of 9.78% during the forecast period (2025-2030).

The power module packaging industry is experiencing significant transformation driven by global semiconductor manufacturing initiatives and technological advancements. Major investments are reshaping the manufacturing landscape, exemplified by Intel's announcement in 2023 to invest over USD 33 billion in Germany as part of its European expansion strategy. The industry is witnessing a fundamental shift in packaging technologies, with increased focus on silicon carbide (SiC) and gallium nitride (GaN) based solutions. These advanced materials are enabling higher switching frequencies, improved thermal management, and enhanced power density, which are particularly crucial for next-generation applications.

The integration of advanced packaging technologies is revolutionizing power module package designs, with innovations in substrate materials, die-attach methods, and cooling solutions. The industry is seeing a transition from traditional wire bonding to advanced interconnect technologies like copper clip and silver sintering, enabling better thermal performance and reliability. Manufacturers are increasingly adopting planar interconnect technology and pressure-based bondless connections, which offer enhanced reliability and reduced parasitic inductance. These technological advancements are particularly significant as they enable the development of more compact and efficient power module packages.

The global push towards renewable energy integration is creating unprecedented demands for power module packaging solutions. China leads this transformation with an impressive 228 gigawatts of solar capacity and 310 gigawatts of wind capacity, surpassing the rest of the world combined. The industry is responding with innovative module packaging solutions optimized for renewable energy applications, including advanced thermal management systems and high-reliability designs suitable for harsh environmental conditions. This shift is driving the development of more robust and efficient packaging solutions capable of handling higher power densities and operating temperatures.

The market is witnessing a significant evolution in materials and manufacturing processes, with a focus on sustainability and efficiency. According to the International Energy Agency, annual clean energy investment needs to increase to approximately USD 4 trillion by 2030 to achieve net zero emissions goals. This has spurred innovation in packaging materials, with manufacturers exploring alternatives to traditional materials for better performance and environmental sustainability. The industry is seeing increased adoption of advanced ceramic substrates, novel die-attach materials, and innovative encapsulation solutions that offer improved thermal performance while meeting stringent environmental requirements. This aligns with the growing demand in the packaging materials for IGBT and SiC modules market.

As the industry evolves, it is essential to conduct a comprehensive power packaging analysis to understand the impact of these changes on the new packages and materials for power devices market. The focus on module size and efficiency continues to drive innovation and development in this dynamic sector.

Power Module Packaging Market Trends

Increasing Demand from the Industrial and Consumer Electronics Segment

The consumer electronics industry is experiencing a significant transformation driven by the increasing demand for smarter and more advanced devices, particularly with the integration of Internet of Things (IoT) technology. According to Ericsson's projections, IoT connections are expected to reach approximately 35 billion by 2028, encompassing various connected devices such as machines, vehicles, meters, point-of-sale terminals, sensors, and consumer electronics. The proliferation of short-range IoT devices, which stood at 10.3 billion units worldwide in 2022, is anticipated to reach 25 billion by 2027, demonstrating the robust growth in smart device adoption. This surge in IoT implementation is compelling businesses to develop new products and services, subsequently driving the demand for power module packaging solutions.

The growing production and sales of consumer electronics, including refrigerators, computers, televisions, and charging devices for handheld electronics, are significantly contributing to market growth. This trend is particularly evident in major manufacturing regions like China, where the household appliance industry has evolved into a multi-billion-dollar sector. In 2022, the Chinese electrical household appliances sector achieved a market volume of approximately CNY 1.75 billion, highlighting the substantial demand for power module market in consumer electronics applications. Additionally, the integration of 5G technology in smartphones and the development of foldable smartphones are creating new opportunities for power module packaging solutions, despite temporary market fluctuations due to economic factors in 2023. The market is expected to show signs of recovery in 2024 module, driven by increased demand for 5G smartphones and expanding network connectivity across nations.

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Energy-Efficient Devices

The global push toward energy efficiency and sustainable power solutions is creating substantial demand for advanced power module packaging technologies. This trend is particularly evident in the renewable energy sector, where countries are making significant investments in solar and wind power infrastructure. For instance, China has demonstrated remarkable progress in this direction, with its solar capacity reaching 228 gigawatts (GW) and wind capacity achieving 310 GW, surpassing the combined capacity of all other countries. The commitment to renewable energy is further exemplified by China's state-owned energy companies' planned investment of USD 14.5 billion through 2025, aimed at diversifying their energy portfolio and supporting the nation's goal of achieving net-zero carbon dioxide emissions by 2060.

The drive for energy efficiency is also reflected in the development of more advanced power storage and conversion technologies. As the industry moves toward more efficient batteries and power management systems, the cost of renewable energy solutions, particularly solar energy, is expected to decrease by 66% compared to current prices. This trend is supported by government initiatives worldwide, such as India's commitment to achieving net-zero emissions by 2070 and its ambitious target of 500 gigawatts of renewable energy capacity by 2030. The Indian government's recent announcement in February 2023 to invest USD 4.3 billion toward energy transition and net-zero targets, including USD 2.57 billion allocated for increasing the production of high-efficiency solar panels, demonstrates the growing emphasis on energy-efficient solutions and their impact on power supply modules market requirements.

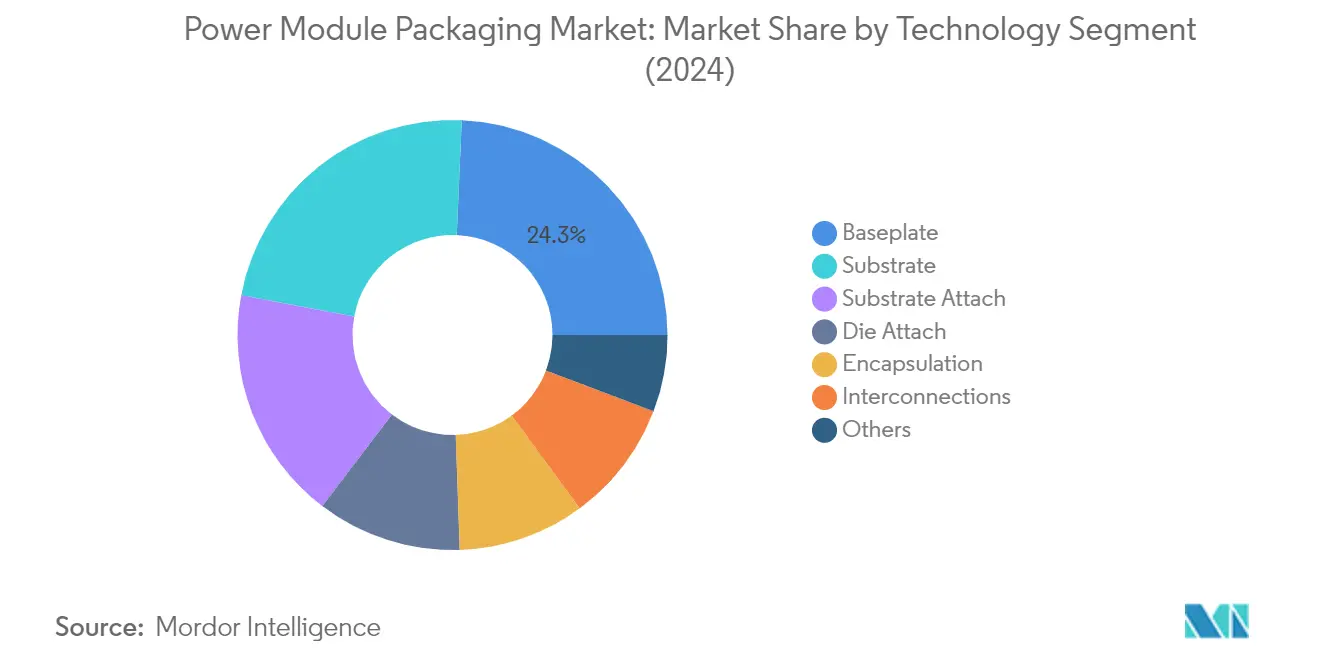

Segment Analysis: By Technology

Baseplate Segment in Power Module Packaging Market

The baseplate segment maintains its dominant position in the power module packaging market, commanding approximately 24% market share in 2024. Baseplates serve as crucial components in power module packages, acting as an interface between the superstructure and foundation while ensuring uniform distribution of loads. The segment's leadership is driven by the increasing adoption of copper and aluminum silicon carbide (AlSiC) baseplates, which offer superior thermal management capabilities. Modern baseplate designs incorporate advanced features like pin-fin or fin-cooling structures, enabling enhanced heat dissipation and improved module performance. The integration of pre-applied thermal interface material (TIM) in baseplates has further strengthened their market position by eliminating the need for thermal grease application during assembly, thereby improving manufacturing efficiency.

Interconnections Segment in Power Module Packaging Market

The interconnections segment is projected to experience the highest growth rate of approximately 15% during the forecast period 2024-2029. This remarkable growth is attributed to the increasing adoption of advanced interconnection technologies such as copper wire bonds, silver sintering, and wirebondless interconnects. The segment's expansion is further driven by the development of planar interconnect technology and pressure-based bondless connections, which offer enhanced reliability and reduced parasitic inductance. The industry's shift toward higher power densities and faster switching frequencies has necessitated innovations in interconnection methods, particularly in applications requiring improved thermal and electrical performance. The emergence of hybrid bonding techniques, including copper-to-copper direct bonding, represents a significant advancement in interconnection technology, contributing to the segment's accelerated growth.

Remaining Segments in Power Module Packaging Market

The power module packaging market encompasses several other vital segments, including substrate, die attach, substrate attach, and encapsulation technologies. The substrate segment plays a fundamental role in providing interconnections and cooling capabilities, while die attach technologies focus on securing semiconductor dies to packages with enhanced thermal and electrical properties. Substrate attach technologies contribute to overall module reliability through advanced bonding methods and materials, while encapsulation solutions provide essential protection against environmental factors. Each of these segments continues to evolve with technological advancements, particularly in areas such as thermal management, reliability enhancement, and miniaturization, collectively driving the market's growth and innovation in power packaging analysis solutions.

Power Module Packaging Market Geography Segment Analysis

Power Module Packaging Market in North America

The North American power module packaging market holds approximately 17% of the global market share in 2024, establishing itself as a significant regional market driven by technological advancements and robust semiconductor manufacturing capabilities. The region's growth is primarily fueled by developments in next-generation electric vehicles, increasing demand for consumer electronics, and the integration of semiconductor devices across various industries, particularly in industrial automation. The United States continues to dominate the North American market, supported by the government's strategic push toward increasing domestic chip production and rising semiconductor demand across multiple sectors. The market's expansion is further reinforced by substantial investments in research and development, with companies focusing on innovative packaging solutions for power modules. The presence of leading semiconductor manufacturers and advanced packaging facilities has created a strong ecosystem for market growth. Additionally, the region's focus on renewable energy integration and electric vehicle adoption has created new opportunities for power module packaging applications. The market is also benefiting from the increasing adoption of advanced technologies in automotive applications and the growing demand for efficient power management solutions in industrial applications.

Power Module Packaging Market in Europe

The European power module packaging market has demonstrated steady development, recording approximately 1% growth from 2019 to 2024, shaped by the region's strong focus on technological innovation and sustainable energy solutions. The market is characterized by significant investments in renewable energy infrastructure and the rapid adoption of electric vehicles, particularly in countries like Germany and the United Kingdom. The region's commitment to reducing greenhouse gas emissions and transitioning to cleaner energy sources has created substantial opportunities for power module packaging applications. The automotive sector remains a key driver, with European manufacturers increasingly incorporating advanced power electronics in their vehicle designs. The presence of major semiconductor manufacturers and research institutions has fostered continuous innovation in packaging technologies. The market is further strengthened by robust government support for semiconductor manufacturing and packaging capabilities, particularly through initiatives aimed at reducing dependency on external suppliers. The region's focus on industrial automation and smart manufacturing has also created sustained demand for power module packaging solutions. Additionally, the growing emphasis on energy efficiency in commercial and industrial applications continues to drive market development.

Power Module Packaging Market in Asia-Pacific

The Asia-Pacific power module packaging market is positioned for substantial expansion, with a projected growth rate of approximately 10% during 2024-2029, establishing itself as the most dynamic regional market globally. The region's dominance is underpinned by the presence of major semiconductor manufacturers, rapid industrialization, and a vast consumer electronics market. Countries like China, Japan, South Korea, and Taiwan are at the forefront of semiconductor manufacturing and packaging technologies, driving significant market growth. The region's robust automotive sector, particularly in electric vehicle manufacturing, has created substantial demand for power module packaging solutions. The presence of advanced manufacturing facilities and continuous technological innovations has positioned Asia-Pacific as a global hub for power module packaging. The market is further strengthened by significant investments in research and development, focusing on developing advanced packaging technologies. The region's strong focus on renewable energy adoption and industrial automation has created additional growth opportunities. Moreover, the presence of a well-established electronics manufacturing ecosystem and supportive government policies has created a favorable environment for market expansion.

Power Module Packaging Market in Rest of the World

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market for power module packaging, characterized by growing opportunities in renewable energy and automotive applications. The Middle East region is witnessing significant developments in the automotive industry, particularly in the luxury electric vehicle segment, creating new demands for power module packaging solutions. Countries in Latin America are increasingly adopting electric vehicles and investing in renewable energy infrastructure, driving the demand for power module packaging technologies. The market is benefiting from increasing investments in industrial automation and the growing adoption of advanced manufacturing technologies. Government initiatives to promote clean energy and sustainable transportation solutions are creating new opportunities for market growth. The region's focus on diversifying its economy and reducing dependence on traditional industries has led to increased investments in semiconductor technologies and related packaging solutions. The market is also driven by the growing demand for consumer electronics and the expansion of manufacturing capabilities in these regions. Additionally, the increasing focus on energy efficiency and sustainable development has created new applications for power module packaging solutions.

Get Analysis on Important Geographic Markets

Download PDF

Power Module Packaging Industry Overview

Top Companies in Power Module Packaging Market

The power module packaging market features prominent players like Fuji Electric, Infineon Technologies, Mitsubishi Electric, Semikron Danfoss, Amkor Technology, Hitachi, STMicroelectronics, MacMic Science & Technology, Texas Instruments, Starpower Semiconductor, and Toshiba Corporation. These companies are heavily investing in research and development to advance their technological capabilities, particularly in areas like SiC and GaN-based power modules. The industry demonstrates a strong focus on manufacturing optimization, with many players adopting vertical integration strategies to maintain better control over their supply chains and reduce costs. Companies are expanding their geographical presence through strategic partnerships and establishing new manufacturing facilities, especially in key markets across Asia-Pacific and North America. Innovation trends center around developing more efficient and compact module packaging solutions, with particular emphasis on automotive and industrial applications. Operational agility is being enhanced through investments in automated production lines and clean-room facilities, while strategic moves increasingly focus on sustainability and energy efficiency in product development.

Market Consolidation Drives Industry Evolution Pattern

The power module packaging market exhibits a relatively consolidated structure dominated by large multinational conglomerates with diverse product portfolios and strong technological capabilities. These established players leverage their extensive research and development capabilities, manufacturing expertise, and global distribution networks to maintain their market positions. Japanese and European manufacturers hold significant market share, particularly in high-end applications, while Chinese companies are rapidly expanding their presence in the mid-range segment. The market has witnessed notable merger and acquisition activities, exemplified by the formation of Semikron Danfoss, as companies seek to combine complementary technologies and expand their market reach.

The competitive landscape is characterized by a mix of integrated device manufacturers (IDMs) and specialized packaging companies, each bringing unique strengths to the market. IDMs benefit from their ability to control the entire value chain from chip design to final packaging, while specialized players excel in providing customized solutions for specific applications. Market entry barriers remain high due to substantial capital requirements, technical expertise needs, and the importance of established customer relationships. Regional players, particularly in Asia, are increasingly challenging global leaders through government support and aggressive pricing strategies, though they often focus on specific market segments rather than competing across the entire product spectrum.

Innovation and Adaptability Drive Future Success

Success in the SiC module packaging technology market increasingly depends on companies' ability to innovate while maintaining cost competitiveness. Incumbent players must focus on developing next-generation packaging technologies that address the growing demands for higher power density, improved thermal management, and enhanced reliability. Companies need to establish strong partnerships with semiconductor manufacturers and end-users to ensure their packaging solutions align with evolving requirements. The ability to offer comprehensive solutions that include design support, testing services, and after-sales support is becoming increasingly important for maintaining market position.

For emerging players and contenders, success lies in identifying and exploiting specific market niches where they can build competitive advantages. This includes focusing on emerging applications in electric vehicles, renewable energy, and industrial automation where established players may not have entrenched positions. Companies must also navigate the complex regulatory landscape, particularly regarding environmental standards and safety requirements in automotive and industrial applications. The risk of substitution remains relatively low due to the specialized nature of power module packaging, but companies must continuously innovate to address evolving customer needs and maintain their competitive edge. Building strong relationships with key customers and developing specialized expertise in high-growth application areas will be crucial for long-term success.

Power Module Packaging Market Leaders

-

Fuji Electric Co. Ltd

-

Infineon Technologies AG

-

Mitsubishi Electric Corporation (Powerex Inc.)

-

Semikron

-

Amkor Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Power Module Packaging Market News

- December 2023: Infineon Technologies AG launched the 4.5 kV XHP 3 IGBT modules in response to the global push for downsizing and integration. The 4.5 kV XHP will fundamentally change the landscape for medium voltage drives (MVD) and transportation applications operating at 2000 to 3300 V AC in 2- and 3-level topologies.

- December 2023: STMicroelectronics announced that it had signed a long-term silicon carbide (SiC) supply agreement with Li Auto. Under this agreement, STMicroelectronics would provide Li Auto with SiC MOSFET devices to support Li Auto’s strategy around high-voltage battery electric vehicles (BEVs) in various market segments.

Power Module Packaging Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHT

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 and Macroeconomic Trends on the Industry

- 4.4 Technology Snapshot

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Demand from the Industrial and Consumer Electronics Segment

- 5.1.2 Rising Demand for Energy-efficient Devices

-

5.2 Market Restraints

- 5.2.1 Market Consolidation Affecting Overall Profitability

6. MARKET SEGMENTATION

-

6.1 By Technology

- 6.1.1 Substrate

- 6.1.2 Baseplate

- 6.1.3 Die Attach

- 6.1.4 Substrate Attach

- 6.1.5 Encapsulations

- 6.1.6 Interconnections

- 6.1.7 Other Technologies

-

6.2 By Geography***

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Fuji Electric Co. Ltd

- 7.1.2 Infineon Technologies AG

- 7.1.3 Mitsubishi Electric Corporation (Powerex Inc.)

- 7.1.4 Semikron

- 7.1.5 Amkor Technology Inc.

- 7.1.6 Hitachi Ltd

- 7.1.7 STMicroelectronics NV

- 7.1.8 MacMic Science & Technology Co. Ltd

- 7.1.9 Texas Instruments Inc.

- 7.1.10 Starpower Semiconductor Ltd

- 7.1.11 Toshiba Corporation

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Power Module Packaging Industry Segmentation

A power module or power electronic module acts as a physical container for the storage of several power components, usually power semiconductor devices. The market growth is driven by a reduction in energy wastage, the use of efficient distributed cooling schemes, a reduction in footprint, and a consequent increase in power density. Moreover, the growing demand for power modules in the industrial and consumer electronics sectors is likely to drive the growth of the power module packaging market.

The power module packaging market is segmented by technology (substrate, baseplate, die-attach, substrate attach, encapsulations, interconnections, and other technologies) and geography (North America, Europe, Asia-Pacific, and the Rest of the World). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Technology | Substrate |

| Baseplate | |

| Die Attach | |

| Substrate Attach | |

| Encapsulations | |

| Interconnections | |

| Other Technologies | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Power Module Packaging Market Research FAQs

How big is the Power Module Packaging Market?

The Power Module Packaging Market size is expected to reach USD 2.74 billion in 2025 and grow at a CAGR of 9.78% to reach USD 4.38 billion by 2030.

What is the current Power Module Packaging Market size?

In 2025, the Power Module Packaging Market size is expected to reach USD 2.74 billion.

Who are the key players in Power Module Packaging Market?

Fuji Electric Co. Ltd, Infineon Technologies AG, Mitsubishi Electric Corporation (Powerex Inc.), Semikron and Amkor Technology Inc. are the major companies operating in the Power Module Packaging Market.

Which is the fastest growing region in Power Module Packaging Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Power Module Packaging Market?

In 2025, the Asia Pacific accounts for the largest market share in Power Module Packaging Market.

What years does this Power Module Packaging Market cover, and what was the market size in 2024?

In 2024, the Power Module Packaging Market size was estimated at USD 2.47 billion. The report covers the Power Module Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Power Module Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Power Module Packaging Market Research

Mordor Intelligence provides a comprehensive analysis of the power module packaging market. We leverage our extensive experience in industrial module power research and consulting. Our latest report examines the evolving landscape of power module packaging materials and technologies. This includes SiC module packaging technology and IGBT packaging materials. The analysis covers various aspects, from module size considerations to battery pack packaging solutions. It offers detailed insights into DC-DC converter power modules and their applications.

The report gives stakeholders actionable intelligence on new packages and materials for power devices. It particularly focuses on North America new packages and materials trends and the emerging Mexico intelligent power modules market. Available as an easy-to-download report PDF, our analysis includes a detailed examination of power module package innovations and converter modules developments through 2024. Industry participants benefit from our thorough assessment of power supply modules and power driver module technologies. This enables informed decision-making in this rapidly evolving sector. The report also addresses global intelligent power modules specifications and packaging materials for IGBT and SiC modules, offering valuable insights for manufacturers, suppliers, and end-users.