| Study Period | 2017 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Market Size (2024) | USD 0.68 Billion |

| Market Size (2029) | USD 1.84 Billion |

| CAGR (2024 - 2029) | 21.87 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Power and Utilities MLCC Market Analysis

The Power and Utilities MLCC Market size is estimated at 0.68 billion USD in 2024, and is expected to reach 1.84 billion USD by 2029, growing at a CAGR of 21.87% during the forecast period (2024-2029).

The power and utilities sector is undergoing a profound transformation driven by the global push toward sustainable energy solutions and grid modernization. This shift is particularly evident in China, where power consumption reached 8,637 TWh in 2022, marking a 3.6% year-over-year increase, with the industrial sector consuming 5,700 TWh and the tertiary sector reaching 1,486 TWh. The surge in energy demand, coupled with the imperative to reduce carbon emissions, has accelerated the adoption of advanced electronic components in power generation and distribution systems. This transformation is reshaping the infrastructure requirements across the utility landscape, driving the need for more sophisticated and efficient electronic components, including MLCC and energy storage capacitors.

Smart grid initiatives and advanced metering infrastructure deployments are revolutionizing utility operations and consumer engagement. In the United States, the installation of over 100 million advanced smart electric meters, with residential installations accounting for 88% of the total, demonstrates the scale of this transformation. These deployments are enabling more efficient power distribution, real-time monitoring, and improved demand response capabilities. The integration of these advanced metering systems is creating new opportunities for MLCC applications in smart grid components, particularly in areas requiring high-performance electronic components for accurate measurement and communication.

Regional renewable energy initiatives are gaining momentum, with notable achievements and commitments shaping the market landscape. The United Kingdom reached a significant milestone in May 2023 by generating its trillionth kilowatt hour of electricity from renewable sources, demonstrating the viability of large-scale renewable energy integration. This achievement is complemented by Saudi Arabia's ambitious commitment to generate 50% of its electricity from renewable sources by 2030, signaling a broader shift toward sustainable energy solutions across diverse geographic regions. These initiatives are driving substantial investments in power infrastructure and creating new applications for electronic components, such as energy storage capacitors, in renewable energy systems.

The increasing electrification of transportation is catalyzing significant changes in power utility infrastructure and grid management systems. With electric vehicle market share in the United States reaching over 6% of new car sales in the first half of 2022, utilities are rapidly adapting their infrastructure to support this growing demand. This transition is necessitating substantial upgrades to power distribution systems and creating new requirements for electronic components in charging infrastructure and grid management systems. The integration of vehicle-to-grid technologies and smart charging solutions is further driving the need for advanced electronic components, including MLCC, capable of managing complex power flows and ensuring system reliability.

Global Power and Utilities MLCC Market Trends

Stringent emission standards are expected to increase demand

- Inverter shipments increased from 62296.3 million units in 2021 to 93412.9 million units in 2022. MLCCs use a temperature-compensating ceramic with minimal capacitance variation, making them ideal for use as components in snubber circuits used in inverters that handle large voltages during switching and where compactness and heat tolerance are required.

- With growing stringent emission standards globally, automakers are gradually shifting their production from conventional engine vehicles to hybrid and electric vehicles. Inverters of various varieties, including traction inverters and soft-switching inverters, are used in electric vehicles for a variety of applications. Governments in various countries are spending heavily on electric mobility projects and encouraging customers to adopt electric vehicles, which will provide an opportunity for electric vehicle power inverter manufacturers. The rise in the demand for electric vehicles is also expected to increase the sales of the components used in electric vehicles, such as power inverters. Power generation from solar PV increased by a record 179 TWh in 2021, marking 22% growth in 2020. Solar PV accounted for 3.6% of global electricity generation, and it remains the third largest renewable electricity technology behind hydropower and wind. With the rising concerns over pollution worldwide due to industrialization, governments are introducing policies to drive solar PV deployment. For instance, in August 2022, the federal government of the United States introduced the Inflation Reduction Act, a law significantly expanding support for renewable energy in the next 10 years through tax credits and other measures.

Understand The Key Trends Shaping This Market

Download PDF

Increasing utilization of smart lighting in various applications

- LED shipments increased from 1.3 million units in 2021 to 2.65 million units in 2022. MLCCs are used in LEDs to suppress electromagnetic interference (EMI) and provide DC supply smoothing and acoustic noise reduction. MLCCs used in LEDs typically need to meet specific electrical and environmental requirements, such as high capacitance values, low equivalent series resistance (ESR), high voltage ratings, and appropriate temperature stability.

- LED lighting can be used in various applications, including commercial and residential, automotive, decorative, and outdoor lighting. The rising population leading to rising residential and commercial construction is one of the major factors that has increased the demand for various basic amenities, especially power. The COVID-19 pandemic harmed the global economy. The demand for LED lighting was lowered due to construction site suspensions and lockdowns. However, the second half of 2021 witnessed a surge in construction due to the launch of new and upgraded projects, contributing to the industry's steady recovery for LED lighting.

- In 2021, electricity consumption by lighting in the residential and services sectors grew by around 5%, which drove the increase in emissions. Although several countries began to phase out incandescent bulbs more than 10 years ago, many are now beginning to phase out fluorescent lighting to make LEDs the leading lighting technology while saving significant CO2 emissions.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Supportive government investments are expected to boost the adoption

- The growing demand for solar power is expected to stimulate market growth

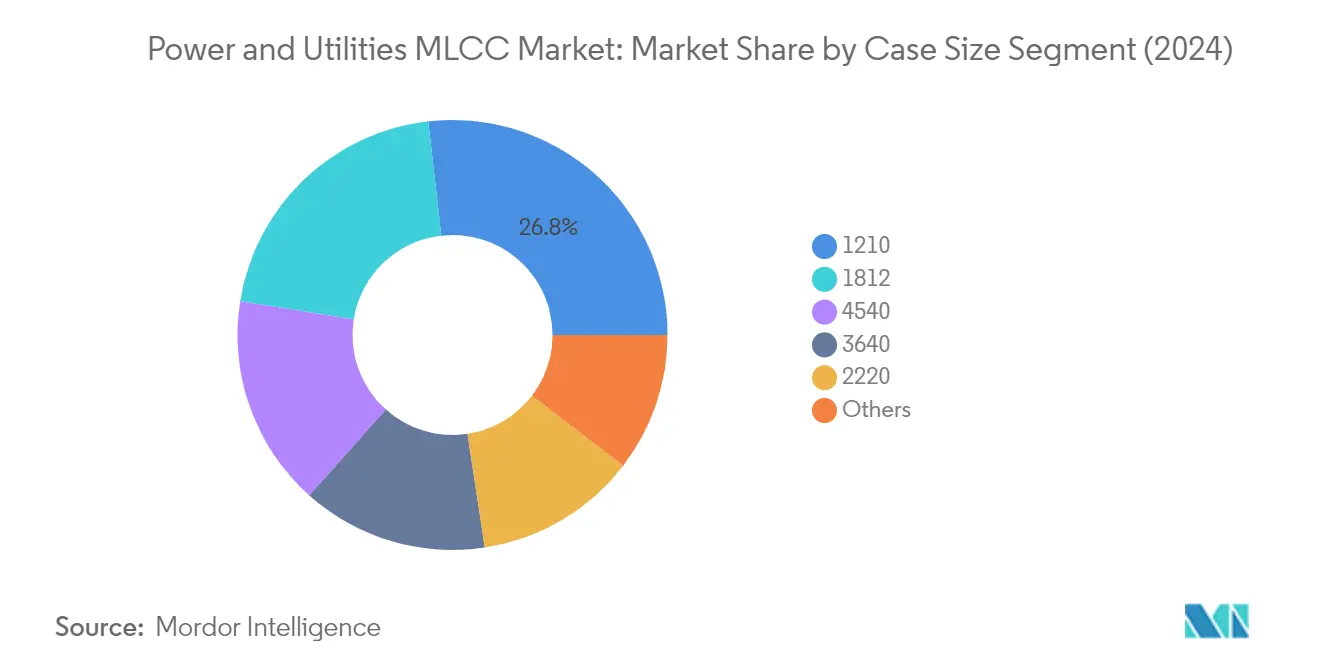

Segment Analysis: Case Size

1210 Segment in Power and Utilities MLCC Market

The 1210 case size segment dominates the power and utilities MLCC market, commanding approximately 27% market share in 2024. This segment's prominence is driven by its crucial role in enabling uninterrupted functionality and effective management of power interruptions in smart meters. The 1210 MLCCs serve as vital energy storage devices, ensuring operational continuity and protecting critical data during temporary power outages while enabling precise energy consumption monitoring. Their compact size makes them particularly well-suited for integration into space-constrained designs of modern smart meters and power management systems. The segment's strong position is further reinforced by the increasing deployment of smart grid technologies and the growing emphasis on grid modernization initiatives across various regions.

1812 Segment in Power and Utilities MLCC Market

The 1812 case size segment is experiencing remarkable growth, projected to expand at approximately 20% annually from 2024 to 2029. This accelerated growth is primarily attributed to the segment's increasing adoption in renewable energy applications, particularly in solar and wind power installations. The 1812 MLCCs are gaining traction due to their superior performance in high-voltage applications and ability to withstand harsh environmental conditions. Their robust design and reliability make them ideal for use in power conversion equipment and grid infrastructure. The segment's growth is further supported by the global push toward clean energy adoption and the increasing investments in renewable energy infrastructure, particularly in regions like Asia-Pacific where significant renewable energy projects are being implemented.

Remaining Segments in Case Size

The other case sizes, including 2220, 3640, 4540, and various other specifications, collectively serve diverse applications within the power and utilities sector. The 2220 case size is particularly valued in European markets for its role in clean energy transitions, while the 3640 size finds extensive applications in North American power distribution systems. The 4540 case size is gaining prominence in Asia's evolving energy landscape, especially in smart grid applications. The remaining specialized case sizes cater to specific requirements in various power management and utility applications, each contributing to the market's overall technological advancement and efficiency improvements in power distribution systems.

Segment Analysis: Voltage

More than 1100V Segment in Power and Utilities MLCC Market

The More than 1100V segment has established itself as the dominant force in the power and utilities MLCC market, commanding approximately 43% market share in 2024. This segment's prominence is primarily driven by the increasing adoption of high voltage MLCC applications in renewable energy infrastructure, particularly in solar photovoltaic panels and wind power systems. The segment's growth is further bolstered by government initiatives toward reducing carbon footprints and rising investments in renewable energy infrastructure worldwide. The integration of these high voltage MLCCs in smart grid technologies and power distribution systems has become crucial for ensuring system reliability and efficiency. Additionally, the segment's market position is strengthened by its essential role in supporting the modernization of power infrastructure and the growing demand for high-voltage applications in industrial power systems.

Less than 600V Segment in Power and Utilities MLCC Market

The Less than 600V segment is emerging as the fastest-growing category in the power and utilities MLCC market, with a projected growth rate of approximately 23% during 2024-2029. This remarkable growth trajectory is primarily attributed to the increasing integration of LED lighting solutions and smart meter applications across the power and utilities sector. The segment is experiencing substantial momentum due to the global transition toward energy-efficient lighting technologies and the implementation of smart grid infrastructure. The expansion is further supported by various government regulations mandating energy-efficient solutions and the growing adoption of smart meters in residential and commercial sectors. Additionally, the segment's growth is driven by its critical role in supporting low-voltage applications in renewable energy systems, particularly in solar inverters and energy storage capacitors.

Remaining Segments in Voltage Segmentation

The 600V to 1100V segment serves as a crucial intermediate voltage range in the power and utilities MLCC market, bridging the gap between low and high voltage applications. This segment plays a vital role in various power conversion and distribution systems, particularly in floating photovoltaic systems and grid infrastructure applications. The segment's significance is emphasized by its applications in power supplies, industrial automation systems, and energy management solutions. Furthermore, this voltage range is particularly important in applications requiring moderate power handling capabilities while maintaining system reliability and efficiency, making it an essential component in the broader power and utilities infrastructure landscape.

Segment Analysis: Capacitance

Less than 10 μF Segment in Power and Utilities MLCC Market

The less than 10 1⁄4F segment has established itself as the dominant force in the power and utilities MLCC market, commanding approximately 48% of the total market share in 2024. This segment's prominence is driven by its crucial role in supporting the digital transformation of power and utility infrastructure. These capacitors are instrumental in facilitating enhanced connectivity and automation across power distribution networks, particularly in smart grid applications. The evolution of the energy value chain from a linear model to a circular one has further amplified the importance of less than 10 1⁄4F MLCCs, as they play a vital role in managing bi-directional energy flows and supporting greater variability from renewable sources. The integration of 5G technology in power grids has also boosted demand for these capacitors, as they contribute to the seamless functioning of 5G-enabled devices and systems, facilitating near real-time data flow and reliable transmission of power grid data.

More than 100 μF Segment in Power and Utilities MLCC Market

The more than 100 1⁄4F segment is positioned as the fastest-growing category in the power and utilities MLCC market, projected to expand at approximately 23% CAGR from 2024 to 2029. This remarkable growth trajectory is primarily attributed to the segment's critical role in supporting the integration of renewable energy sources and advanced power management systems. The increasing adoption of solar photovoltaic systems and the growing emphasis on grid modernization initiatives are driving the demand for these high-capacity MLCCs. These components are essential in ensuring efficient power transfer, minimizing energy losses, and contributing to achieving ambitious renewable energy targets. The segment's growth is further bolstered by the rising implementation of smart grid technologies and the need for robust energy storage capacitors, where more than 100 1⁄4F MLCCs serve as crucial components in power conversion and energy management systems.

Remaining Segments in Capacitance

The 10 1⁄4F to 100 1⁄4F segment serves as a vital bridge between low and high capacitance applications in the power and utilities sector. This intermediate capacitance range is particularly important in supporting advanced metering infrastructure (AMI) and smart meter deployments. These capacitors play a crucial role in ensuring stable power supply to metering circuits, filtering out noise, and contributing to accurate energy measurements and data collection. The segment's significance is further enhanced by its applications in power distribution systems, where these capacitors help maintain voltage stability and power quality. Their role in supporting the transition to smart grid infrastructure and enabling efficient energy management systems makes them an integral part of the modern power and utilities landscape.

Segment Analysis: Dielectric Type

Class 1 Segment in Power and Utilities MLCC Market

Class 1 MLCCs have established themselves as the dominant force in the power and utilities MLCC market, commanding approximately 84% market share in 2024. This segment's prominence is driven by its vital role in ensuring the efficient operation of battery storage systems within the power and utilities industry. The increasing adoption of renewable energy sources, particularly wind and solar power, has necessitated grid-scale storage solutions where Class 1 MLCCs are integral components. These capacitors are especially crucial in AC/DC power adapters, serving as essential components underpinning the seamless operation of power and utility infrastructure. Their significance extends to the stability and performance of grid-scale storage facilities, where they contribute to the overall efficiency and reliability of power distribution systems. The Investment and Infrastructure Act (IIJA)'s substantial investment of USD 7 billion into domestic battery and component manufacturing has further strengthened the position of Class 1 MLCCs in the market.

Class 2 Segment in Power and Utilities MLCC Market

The Class 2 segment is experiencing remarkable growth, projected to expand at approximately 26% annually from 2024 to 2029. This impressive growth trajectory is primarily driven by the accelerating adoption of electric vehicles (EVs) and the corresponding expansion of charging infrastructure. The segment's growth is further bolstered by federal and state government initiatives, such as the Biden administration's target of achieving a 50% EV market share by 2030 and California's requirement for 100% zero-emission vehicles by 2035. The deployment of 500,000 fast-charging stations across the United States, supported by the Investment and Infrastructure Act (IIJA), is creating substantial demand for Class 2 MLCCs, which are essential components in the electrical systems and control circuits of these charging stations. The segment's growth is also supported by the increasing focus on integrating vehicles with the grid, spreading out demand over time, and upgrading distribution system equipment, where Class 2 MLCCs play a crucial role in ensuring reliable and efficient grid-to-vehicle connections.

Power and Utilities MLCC Market Geography Segment Analysis

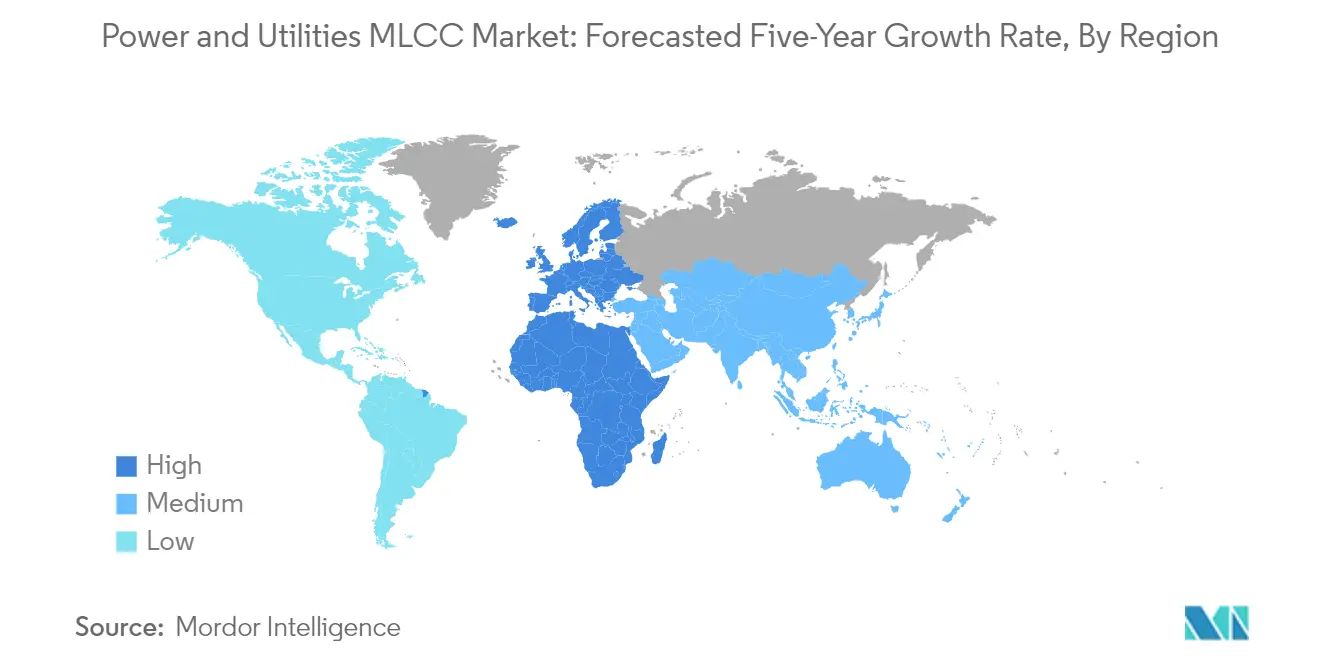

Power and Utilities MLCC Market in Asia-Pacific

The Asia-Pacific region maintains its dominance in the power and utilities MLCC market, commanding approximately 45% of the global market share in 2024. The region's leadership is driven by thriving economies such as China, India, South Korea, Singapore, and Japan, all experiencing robust growth in power consumption and utility demand. Critical factors like population expansion, urbanization, and industrial advancements further drive the region's need for augmented power generation capacities and enhanced utility infrastructure. The Indian government's proactive efforts to promote the widespread adoption of smart meters as part of energy infrastructure modernization have resulted in a notable surge in demand for MLCCs. China's comprehensive grid modernization initiative enhances power transmission and distribution networks, incorporating advanced technologies, smart grids, and energy management systems. This strategic approach optimizes grid performance and facilitates the seamless integration of renewable energy sources. The region's commitment to clean energy transition and infrastructure development continues to create substantial opportunities for MLCC manufacturers and suppliers.

Power and Utilities MLCC Market in Europe

Europe has demonstrated remarkable progress in the power and utilities MLCC market, achieving approximately 15% growth annually from 2019 to 2024. The region is actively investing in grid modernization to accommodate the growing penetration of renewable energy sources. Smart grid technologies, including advanced metering systems, demand response mechanisms, and energy storage solutions, are being deployed to enhance grid flexibility, improve energy efficiency, and enable better integration of renewable energy into the power system. The adoption of smart metering systems varies significantly across European countries, with nations like Denmark, Sweden, Estonia, Spain, Finland, and Norway achieving near-complete deployment in households. The integration of renewable energy sources into the electrical grid relies heavily on advanced smart grid technologies, which drive the demand for MLCCs. These components are vital in enabling efficient communication, monitoring, and control of renewable energy sources within the grid, ensuring reliable data transmission for the success of smart grid applications in the renewable energy industry.

Power and Utilities MLCC Market in North America

The North American power and utilities MLCC market is projected to grow at approximately 23% annually from 2024 to 2029. The implementation of various government regulations mandating the installation of smart meters and increased investments in smart grid technology are the major factors fueling the market's growth. The region's commitment to renewable energy adoption and grid modernization initiatives creates substantial opportunities for MLCC manufacturers. Cities across the region are increasingly investing in energy-efficient street lighting systems to replace or enhance their outdated systems, while reliable and bright public lighting reduces accidents and crime and allows for economic activities after sunset. Modern energy-efficient street-lighting technology can significantly lower energy consumption and operation and maintenance costs. The increasing adoption of smart cities and green building concepts continues to drive innovative smart meter applications, creating sustained demand for MLCCs in various power and utility applications.

Power and Utilities MLCC Market in Rest of the World

The Rest of the World region is emerging as a dynamic player in the power and utilities MLCC market, with significant developments particularly in Middle Eastern countries. Saudi Arabia's commitment to renewable energy sources and sustainable development is reshaping the regional market landscape. The transformation toward cleaner energy sources requires advanced automation systems and energy-efficient technologies, in which MLCCs play an integral role. Their importance in ensuring stable power supply, managing electrical fluctuations, and supporting the digitization of automation systems aligns perfectly with the region's sustainability goals. The focus on renewable energy expansion is expected to trigger substantial investments in infrastructure and manufacturing, creating robust demand for MLCCs of varying capacitances, especially those designed for high-capacity applications. As the region continues to invest in advanced technologies and automation systems, the demand for MLCCs remains strong, making it an exciting prospect for industry stakeholders.

Get Analysis on Important Geographic Markets

Download PDF

Power and Utilities MLCC Industry Overview

Top Companies in Power and Utilities MLCC Market

The power and utilities MLCC market is characterized by intense competition among major players who are actively pursuing innovation and expansion strategies. Companies are focusing on developing miniaturized MLCCs with enhanced capacity and internal voltage capabilities to meet evolving industry demands. Operational excellence is being achieved through investments in advanced manufacturing facilities and the implementation of closed-loop recycling systems for materials like PET films. Strategic moves include establishing new production sites in key markets and forming partnerships to strengthen market presence. Companies are also emphasizing sustainability initiatives, with many implementing environmental management systems and obtaining certifications for carbon footprint reduction. The industry witnesses continuous product development efforts, particularly in areas such as soft termination technology and metal terminal-type MLCCs for specialized applications.

Market Dominated by Global Technology Conglomerates

The power and utilities MLCC market exhibits a high degree of consolidation, with the top five companies collectively controlling a significant portion of the market share. These dominant players are primarily large-scale global technology conglomerates with diverse product portfolios extending beyond MLCCs into various electronic components and solutions. The market structure favors established manufacturers with extensive research and development capabilities, advanced manufacturing facilities, and strong distribution networks spanning multiple continents. These companies leverage their technological expertise and economies of scale to maintain competitive advantages in the market.

The industry has witnessed several strategic mergers and acquisitions aimed at expanding production capabilities and strengthening market positions. Companies are actively pursuing vertical integration strategies to secure supply chains and enhance operational efficiency. The market also sees the presence of specialized regional players who focus on specific geographic markets or niche applications within the power and utilities sector. These smaller players often compete through specialized product offerings and strong local customer relationships, though their market influence remains limited compared to the global leaders.

Innovation and Sustainability Drive Future Success

For incumbent companies to maintain and expand their market share, focusing on technological innovation and sustainable manufacturing practices is crucial. Leading firms are investing heavily in research and development to create more efficient and environmentally friendly MLCCs, while also expanding their production capabilities to meet growing demand. The ability to offer comprehensive solutions that address specific power and utility applications, combined with strong after-sales support and technical expertise, remains critical for market success. Companies are also strengthening their regional presence through strategic partnerships and localized manufacturing facilities to better serve key markets.

For contenders aiming to gain ground in the market, developing specialized products for emerging applications in renewable energy and smart grid systems presents significant opportunities. Success factors include building strong relationships with key customers in the power and utilities sector, investing in advanced manufacturing capabilities, and maintaining high quality standards while offering competitive pricing. The industry faces moderate substitution risk from alternative technologies, though MLCCs remain essential components in most power and utility applications. Regulatory compliance, particularly regarding environmental standards and product safety certifications, continues to shape market dynamics and influence company strategies. The power transmission component industry is also closely linked to these developments, as it relies on innovative MLCC solutions to enhance efficiency and reliability.

Power and Utilities MLCC Market Leaders

-

Kyocera AVX Components Corporation (Kyocera Corporation)

-

Murata Manufacturing Co., Ltd

-

Samsung Electro-Mechanics

-

Taiyo Yuden Co., Ltd

-

Yageo Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Power and Utilities MLCC Market News

- June 2023: The growing demand for industrial equipments has driven the company to introduce NTS/NTF NTS/NTF Series of SMD type MLCC. These capacitors are rated with 25 to 500 Vdc with a capacitance ranging from 0.010 to 47µF. These MLCCs are used in on-board power supplies,voltage regulators for computers,smoothing circuit of DC-DC converters,etc.

- July 2022: In 2022, Walsin Technology developed and released several new MLCC products are completed gradually, included high capacitance MLCCs with various temperature coefficients (X5R & X7R), high temperature MLCC, Feedthrough MLCC, miniaturized and low profile MLCCs, etc. (01005)

- June 2022: The passive components supplier YAGEO Group offers its CL series MLCC for applications requiring low ESL. The parasitic ESL will reduce the noise and voltage fluctuations brought on by the MLCC's discharged high-frequency current. More regular MLCCs must be configured, or the preferable option is to use a low ESL MLCC to stabilize the power line operation.

Free With This Report

We provide a complimentary and exhaustive set of data points on the country and regional level metrics that present the fundamental structure of the industry. Presented in the form of 40+ free charts, the sections cover difficult to find data on various indicators including but not limited to smartphones sales, raw materials pricing trends, and EV sales etc

Power and Utilities MLCC Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 Power And Utilities Equipment Sales

- 4.1.1 Global Inverters Sales

- 4.1.2 Global LEDs Sales

- 4.1.3 Global Smart Meters Sales

- 4.1.4 Global Solar PV Inverters and Optimizers Sales

- 4.2 Regulatory Framework

- 4.3 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

5.1 Case Size

- 5.1.1 1210

- 5.1.2 1812

- 5.1.3 2 220

- 5.1.4 3 640

- 5.1.5 4 540

- 5.1.6 Others

-

5.2 Voltage

- 5.2.1 600V to 1100V

- 5.2.2 Less than 600V

- 5.2.3 More than 1100V

-

5.3 Capacitance

- 5.3.1 10 μF to 100 μF

- 5.3.2 Less than 10 μF

- 5.3.3 More than 100 μF

-

5.4 Dielectric Type

- 5.4.1 Class 1

- 5.4.2 Class 2

-

5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of the World

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Würth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

- *List Not Exhaustive

7. KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- SALES OF GLOBAL INVERTERS , MILLION, GLOBAL, 2017 - 2029

- Figure 2:

- SALES OF GLOBAL LEDS , MILLION, GLOBAL, 2017 - 2029

- Figure 3:

- SALES OF GLOBAL SMART METERS , MILLION, GLOBAL, 2017 - 2029

- Figure 4:

- SALES OF GLOBAL SOLAR PV INVERTERS AND OPTIMIZERS , MILLION, GLOBAL, 2017 - 2029

- Figure 5:

- VOLUME OF GLOBAL POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 6:

- VALUE OF GLOBAL POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 7:

- VOLUME OF GLOBAL POWER AND UTILITIES MLCC MARKET BY CASE SIZE, , GLOBAL, 2017 - 2029

- Figure 8:

- VALUE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY CASE SIZE, USD, GLOBAL, 2017 - 2029

- Figure 9:

- VALUE SHARE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY CASE SIZE, %, GLOBAL, 2017 - 2029

- Figure 10:

- VOLUME SHARE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY CASE SIZE, %, GLOBAL, 2017 - 2029

- Figure 11:

- VOLUME OF 1210 POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 12:

- VALUE OF 1210 POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 13:

- VOLUME OF 1812 POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 14:

- VALUE OF 1812 POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 15:

- VOLUME OF 2 220 POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 16:

- VALUE OF 2 220 POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 17:

- VOLUME OF 3 640 POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 18:

- VALUE OF 3 640 POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 19:

- VOLUME OF 4 540 POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 20:

- VALUE OF 4 540 POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 21:

- VOLUME OF OTHERS POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 22:

- VALUE OF OTHERS POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 23:

- VOLUME OF GLOBAL POWER AND UTILITIES MLCC MARKET BY VOLTAGE, , GLOBAL, 2017 - 2029

- Figure 24:

- VALUE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY VOLTAGE, USD, GLOBAL, 2017 - 2029

- Figure 25:

- VALUE SHARE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY VOLTAGE, %, GLOBAL, 2017 - 2029

- Figure 26:

- VOLUME SHARE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY VOLTAGE, %, GLOBAL, 2017 - 2029

- Figure 27:

- VOLUME OF 600V TO 1100V POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 28:

- VALUE OF 600V TO 1100V POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 29:

- VOLUME OF LESS THAN 600V POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 30:

- VALUE OF LESS THAN 600V POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 31:

- VOLUME OF MORE THAN 1100V POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 32:

- VALUE OF MORE THAN 1100V POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 33:

- VOLUME OF GLOBAL POWER AND UTILITIES MLCC MARKET BY CAPACITANCE, , GLOBAL, 2017 - 2029

- Figure 34:

- VALUE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY CAPACITANCE, USD, GLOBAL, 2017 - 2029

- Figure 35:

- VALUE SHARE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY CAPACITANCE, %, GLOBAL, 2017 - 2029

- Figure 36:

- VOLUME SHARE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY CAPACITANCE, %, GLOBAL, 2017 - 2029

- Figure 37:

- VOLUME OF 10 ΜF TO 100 ΜF POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 38:

- VALUE OF 10 ΜF TO 100 ΜF POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 39:

- VOLUME OF LESS THAN 10 ΜF POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 40:

- VALUE OF LESS THAN 10 ΜF POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 41:

- VOLUME OF MORE THAN 100 ΜF POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 42:

- VALUE OF MORE THAN 100 ΜF POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 43:

- VOLUME OF GLOBAL POWER AND UTILITIES MLCC MARKET BY DIELECTRIC TYPE, , GLOBAL, 2017 - 2029

- Figure 44:

- VALUE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY DIELECTRIC TYPE, USD, GLOBAL, 2017 - 2029

- Figure 45:

- VALUE SHARE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY DIELECTRIC TYPE, %, GLOBAL, 2017 - 2029

- Figure 46:

- VOLUME SHARE OF GLOBAL POWER AND UTILITIES MLCC MARKET BY DIELECTRIC TYPE, %, GLOBAL, 2017 - 2029

- Figure 47:

- VOLUME OF CLASS 1 POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 48:

- VALUE OF CLASS 1 POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 49:

- VOLUME OF CLASS 2 POWER AND UTILITIES MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 50:

- VALUE OF CLASS 2 POWER AND UTILITIES MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 51:

- VOLUME OF POWER AND UTILITIES MLCC MARKET, BY REGION, NUMBER, , 2017 - 2029

- Figure 52:

- VALUE OF POWER AND UTILITIES MLCC MARKET, BY REGION, USD, 2017 - 2029

- Figure 53:

- CAGR OF POWER AND UTILITIES MLCC MARKET, BY REGION, %, 2017 - 2029

- Figure 54:

- CAGR OF POWER AND UTILITIES MLCC MARKET, BY REGION, %, 2017 - 2029

- Figure 55:

- VOLUME OF GLOBAL POWER AND UTILITIES MLCC MARKET,NUMBER, IN ASIA-PACIFIC, 2017 - 2029

- Figure 56:

- VALUE OF GLOBAL POWER AND UTILITIES MLCC MARKET, IN ASIA-PACIFIC, 2017 - 2029

- Figure 57:

- VOLUME OF GLOBAL POWER AND UTILITIES MLCC MARKET,NUMBER, IN EUROPE, 2017 - 2029

- Figure 58:

- VALUE OF GLOBAL POWER AND UTILITIES MLCC MARKET, IN EUROPE, 2017 - 2029

- Figure 59:

- VOLUME OF GLOBAL POWER AND UTILITIES MLCC MARKET,NUMBER, IN NORTH AMERICA, 2017 - 2029

- Figure 60:

- VALUE OF GLOBAL POWER AND UTILITIES MLCC MARKET, IN NORTH AMERICA, 2017 - 2029

- Figure 61:

- VOLUME OF GLOBAL POWER AND UTILITIES MLCC MARKET,NUMBER, IN REST OF THE WORLD, 2017 - 2029

- Figure 62:

- VALUE OF GLOBAL POWER AND UTILITIES MLCC MARKET, IN REST OF THE WORLD, 2017 - 2029

- Figure 63:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, COUNT, GLOBAL, 2017 - 2029

- Figure 64:

- MOST ADOPTED STRATEGIES, COUNT, GLOBAL, 2017 - 2029

- Figure 65:

- VALUE SHARE OF MAJOR PLAYERS, %, GLOBAL, 2017 - 2029

Power and Utilities MLCC Industry Segmentation

1210, 1812, 2 220, 3 640, 4 540, Others are covered as segments by Case Size. 600V to 1100V, Less than 600V, More than 1100V are covered as segments by Voltage. 10 μF to 100 μF, Less than 10 μF, More than 100 μF are covered as segments by Capacitance. Class 1, Class 2 are covered as segments by Dielectric Type. Asia-Pacific, Europe, North America are covered as segments by Region.| Case Size | 1210 |

| 1812 | |

| 2 220 | |

| 3 640 | |

| 4 540 | |

| Others | |

| Voltage | 600V to 1100V |

| Less than 600V | |

| More than 1100V | |

| Capacitance | 10 μF to 100 μF |

| Less than 10 μF | |

| More than 100 μF | |

| Dielectric Type | Class 1 |

| Class 2 | |

| Region | Asia-Pacific |

| Europe | |

| North America | |

| Rest of the World |

Need A Different Region or Segment?

Customize Now

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform

Get More Details On Research Methodology

Download PDF