| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 21.73 Billion |

| Market Size (2030) | USD 27.32 Billion |

| CAGR (2025 - 2030) | 4.68 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Powder Metallurgy Market Analysis

The Powder Metallurgy Market size is estimated at USD 21.73 billion in 2025, and is expected to reach USD 27.32 billion by 2030, at a CAGR of 4.68% during the forecast period (2025-2030).

The powder metallurgy industry is experiencing significant transformation through technological advancement and industry consolidation. Leading powder metallurgy companies are increasingly focusing on innovation and research & development to strengthen their market positions. This is evidenced by the installation of over 200 ABB S3 robots by Hitachi Chemical Co. Ltd at its powder metallurgy facilities, demonstrating the industry's shift towards automated and efficient production processes. Companies are also actively pursuing strategic mergers and acquisitions, as demonstrated by Sumitomo Electric Industries' acquisition of European manufacturers Sinterwerke Herne GmbH and Sinterwerke Grenchen AG, highlighting the industry's move towards consolidated operations and expanded global reach.

The aerospace sector represents a significant growth avenue for powder metallurgy applications, with the global aviation fleet comprising over 440,000 general aviation aircraft. Major aerospace manufacturers are expanding their production capabilities and investing in new technologies to meet the growing demand for lightweight and high-performance components. The industry is witnessing increased collaboration between powder metallurgy manufacturers and aerospace companies to develop specialized materials and components that meet stringent industry requirements. This trend is particularly evident in Germany, where more than 2,300 aerospace firms are actively engaged in various aspects of aerospace manufacturing, creating substantial opportunities for powder metallurgy applications.

The electronics manufacturing sector is emerging as a crucial market for powder metallurgy applications, particularly in established markets like the United Kingdom, which hosts approximately 18,000 electronics companies. The industry is witnessing increased adoption of powder metallurgy components in electronic devices, particularly in applications requiring high precision and complex geometries. Manufacturers are developing specialized powder metallurgy solutions for electronic components, focusing on materials that offer improved conductivity, thermal management, and miniaturization capabilities. This trend is driven by the growing demand for sophisticated electronic devices and the need for advanced manufacturing processes that can meet precise specifications.

The industry is witnessing a significant shift towards sustainable manufacturing practices and material optimization. Manufacturers are investing in advanced powder metallurgy processing technologies that reduce material waste and energy consumption during the production process. The focus is increasingly on developing eco-friendly production methods and recycling capabilities to minimize environmental impact. This transformation is accompanied by the development of new material compositions and processing techniques that enhance product performance while maintaining sustainability objectives. Industry players are also exploring opportunities in emerging applications such as metal additive manufacturing and advanced materials development, positioning themselves for future growth opportunities in high-value markets.

Powder Metallurgy Market Trends

Increasing Preference for Powder Metallurgy Amongst Automotive OEMs

Powder metallurgy (PM) has emerged as a preferred manufacturing technology among automotive OEMs due to its superior capabilities in producing complex components with high dimensional accuracy and minimal material wastage. The technology enables manufacturers to develop mechanical parts with diverse compositions, including metal-nonmetal and metal-metal combinations, while ensuring consistent properties throughout the component. This manufacturing versatility has become particularly valuable as global automotive production continues to expand, with approximately 50 million passenger cars manufactured worldwide in the first three quarters of 2022, representing a 9% increase compared to the same period in 2021, according to the European Automobile Manufacturers' Association (ACEA).

The adoption of powder metallurgy in the automotive sector is further driven by its extensive application across various vehicle components, including bearings, gears, chassis components, steering systems, exhaust components, transmission parts, shock absorber components, engine components, and brake discs. The technology's ability to produce self-lubricating components with controlled porosity makes it particularly suitable for these applications, offering improved performance and longevity. The growing electric vehicle market has also contributed to increased demand for powder metal components, as evidenced by China's remarkable 96.9% year-over-year growth in new energy vehicle production from December 2021 to December 2022, creating new opportunities for powder metal parts in electric powertrains and battery systems.

Understand The Key Trends Shaping This Market

Download PDF

Growing Implementation in Electrical and Electromagnetic Applications

The electrical and electronics industry has witnessed increasing adoption of powder metallurgy due to its unique capabilities in producing components with superior magnetic properties and electrical conductivity. Soft magnetic materials manufactured through powder metallurgy processing are becoming increasingly important in electrical equipment, offering improved performance in high-frequency applications while enabling smaller form factors and enhanced energy efficiency. The technology's ability to create components with precise magnetic properties has made it invaluable in manufacturing various electronic components, ranging from small consumer electronics to industrial power systems.

The versatility of powder metallurgy in electrical applications extends to the production of multiple specialized components, including insulated gate bipolar transistors (IGBT), electric motors, and electromagnetic cores. The manufacturing process allows for the creation of complex shapes with excellent magnetic properties, crucial for modern electronic devices. Additionally, the technology enables the production of components with specific electrical and thermal conductivity properties, making it particularly valuable in manufacturing heat sinks, circuit board components, and electrical contacts. The ability to create materials with controlled porosity and self-lubricating properties has also made powder metallurgy essential in producing reliable, long-lasting electrical components for various applications, from mobile devices to industrial machinery.

Segment Analysis: By Product Type

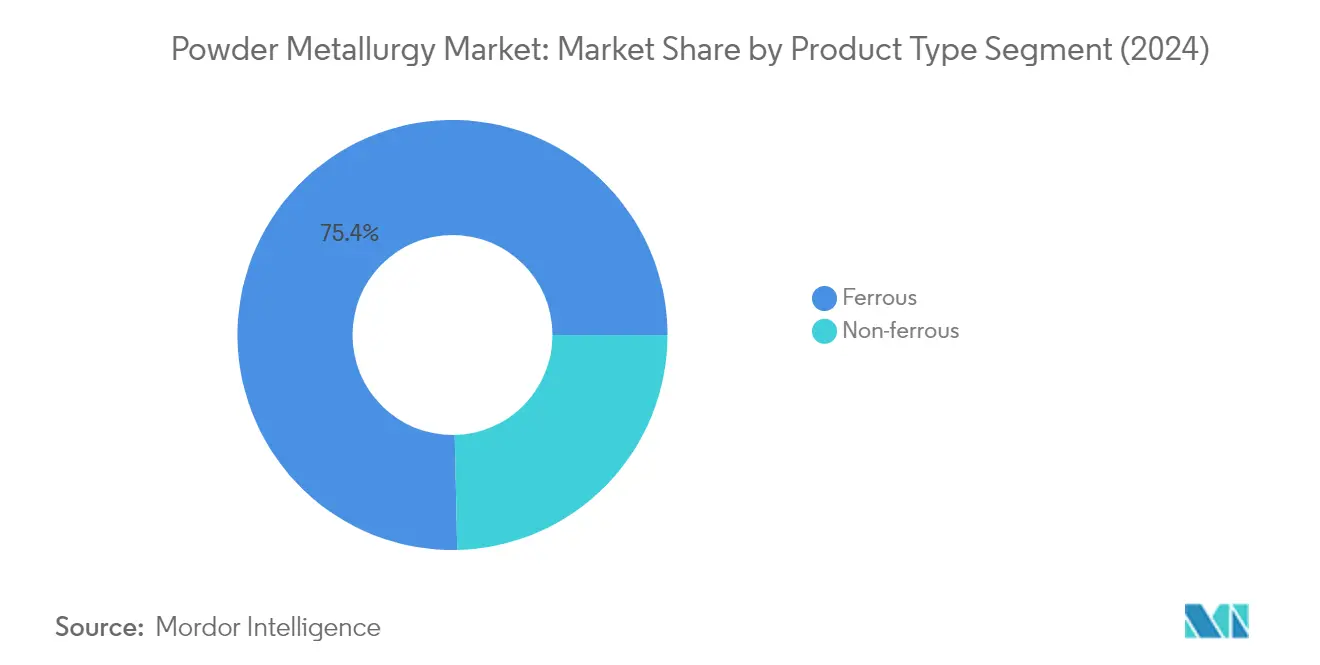

Ferrous Segment in Powder Metallurgy Market

The ferrous segment continues to dominate the global powder metallurgy market, commanding approximately 75% market share in 2024. This segment's prominence can be attributed to the superior mechanical properties of ferrous powders, including high hardness, tensile strength, magnetic functionality, and broad flexibility. Ferrous powder metal components find extensive applications across various industries, particularly in automotive engine components, transmission parts, and chassis applications where durability and strength are paramount. The segment is also witnessing robust growth, expected to grow at around 5% from 2024-2029, driven by increasing demand from construction, engineering, and automotive sectors. The versatility of ferrous powders in producing complex shapes and components, combined with their cost-effectiveness and excellent wear resistance properties, continues to fuel their adoption in manufacturing processes worldwide.

Non-ferrous Segment in Powder Metallurgy Market

The non-ferrous segment, encompassing materials like aluminum, copper, titanium, and their alloys, holds the remaining quarter of the market share. This segment plays a crucial role in applications requiring specific properties such as lightweight construction, high conductivity, or corrosion resistance. Non-ferrous powder metallurgy materials are particularly valuable in aerospace components, electronic devices, and medical implants where unique material characteristics are essential. The segment's growth is supported by ongoing technological advancements in powder production and processing techniques, enabling manufacturers to achieve higher precision and performance in their final products.

Segment Analysis: By Application

Automotive Segment in Powder Metallurgy Market

The automotive segment dominates the global powder metallurgy market, accounting for approximately 71% of the total market share in 2024. This significant market position is attributed to the extensive use of powder metal parts in manufacturing various automotive components, including engine parts, transmission components, and chassis elements. The automotive industry's preference for powder metallurgy continues to grow due to its ability to produce complex-shaped components with high precision and cost-effectiveness. The technology's capability to manufacture parts with excellent controlled porosity and self-lubricating properties makes it particularly valuable for automotive applications. Additionally, powder metallurgy's sustainability benefits, including net-shape capabilities and high-material utilization that minimize energy inputs and environmental impact, have further strengthened its position in the automotive sector.

Aerospace Segment in Powder Metallurgy Market

The aerospace segment represents a rapidly evolving sector in the powder metallurgy market, with titanium alloy-based powders being the most widely utilized materials in aircraft component manufacturing. The segment's growth is driven by the increasing demand for lightweight, high-strength components that can withstand extreme operating conditions. Powder metallurgy's ability to produce complex aerospace components with superior mechanical properties and dimensional accuracy makes it an ideal choice for this sector. The technology offers significant advantages in manufacturing critical aircraft parts, including reduced material waste, improved performance characteristics, and the capability to create components with unique design specifications that would be difficult to achieve through conventional manufacturing methods.

Remaining Segments in Application Market

The industrial machinery, electrical and electronics, and other applications segments collectively form a significant portion of the powder metallurgy market. The industrial machinery segment utilizes powder metallurgy for manufacturing cutting tools, polishing equipment, and drilling tools, serving numerous industries. The electrical and electronics segment leverages powder metallurgy's excellent electrical and thermal conductivity properties for producing components used in consumer electronics, circuit boards, and electronic assemblies. Other applications include medical devices and components used in medical implants, where powder metallurgy's ability to create complex shapes and maintain precise specifications is particularly valuable. These segments continue to drive innovation in powder metallurgy applications, contributing to the overall market growth through diverse end-use requirements and technological advancements.

Powder Metallurgy Market Geography Segment Analysis

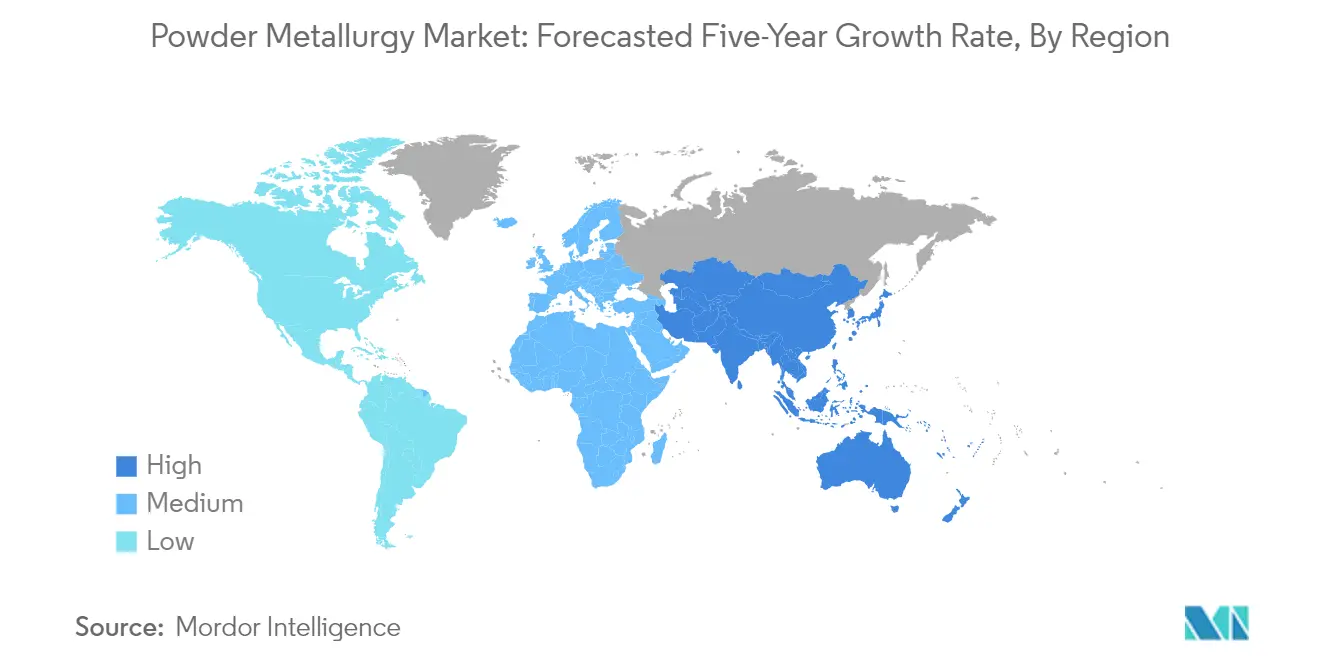

Powder Metallurgy Market in Asia-Pacific

The Asia-Pacific region represents a dominant force in the global powder metallurgy market, encompassing major manufacturing hubs like China, India, Japan, South Korea, and the ASEAN countries. The region's strength stems from its robust automotive manufacturing sector, expanding electronics industry, and growing industrial machinery production. Each country in the region brings unique advantages: China with its massive manufacturing base, Japan with its high-tech automotive sector, South Korea with its advanced electronics industry, India with its growing industrial base, and ASEAN countries with their emerging manufacturing capabilities. The presence of major automotive OEMs and electronics manufacturers has been driving significant investments in powder metallurgy capabilities across the region.

Powder Metallurgy Market in China

China stands as the powerhouse of the Asia-Pacific powder metallurgy market, commanding approximately 53% share of the regional market. The country's dominance is built on its extensive automotive manufacturing base, robust electronics industry, and significant investments in industrial machinery. China's powder metallurgy sector benefits from strong government support for advanced manufacturing technologies, particularly in automotive and aerospace applications. The country's massive production capabilities, coupled with its large domestic market, have attracted significant investments from both domestic and international powder metallurgy companies. The presence of major automotive OEMs and their suppliers has created a strong ecosystem for powder metallurgy applications, particularly in components for engines, transmissions, and electrical systems.

Powder Metallurgy Market Growth in China

China is expected to maintain its position as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 6% during 2024-2029. The country's growth trajectory is supported by the increasing adoption of powder metallurgy in emerging applications such as electric vehicles, advanced electronics, and aerospace components. China's focus on technological advancement and industrial upgrading, particularly in high-end manufacturing sectors, is creating new opportunities for powder metallurgy applications. The government's push towards advanced manufacturing capabilities and emphasis on domestic production of critical components is expected to further drive market growth. The expansion of the country's aerospace and electronics sectors is also creating new avenues for powder metallurgy applications.

Powder Metallurgy Market in North America

North America represents a mature and technologically advanced market for powder metallurgy, with the United States, Canada, and Mexico as key contributors. The region's market is characterized by high adoption of advanced powder metallurgy technologies, particularly in automotive and aerospace applications. The presence of major automotive manufacturers, aerospace companies, and industrial equipment manufacturers drives the demand for powder metallurgy components. The region benefits from strong research and development capabilities, advanced manufacturing infrastructure, and high technical expertise in powder metallurgy applications.

Powder Metallurgy Market in United States

The United States dominates the North American powder metallurgy market with approximately 69% share of the regional market. The country's leadership position is supported by its advanced manufacturing capabilities, strong aerospace sector, and significant automotive production base. The presence of major powder metallurgy manufacturers, coupled with continuous technological innovations, has established the United States as a center for advanced powder metallurgy applications. The country's robust aerospace industry, particularly in commercial and defense sectors, drives significant demand for high-performance powder metallurgy components. The automotive sector remains a major consumer, with increasing applications in electric vehicles and advanced powertrains.

Powder Metallurgy Market Growth in United States

The United States is projected to maintain its position as the fastest-growing market in North America, with an expected growth rate of approximately 4% during 2024-2029. The growth is driven by increasing adoption of powder metallurgy in advanced applications, particularly in aerospace and electric vehicle components. The country's focus on lightweight materials and advanced manufacturing technologies is creating new opportunities for powder metallurgy applications. The expansion of the aerospace sector, coupled with the growing trend towards electric vehicles, is expected to drive continued growth in powder metallurgy demand.

Powder Metallurgy Market in Europe

Europe maintains a strong position in the global powder metallurgy market, with Germany, the United Kingdom, Italy, and France serving as key markets. The region's market is characterized by high technological sophistication, strong focus on research and development, and significant presence in automotive and aerospace applications. The European market benefits from the presence of established automotive manufacturers, aerospace companies, and industrial equipment producers. The region's focus on sustainable manufacturing and advanced materials technology continues to drive innovations in powder metallurgy applications.

Powder Metallurgy Market in Germany

Germany leads the European powder metallurgy market, leveraging its strong automotive manufacturing base and advanced industrial capabilities. The country's leadership is built on its extensive network of automotive OEMs, tier-1 suppliers, and specialized powder metallurgy manufacturers. Germany's market position is strengthened by its focus on high-quality manufacturing, continuous technological innovation, and strong research and development capabilities. The country's automotive sector remains the primary driver for powder metallurgy applications, with growing demand from aerospace and industrial machinery sectors.

Powder Metallurgy Market Growth in Germany

Germany maintains its position as the fastest-growing market in Europe, driven by increasing adoption of advanced manufacturing technologies and expansion of electric vehicle production. The country's growth is supported by continuous investments in research and development, particularly in areas such as advanced materials and sustainable manufacturing processes. The transition towards electric vehicles and Industry 4.0 initiatives is creating new opportunities for powder metallurgy applications in the country.

Powder Metallurgy Market in South America

The South American powder metallurgy market, primarily represented by Brazil and Argentina, shows steady development despite economic challenges in the region. Brazil emerges as both the largest and fastest-growing market in the region, benefiting from its substantial automotive manufacturing base and growing industrial sector. The region's market is characterized by increasing investments in manufacturing capabilities and growing adoption of powder metallurgy technologies, particularly in automotive applications. While economic volatility presents challenges, the growing industrialization and modernization of manufacturing processes continue to drive market development.

Powder Metallurgy Market in Middle East & Africa

The Middle East & Africa region, with key markets in Saudi Arabia and South Africa, represents an emerging market for powder metallurgy applications. South Africa leads the regional market, benefiting from its established automotive and mining sectors, while Saudi Arabia shows promising growth potential driven by industrial diversification initiatives. The region's market is characterized by increasing investments in manufacturing capabilities and growing adoption of powder metallurgy technologies across various industrial applications. The focus on industrial diversification in Middle Eastern countries and the established manufacturing base in South Africa continue to create new opportunities for powder metallurgy applications.

Get Analysis on Important Geographic Markets

Download PDF

Powder Metallurgy Industry Overview

Top Companies in Powder Metallurgy Market

The powder metallurgy market is characterized by companies focusing heavily on technological advancement and innovation across their product portfolios. Leading powder metallurgy companies are investing substantially in research and development to develop differentiated products, particularly for emerging applications in the automotive and aerospace sectors. Companies are increasingly adopting automation and digital technologies to enhance production efficiency and reduce operational costs. Strategic expansions through new manufacturing facilities, particularly in high-growth regions like Asia-Pacific, demonstrate the industry's focus on increasing production capacity and market reach. Additionally, manufacturers are strengthening their positions through strategic collaborations, joint ventures, and acquisitions to expand their technological capabilities and geographic presence, while also focusing on developing sustainable and cost-effective manufacturing processes.

Consolidated Market Led By Global Leaders

The powder metallurgy industry exhibits a partially fragmented structure with a few major global players holding significant market share alongside numerous regional manufacturers. Companies like Hitachi Chemical, Höganäs, Melrose, Sumitomo Electric, and ATI dominate the global landscape through their extensive product portfolios and strong manufacturing capabilities. These market leaders are characterized by their vertically integrated operations, spanning from metal powder production to finished components, providing them with competitive advantages in terms of cost and quality control.

The industry has witnessed considerable consolidation through strategic mergers and acquisitions, particularly aimed at expanding geographic presence and technological capabilities. Major players are increasingly focusing on acquiring smaller, specialized manufacturers to enhance their product offerings and strengthen their market position. The trend of forming strategic partnerships and joint ventures, especially in emerging markets, indicates the industry's move towards greater consolidation while maintaining regional manufacturing presence to serve local markets effectively.

Innovation and Adaptability Drive Market Success

Success in the powder metallurgy market increasingly depends on companies' ability to innovate and adapt to changing industry demands, particularly in emerging applications like electric vehicles and aerospace components. Market leaders are focusing on developing specialized products with enhanced properties while maintaining cost competitiveness through operational efficiency. Companies are also investing in sustainable manufacturing practices and circular economy initiatives to address growing environmental concerns and regulatory requirements, while simultaneously expanding their presence in high-growth markets through strategic partnerships and local manufacturing facilities.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized products and applications. The ability to offer customized solutions, maintain strong relationships with end-users, and demonstrate technological expertise in specific applications is crucial for gaining market share. Companies must also focus on developing robust supply chain networks and maintaining operational flexibility to address market volatility and changing customer demands. Additionally, investment in research and development capabilities and strategic collaborations with established players can provide smaller companies with opportunities to expand their market presence and technological capabilities.

Powder Metallurgy Market Leaders

-

Höganäs AB

-

Melrose Industries PLC

-

Sumitomo Electric Industries, Ltd.

-

ATI

-

Showa Denko Materials Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Powder Metallurgy Market News

- March 2023: Höganäs is set to inaugurate its new ArcX facility in Houston, Texas, to further strengthen the company's position in metal powder coating solutions.

- February 2023: Sumitomo Electric Industries, Ltd. launched a sales firm in India, Sumitomo Electric Hardmetal India Private Limited, to increase cutting tool sales in the country.

Powder Metallurgy Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Preference for Powder Metallurgy by Automotive OEMs

- 4.1.2 Growing Implementation in Electrical and Electromagnetic Applications

-

4.2 Restraints

- 4.2.1 Increasing Raw Material and Tooling Costs

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 Product Type

- 5.1.1 Ferrous

- 5.1.2 Non-ferrous

-

5.2 Application

- 5.2.1 Automotive

- 5.2.2 Industrial Machinery

- 5.2.3 Electrical and Electronics

- 5.2.4 Aerospace

- 5.2.5 Other Applications

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 ATI

- 6.4.2 Catalus Corporation

- 6.4.3 fine-sinter Co., Ltd.

- 6.4.4 H.C. Starck Tungsten GmbH

- 6.4.5 Showa Denko Materials Co., Ltd.

- 6.4.6 Hoganas AB

- 6.4.7 Horizon Technology

- 6.4.8 Melrose Industries PLC

- 6.4.9 Miba AG

- 6.4.10 Perry Tool & Research, Inc.

- 6.4.11 Phoenix Sintered Metals, LLC

- 6.4.12 Precision Sintered Parts

- 6.4.13 Sandvik AB

- 6.4.14 Sumitomo Electric Industries, Ltd.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Adoption of Powder Metallurgy Techniques in Medical Sector

- 7.2 Rapid Growth in Aerospace and Defense Sector

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Powder Metallurgy Industry Segmentation

Powder metallurgy is a way to make things that use less energy and have better performance and more design options than traditional methods like casting, forging, extrusion, stamping, and machining.

The powder metallurgy market is segmented by product type, application, and geography. By product type, the market is segmented into ferrous and non-ferrous metals. By application, the market is segmented into automotive, industrial machinery, electrical and electronics, aerospace, and other applications. The report also covers the market size and forecasts in 15 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD).

| Product Type | Ferrous | ||

| Non-ferrous | |||

| Application | Automotive | ||

| Industrial Machinery | |||

| Electrical and Electronics | |||

| Aerospace | |||

| Other Applications | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Powder Metallurgy Market Research FAQs

How big is the Powder Metallurgy Market?

The Powder Metallurgy Market size is expected to reach USD 21.73 billion in 2025 and grow at a CAGR of 4.68% to reach USD 27.32 billion by 2030.

What is the current Powder Metallurgy Market size?

In 2025, the Powder Metallurgy Market size is expected to reach USD 21.73 billion.

Who are the key players in Powder Metallurgy Market?

Höganäs AB, Melrose Industries PLC, Sumitomo Electric Industries, Ltd., ATI and Showa Denko Materials Co., Ltd. are the major companies operating in the Powder Metallurgy Market.

Which is the fastest growing region in Powder Metallurgy Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Powder Metallurgy Market?

In 2025, the Asia-Pacific accounts for the largest market share in Powder Metallurgy Market.

What years does this Powder Metallurgy Market cover, and what was the market size in 2024?

In 2024, the Powder Metallurgy Market size was estimated at USD 20.71 billion. The report covers the Powder Metallurgy Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Powder Metallurgy Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Powder Metallurgy Market Research

Mordor Intelligence provides a comprehensive analysis of the powder metallurgy market. We leverage extensive expertise in metal powder processing and manufacturing technologies. Our detailed research covers the entire spectrum of powder metallurgy applications. This includes metal injection molding, hot isostatic pressing, and powder compaction processes. The report examines key developments in metal powder production, sintering technology, and powder consolidation. It also analyzes the evolution of powder metallurgy materials and atomized metal powder manufacturing techniques.

Stakeholders across the powder metallurgy industry gain valuable insights through our detailed analysis, available in an easy-to-read report pdf format. The research encompasses crucial aspects of powder metal manufacturing, including powder metal components production, powder metallurgy equipment utilization, and powder metallurgy tooling innovations. Our analysis extends to emerging technologies like metal additive manufacturing and powder forging. It provides strategic insights into future trends in powder metallurgy. The report offers comprehensive coverage of sintered metal applications and metallic powder developments, enabling businesses to make informed decisions in this rapidly evolving sector.