Market Size of Pouch Packaging Industry

| Study Period | 2019 - 2029 |

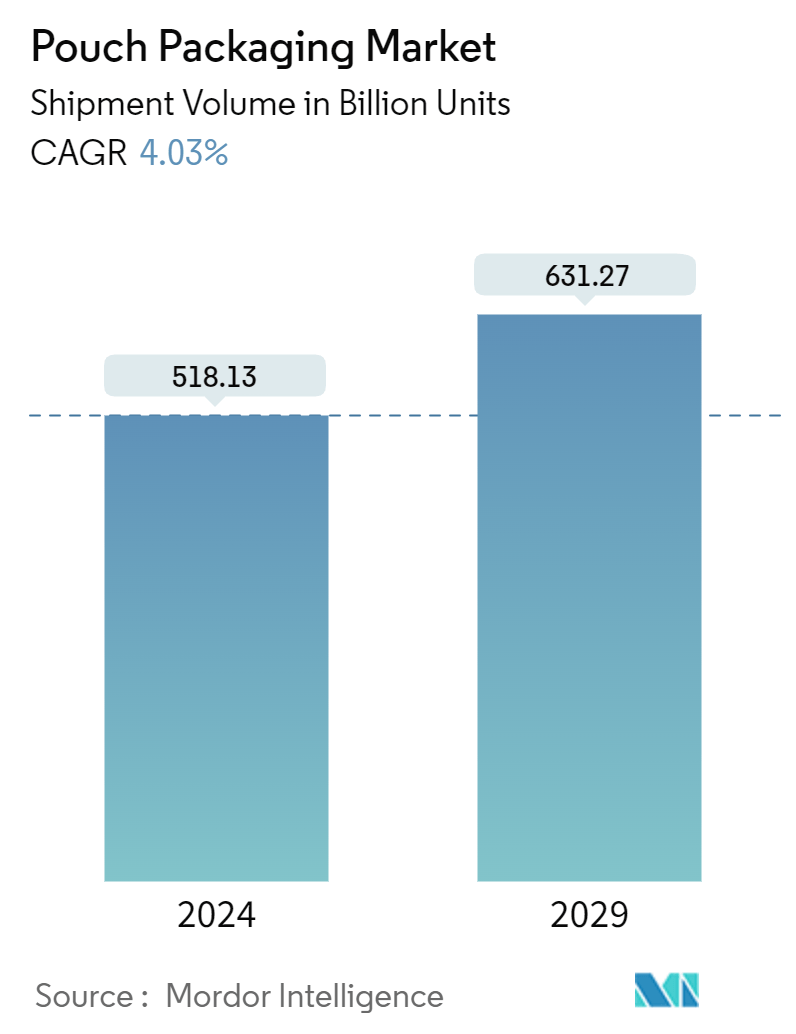

| Market Volume (2024) | 518.13 Billion units |

| Market Volume (2029) | 631.27 Billion units |

| CAGR (2024 - 2029) | 4.03 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players*Disclaimer: Major Players sorted in no particular order |

Pouch Packaging Market Analysis

The Pouch Packaging Market size in terms of shipment volume is expected to grow from 518.13 Billion units in 2024 to 631.27 Billion units by 2029, at a CAGR of 4.03% during the forecast period (2024-2029).

- Pouches are among the most widely used packaging products in the food and beverage industry, including pet food, baby food, and liquid packaging (tea, coffee, and juices). Owing to their different features, they are easy to open (like a tear notch and laser perforation), easy to use (with zippers and shapes), and reclosable.

- Pouches have experienced significant advancements in recent years, fueled by a growing emphasis on sustainability, technological innovation, and design flexibility. Moreover, as they are chemically inert, they are widely used in various industries, such as pharmaceuticals, pet food, and cosmetics.

- For instance, in August 2023, Dow Inc., a United States-based chemicals company, partnered with Mengniu, a China-based dairy company, to launch an all-polyethylene (PE) yogurt pouch designed for recyclability. The new product launch enables both companies to achieve a circular economy in China.

- Stand-up pouches are experiencing a remarkable transformation driven by sustainability concerns, intelligent packaging technologies, and printing advancements. Brands that use biodegradable and compostable materials demonstrate their commitment to the environment while promoting eco-conscious consumers. For instance, Kellogg's has launched a range of cereal pouches made from plant-based plastic. Pouches are recyclable, and the company aims to make all of its cereal packaging 100% recyclable by 2025.

- The pouch packaging market growth can be attributed to several factors, such as the rising demand for convenient, portable, and single-serve food and beverage products that align well with consumers' on-the-go lifestyles. Pouche packaging caters to this increasing demand with its lightweight and easily resealable features.

- One of the most significant trends in the packaging industry is the shift toward eco-friendly and sustainable materials. Consumers and regulators alike are increasingly concerned about the environmental consequences of packaging waste. In addition, manufacturers are exploring alternatives to traditional plastic pouches, such as biodegradable and compostable pouches. In July 2023, Walki and Rovema designed a paper pouch for confectionery to replace plastic. The company developed a reinforced euro-hole pouch to keep the packaging intact and environmentally sustainable.

Pouch Packaging Industry Segmentation

Pouch packaging is a flexible packaging product that is used for flowable liquid products. The study covers the pouch packaging market tracked in terms of volume (units). Pouch packaging is a flexible packaging product made from barrier films or paper or foil, depending on the end-user requirement. The study analyzes the factors that impact geopolitical developments in the studied market based on the prevalent base scenarios, key themes, and end-user industries-related demand cycles.

The Pouch Packaging Market is Segmented by Material Type ( Paper, Plastic and Aluminum), by Resin Type - Plastic ( Polyethylene, Polypropylene, PET, PVC, EVOH, Other Resins), by Product ( Flat ( Pillow and Side Seal), Stand Up), by End-User Industry (Food (Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry, And Seafood, Pet Food, Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)), Beverage, Medical and Pharmaceutical, Personal Care and Household Care, and Other End-User Industries) and Geography (North America [United States and Canada], Europe [France, Germany, Italy, United Kingdom, Spain, Poland, Nordic and Rest of Europe], Asia-Pacific [China, India, Japan, Thailand, Indonesia, Vietnam, Australia and New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Colombia, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, Egypt, South Africa, Nigeria, Morocco and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of volume (units) for all the above segments.

| By Material | ||||||||

| ||||||||

| Paper | ||||||||

| Aluminum |

| By Product | |

| Flat (Pillow & Side-Seal) | |

| Stand-up |

| By End-User Industry | ||||||||||

| ||||||||||

| Beverage | ||||||||||

| Medical and Pharmaceutical | ||||||||||

| Personal Care and Household Care | ||||||||||

| Other End user Industries ( Automotive, Chemical, Agriculture) |

| By Geography*** | |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

|

Pouch Packaging Market Size Summary

The pouch packaging market is experiencing robust growth, driven by its extensive application in the food and beverage industry, including sectors like pet food, baby food, and liquid packaging. Pouches are favored for their user-friendly features such as easy opening, resealability, and lightweight nature, making them ideal for on-the-go consumers. The market is witnessing significant advancements due to a heightened focus on sustainability, technological innovations, and design flexibility. Companies are increasingly adopting eco-friendly materials, such as biodegradable and compostable options, to meet consumer and regulatory demands for sustainable packaging solutions. This shift is further supported by collaborations and product launches aimed at enhancing recyclability and reducing environmental impact, such as the all-polyethylene yogurt pouch by Dow Inc. and Mengniu.

The demand for pouch packaging is further bolstered by changing consumer lifestyles, which have led to a surge in the consumption of ready-to-eat and snack foods. The convenience and portability of pouches cater to the busy lifestyles of modern consumers, particularly in regions like North America, where savory snacks are gaining popularity. The market is characterized by a fragmented landscape with numerous players, including Bischof + Klein SE & Co. KG, Amcor Group GmbH, and ProAmpac Intermediate Inc., who are actively innovating to expand their market presence. Recent developments, such as the introduction of sustainable fiber-based pouches and strategic acquisitions, highlight the industry's commitment to enhancing packaging performance and sustainability. These trends are expected to drive the market's growth during the forecast period, as manufacturers continue to explore advanced technologies and materials to meet evolving consumer preferences.

Pouch Packaging Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Buyers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitutes

-

1.3.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Material

-

2.1.1 Plastic

-

2.1.1.1 Polyethylene

-

2.1.1.2 Polypropylene

-

2.1.1.3 PET

-

2.1.1.4 PVC

-

2.1.1.5 EVOH

-

2.1.1.6 Other Resins

-

-

2.1.2 Paper

-

2.1.3 Aluminum

-

-

2.2 By Product

-

2.2.1 Flat (Pillow & Side-Seal)

-

2.2.2 Stand-up

-

-

2.3 By End-User Industry

-

2.3.1 Food

-

2.3.1.1 Candy & Confectionery

-

2.3.1.2 Frozen Foods

-

2.3.1.3 Fresh Produce

-

2.3.1.4 Dairy Products

-

2.3.1.5 Dry Foods

-

2.3.1.6 Meat, Poultry, And Seafood

-

2.3.1.7 Pet Food

-

2.3.1.8 Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)

-

-

2.3.2 Beverage

-

2.3.3 Medical and Pharmaceutical

-

2.3.4 Personal Care and Household Care

-

2.3.5 Other End user Industries ( Automotive, Chemical, Agriculture)

-

-

2.4 By Geography***

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

-

2.4.2 Europe

-

2.4.2.1 France

-

2.4.2.2 Germany

-

2.4.2.3 Italy

-

2.4.2.4 United Kingdom

-

2.4.2.5 Spain

-

2.4.2.6 Poland

-

2.4.2.7 Nordic

-

-

2.4.3 Asia

-

2.4.3.1 China

-

2.4.3.2 India

-

2.4.3.3 Japan

-

2.4.3.4 Thailand

-

2.4.3.5 Australia and New Zealand

-

2.4.3.6 Indonesia

-

2.4.3.7 Vietnam

-

-

2.4.4 Latin America

-

2.4.4.1 Brazil

-

2.4.4.2 Mexico

-

2.4.4.3 Colombia

-

-

2.4.5 Middle East and Africa

-

2.4.5.1 United Arab Emirates

-

2.4.5.2 Saudi Arabia

-

2.4.5.3 Egypt

-

2.4.5.4 South Africa

-

2.4.5.5 Nigeria

-

2.4.5.6 Morocco

-

-

-

Pouch Packaging Market Size FAQs

How big is the Pouch Packaging Market?

The Pouch Packaging Market size is expected to reach 518.13 billion units in 2024 and grow at a CAGR of 4.03% to reach 631.27 billion units by 2029.

What is the current Pouch Packaging Market size?

In 2024, the Pouch Packaging Market size is expected to reach 518.13 billion units.