| Study Period | 2017 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Market Size (2024) | USD 0.54 Billion |

| Market Size (2029) | USD 1.23 Billion |

| CAGR (2024 - 2029) | 18.05 % |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Market Size")

Polyvinylidene Fluoride (PVDF) Market Analysis

The Polyvinylidene Fluoride (PVDF) Market size is estimated at 0.54 billion USD in 2024, and is expected to reach 1.23 billion USD by 2029, growing at a CAGR of 18.05% during the forecast period (2024-2029).

The polyvinylidene fluoride industry has emerged as a crucial segment within the broader fluoropolymers market, with PVDF accounting for 16.21% of total fluoropolymer consumption in 2022. This significant market position is driven by PVDF's unique combination of properties, including high chemical resistance, UV stability, and flame resistance, making it indispensable across various industrial applications. The material's growing importance is particularly evident in advanced manufacturing initiatives, exemplified by China's ambitious smart manufacturing development plan that aims to digitize 70% of its large enterprises by 2025. This transformation in manufacturing processes has created new opportunities for PVDF market applications, especially in high-precision equipment and smart manufacturing components.

The industry is witnessing substantial investments in PVDF production capacity and technological advancement, particularly in the electrical and electronics sector. A notable example is Schneider's USD 100 million investment in 2022 to boost electrical goods production in North America, demonstrating the industry's commitment to expanding manufacturing capabilities. The focus on technological advancement has led to the development of enhanced PVDF grades with improved performance characteristics, particularly for high-purity applications in semiconductor manufacturing and advanced electronics. These developments have been crucial in addressing the growing demand for high-performance materials in emerging technologies.

The market is experiencing a significant shift toward sustainable and energy-efficient solutions, with PVDF playing a vital role in green technology applications. The material's exceptional chemical resistance and durability make it particularly valuable in renewable energy infrastructure and energy storage systems. This trend is reinforced by stringent environmental regulations and increasing corporate sustainability initiatives, driving the adoption of PVDF in eco-friendly applications. The material's ability to maintain its properties under extreme conditions while offering long-term reliability has made it a preferred choice in sustainable infrastructure projects.

The industry landscape is being reshaped by rapid technological advancements in end-use applications, particularly in high-performance coatings and advanced materials. PVDF's superior properties, including its high tensile strength and resistance to radiation, have made it increasingly important in specialized industrial applications. The material's versatility is demonstrated through its expanding use in critical applications such as chemical processing equipment, where it serves in components like bearings, vessels, pipes, and valve linings. This versatility, combined with ongoing research and development efforts, continues to open new application possibilities across various industrial sectors.

Global Polyvinylidene Fluoride (PVDF) Market Trends

Technological advancements in electronics industry may foster the growth

- The rapid pace of technological innovation in electronic products is driving the consistent demand for new and fast electrical and electronic products. In 2022, the global revenue of electrical and electronics stood at USD 5,807 billion, with Asia-Pacific holding a 74% market share, followed by Europe with a 13% share. The global electrical and electronics market is expected to record a CAGR of 6.61% during the forecast period.

- In 2018, the Asia-Pacific region witnessed strong economic growth owing to rapid industrialization in China, South Korea, Japan, India, and ASEAN countries. In 2020, due to the pandemic, there was a slowdown in global electrical and electronics production due to the shortage of chips and inefficiencies in the supply chain, which led to a stagnant growth rate of 0.1% in revenue compared to the previous year. This growth was driven by the demand for consumer electronics for remote working and home entertainment as people were forced to remain indoors during the pandemic.

- The demand for advanced technologies, such as digitalization, robotics, virtual reality, augmented reality, IoT (Internet of Things), and 5G connectivity, is expected to grow during the forecast period. Global electrical and electronics production is expected to register a growth rate of 5.9% in 2027. As a result of technological advancements, the demand for consumer electronics is expected to rise during the forecast period. For instance, the global consumer electronics industry is projected to witness a revenue reach of around USD 904.6 billion in 2027, compared to USD 719.1 billion in 2023. As a result, technological development is projected to lead the demand for electrical and electronic products during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Fast-paced growth of aviation industry and increased aircraft contracts may aid market growth

- Fast-paced urbanization and investments in Asia-Pacific region may boost the industry

- Growing demand for electric vehicles may boost automobile industry growth

- Demand for flexible packaging from the food and beverage industry boosting market growth

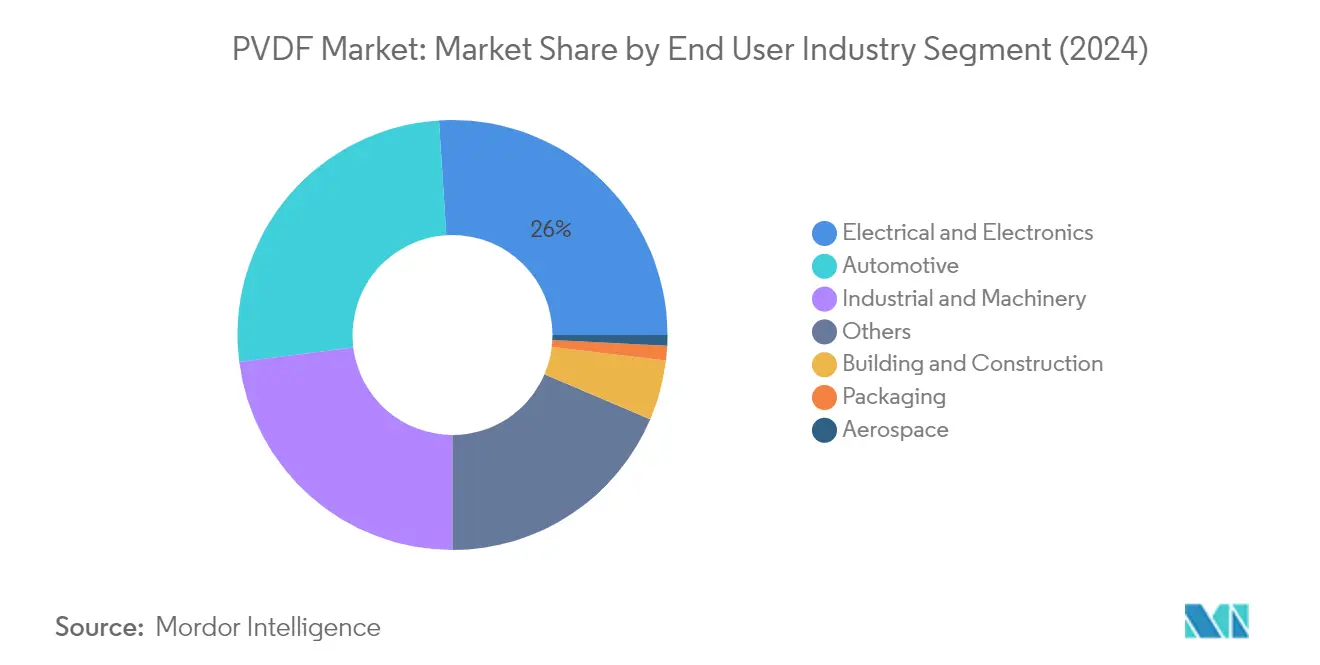

Segment Analysis: End User Industry

Electrical & Electronics Segment in PVDF Market

The Electrical and Electronics segment has emerged as a dominant force in the global polyvinylidene fluoride PVDF market, commanding approximately 26% market share in 2024. This significant market position is primarily driven by PVDF's exceptional properties, including flexibility, lightweight nature, low thermal conductivity, and superior chemical corrosion resistance. The material's widespread adoption in cable insulation applications and its growing use as an insulating material in batteries, particularly lithium-ion batteries, has solidified its position. The segment's prominence is particularly notable in the Asia-Pacific region, where major manufacturing hubs in countries like China, Vietnam, India, Taiwan, and Malaysia contribute significantly to the global demand. The material's high-purity PVDF levels and resistance to various environmental factors make it indispensable in manufacturing critical electronic components and insulation materials.

Automotive Segment in PVDF Market

The Automotive segment is experiencing remarkable growth in the PVDF resin market, with projections indicating an impressive growth rate of approximately 31% from 2024 to 2029. This exceptional growth trajectory is primarily fueled by the increasing adoption of PVDF in various automotive applications, including brake tubes, underbody fasteners, and taillight housings, where its chemical, corrosion, and abrasion-resistant properties prove invaluable. The segment's growth is particularly driven by the expanding electric vehicle (EV) market, where PVDF plays a crucial role in lithium-ion battery production. The material's versatility and performance characteristics align perfectly with the automotive industry's evolving needs for stronger yet lighter materials and improved power-efficient battery requirements, making it an essential component in modern vehicle manufacturing.

Remaining Segments in End User Industry

The PVDF market encompasses several other significant segments, including Industrial and Machinery, Building and Construction, Aerospace, and Packaging, each serving unique applications. The Industrial and Machinery segment utilizes PVDF in bearings, vessels, pipes, and pump impeller casings, benefiting from its excellent tensile strength and radiation resistance. In the Building and Construction sector, PVDF's durability and weather resistance make it ideal for architectural applications and coatings. The Aerospace segment leverages PVDF's flame-resistant properties and insulating qualities for specialized applications, while the Packaging segment utilizes its deformation characteristics and heat resistance for various packaging solutions. These diverse applications demonstrate PVDF's versatility and importance across multiple industries, including the emerging medical-grade PVDF applications.

Polyvinylidene Fluoride (PVDF) Market Geography Segment Analysis

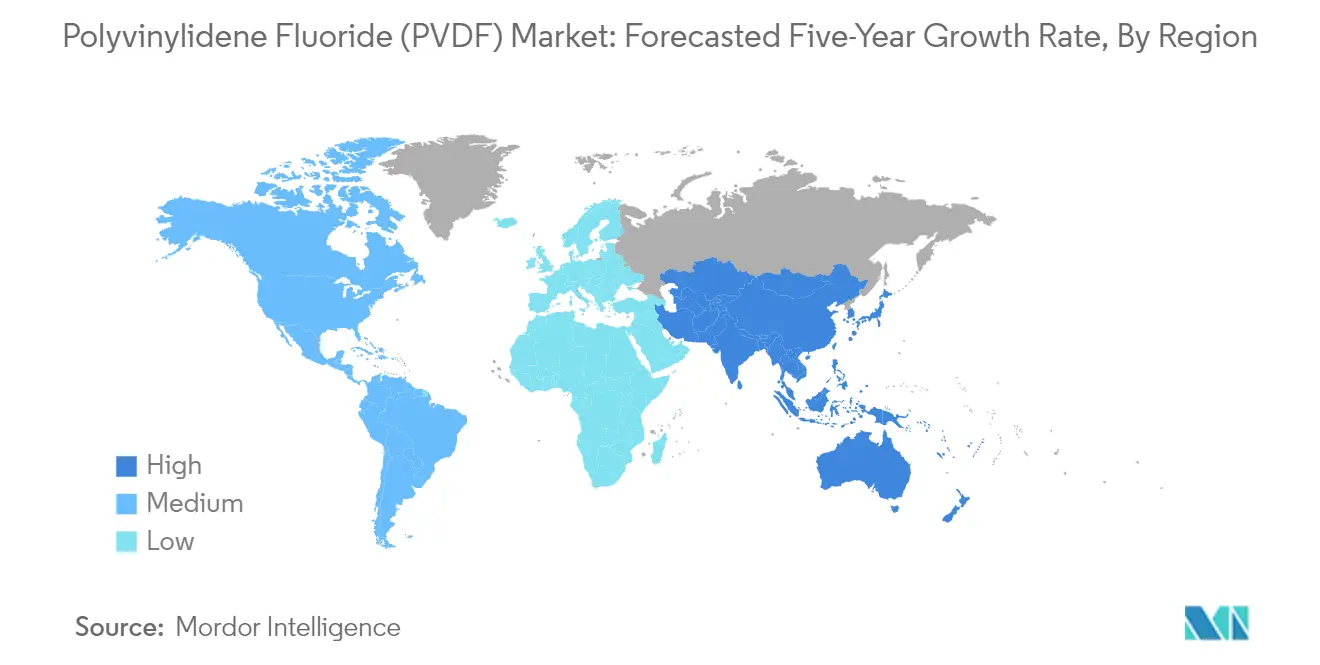

Polyvinylidene Fluoride (PVDF) Market in Asia-Pacific

Asia-Pacific represents the dominant region in the global polyvinylidene fluoride (PVDF) market, driven by its robust manufacturing base across multiple end-use industries. The region's strength lies in its diverse industrial landscape, spanning from automotive and electronics manufacturing hubs in China and South Korea to emerging industrial powerhouses like India and Malaysia. The presence of major electronics manufacturers, growing automotive production, and increasing adoption of PVDF in industrial applications have solidified the region's position as a key market.

Polyvinylidene Fluoride (PVDF) Market in China

China stands as the powerhouse of polyvinylidene fluoride consumption in Asia-Pacific, commanding approximately 60% of the regional market share in 2024. The country's dominance is attributed to its extensive manufacturing capabilities across various sectors, particularly in the electrical and electronics and industrial machinery industries. China's strong position is reinforced by its growing automotive sector, expanding electronics manufacturing base, and increasing adoption of PVDF in various industrial applications. The country's focus on developing advanced manufacturing capabilities and its position as a global manufacturing hub continues to drive substantial PVDF demand.

Polyvinylidene Fluoride (PVDF) Market in India

India emerges as the fastest-growing market for polyvinylidene fluoride (PVDF) in the Asia-Pacific region, with a projected growth rate of approximately 18% during 2024-2029. The country's rapid industrialization, expanding automotive sector, and growing electronics manufacturing capabilities are driving this exceptional growth. India's strategic focus on becoming a global manufacturing hub, coupled with government initiatives promoting domestic manufacturing, has created a favorable environment for PVDF consumption. The country's automotive sector expansion and increasing investments in industrial infrastructure are further catalyzing market growth.

Polyvinylidene Fluoride (PVDF) Market in Europe

The European polyvinylidene fluoride market is characterized by its sophisticated industrial base and strong presence in high-tech manufacturing sectors. The region's market is driven by its advanced automotive industry, robust electronics manufacturing sector, and stringent quality requirements across industries. The presence of major automotive and industrial machinery manufacturers, particularly in Germany, France, and Italy, continues to drive steady demand for PVDF materials.

Polyvinylidene Fluoride (PVDF) Market in Germany

Germany maintains its position as the largest PVDF market in Europe, holding approximately 23% of the regional market share in 2024. The country's leadership is built on its strong industrial machinery sector, advanced automotive manufacturing capabilities, and robust chemical processing industry. Germany's emphasis on high-quality manufacturing and technological innovation continues to drive the demand for PVDF in various applications, particularly in industrial machinery and automotive sectors.

Polyvinylidene Fluoride (PVDF) Market in United Kingdom

The United Kingdom represents the fastest-growing PVDF market in Europe, with an expected growth rate of approximately 8% during 2024-2029. The country's growth is driven by increasing investments in automotive manufacturing, expanding electronics industry, and growing adoption of PVDF in various industrial applications. The UK's focus on sustainable manufacturing practices and technological advancement in its industrial sector continues to create new opportunities for PVDF applications.

Polyvinylidene Fluoride (PVDF) Market in North America

North America represents a mature yet dynamic market for polyvinylidene fluoride, characterized by its advanced manufacturing capabilities and diverse industrial applications. The region's market is primarily driven by the United States' robust industrial base, while Canada and Mexico contribute significantly through their growing manufacturing sectors. The United States leads the regional market as the largest consumer, while Mexico shows the most promising growth potential.

Polyvinylidene Fluoride (PVDF) Market in Middle East

The Middle East PVDF market is experiencing steady growth, driven by increasing industrialization and infrastructure development across the region. Saudi Arabia leads the regional market as the largest consumer, benefiting from its robust industrial sector and growing investments in manufacturing capabilities. The United Arab Emirates emerges as the fastest-growing market, supported by its ambitious industrial development plans and increasing adoption of PVDF in various applications.

Polyvinylidene Fluoride (PVDF) Market in South America

The South American PVDF market demonstrates significant growth potential, driven by increasing industrialization and manufacturing activities across the region. Brazil maintains its position as the largest market, supported by its extensive automotive and industrial sectors. Argentina shows promising growth prospects, emerging as the fastest-growing market in the region, driven by its expanding manufacturing base and increasing investments in industrial infrastructure.

Polyvinylidene Fluoride (PVDF) Market in Africa

The African PVDF market, while relatively smaller compared to other regions, shows promising growth potential driven by increasing industrialization and infrastructure development. South Africa leads the regional market as the largest consumer, benefiting from its relatively advanced manufacturing sector and diverse industrial base. Nigeria emerges as a significant market, supported by its growing automotive and construction sectors, while other African nations are gradually increasing their PVDF consumption as their industrial sectors develop.

Get Analysis on Important Geographic Markets

Download PDF

Polyvinylidene Fluoride (PVDF) Industry Overview

Top Companies in Polyvinylidene Fluoride (PVDF) Market

The polyvinylidene fluoride PVDF market is characterized by significant product innovation efforts focused on developing sustainable and high-performance grades, particularly for emerging applications like lithium-ion batteries and renewable energy. Leading companies are emphasizing capacity expansions, with major investments in new PVDF production facilities across Asia-Pacific and North America to meet growing demand. Strategic partnerships and collaborations, especially in the electric vehicle and energy storage sectors, have become increasingly important for market penetration. Companies are also focusing on vertical integration strategies, securing raw material supplies like fluorspar to maintain competitive advantages. The industry has seen a strong focus on research and development activities to improve product performance and develop specialized grades for specific end-use applications, particularly in high-growth sectors like electronics and automotive.

Consolidated Market Led By Global Players

The global PVDF market exhibits a highly consolidated structure, with the top five companies dominating the majority of the market share. These major players are primarily large chemical conglomerates with diverse product portfolios and a strong global presence, leveraging their extensive distribution networks and technical expertise. The market is characterized by high entry barriers due to complex manufacturing processes, stringent quality requirements, and significant capital investments needed for production facilities.

The competitive landscape is marked by established relationships between major manufacturers and key end-users, particularly in the automotive and electronics sectors. Regional players maintain their presence through specialized product offerings and strong local distribution networks. The market has seen limited merger and acquisition activity, with companies primarily focusing on organic growth through capacity expansions and technology improvements rather than consolidation through acquisitions.

Innovation and Capacity Drive Market Success

For incumbent companies to maintain and expand their market position, a focus on technological innovation and product customization capabilities is crucial. Success factors include developing sustainable production processes, securing long-term supply contracts with key end-users, and maintaining cost competitiveness through operational efficiency. Companies need to strengthen their presence in high-growth regions while investing in research and development to address evolving application requirements, particularly in emerging sectors like electric vehicles and renewable energy.

New entrants and smaller players can gain market share by focusing on specialized applications and niche markets where larger players may have limited presence. Building strong relationships with local customers, offering technical support services, and developing innovative solutions for specific industry challenges are key strategies for market penetration. The ability to comply with evolving environmental regulations and sustainability requirements while maintaining product quality and competitive pricing will be crucial for long-term success in the market.

Polyvinylidene Fluoride (PVDF) Market Leaders

-

Arkema

-

Dongyue Group

-

Kureha Corporation

-

Sinochem

-

Solvay

- *Disclaimer: Major Players sorted in no particular order

Market/1708339753095_PolyvinylideneFluoride(PVDF)Market_market_concentration.svg)

Need More Details on Market Players and Competiters?

Download PDF

Polyvinylidene Fluoride (PVDF) Market News

- November 2022: Solvay and Orbia announced a framework agreement to form a partnership for the production of suspension-grade polyvinylidene fluoride (PVDF) for battery materials, resulting in the largest capacity in North America.

- October 2022: Dongyue Group completed the construction of its PVDF project with a capacity of around 10,000 tons per year in China. Upon completion of this project, the company's total PVDF production capacity reached 25,000 tons/year.

- February 2022: Solvay announced the product expansion of Solef, a PVDF resin brand with the largest production site in Europe.

Free With This Report

We provide a complimentary and exhaustive set of data points on global and regional metrics that present the fundamental structure of the industry. Presented in the form of 15+ free charts, the section covers rare data on various end-user production trends including passenger vehicle production, commercial vehicle production, motorcycle production, aerospace components production, electrical and electronics production, and regional data for engineering plastics demand etc.

Polyvinylidene Fluoride (PVDF) Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Lithium-ion (Li-ion) Battery - A Major Driving Factor for PVDF Demand

-

4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 EU

- 4.3.7 India

- 4.3.8 Japan

- 4.3.9 Malaysia

- 4.3.10 Mexico

- 4.3.11 Nigeria

- 4.3.12 Russia

- 4.3.13 Saudi Arabia

- 4.3.14 South Africa

- 4.3.15 South Korea

- 4.3.16 United Arab Emirates

- 4.3.17 United Kingdom

- 4.3.18 United States

- 4.4 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

-

5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Country

- 5.2.1.1.1 Nigeria

- 5.2.1.1.2 South Africa

- 5.2.1.1.3 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Country

- 5.2.2.1.1 Australia

- 5.2.2.1.2 China

- 5.2.2.1.3 India

- 5.2.2.1.4 Japan

- 5.2.2.1.5 Malaysia

- 5.2.2.1.6 South Korea

- 5.2.2.1.7 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Country

- 5.2.3.1.1 France

- 5.2.3.1.2 Germany

- 5.2.3.1.3 Italy

- 5.2.3.1.4 Russia

- 5.2.3.1.5 United Kingdom

- 5.2.3.1.6 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Country

- 5.2.4.1.1 Saudi Arabia

- 5.2.4.1.2 United Arab Emirates

- 5.2.4.1.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Country

- 5.2.5.1.1 Canada

- 5.2.5.1.2 Mexico

- 5.2.5.1.3 United States

- 5.2.6 South America

- 5.2.6.1 By Country

- 5.2.6.1.1 Argentina

- 5.2.6.1.2 Brazil

- 5.2.6.1.3 Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Dongyue Group

- 6.4.4 Hubei Everflon Polymer Co., Ltd.

- 6.4.5 Kureha Corporation

- 6.4.6 RTP Company

- 6.4.7 Sinochem

- 6.4.8 Solvay

- 6.4.9 Zhejiang Juhua Co., Ltd.

- 6.4.10 ZheJiang Yonghe Refrigerant Co.,Ltd

7. KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- PRODUCTION REVENUE OF AEROSPACE COMPONENTS, USD, GLOBAL, 2017 - 2029

- Figure 2:

- PRODUCTION VOLUME OF AUTOMOBILES, UNITS, GLOBAL, 2017 - 2029

- Figure 3:

- FLOOR AREA OF NEW CONSTRUCTION, SQUARE FEET, GLOBAL, 2017 - 2029

- Figure 4:

- PRODUCTION REVENUE OF ELECTRICAL AND ELECTRONICS, USD, GLOBAL, 2017 - 2029

- Figure 5:

- PRODUCTION VOLUME OF PLASTIC PACKAGING, TONS, GLOBAL, 2017 - 2029

- Figure 6:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, GLOBAL, 2017 - 2029

- Figure 7:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, GLOBAL, 2017 - 2029

- Figure 8:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, TONS, GLOBAL, 2017 - 2029

- Figure 9:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, USD, GLOBAL, 2017 - 2029

- Figure 10:

- VOLUME SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, GLOBAL, 2017, 2023, AND 2029

- Figure 11:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, GLOBAL, 2017, 2023, AND 2029

- Figure 12:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN AEROSPACE INDUSTRY, TONS, GLOBAL, 2017 - 2029

- Figure 13:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN AEROSPACE INDUSTRY, USD, GLOBAL, 2017 - 2029

- Figure 14:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN AEROSPACE INDUSTRY BY REGION, %, GLOBAL, 2022 VS 2029

- Figure 15:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN AUTOMOTIVE INDUSTRY, TONS, GLOBAL, 2017 - 2029

- Figure 16:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN AUTOMOTIVE INDUSTRY, USD, GLOBAL, 2017 - 2029

- Figure 17:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN AUTOMOTIVE INDUSTRY BY REGION, %, GLOBAL, 2022 VS 2029

- Figure 18:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN BUILDING AND CONSTRUCTION INDUSTRY, TONS, GLOBAL, 2017 - 2029

- Figure 19:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN BUILDING AND CONSTRUCTION INDUSTRY, USD, GLOBAL, 2017 - 2029

- Figure 20:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN BUILDING AND CONSTRUCTION INDUSTRY BY REGION, %, GLOBAL, 2022 VS 2029

- Figure 21:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN ELECTRICAL AND ELECTRONICS INDUSTRY, TONS, GLOBAL, 2017 - 2029

- Figure 22:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN ELECTRICAL AND ELECTRONICS INDUSTRY, USD, GLOBAL, 2017 - 2029

- Figure 23:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN ELECTRICAL AND ELECTRONICS INDUSTRY BY REGION, %, GLOBAL, 2022 VS 2029

- Figure 24:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN INDUSTRIAL AND MACHINERY INDUSTRY, TONS, GLOBAL, 2017 - 2029

- Figure 25:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN INDUSTRIAL AND MACHINERY INDUSTRY, USD, GLOBAL, 2017 - 2029

- Figure 26:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN INDUSTRIAL AND MACHINERY INDUSTRY BY REGION, %, GLOBAL, 2022 VS 2029

- Figure 27:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN PACKAGING INDUSTRY, TONS, GLOBAL, 2017 - 2029

- Figure 28:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN PACKAGING INDUSTRY, USD, GLOBAL, 2017 - 2029

- Figure 29:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN PACKAGING INDUSTRY BY REGION, %, GLOBAL, 2022 VS 2029

- Figure 30:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN OTHER END-USER INDUSTRIES INDUSTRY, TONS, GLOBAL, 2017 - 2029

- Figure 31:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN OTHER END-USER INDUSTRIES INDUSTRY, USD, GLOBAL, 2017 - 2029

- Figure 32:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED IN OTHER END-USER INDUSTRIES INDUSTRY BY REGION, %, GLOBAL, 2022 VS 2029

- Figure 33:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY REGION, TONS, GLOBAL, 2017 - 2029

- Figure 34:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY REGION, USD, GLOBAL, 2017 - 2029

- Figure 35:

- VOLUME SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY REGION, %, GLOBAL, 2017, 2023, AND 2029

- Figure 36:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY REGION, %, GLOBAL, 2017, 2023, AND 2029

- Figure 37:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, TONS, AFRICA, 2017 - 2029

- Figure 38:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, USD, AFRICA, 2017 - 2029

- Figure 39:

- VOLUME SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, AFRICA, 2017, 2023, AND 2029

- Figure 40:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, AFRICA, 2017, 2023, AND 2029

- Figure 41:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, NIGERIA, 2017 - 2029

- Figure 42:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, NIGERIA, 2017 - 2029

- Figure 43:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, NIGERIA, 2022 VS 2029

- Figure 44:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, SOUTH AFRICA, 2017 - 2029

- Figure 45:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, SOUTH AFRICA, 2017 - 2029

- Figure 46:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, SOUTH AFRICA, 2022 VS 2029

- Figure 47:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, REST OF AFRICA, 2017 - 2029

- Figure 48:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, REST OF AFRICA, 2017 - 2029

- Figure 49:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, REST OF AFRICA, 2022 VS 2029

- Figure 50:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, TONS, ASIA-PACIFIC, 2017 - 2029

- Figure 51:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 52:

- VOLUME SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, ASIA-PACIFIC, 2017, 2023, AND 2029

- Figure 53:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, ASIA-PACIFIC, 2017, 2023, AND 2029

- Figure 54:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, AUSTRALIA, 2017 - 2029

- Figure 55:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, AUSTRALIA, 2017 - 2029

- Figure 56:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, AUSTRALIA, 2022 VS 2029

- Figure 57:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, CHINA, 2017 - 2029

- Figure 58:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, CHINA, 2017 - 2029

- Figure 59:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, CHINA, 2022 VS 2029

- Figure 60:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, INDIA, 2017 - 2029

- Figure 61:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, INDIA, 2017 - 2029

- Figure 62:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, INDIA, 2022 VS 2029

- Figure 63:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, JAPAN, 2017 - 2029

- Figure 64:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, JAPAN, 2017 - 2029

- Figure 65:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, JAPAN, 2022 VS 2029

- Figure 66:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, MALAYSIA, 2017 - 2029

- Figure 67:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, MALAYSIA, 2017 - 2029

- Figure 68:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, MALAYSIA, 2022 VS 2029

- Figure 69:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, SOUTH KOREA, 2017 - 2029

- Figure 70:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, SOUTH KOREA, 2017 - 2029

- Figure 71:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, SOUTH KOREA, 2022 VS 2029

- Figure 72:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, REST OF ASIA-PACIFIC, 2017 - 2029

- Figure 73:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, REST OF ASIA-PACIFIC, 2017 - 2029

- Figure 74:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, REST OF ASIA-PACIFIC, 2022 VS 2029

- Figure 75:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, TONS, EUROPE, 2017 - 2029

- Figure 76:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, USD, EUROPE, 2017 - 2029

- Figure 77:

- VOLUME SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, EUROPE, 2017, 2023, AND 2029

- Figure 78:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, EUROPE, 2017, 2023, AND 2029

- Figure 79:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, FRANCE, 2017 - 2029

- Figure 80:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, FRANCE, 2017 - 2029

- Figure 81:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, FRANCE, 2022 VS 2029

- Figure 82:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, GERMANY, 2017 - 2029

- Figure 83:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, GERMANY, 2017 - 2029

- Figure 84:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, GERMANY, 2022 VS 2029

- Figure 85:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, ITALY, 2017 - 2029

- Figure 86:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, ITALY, 2017 - 2029

- Figure 87:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, ITALY, 2022 VS 2029

- Figure 88:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, RUSSIA, 2017 - 2029

- Figure 89:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, RUSSIA, 2017 - 2029

- Figure 90:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, RUSSIA, 2022 VS 2029

- Figure 91:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, UNITED KINGDOM, 2017 - 2029

- Figure 92:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, UNITED KINGDOM, 2017 - 2029

- Figure 93:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, UNITED KINGDOM, 2022 VS 2029

- Figure 94:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, REST OF EUROPE, 2017 - 2029

- Figure 95:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, REST OF EUROPE, 2017 - 2029

- Figure 96:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, REST OF EUROPE, 2022 VS 2029

- Figure 97:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, TONS, MIDDLE EAST, 2017 - 2029

- Figure 98:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, USD, MIDDLE EAST, 2017 - 2029

- Figure 99:

- VOLUME SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, MIDDLE EAST, 2017, 2023, AND 2029

- Figure 100:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, MIDDLE EAST, 2017, 2023, AND 2029

- Figure 101:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, SAUDI ARABIA, 2017 - 2029

- Figure 102:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, SAUDI ARABIA, 2017 - 2029

- Figure 103:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, SAUDI ARABIA, 2022 VS 2029

- Figure 104:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, UNITED ARAB EMIRATES, 2017 - 2029

- Figure 105:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, UNITED ARAB EMIRATES, 2017 - 2029

- Figure 106:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, UNITED ARAB EMIRATES, 2022 VS 2029

- Figure 107:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, REST OF MIDDLE EAST, 2017 - 2029

- Figure 108:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, REST OF MIDDLE EAST, 2017 - 2029

- Figure 109:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, REST OF MIDDLE EAST, 2022 VS 2029

- Figure 110:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, TONS, NORTH AMERICA, 2017 - 2029

- Figure 111:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, USD, NORTH AMERICA, 2017 - 2029

- Figure 112:

- VOLUME SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, NORTH AMERICA, 2017, 2023, AND 2029

- Figure 113:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, NORTH AMERICA, 2017, 2023, AND 2029

- Figure 114:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, CANADA, 2017 - 2029

- Figure 115:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, CANADA, 2017 - 2029

- Figure 116:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, CANADA, 2022 VS 2029

- Figure 117:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, MEXICO, 2017 - 2029

- Figure 118:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, MEXICO, 2017 - 2029

- Figure 119:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, MEXICO, 2022 VS 2029

- Figure 120:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, UNITED STATES, 2017 - 2029

- Figure 121:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, UNITED STATES, 2017 - 2029

- Figure 122:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, UNITED STATES, 2022 VS 2029

- Figure 123:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, TONS, SOUTH AMERICA, 2017 - 2029

- Figure 124:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, USD, SOUTH AMERICA, 2017 - 2029

- Figure 125:

- VOLUME SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, SOUTH AMERICA, 2017, 2023, AND 2029

- Figure 126:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY COUNTRY, %, SOUTH AMERICA, 2017, 2023, AND 2029

- Figure 127:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, ARGENTINA, 2017 - 2029

- Figure 128:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, ARGENTINA, 2017 - 2029

- Figure 129:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, ARGENTINA, 2022 VS 2029

- Figure 130:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, BRAZIL, 2017 - 2029

- Figure 131:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, BRAZIL, 2017 - 2029

- Figure 132:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, BRAZIL, 2022 VS 2029

- Figure 133:

- VOLUME OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, TONS, REST OF SOUTH AMERICA, 2017 - 2029

- Figure 134:

- VALUE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED, USD, REST OF SOUTH AMERICA, 2017 - 2029

- Figure 135:

- VALUE SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) CONSUMED BY END USER INDUSTRY, %, REST OF SOUTH AMERICA, 2022 VS 2029

- Figure 136:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, GLOBAL, 2019 - 2021

- Figure 137:

- MOST ADOPTED STRATEGIES, COUNT, GLOBAL, 2019 - 2021

- Figure 138:

- PRODUCTION CAPACITY SHARE OF POLYVINYLIDENE FLUORIDE (PVDF) BY MAJOR PLAYERS, %, GLOBAL, 2022

Polyvinylidene Fluoride (PVDF) Industry Segmentation

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.| End User Industry | Aerospace | |||

| Automotive | ||||

| Building and Construction | ||||

| Electrical and Electronics | ||||

| Industrial and Machinery | ||||

| Packaging | ||||

| Other End-user Industries | ||||

| Region | Africa | By Country | Nigeria | |

| South Africa | ||||

| Rest of Africa | ||||

| Asia-Pacific | By Country | Australia | ||

| China | ||||

| India | ||||

| Japan | ||||

| Malaysia | ||||

| South Korea | ||||

| Rest of Asia-Pacific | ||||

| Europe | By Country | France | ||

| Germany | ||||

| Italy | ||||

| Russia | ||||

| United Kingdom | ||||

| Rest of Europe | ||||

| Middle East | By Country | Saudi Arabia | ||

| United Arab Emirates | ||||

| Rest of Middle East | ||||

| North America | By Country | Canada | ||

| Mexico | ||||

| United States | ||||

| South America | By Country | Argentina | ||

| Brazil | ||||

| Rest of South America | ||||

Need A Different Region or Segment?

Customize Now

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyvinylidene fluoride market.

- Resin - Under the scope of the study, virgin polyvinylidene fluoride resin in the primary forms such as powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF