| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 1.59 Billion |

| Market Size (2030) | USD 1.84 Billion |

| CAGR (2025 - 2030) | 3.04 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Coated Films Market Major Players")

Coated Films Market Size")

PVDC Coated Films Market Analysis

The Polyvinylidene Chloride Coated Films Market size is estimated at USD 1.59 billion in 2025, and is expected to reach USD 1.84 billion by 2030, at a CAGR of 3.04% during the forecast period (2025-2030).

The global PVDC Coated Films industry is experiencing significant transformation driven by evolving regulatory landscapes and sustainability initiatives. In February 2023, Colombia became the second country in Latin America to launch the Plastics Pact, focusing on creating a more circular economy for plastics by working across the packaging value chain. This initiative reflects the broader industry shift towards sustainable packaging solutions, with many manufacturers investing in research and development to create eco-friendly alternatives. The pharmaceutical sector remains a crucial end-user, with China's market showing substantial growth potential as over 90% of drugs registered in the country are generic, indicating a strong demand for cost-effective packaging solutions.

The packaging industry is witnessing substantial technological advancements and capacity expansions across key markets. In February 2023, Amcor announced the opening of its new advanced manufacturing facility for flexible packaging in Huizhou, China, with an investment of around USD 100 million. This facility, one of the largest flexible packaging plants by manufacturing capacity in China, is equipped with high-speed printing presses, laminators, and bag-making machines that can deliver double-digit reductions in manufacturing cycle times. Such developments are reshaping the industry's production capabilities and efficiency standards.

The pharmaceutical packaging segment is experiencing significant growth, driven by increasing healthcare expenditure and expanding generic drug markets. According to the United States Department of Agriculture (USDA), in 2022, the country exported USD 874.8 million worth of sweet bakery products and mixes and USD 1.9 billion worth of chocolate and cocoa products across the globe, indicating robust demand for high-performance packaging solutions. The industry is also witnessing major infrastructure developments, such as Bayer's ongoing development of the Solida-1 pharmaceutical production facility in Leverkusen, expected to be operational in 2024.

The market is experiencing a notable shift in regional manufacturing capabilities and trade dynamics. In Germany, the food industry is expected to generate USD 245.50 billion in revenue in 2023 and is projected to grow by 3.64% annually between 2023-27, indicating strong potential for packaging applications. This growth is complemented by increasing investments in advanced manufacturing facilities and the development of specialized PVDC Coating technologies. Industry players are focusing on developing multi-functional films that offer enhanced barrier properties while meeting evolving regulatory requirements and sustainability goals.

PVDC Coated Films Market Trends

GROWING PROCESSED FOOD INDUSTRY

The processed food industry has emerged as a significant driver for PVDC-coated films market, primarily due to the material's superior barrier properties and protective characteristics. According to the US Department of Agriculture (USDA), the total export of processed food products reached USD 38 billion in 2022, with Canada being the largest market, importing USD 11.43 billion worth of processed foods. The industry's growth is further evidenced by significant exports of sweet bakery products and mixes (USD 874.8 million) and chocolate and cocoa products (USD 1.9 billion) across the globe in 2022. These statistics underscore the increasing demand for high-quality packaging solutions that can preserve food quality and extend shelf life, making PVDC-coated films an ideal choice due to their excellent barrier properties against moisture, oxygen, and aroma.

The changing dynamics of consumer behavior and lifestyle patterns have significantly influenced the processed food packaging industry. PVDC-coated films have gained prominence due to their non-toxic, tasteless, and odorless properties, combined with excellent heat-sealing characteristics and superior flexibility. The films are extensively used in packaging various processed foods, including cheese, breakfast cereals, bread, cakes, biscuits, chips, ready-to-eat meals, condiments, sauces, and dairy products. The growing trend of convenience foods and ready-to-eat meals has further accelerated the demand for these films, as they provide exceptional protection against moisture loss, moisture gain, oxidation of ingredients, and aroma and flavor loss, while also preventing oil or gas permeation. The use of PVDC food packaging is critical in maintaining these qualities.

Understand The Key Trends Shaping This Market

Download PDF

USAGE OF PVDC-COATED FILMS IN FRESH MEAT PACKAGING

The meat industry's specific packaging requirements have become a crucial driver for PVDC-coated films, particularly due to their superior barrier properties in both dry and high-moisture environments. According to the Food and Agriculture Organization (FAO), the total meat production across the globe accounted for approximately 340 million tonnes in 2022, with projections indicating an increase to 377 Mt by 2031. This substantial production volume requires sophisticated packaging solutions that can maintain product freshness and safety throughout the supply chain. PVDC-coated films have emerged as an optimal solution due to their ability to extend meat product shelf life up to 100 days, significantly reducing food waste and maintaining product quality during transportation and storage.

The increasing consumption of poultry meat has created additional demand for effective packaging solutions, with PVDC film playing a crucial role in this segment. Global poultry meat consumption is projected to increase to 154 Mt by 2031, accounting for nearly half of the additional meat consumed. The poultry meat production is expected to show consistent growth, reaching 147,725 kt ready-to-cook (RTC) by 2028. PVDC film is particularly valuable in this sector as it provides excellent permeability properties that remain unaffected by relative humidity, making it ideal for packaging meat products in wet and humid environments. Their ability to maintain barrier properties when exposed to high-moisture environments, combined with excellent abrasion resistance during transport, storage, and distribution, makes them essential for maintaining product quality and safety in the meat packaging industry. The use of PVDC barrier material is essential for these applications.

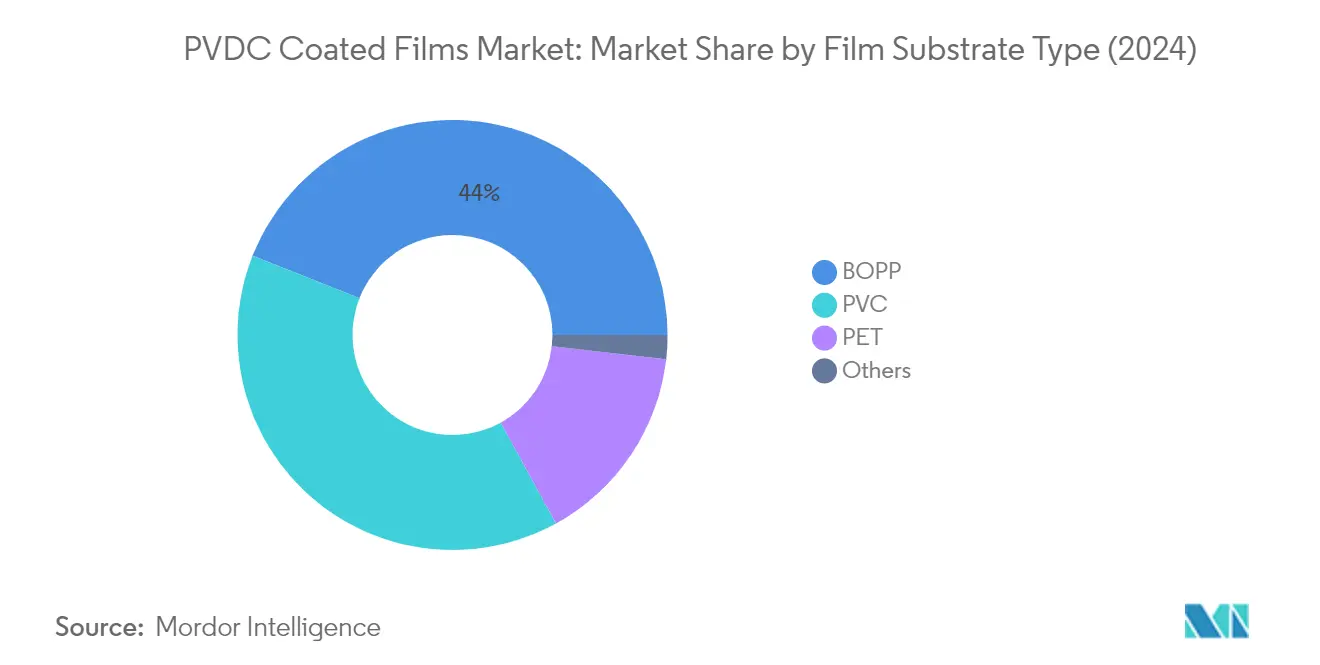

Segment Analysis: Film Substrate Type

BOPP Segment in PVDC Coated Films Market

Bi-axially Oriented Polypropylene (BOPP) continues to dominate the PVDC coated films market, commanding approximately 44% of the market share in 2024. The segment's leadership position is attributed to BOPP films' excellent clarity and smooth surface, along with good chemical and abrasion resistance. These films are widely preferred to achieve good moisture barrier properties and find major applications in food and beverage, personal care, and cosmetics packaging. The PVDC-coated BOPP films exhibit high gloss, ensuring a luxury appeal for products in the cosmetics and beverage category. Additionally, these films offer unmatched advantages in preserving aroma and demonstrate high resistance to both acids and bases, making them particularly suitable for packaging dairy products, foodstuff, and coffee.

PET Segment in PVDC Coated Films Market

The Polyethylene Terephthalate (PET) segment is emerging as the fastest-growing category in the PVDC coated films market for the period 2024-2029. This growth is driven by PVDC PET films' outstanding barrier properties to gas and water vapor, coupled with their suitability for direct contact with food. The segment's expansion is further supported by its good resistance to high and low temperatures, along with excellent resistance to chemicals and effectiveness as a barrier against flavors and oils. These properties make PET films particularly suitable for packaging stored in ambient or cold conditions, high barrier vacuum applications, and modified atmosphere transparent packaging for products like fresh pasta, processed meat, mayonnaise, and cosmetics. The versatility of PET films in lidding, stand-up pouches, and vertical or horizontal FFS applications is also contributing to their increasing adoption across various end-use industries.

Remaining Segments in Film Substrate Type

The remaining segments in the PVDC coated films market include Polyvinyl Chloride (PVC) and other substrate types. PVDC coated PVC film, also known as vinyl films, represent a significant portion of the market and are particularly dominant in pharmaceutical blister packaging applications. These films can be manufactured with varying degrees of rigidity and flexibility, offering different finishes including clear, colored, translucent, opaque, matte, or glossy. The other substrate types segment includes specialized films like BOPET, BOPA, PE films, and ONY films, which cater to specific niche applications in the packaging industry. These alternative substrates provide unique properties such as enhanced cavities for packaging and specialized barrier properties for specific end-use requirements.

Segment Analysis: Application

Food Packaging Segment in PVDC Coated Films Market

The food packaging segment dominates the PVDC coated films market, accounting for approximately 63% of the total market share in 2024. This significant market position is driven by the superior properties of PVDC-coated films, including high chemical resistance, inertness, and low odor characteristics. The films' optical clarity and high gloss, combined with oxygen and moisture barrier properties comparable to metallized films, make them particularly suitable for food packaging applications. The segment's growth is further supported by changing consumer behavior, particularly the increasing demand for processed and convenience foods. PVDC-coated films' excellent bond strength, low water absorption, and superior cling properties make them ideal for food wrapping applications, especially in protecting contents from toxins and moisture while preventing spillage and tampering.

Pharmaceutical Blister Packaging Segment in PVDC Coated Films Market

The pharmaceutical blister packaging segment is experiencing robust growth in the PVDC coated films market, projected to expand significantly from 2024 to 2029. This growth is primarily driven by the increasing demand for high-barrier packaging solutions in the pharmaceutical industry, particularly for moisture-sensitive drugs and medications. The segment's expansion is supported by stringent regulatory requirements for pharmaceutical packaging, where PVDC-coated films' superior barrier properties against moisture, oxygen, and other environmental factors make them particularly valuable. The growth is further accelerated by the rising global pharmaceutical production, especially in emerging markets, and the increasing preference for blister packaging in drug delivery systems. The segment also benefits from the growing focus on patient compliance and drug stability, where PVDC-coated films' ability to protect sensitive medications from environmental factors plays a crucial role.

Polyvinylidene Chloride (PVDC) Coated Films Market Geography Segment Analysis

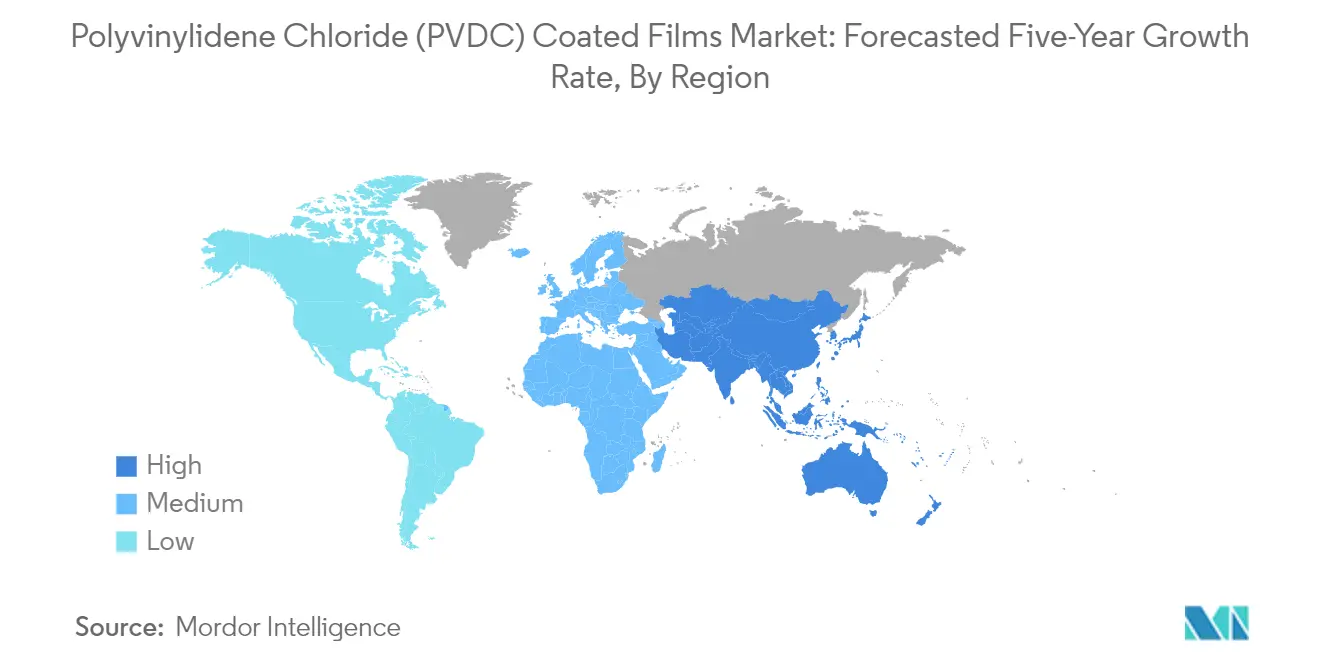

Polyvinylidene Chloride (PVDC) Coated Films Market in Asia-Pacific

The Asia-Pacific region represents the dominant force in the global PVDC coated films market, driven by robust growth in food processing, pharmaceutical manufacturing, and packaging industries. Countries like China, India, Japan, and South Korea are witnessing increased demand for high-barrier packaging solutions across various applications. The region's growth is supported by expanding middle-class populations, changing consumer preferences for packaged foods, and significant investments in pharmaceutical manufacturing capabilities. Rising environmental awareness and sustainability concerns are also shaping market dynamics, with manufacturers focusing on developing more eco-friendly alternatives while maintaining barrier properties.

Polyvinylidene Chloride (PVDC) Coated Films Market in China

China leads the Asia-Pacific PVDC coated films market, commanding approximately 35% of the regional market share in 2024. The country's dominance is attributed to its massive food processing industry and extensive pharmaceutical manufacturing base. China's packaging industry has witnessed consistent growth, with food packaging accounting for roughly 60% of the total market share. The country's pharmaceutical sector continues to expand, supported by government initiatives and increasing healthcare expenditure. The presence of numerous food and beverage manufacturers, coupled with rising domestic consumption and export activities, further strengthens China's position in the regional market.

Polyvinylidene Chloride (PVDC) Coated Films Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with an expected growth rate of approximately 5% during 2024-2029. The country's rapid expansion is driven by increasing urbanization, rising disposable incomes, and growing demand for packaged food products. India's pharmaceutical sector, being one of the largest globally, continues to drive demand for high-barrier packaging solutions. The government's initiatives to boost domestic pharmaceutical manufacturing and the food processing industry are creating new opportunities for PVDC coated films manufacturers. The country's packaging industry is witnessing significant technological advancements and capacity expansions to meet the growing demand from various end-user industries.

Polyvinylidene Chloride (PVDC) Coated Films Market in North America

North America represents a mature market for PVDC coated films, characterized by advanced packaging technologies and stringent quality standards. The region's market is driven by strong demand from the pharmaceutical and food packaging sectors, particularly in the United States, Canada, and Mexico. The presence of major pharmaceutical manufacturers and food processing companies continues to support market growth. Innovation in packaging solutions, focus on extended shelf life, and increasing demand for convenience foods are key factors shaping the market dynamics in this region.

Polyvinylidene Chloride (PVDC) Coated Films Market in United States

The United States dominates the North American market, accounting for approximately 80% of the regional market share in 2024. The country's leadership position is supported by its extensive pharmaceutical industry and large-scale food processing sector. The United States boasts one of the world's most advanced healthcare systems and pharmaceutical manufacturing capabilities, driving consistent demand for high-barrier packaging solutions. The country's food and beverage industry continues to innovate in packaging solutions, particularly focusing on extended shelf life and product protection.

Polyvinylidene Chloride (PVDC) Coated Films Market in Mexico

Mexico demonstrates the highest growth potential in North America, with an anticipated growth rate of approximately 4% during 2024-2029. The country's expanding pharmaceutical manufacturing base and growing food processing industry are key drivers of market growth. Mexico's strategic location and trade agreements with major economies have attracted significant investments in manufacturing capabilities. The country's packaging industry is undergoing rapid modernization, with increasing adoption of advanced packaging solutions to meet international standards and growing domestic demand.

Polyvinylidene Chloride (PVDC) Coated Films Market in Europe

Europe maintains a significant presence in the global PVDC coated films market, with a well-established packaging industry and strong focus on pharmaceutical manufacturing. The region encompasses key markets including Germany, United Kingdom, Italy, and France, each contributing significantly to market growth. Environmental regulations and sustainability initiatives are particularly influential in shaping market dynamics across European countries. The region's pharmaceutical sector and food processing industry continue to drive demand for high-barrier packaging solutions.

Polyvinylidene Chloride (PVDC) Coated Films Market in Germany

Germany stands as the largest market for PVDC coated films in Europe, supported by its robust pharmaceutical and food packaging industries. The country's leadership in manufacturing technologies and packaging innovations continues to drive market growth. Germany's pharmaceutical sector, being one of the largest in Europe, maintains consistent demand for high-quality packaging materials. The country's food and beverage industry, particularly in processed foods and dairy products, further strengthens the market for PVDC coated films.

Polyvinylidene Chloride (PVDC) Coated Films Market in United Kingdom

The United Kingdom emerges as the fastest-growing market in Europe, demonstrating strong potential in the PVDC coated films sector. The country's pharmaceutical industry continues to drive innovation in packaging solutions, supported by significant research and development activities. The UK's food packaging sector maintains steady growth, particularly in convenience foods and ready-to-eat meals. Despite regulatory challenges, the market continues to evolve with increasing focus on sustainable packaging solutions while maintaining essential barrier properties.

Polyvinylidene Chloride (PVDC) Coated Films Market in South America

South America represents an emerging market for PVDC coated films, with Brazil and Argentina being the key contributors to regional growth. The market is characterized by increasing demand from the pharmaceutical and food packaging sectors, particularly in Brazil, which leads the region in terms of market size. Argentina demonstrates the highest growth potential in the region, driven by its expanding pharmaceutical sector and food processing industry. The region's market growth is supported by increasing urbanization, rising disposable incomes, and growing demand for packaged food products. Local manufacturers are focusing on technological upgrades and capacity expansions to meet the growing demand from various end-user industries.

Polyvinylidene Chloride (PVDC) Coated Films Market in Middle East & Africa

The Middle East & Africa region shows promising growth potential in the PVDC coated films market, with Saudi Arabia and South Africa emerging as key markets. Saudi Arabia leads the region in terms of market size, supported by its growing pharmaceutical sector and food processing industry. South Africa demonstrates the highest growth potential, driven by increasing investments in pharmaceutical manufacturing and packaging solutions. The region's market is characterized by growing urbanization, increasing healthcare expenditure, and rising demand for packaged food products. Government initiatives to boost domestic manufacturing capabilities and increasing foreign investments are expected to further drive market growth in the region.

Get Analysis on Important Geographic Markets

Download PDF

PVDC Coated Films Industry Overview

Top Companies in PVDC Coated Films Market

The global PVDC coated films market is led by established players like Innovia Films, Perlen Packaging AG, and Kureha Corporation, who have maintained their positions through continuous innovation and strategic expansion. Companies across the industry are focusing on developing sustainable and eco-friendly PVDC coating alternatives while maintaining high barrier properties to address growing environmental concerns. Operational excellence is being achieved through investments in advanced manufacturing technologies and automation to improve production efficiency and quality consistency. Strategic moves in the industry include vertical integration to control raw material supply, geographic expansion through new manufacturing facilities, and strengthening distribution networks in emerging markets. Companies are also emphasizing research and development to create specialized products for pharmaceutical and food packaging applications, while simultaneously pursuing certifications and compliance with international quality standards to enhance their market credibility.

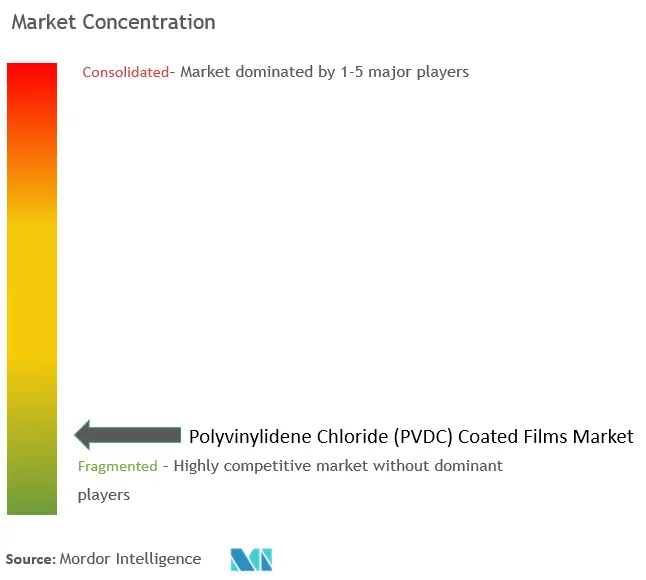

Fragmented Market with Strong Regional Players

The PVDC coated films market exhibits a mix of global conglomerates and specialized regional manufacturers, creating a relatively fragmented competitive landscape. Global players leverage their extensive research capabilities, established distribution networks, and economies of scale to maintain market leadership, while regional specialists thrive by offering customized solutions and maintaining strong relationships with local customers. The market has witnessed significant consolidation through strategic acquisitions, particularly by larger companies looking to expand their geographic presence and product portfolio, as exemplified by CCL Industries' acquisition of Treofan and Flexpol to strengthen Innovia Films' market position.

The competitive dynamics are further shaped by the presence of backward-integrated companies that manufacture both PVDC film manufacturers and coated films, giving them a competitive advantage in terms of cost and supply chain control. Market participants are increasingly focusing on developing value-added products and establishing long-term partnerships with end-users to maintain their competitive edge. The industry also sees collaboration between companies for technology sharing and market access, particularly in regions with stringent regulatory requirements or specific technical expertise needs.

Innovation and Sustainability Drive Future Success

For incumbent players to maintain and expand their market share, a multi-faceted approach combining technological innovation, sustainability initiatives, and strategic partnerships is crucial. Companies need to invest in developing alternative coating technologies that provide similar barrier properties while meeting increasingly stringent environmental regulations. The ability to offer comprehensive packaging solutions, rather than just products, will become increasingly important as end-users seek partners who can provide technical support and customization capabilities. Market leaders must also focus on digitalizing their operations and implementing smart manufacturing practices to improve efficiency and reduce costs.

New entrants and challenger companies can gain ground by focusing on niche applications and underserved markets, particularly in regions with growing pharmaceutical and food packaging demands. Success in the market will increasingly depend on the ability to navigate regulatory challenges, particularly regarding environmental compliance and food safety standards. Companies must also address the growing threat of substitutes by demonstrating superior performance characteristics and cost-effectiveness of their PVDC coated films. Building strong relationships with key end-users through excellent technical support and responsive customer service will be crucial for long-term success, as will the ability to quickly adapt to changing market requirements and consumer preferences.

PVDC Coated Films Market Leaders

-

UNITIKA LTD

-

Perlen Packaging

-

KUREHA CORPORATION

-

Innovia Films

-

Vibac Group S.p.a.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

PVDC Coated Films Market News

- April 2022: Jindal Poly Films, a wholly owned subsidiary of Jindal PolyPack, acquired SMI Coated Products. The acquisition helped the company expand its product segments, such as labels and other related products. Jindal PolyPack owns the world's largest production sites for BOPP and BOPET films.

- April 2022: Cosmo Films Ltd. planned to set up a production plant for cast polypropylene in Aurangabad. The new production line has an annual rate capacity of 25,000 million tonnes and will help the company to expand its footprints.

PVDC Coated Films Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Processed Food Industry

- 4.1.2 Usage Of PVDC Coated Films In Fresh Meat Packaging

-

4.2 Restraints

- 4.2.1 Availability of Substitutes

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 Film Substrate Type

- 5.1.1 Bi-axially Oriented Polypropylene (BOPP)

- 5.1.2 Polyethylene Terephthalate (PET)

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Other Film Substrate Types

-

5.2 Application

- 5.2.1 Food Packaging

- 5.2.2 Pharmaceutical Blister Packaging

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 ACG

- 6.4.2 Cosmo Films

- 6.4.3 Innovia Films

- 6.4.4 Jindal Poly Films Limited

- 6.4.5 Kaveri Metallising & Coating Ind. Private Limited

- 6.4.6 Perlen Packaging

- 6.4.7 POLINAS

- 6.4.8 UNITIKA LTD

- 6.4.9 Vibac Group S.p.a.

- 6.4.10 Glenroy Inc.

- 6.4.11 KUREHA CORPORATION

- 6.4.12 Asahi Kasei Corporation

- 6.4.13 Huawei Pharma Foil Packaging

- 6.4.14 Klöckner Pentaplast

- 6.4.15 Liveo Research

- 6.4.16 Polyplex

- 6.4.17 Qingdao Kingchuan Packaging

- 6.4.18 RMCL

- 6.4.19 Solvay

- 6.4.20 Tekni-Plex Inc.

- 6.4.21 Tipack Group

- 6.4.22 Transparent Paper Ltd.

- 6.4.23 Valtec Italia SRL

- 6.4.24 Bilcare Limited

- 6.4.25 Caprihans India Limited

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Research on Recycling PVDC

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

PVDC Coated Films Industry Segmentation

PVDC-coated films are obtained by coating OPP or other types of base film with a very thin layer of PVDC. It is widely used as a packaging material that provides moisture-proofing and gas-barrier properties in addition to the properties of the base film. Low dependency on the oxygen barrier property on humidity, moisture-barrier property, and excellent aroma-retaining properties further increase its market concentration for the food industry. The polyvinylidene chloride market is segmented by film substrate type, application, and geography. By film substrate type, the market is segmented into bi-axially oriented polypropylene (BOPP), polyethylene terephthalate (PET), polyvinyl chloride (PVC), and other film substrate types. By application, the market is segmented into food packaging and pharmaceutical blister packaging. The report also covers the market size and forecasts for the market in 15 countries across the globe. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Film Substrate Type | Bi-axially Oriented Polypropylene (BOPP) | ||

| Polyethylene Terephthalate (PET) | |||

| Polyvinyl Chloride (PVC) | |||

| Other Film Substrate Types | |||

| Application | Food Packaging | ||

| Pharmaceutical Blister Packaging | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

PVDC Coated Films Market Research FAQs

How big is the Polyvinylidene Chloride (PVDC) Coated Films Market?

The Polyvinylidene Chloride (PVDC) Coated Films Market size is expected to reach USD 1.59 billion in 2025 and grow at a CAGR of 3.04% to reach USD 1.84 billion by 2030.

What is the current Polyvinylidene Chloride (PVDC) Coated Films Market size?

In 2025, the Polyvinylidene Chloride (PVDC) Coated Films Market size is expected to reach USD 1.59 billion.

Who are the key players in Polyvinylidene Chloride (PVDC) Coated Films Market?

UNITIKA LTD, Perlen Packaging, KUREHA CORPORATION, Innovia Films and Vibac Group S.p.a. are the major companies operating in the Polyvinylidene Chloride (PVDC) Coated Films Market.

Which is the fastest growing region in Polyvinylidene Chloride (PVDC) Coated Films Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Polyvinylidene Chloride (PVDC) Coated Films Market?

In 2025, the Asia Pacific accounts for the largest market share in Polyvinylidene Chloride (PVDC) Coated Films Market.

What years does this Polyvinylidene Chloride (PVDC) Coated Films Market cover, and what was the market size in 2024?

In 2024, the Polyvinylidene Chloride (PVDC) Coated Films Market size was estimated at USD 1.54 billion. The report covers the Polyvinylidene Chloride (PVDC) Coated Films Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Polyvinylidene Chloride (PVDC) Coated Films Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Polyvinylidene Chloride (PVDC) Coated Films Market Research

Mordor Intelligence delivers a comprehensive analysis of the polyvinylidene chloride industry, focusing on PVDC coated films and related technologies. Our extensive research covers PVDC coating applications, including PVDC food packaging solutions and advanced barrier films. The report examines various aspects of PVDC film manufacturing. This includes PVC PVDC film combinations and specialized coated films for pharmaceutical applications. These insights provide stakeholders with crucial information on market dynamics and technological innovations.

Industry participants can access detailed analyses of PVDC barrier material developments. This includes innovations in PVDC PET applications and polyvinylidene chloride food packaging solutions. The report, available as an easy-to-download PDF, features in-depth coverage of leading PVDC film manufacturers and their technological capabilities. Our research encompasses emerging trends in PVDC coated films market segments. It offers valuable insights for strategic decision-making across the value chain, from raw materials to end-user applications.