Market Size")

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 6.00 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players Market Major Players")

*Disclaimer: Major Players sorted in no particular order |

Polyvinyl Butyral (PVB) Market Analysis

The Polyvinyl Butyral Market is expected to register a CAGR of greater than 6% during the forecast period.

The polyvinyl butyral industry is experiencing significant transformation driven by the global shift towards renewable energy sources and sustainable technologies. The solar power sector has emerged as a crucial growth catalyst, with projections indicating the installation of over 2,457 gigawatts of power capacity worldwide over the next 25 years. Major economies are implementing supportive regulatory frameworks and incentive programs to accelerate solar power adoption. This transition is creating substantial opportunities for polyvinyl butyral manufacturers, particularly in photovoltaic panel production where polyvinyl butyral serves as a critical component in glass-to-glass configuration and building-integrated PV modules.

The automotive sector is undergoing a revolutionary transformation with the accelerating adoption of electric vehicles, creating new opportunities for polyvinyl butyral applications. Industry forecasts suggest electric vehicles will constitute approximately 28% of global passenger car sales by 2030, representing a significant market expansion opportunity. This trend is supported by major investments from automotive manufacturers, exemplified by Ford and SK Innovation's recent $11.4 billion commitment to establish new EV manufacturing facilities and battery plants in Tennessee and Kentucky. These developments are driving innovations in automotive glass applications, particularly in areas of safety, acoustics, and display technologies.

Infrastructure development continues to be a major growth driver across global markets, with particular emphasis on sustainable and energy-efficient construction projects. The construction industry is witnessing increased adoption of advanced glazing solutions that incorporate polyvinyl butyral interlayers for enhanced safety, security, and energy efficiency. Technological advancements in laminated glass applications are expanding PVB market utility beyond traditional applications, with growing demand in specialized segments such as sound insulation, UV protection, and decorative architectural elements.

The industry landscape is being reshaped by strategic investments and technological innovations from major market players. Companies are focusing on developing enhanced polyvinyl butyral formulations that offer improved performance characteristics while meeting increasingly stringent environmental regulations. Solar Power Europe projects cumulative installations of solar PV capacity to reach 1,326.9 gigawatts by 2023, indicating substantial growth potential for polyvinyl butyral applications in the solar energy sector. This technological evolution is accompanied by increasing emphasis on sustainable manufacturing practices and recycling initiatives, reflecting the industry's commitment to environmental stewardship while maintaining product performance and reliability.

Polyvinyl Butyral (PVB) Market Trends

Growing Applications for Laminated Glass

Polyvinyl butyral (PVB) has become increasingly critical in laminated safety glass applications due to its exceptional binding, optical clarity, adhesion properties, toughness, and flexibility. The material's ability to hold glass fragments together upon impact while maintaining surface smoothness and clarity has made it indispensable in safety applications across various sectors. This is evidenced by Toyota's increased vehicle production and sales, reaching approximately 9.7 million units in 2022, where laminated safety glass with a PVB interlayer is extensively used in windshields and windows. The material's growing adoption in residential and commercial complexes prone to theft, burglary, and criminal activities has further accelerated its demand, particularly in applications requiring high security, such as banks, money-exchange centers, jewelry shops, museums, and art galleries.

The construction sector has emerged as a major driver for PVB-based laminated safety glass applications, supported by significant infrastructure developments across regions. In Japan alone, the Ministry of Land, Infrastructure, Transport, and Tourism reported construction sector investments reaching 66,990 billion yen (USD 508.16 billion) in 2022, representing a 0.6% increase over the previous year. The material's application extends to disaster-prone areas, particularly regions susceptible to hurricanes and tornadoes, where safety glass film provides superior protection. Additionally, the growing adoption in solar power applications, particularly in photovoltaic panels and modules, has created new avenues for PVB consumption, driven by increasing renewable energy initiatives globally.

Understand The Key Trends Shaping This Market

Download PDF

Other Drivers

The multifunctional benefits of PVB have significantly contributed to its growing adoption across various applications. Its superior sound insulation capabilities have made it particularly valuable in modern residential and commercial construction, where maintaining a quiet environment is crucial. The material's special UV filtering function provides essential protection for human skin while safeguarding valuable furniture and artworks from fading, making it increasingly popular in high-end residential and commercial applications. These properties have become especially important in urban developments, where noise pollution and UV protection are primary concerns.

The automotive sector's transformation, particularly the shift toward electric vehicles, has created additional demand for PVB. According to the China Association of Automobile Manufacturers, the country witnessed an increase in automotive production of around 2.1% in 2022, with approximately 26.86 million units sold compared to 26.27 million in 2021. The material's role in reducing noise transmission and providing enhanced safety features aligns perfectly with the premium quality requirements of electric vehicles. Furthermore, the growing photovoltaic industry has emerged as a significant driver, with PVB being increasingly used in the production of PV panels due to its excellent UV filtering and adhesion properties, contributing to the overall durability and efficiency of solar installations. The use of protective glass film in these panels enhances their longevity and performance.

Segment Analysis: Type

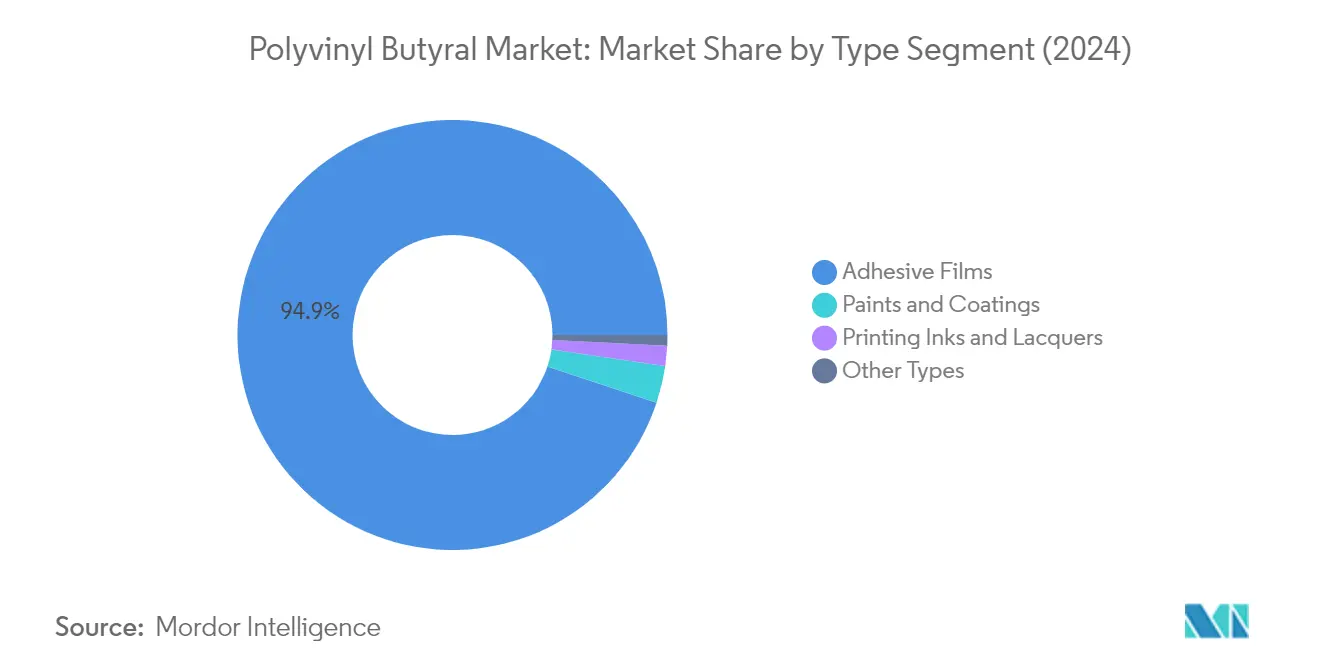

Adhesive Films Segment in Polyvinyl Butyral Market

The Adhesive Films segment continues to dominate the global polyvinyl butyral market, commanding approximately 95% of the total market share in 2024. This overwhelming market dominance is primarily attributed to its extensive use in laminated safety glass applications, particularly in the automotive and architectural laminated glass sectors. The segment's strength lies in PVB film's exceptional properties as an interlayer material, providing crucial safety features by preventing glass shatter and maintaining structural integrity upon impact. In the automotive sector, these films are essential components in windshield manufacturing, while in construction, they are widely used in safety glass applications for high-rise buildings, security installations, and sound-proof barriers. The segment is also experiencing robust growth, projected to expand at around 5.5% during 2024-2029, driven by increasing safety regulations in construction and automotive industries, along with growing demand for laminated glass in solar panels and other emerging applications.

Remaining Segments in Type Segmentation

The remaining segments in the polyvinyl butyral market include Paints and Coatings, Printing Inks and Lacquers, and Other Types such as binders for ceramics and composite fibers. The Paints and Coatings segment plays a vital role in providing corrosion protection and adhesion promotion in various industrial applications, particularly in metal primers and protective coatings. The Printing Inks and Lacquers segment serves specialized applications in the packaging and printing industries, where PVB's adhesion and binding properties are highly valued. The Other Types segment, including applications in ceramics and composite fibers, represents niche but important uses of PVB, particularly in advanced materials and specialty applications where its unique binding and adhesive properties provide specific technical advantages.

Segment Analysis: End-User Industry

Automotive & Transportation Segment in Polyvinyl Butyral Market

The Automotive & Transportation segment continues to dominate the global polyvinyl butyral market, holding approximately 55% of the market share in 2024. This significant market position is primarily driven by the mandatory use of PVB in automotive windshields and laminated safety glass applications. The segment's dominance is further strengthened by the growing adoption of electric vehicles globally, with major automotive manufacturers increasing their investments in EV production facilities. The extensive use of PVB in automotive applications is attributed to its excellent properties, including impact resistance, adhesion strength, and optical clarity, making it an indispensable component in vehicle safety systems. Additionally, the increasing focus on passenger safety and stringent automotive safety regulations across major markets has maintained the steady demand for PVB in this segment.

Power Generation Segment in Polyvinyl Butyral Market

The Power Generation segment is emerging as the fastest-growing segment in the polyvinyl butyral market, projected to grow at approximately 8% CAGR during 2024-2029. This remarkable growth is primarily driven by the increasing adoption of solar photovoltaic (PV) modules where PVB film is used as an encapsulation material. The segment's growth is further accelerated by ambitious renewable energy targets set by various countries and substantial investments in solar power infrastructure globally. The superior properties of PVB, including excellent thermal stability, UV resistance, and moisture protection, make it an ideal choice for solar panel manufacturing. Additionally, the growing focus on building-integrated photovoltaics (BIPV) and the increasing installation of solar farms across regions are creating substantial opportunities for PVB applications in this segment.

Remaining Segments in End-User Industry

The Construction segment represents another significant portion of the polyvinyl butyral market, driven by the increasing use of architectural laminated glass in commercial and residential buildings. The segment's growth is supported by ongoing urbanization trends and the growing emphasis on energy-efficient building materials. Other end-user industries, including aerospace and defense, also contribute to the market growth through specialized applications of PVB in aircraft windshields and high-security installations. These segments collectively demonstrate the versatility of PVB applications across various industries, with demand being driven by factors such as safety regulations, energy efficiency requirements, and technological advancements in building materials.

Polyvinyl Butyral (PVB) Market Geography Segment Analysis

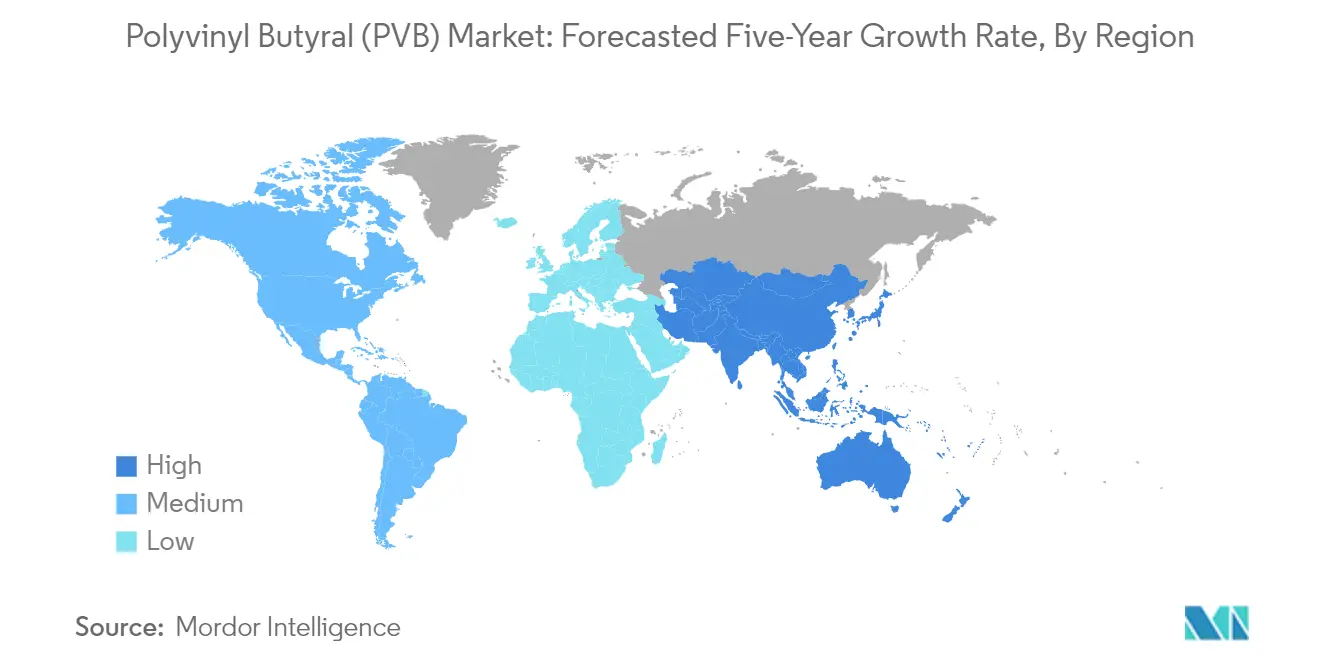

Polyvinyl Butyral Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic polyvinyl butyral market globally, driven by robust growth in the construction, automotive, and renewable energy sectors. Key markets include China, India, Japan, and South Korea, each contributing significantly to regional demand. The region's growth is supported by increasing investments in infrastructure development, rising automotive production, and the growing adoption of solar energy technologies. Manufacturing capacity expansions and technological advancements in polyvinyl butyral production have further strengthened the region's position in the global market.

Polyvinyl Butyral Market in China

China dominates the Asia-Pacific polyvinyl butyral market, holding approximately 54% share of the regional market. The country's market leadership is driven by its massive construction industry, which includes numerous high-rise buildings and infrastructure projects. China's position is further strengthened by its status as the world's largest automotive manufacturer and its ambitious renewable energy goals. The country's robust manufacturing infrastructure, coupled with government initiatives promoting sustainable development and clean energy, continues to drive demand for polyvinyl butyral in various applications.

Growth Dynamics in Chinese PVB Market

China is expected to maintain its position as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 6% during 2024-2029. This growth is primarily driven by the country's aggressive expansion in solar power installations, electric vehicle production, and sustainable construction practices. The Chinese government's commitment to renewable energy development, coupled with ongoing urbanization and infrastructure development projects, continues to create substantial opportunities for polyvinyl butyral manufacturers and suppliers in the region.

Polyvinyl Butyral Market in North America

The North American polyvinyl butyral market maintains a strong position globally, characterized by advanced manufacturing capabilities and high-end applications across the automotive, construction, and renewable energy sectors. The United States, Canada, and Mexico form the key markets in this region, with each country contributing uniquely to the regional market dynamics. The region's market is driven by stringent safety regulations in the construction and automotive sectors, coupled with increasing investments in sustainable building technologies and solar energy installations.

Polyvinyl Butyral Market in United States

The United States leads the North American polyvinyl butyral market, commanding approximately 68% of the regional market share. The country's dominant position is supported by its large automotive manufacturing base, extensive construction activities, and growing solar power installations. The US market benefits from robust research and development activities, leading to innovative polyvinyl butyral applications in various end-use industries. The presence of major polyvinyl butyral manufacturers and ongoing technological advancements further strengthens the country's market position.

Growth Trajectory in US PVB Market

The United States is projected to maintain its position as the fastest-growing market in North America, with an expected growth rate of approximately 6% during 2024-2029. This growth is driven by increasing adoption of electric vehicles, expanding solar power installations, and ongoing infrastructure development projects. The country's focus on sustainable building practices and energy-efficient solutions continues to create new opportunities for polyvinyl butyral applications across various sectors.

Polyvinyl Butyral Market in Europe

The European polyvinyl butyral market is characterized by its strong focus on technological innovation and sustainable solutions across various applications. Key markets include Germany, the United Kingdom, France, and Italy, each contributing significantly to the regional market dynamics. The region's market is driven by strict safety regulations, particularly in the automotive and construction sectors, along with a growing emphasis on renewable energy solutions.

Polyvinyl Butyral Market in Germany

Germany stands as the largest polyvinyl butyral market in Europe, driven by its robust automotive manufacturing sector and advanced construction industry. The country's leadership position is supported by its strong focus on technological innovation and sustainable development practices. Germany's market is characterized by high-quality standards and advanced applications in automotive safety glass, architectural glazing, and solar panel manufacturing.

Growth Dynamics in German PVB Market

Germany maintains its position as the fastest-growing market in Europe, driven by increasing adoption of electric vehicles and expanding solar power installations. The country's commitment to renewable energy development and sustainable construction practices continues to create new opportunities for polyvinyl butyral applications. German manufacturers' focus on research and development, coupled with stringent quality standards, ensures sustained market growth.

Polyvinyl Butyral Market in South America

The South American polyvinyl butyral market demonstrates steady growth potential, with Brazil and Argentina serving as the key markets in the region. Brazil emerges as both the largest and fastest-growing market in the region, driven by its expanding automotive sector and increasing investments in construction and renewable energy projects. The region's market development is supported by growing industrialization, urbanization trends, and increasing adoption of safety standards in construction and automotive applications.

Polyvinyl Butyral Market in Middle East & Africa

The Middle East & Africa polyvinyl butyral market shows promising growth potential, with Saudi Arabia and South Africa serving as key markets. Saudi Arabia emerges as the largest market in the region, supported by extensive construction activities and infrastructure development projects. South Africa demonstrates strong growth potential, driven by increasing investments in renewable energy and automotive sectors. The region's market expansion is further supported by growing urbanization, infrastructure development, and increasing adoption of safety standards across various industries.

Get Analysis on Important Geographic Markets

Download PDF

Polyvinyl Butyral (PVB) Industry Overview

Top Companies in Polyvinyl Butyral (PVB) Market

The global polyvinyl butyral market is characterized by continuous product innovation, particularly in interlayer technologies for automotive and architectural applications. Leading companies are focusing on developing advanced PVB interlayer formulations with enhanced properties for safety, security, and solar control applications. Strategic expansion of production facilities, particularly in high-growth regions like Asia-Pacific, demonstrates the industry's commitment to meeting increasing demand. Companies are investing heavily in research and development to create specialized polyvinyl butyral products for emerging applications such as solar panels and electric vehicles. Operational agility is evident through backward integration strategies, with several major players maintaining in-house production of raw materials like polyvinyl alcohol and butyraldehyde to ensure supply chain stability and cost advantages.

Consolidated Market with Strong Regional Players

The polyvinyl butyral market exhibits a highly consolidated structure, with the top five global players commanding a significant share of the market. These major players are predominantly large chemical conglomerates with diverse product portfolios, allowing them to leverage extensive distribution networks and technical expertise. Regional players, particularly in Asia, have established strong footholds in their respective markets through specialized product offerings and local manufacturing capabilities. The market's high entry barriers, including substantial capital requirements and technical expertise, have contributed to maintaining this consolidated structure.

The industry has witnessed strategic mergers and acquisitions aimed at expanding geographical presence and strengthening product portfolios. Companies are increasingly focusing on vertical integration strategies to secure raw material supply and optimize production costs. Joint ventures and collaborations, particularly in emerging markets, have become common approaches for market expansion and technology sharing. The competitive landscape is further shaped by long-term supply agreements with key end-users in the automotive and construction sectors, creating stable business relationships and market positions.

Innovation and Integration Drive Market Success

Success in the polyvinyl butyral industry increasingly depends on developing innovative products that address emerging needs in sustainable construction and automotive safety. Incumbent companies must focus on expanding their technical capabilities and investing in new application development, particularly in renewable energy and electric vehicle segments. Building strong relationships with end-users through customized solutions and technical support services has become crucial for maintaining market position. Companies need to optimize their production processes and supply chains to remain competitive while meeting increasingly stringent quality and environmental standards.

For contenders looking to gain market share, specialization in niche applications and regional market focus offer viable entry strategies. The development of cost-effective manufacturing processes and alternative raw material sources could help overcome entry barriers. Companies must also consider the increasing importance of sustainability and circular economy principles in their business strategies. The risk of substitution from alternative interlayer materials necessitates continuous product improvement and differentiation. Future success will largely depend on the ability to adapt to evolving regulatory requirements, particularly regarding environmental protection and safety standards in key end-use industries.

Polyvinyl Butyral (PVB) Market Leaders

-

Chang Chun Group

-

Eastman Chemical Company

-

Sekisui Chemical Co., Ltd.

-

Kingboard Fogang Specialty Resin Co., Ltd

-

KURARAY CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

_Market-_Market_Concentration.webp)

Need More Details on Market Players and Competiters?

Download PDF

Polyvinyl Butyral (PVB) Market News

- May 2022: Eastman Chemical Company, in partnership with SEEN AG, introduced a new polyvinyl butyral (PVB) interlayer for laminated glass, Saflex FlySafe 3D, a highly effective solution to avoid bird collisions without compromising on the view or beauty of glass facades.

- March 2021: Eastman Chemical Company announced that it is investing in upgrading and expanding its extrusion capabilities to produce interlayer product lines at its Springfield, Massachusetts, manufacturing facility. The investment will strengthen Eastman's supply capability to respond to regional and global demand for Saflex polyvinyl butyral (PVB) products in the automotive and architectural markets.

Polyvinyl Butyral (PVB) Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Construction and Infrastructure Activities Across the World

- 4.1.2 Growing Applications for Laminated Glass

-

4.2 Restraints

- 4.2.1 Availability of Product Substitutes in the Market

- 4.2.2 High Recycling Activities of Polyvinyl Butyral in Developed Economies

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 Type

- 5.1.1 Adhesive Films

- 5.1.2 Paints and Coatings (including Wash Primers)

- 5.1.3 Printing Inks and Lacquers

- 5.1.4 Other Types (Binders for Ceramics and Composite Fibers)

-

5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Construction

- 5.2.3 Power Generation

- 5.2.4 Other End-user Industries (Aerospace, Defense)

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Chang Chun Group

- 6.4.2 Everlam

- 6.4.3 Genau Manufacturing Company LLP

- 6.4.4 Huakai plastic(Chongqing) Co., Ltd.

- 6.4.5 Kingboard FoGang Specialty Resins Co. Ltd

- 6.4.6 KURARAY CO. LTD

- 6.4.7 Eastman Chemical Company

- 6.4.8 Sekisui Chemical Co. Ltd.

- 6.4.9 WMC GLASS

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand from the Photovoltaic Industry

- 7.2 Increasing Adoption of EVs

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Polyvinyl Butyral (PVB) Industry Segmentation

Polyvinyl butyral (PVB) is a clear, colorless, amorphous thermoplastic material that can be produced by reacting polyvinyl alcohol and butyraldehyde. It is mainly used in fabricating various laminated glass products for the automotive, construction, and photovoltaic end-user sectors, owing to its optical clarity and strong adhesive nature. The polyvinyl butyral (PVB) market is segmented by type, end-user industry, and geography. By type, the market is segmented into adhesive films, paints and coatings, printing inks and lacquers, and other types (binders for ceramics and composite fibers). By end-user industry, the market is segmented into automotive, construction, power generation, and other end-user industries (aerospace, defense). The report also covers the market size and forecasts for the polyvinyl butyral (PVB) market in 15 countries across the major regions. For each segment, the market sizing and forecast have been done on the basis of revenue (USD million).

| Type | Adhesive Films | ||

| Paints and Coatings (including Wash Primers) | |||

| Printing Inks and Lacquers | |||

| Other Types (Binders for Ceramics and Composite Fibers) | |||

| End-user Industry | Automotive | ||

| Construction | |||

| Power Generation | |||

| Other End-user Industries (Aerospace, Defense) | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Polyvinyl Butyral (PVB) Market Research FAQs

What is the current Polyvinyl Butyral (PVB) Market size?

The Polyvinyl Butyral (PVB) Market is projected to register a CAGR of greater than 6% during the forecast period (2025-2030)

Who are the key players in Polyvinyl Butyral (PVB) Market?

Chang Chun Group, Eastman Chemical Company, Sekisui Chemical Co., Ltd., Kingboard Fogang Specialty Resin Co., Ltd and KURARAY CO., LTD. are the major companies operating in the Polyvinyl Butyral (PVB) Market.

Which is the fastest growing region in Polyvinyl Butyral (PVB) Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Polyvinyl Butyral (PVB) Market?

In 2025, the Asia-Pacific accounts for the largest market share in Polyvinyl Butyral (PVB) Market.

What years does this Polyvinyl Butyral (PVB) Market cover?

The report covers the Polyvinyl Butyral (PVB) Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Polyvinyl Butyral (PVB) Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Polyvinyl Butyral (PVB) Market Research

Mordor Intelligence delivers a comprehensive analysis of the polyvinyl butyral industry. We leverage our extensive experience in chemical sector research. Our latest report examines the complete value chain of PVB applications. This includes everything from raw materials to end-use applications such as laminated safety glass, safety glass film, and security glass film manufacturing. The analysis covers various product forms, including PVB film, PVB sheet, and specialized PVB interlayer materials. These are used in architectural laminated glass and protective glass film applications.

Our detailed polyvinyl butyral market report, available as an easy-to-download PDF, provides stakeholders with crucial insights into emerging applications. These include photovoltaic encapsulant and solar panel encapsulant technologies. The research encompasses a comprehensive analysis of butyrals and their derivatives, with a special focus on innovative applications like acoustic glass interlayer systems. The report examines the expanding polyvinyl butyral industry landscape and provides accurate polyvinyl butyral market size projections. This enables businesses to make informed decisions in the evolving PVB film market.