Polyolefin (PO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

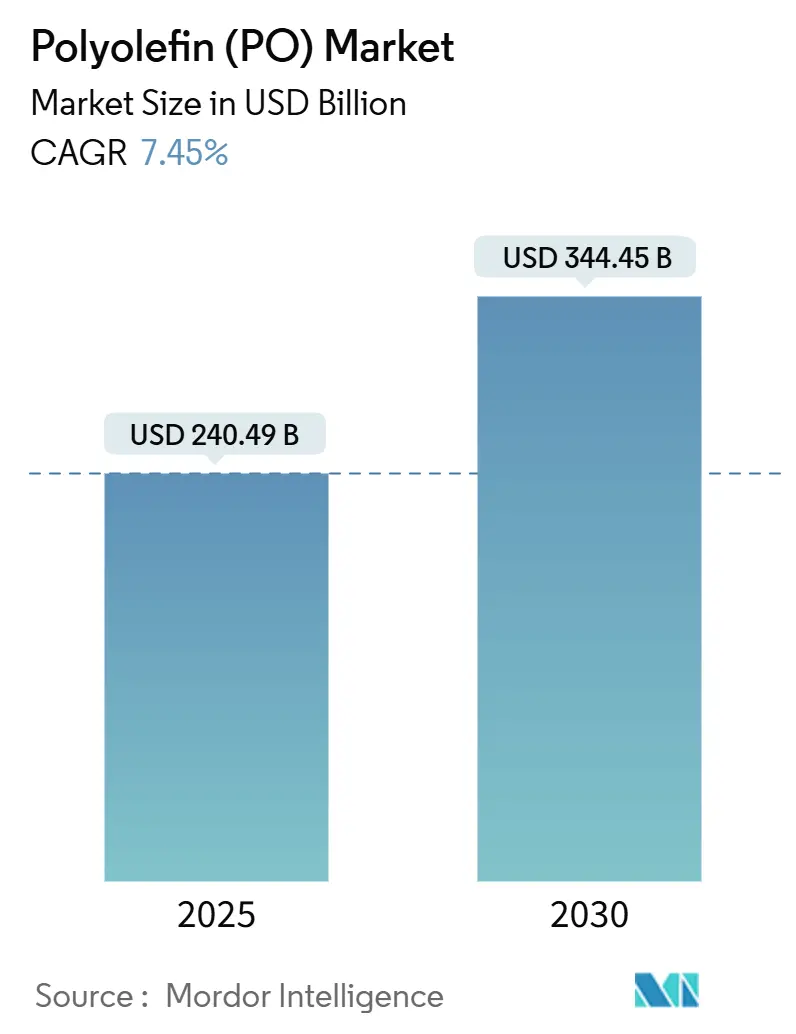

| Market Size (2025) | USD 240.49 Billion |

| Market Size (2030) | USD 344.45 Billion |

| Growth Rate (2025 - 2030) | 7.45% CAGR |

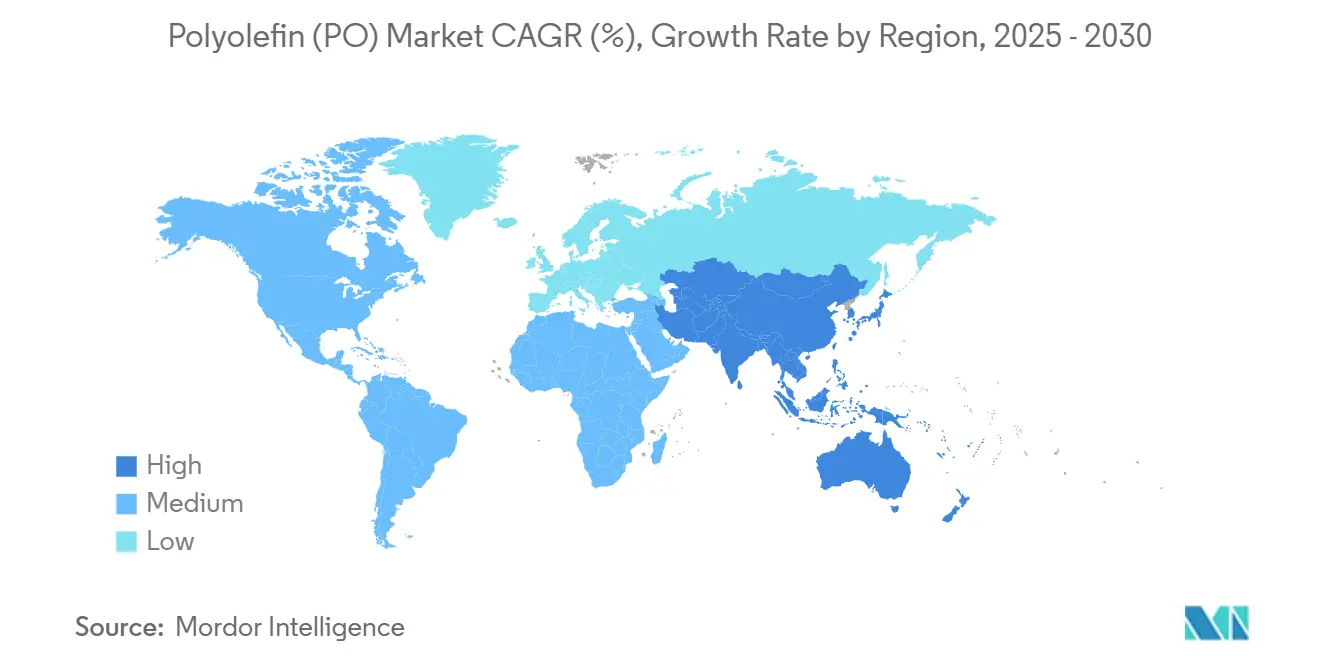

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Polyolefin (PO) Market Analysis by Mordor Intelligence

The Polyolefin Market size is estimated at USD 240.49 billion in 2025, and is expected to reach USD 344.45 billion by 2030, at a CAGR of 7.45% during the forecast period (2025-2030). Strong offtake from packaging, expanding automotive lightweighting programs, and specialty‐grade innovation underpin the trajectory despite margin pressure and regulatory disruption. Asia-Pacific anchors demand, commanding more than half of global consumption in 2024 and maintaining the quickest regional advance through 2030. Within materials, polyethylene keeps a numerical lead, yet polypropylene’s faster growth signals a portfolio pivot toward higher-performance compounds specified by car makers and appliance OEMs. Commercializing metallocene catalysts, rising chemical-recycling capacity, and escalating circular-economy mandates further shape competitive priorities across the polyolefin market.

Key Report Takeaways

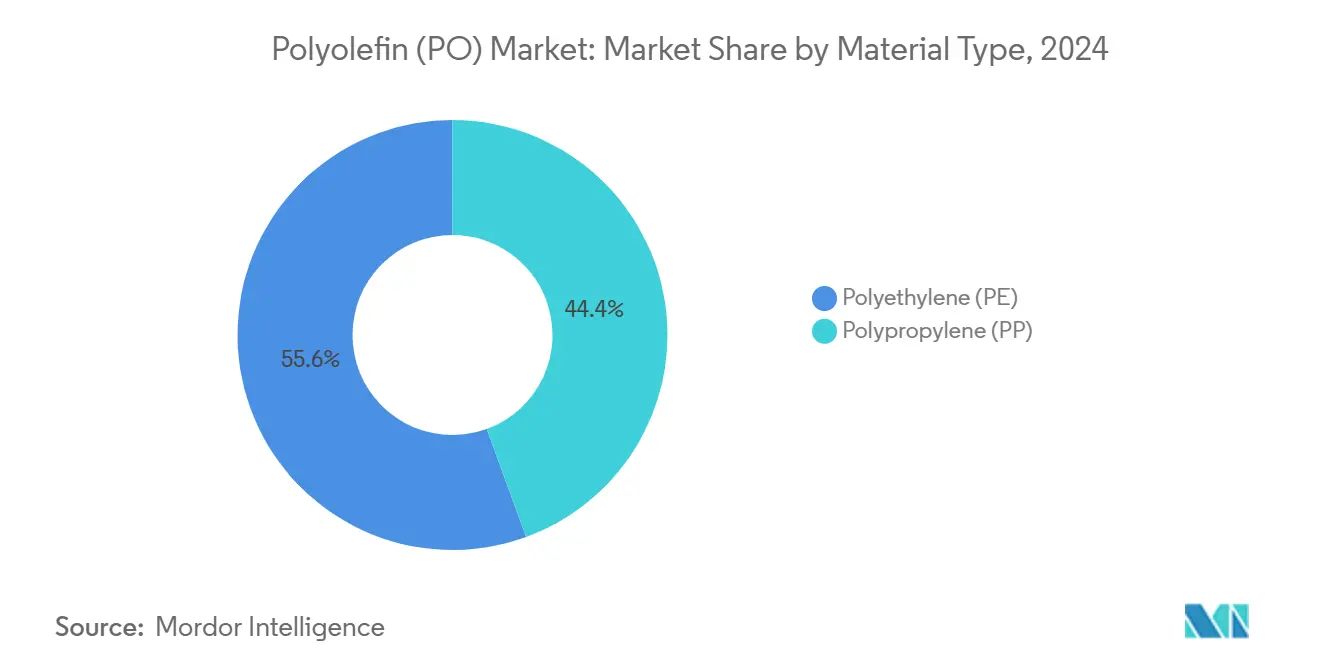

- By material type, polyethylene led with 55.57% Polyolefin market share in 2024, whereas polypropylene is projected to book the fastest 8.37% CAGR through 2030.

- By application, films and sheets held 36.29% of the Polyolefin market size in 2024, while fibers and raffia are forecast to expand at an 8.19% CAGR during 2025-2030.

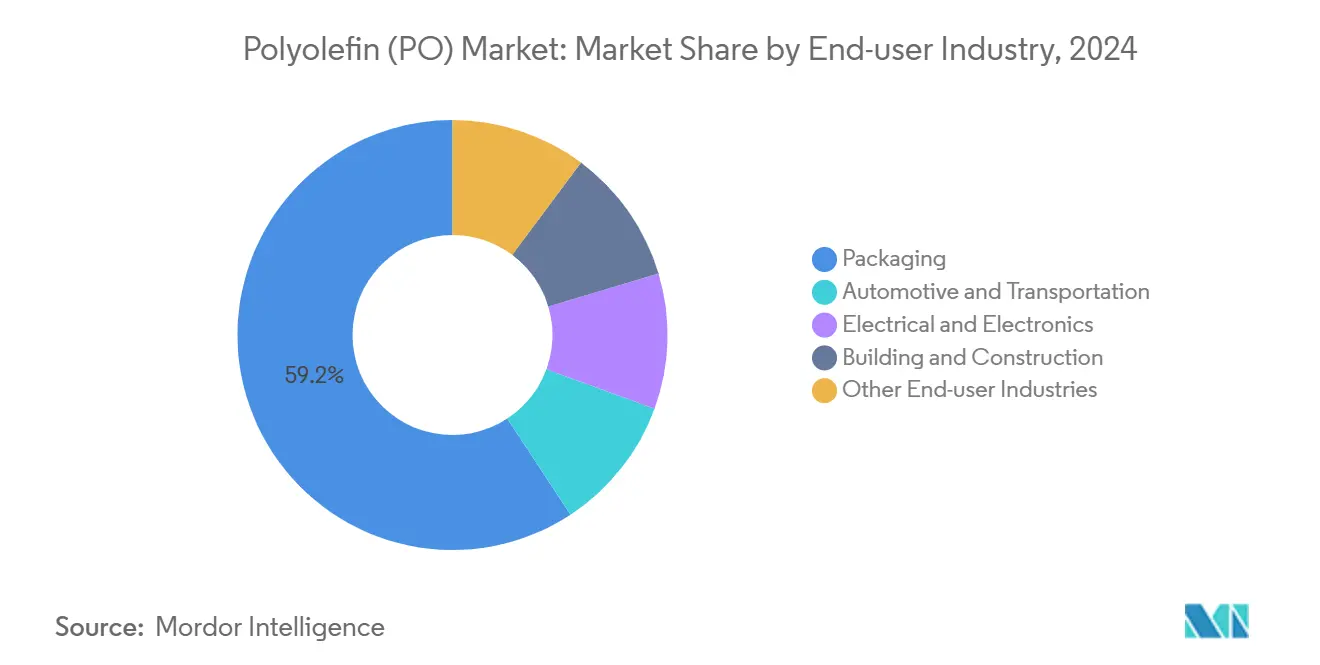

- By end user, packaging captured 59.24% of the Polyolefin market in 2024 and is tracking an 8.26% CAGR to 2030.

- By geography, Asia-Pacific accounted for 51.75 % of the Polyolefin market share in 2024 and posts the quickest 8.60% CAGR through 2030.

Global Polyolefin (PO) Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from Rigid to Flexible Packaging | +1.8% | Global with APAC & North America leadership | Medium term (2-4 years) |

| Demand for Cost-efficient Interior and Consumer Goods | +1.2% | APAC core, spill-over Latin America & MEA | Short term (≤ 2 years) |

| Circular-economy Mandates Driving Chemical-recycling Grades | +1.5% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Surging EV Lightweighting Needs for PP/POE Compounds | +1.9% | China, United States, Germany hubs | Medium term (2-4 years) |

| Metallocene-catalyst Boom Enabling Specialty PE/PP Grades | +1.1% | United States, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift from Rigid to Flexible Packaging

Brand owners migrate to lighter, flexible solutions that meet barrier targets while cutting logistics costs, a shift translating into larger film resin requirements across the polyolefin market. Flexible formats use up to 70% less material than legacy rigid containers, trimming freight emissions and warehouse space. Supply-chain disruptions in 2024 showed that mono-polyethylene pouches travel more efficiently than glass or metal options, ensuring on-shelf availability even during port congestion. Film converters now layer nano-barrier coatings on linear-low-density grades, matching shelf life once available only from multilayer laminates. EU-level design-for-recycling criteria due by 2028 favor these mono-material structures and will accelerate the replacement cycle[1]European Commission, “Packaging and Packaging Waste Regulation: Final Legislative Text,” Europa.eu.

Demand for Cost-efficient Interior and Consumer Goods

Middle-income households in India, Indonesia, and Vietnam increasingly opt for polypropylene furniture and appliance casings that deliver acceptable durability at one-third the cost of engineering plastics. OEMs reduce molding cycle time thanks to the polymer’s broad processing window, cutting electricity consumption in factories strained by high power tariffs. Automotive suppliers are also swapping glass-fiber reinforced ABS parts with impact-modified polyolefin blends for door panels, shaving vehicle mass without expensive carbon composites. The development pipeline further includes talc-filled random-copolymer grades that withstand UV exposure, making them suitable for outdoor consumer goods.

Circular-economy Mandates Driving Chemical-recycling Grades

Europe’s Packaging and Packaging Waste Regulation requires 30% post-consumer recycled content in plastic formats by 2030, compelling brands to secure chemically recycled feedstock to pass food-contact protocols. LyondellBasell’s MoReTec facility entering construction in Germany aims for virgin-equivalent output, positioning the company to monetize premium recycled PE and PP that command 20-30% higher prices. US supermarkets have trialed chemically recycled polyethylene trays for ready meals, proving scalability beyond niche pilot projects. Resin producers expect recycled-content premiums to offset higher depreciation tied to pyrolysis units and solvent cleaning trains.

Surging EV Lightweighting Needs for PP/POE Compounds

Battery enclosures, under-hood ducts, and front-end modules now specify mineral-filled polypropylene compounds that cut weight 25% relative to aluminum. Chinese new-energy vehicle makers adopted polypropylene-based rocker panels in 2024 to meet road-spray abrasion standards while simplifying recycling at end-of-life. European OEMs (original equipment manufacturers) collaborated with compounders on polyolefin elastomer blends that remain dimensionally stable from −40 °C to 90 °C, important for pack cooling plates. As unit battery costs drop, manufacturers refocus on trimming body mass, placing the polyolefin market in pole position for volume growth.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Single-use-plastic and Carbon-tax Regulations | −0.9% | Europe, selective U.S. states | Short term (≤ 2 years) |

| Global Oversupply and Margin Pressure from Mega-crackers | −1.3% | Worldwide, acute in Europe & North America | Medium term (2-4 years) |

| Volatility in Naphtha/propane Feedstock Prices | −0.8% | Asia naphtha, North America propane pools | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Single-use-plastic and Carbon-tax Regulations

The EU bans lightweight produce bags under 1.5 kg beginning in 2030, eliminating a 0.8 million-tonne demand stream for polyethylene film. Simultaneously, carbon levies lift cash costs at European crackers by USD 75 per tonne ethylene equivalent, compressing netbacks relative to exporters from tax-lighter regions. Producers pivot to closed-loop packaging with 35% recycled content to retain retail shelves, yet volumes lost in banned skews take time to replace. Some film converters relocate slit-roll finishing to Turkey and Egypt to avoid levy exposure, altering trade flows within the Polyolefin market.

Global Oversupply and Margin Pressure from Mega-crackers

Capacity additions in the United Arab Emirates, Qatar, and China raised the global ethylene nameplate 14 million tonnes between 2023 and 2025, outpacing polymer demand. Utilization at Europe’s smallest furnaces dipped below 65%, prompting LyondellBasell to review six assets across five countries. Feedstock-rich producers leverage discount ethane and propane to push exports, forcing high-cost naphtha players to rationalize or convert to specialty output. Analysts project that at least 10 million tonnes of further capacity must exit to restore a balanced polyolefin market by 2027.

Segment Analysis

By Material Type: Polyethylene Dominance Faces Polypropylene Upswing

Polyethylene accounted for 55.57 of % Polyolefin market share in 2024, thanks to its entrenched role in packaging, construction, and agriculture. Yet polypropylene is forecast to post an 8.37% CAGR, meaning its slice of the polyolefin market size will expand meaningfully by 2030. Linear-low-density variants prosper as converters of down-gauge film, while high-density grades serve detergent bottles and corrosion-resistant pipes demanded by the water infrastructure boom across India. Low-density polyethylene faces design-for-recycling pressure, but maintains a foothold in extrusion-coating for liquid cartons.

Metallocene innovations enable ultra-thin cast films and high-stiffness polypropylene random copolymers that approach polycarbonate clarity. These grades unlock stretching and thermoforming latitude, helping brand owners migrate from polystyrene and PVC. Automakers specify long-glass polypropylene for front-end carriers, broadening revenue for compounders beyond traditional bumper fascia as chemical-recycling feedstock supply scales, polyethylene and polypropylene producers aim to certify grades with 50% circular content, reinforcing customer loyalty and protecting share in the polyolefin market.

By Application: Films Rule Volume, Fibers Accelerate Gains

Films and sheets comprised 36.29% of 2024 sales, cementing the application’s pole position within the polyolefin market. High-clarity snack pouches, bread bags, and collation shrink dominate consumption in mature regions, while agricultural mulch and greenhouse films propel volume in India and Mexico. Blow-molded HDPE (High-Density Polyethylene) jerry-cans serve industrial lubricants, and extrusion-coated paper cups rely on LDPE (Low-Density Polyethylene) moisture barriers.

Fibers and raffia log the fastest 8.19% CAGR through 2030, stimulated by woven polypropylene sacks for grain logistics and FIBC (Flexible Intermediate Bulk Container) bulk bags leveraged in e-commerce warehousing. Non-woven polypropylene shows rising penetration in hygiene applications as demographics boost adult incontinence product uptake. Injection-molded bins, crates, and thin-wall containers tap impact-copolymer polypropylene that marries toughness with flow, keeping cycle times low even on legacy presses. The end-use diversification insulates the polyolefin market from cyclical shocks, strengthening its aggregate resilience.

By End-user Industry: Packaging Leads Both Scale and Growth

Packaging captured 59.24% revenue in 2024 and will continue to dominate, not merely for food pouches but across healthcare blister packs and closure liners. Circular-economy policies amplify that dominance because mono-material solutions featuring polyethylene or polypropylene are easier to recycle than foil-laminate or Polyethylene Terephthalate (PET)-laminated bottles. The EU’s 2030 target for 30% recycled content in polyolefin formats reinforces high-volume takeaway in the polyolefin market.

Automotive retains a mid-single-digit share yet posts outsized growth from EV platform launches that embrace lightweight polypropylene compounds. Electrical and electronics buyers adopt halogen-free flame-retardant polypropylene for appliance housings, while construction contractors specify HDPE conduit and geomembranes for potable-water projects. Collectively, these segments diversify revenue and buffer the industry from packaging-centric regulation shocks.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific commanded 51.75% polyolefin market share in 2024 and is tracking an 8.60% CAGR through 2030. China’s modernization of logistics packaging, India’s infrastructure push, and ASEAN’s consumer boom all funnel incremental demand[2]Indian Ministry of Chemicals & Fertilizers, “Petrochemicals Targets 2025,” Chemicals.gov.in . Integrated refining-to-chemicals sites grant low conversion cost, but sustainability measures—such as China’s 2026 cap on virgin-plastic consumption—will influence future capacity choices.

North America is the second-largest slice because of abundant shale-based ethane that yields cost-advantaged polyethylene. Regional demand rose 7% for polyethylene and 4% for polypropylene in 2024 due to e-commerce fulfillment and recovering durable goods orders. Resin exports from the Gulf Coast cushion producers during domestic slowdowns, though Panama Canal congestion reroutes cargo via U.S. East Coast ports, stretching transit times.

Europe wrestles with energy costs triple those in the U.S. following gas market upheaval. Nonetheless, early adoption of chemical-recycling technology positions the bloc at the forefront of circular polymer commerce. Producers pivot toward higher-margin specialty grades and service contracts with brand owners seeking traceable recycled content. The Middle East leverages a 15% rise in gas output since 2020 to supply competitively priced resin into Asia and Africa, while South America’s import reliance keeps local prices high, incentivizing Brazilian investments in new steam crackers.

Competitive Landscape

The Polyolefin Market is fragmented. Petrochemical majors with integrated feedstock chains—ExxonMobil, SABIC, and Sinopec—defend margins better than standalone polymerizers vulnerable to naphtha swings. Technology capabilities increasingly separate leaders from laggards. Companies with metallocene licenses, advanced recycling platforms, and application-development centers for EV and medical packaging win specification slots that deliver price premiums. Producers willing to co-invest in sorting lines or operate take-back schemes secure off-take commitments in exchange for locked pricing formulas. Consequently, relationship-driven business models complement scale advantages, creating a multifaceted rivalry matrix within the polyolefin market.

Polyolefin (PO) Industry Leaders

-

SABIC

-

China Petrochemical Corporation

-

LyondellBasell Industries Holdings B.V.

-

Dow

-

ExxonMobil Corportation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Mitsui Chemicals, Inc., Idemitsu Kosan Co., Ltd., and Sumitomo Chemical Co., Ltd. signed a Memorandum of Understanding. This agreement focuses on merging the polyolefin (PO) operations of Prime Polymer Co., Ltd., a joint venture between Mitsui and Idemitsu, with Sumitomo Chemical's polypropylene (PP) and linear low-density polyethylene (LLDPE) businesses in Japan.

- June 2025: LyondellBasell Industries Holdings B.V., a global licensor of polyolefin technologies, signed a deal with SHCCIG Yulin Chemical Co., Ltd. The agreement grants SHCCIG four pivotal technologies for its expansive new petrochemical complex in Yulin City, China. The all-encompassing technology suite features technologies for two polypropylene plants and a high-density polyethylene plant.

Global Polyolefin (PO) Market Report Scope

Polyolefins are macromolecules produced by the polymerization of olefin monomer units. The most common polyolefins used in the market are polyethylene (PE) and polypropylene (PP). Polyolefins possess excellent processability, chemical stability, and long-term durability. It is the most frequently used thermoplastic polymer, with uses ranging from packaging to consumer products to fibers and textiles.

The polyolefin market is segmented by material type, application, and geography. By material type, the market is segmented into polyethylene (PE) and polypropylene (PP). Polyethylene is further categorized into high-density polyethylene (HDPE), low-density polyethylene (LDPE), and linear low-density polyethylene (LLDPE). By application, the market is segmented into films and sheets, injection molding, blow molding, extrusion coating, and fibers and raffia. The report also covers the market sizes and forecasts for the polyolefin market in 15 countries across major regions. For each segment, the market sizes and forecasts are provided in terms of value (USD).

| Polyethylene (PE) | High-Density PE (HDPE) |

| Low-Density PE (LDPE) | |

| Linear Low-Density PE (LLDPE) | |

| Polypropylene (PP) |

| Films and Sheets |

| Injection Molding |

| Blow Molding |

| Extrusion Coating |

| Fibers and Raffia |

| Packaging |

| Automotive and Transportation |

| Electrical and Electronics |

| Building and Construction |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Polyethylene (PE) | High-Density PE (HDPE) |

| Low-Density PE (LDPE) | ||

| Linear Low-Density PE (LLDPE) | ||

| Polypropylene (PP) | ||

| By Application | Films and Sheets | |

| Injection Molding | ||

| Blow Molding | ||

| Extrusion Coating | ||

| Fibers and Raffia | ||

| End-user Industry | Packaging | |

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Building and Construction | ||

| Other End-user Industries | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the Polyolefin market and how fast is it expanding?

Global revenue reached USD 240.49 billion in 2025 and is projected to climb to USD 344.45 billion by 2030, reflecting a 7.45% CAGR.

Which region contributes the largest share of polyolefin demand today?

Asia-Pacific commands 51.75% of global consumption, led by China’s packaging and infrastructure requirements.

Why is packaging expected to remain the top-consuming end use for polyolefins?

Packaging already accounts for 59.24% of 2024 sales and continues to grow because flexible mono-material formats align with circular-economy mandates and deliver logistics savings.

Which application segment is recording the quickest volume growth?

Fibers and raffia show the fastest advance at an 8.19% CAGR through 2030, supported by woven sacks, non-woven hygiene products, and bulk-bag logistics.

How are electric vehicles influencing polyolefin demand?

Automakers specify advanced polypropylene and polyolefin elastomer compounds for battery enclosures and body panels, achieving weight cuts of up to 25% versus metal alternatives.

Page last updated on: