| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 4.76 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Polymer Processing Aid Market Analysis

The Polymer Processing Aid Market is expected to register a CAGR of 4.76% during the forecast period.

The polymer processing aid market is experiencing significant transformation driven by rapid technological advancements and evolving end-user requirements across various sectors. The integration of advanced manufacturing technologies and automation in polymer processing has led to improved production efficiency and product quality. The industry is witnessing a shift towards sustainable and eco-friendly polymer processing aids, with manufacturers focusing on developing products that comply with stringent environmental regulations. This transformation is particularly evident in regions with strict environmental policies, where companies are investing in research and development to create more sustainable solutions.

The telecommunications sector is emerging as a crucial growth catalyst for the polymer processing aid market, particularly in the context of global digital infrastructure expansion. China has demonstrated remarkable progress in this regard, having established 792,000 5G base stations and announcing plans to construct more than 1 million additional stations. The European Union has taken a forward-looking approach by launching its first set of 6G projects worth EUR 60 million, signaling a long-term commitment to telecommunications infrastructure development. These developments are creating substantial demand for polymer processing aids in cable and wire manufacturing applications.

The automotive industry's transition towards electric vehicles is reshaping the demand patterns for polymer processing aids. The global electric vehicle market has shown remarkable growth, with sales share increasing from 2.5% to 4.2%, representing approximately 3.32 million units. This shift is driving innovation in polymer processing aids used in electric vehicle components, particularly in wire insulation, battery components, and lightweight structural elements. Manufacturers are developing specialized processing aids that meet the unique requirements of electric vehicle production, including enhanced thermal stability and electrical insulation properties.

The packaging industry continues to evolve with changing consumer preferences and regulatory requirements, creating new opportunities for polymer processing aid applications. India's packaging market, for instance, is projected to reach USD 204.81 billion by 2025, reflecting the robust growth potential in emerging markets. The industry is witnessing increased demand for advanced polymer processing aids that can enhance the production efficiency of various packaging materials while maintaining compliance with food contact regulations. Manufacturers are focusing on developing processing aids that can improve the surface quality and processing efficiency of packaging materials while reducing overall production costs.

Polymer Processing Aid Market Trends

Increasing Demand for Polypropylene from the Packaging Industry

The packaging industry represents one of the largest consumers of polypropylene, driving significant demand for polymer processing aids. According to the International Mining and Resources Conference (IMARC), the global food packaging market value reached USD 363 billion in 2022 and is projected to expand to USD 512 billion by 2028, indicating substantial growth opportunities for polypropylene applications. The material's versatility in both flexible and rigid packaging applications, combined with its excellent mechanical properties and moldability, has made it increasingly essential for food packaging, consumer goods packaging, and industrial applications. This is further evidenced by the Plastics Industry Association's projection that the packaging segment of the global plastic film market will reach 30,280.8 kilotons by 2023.

The industry is witnessing significant capacity expansions and technological advancements in polypropylene production to meet the rising packaging demand. Companies across regions are focusing on increasing their production capacities, with approximately 6 million metric tons of new polypropylene production capacities being added across Asia and the Middle East. The cast film technique, which primarily serves food and industrial packaging applications, has become increasingly prominent, with the global plastic cast film technology market estimated at USD 14,486.6 million in 2023. This growth is driven by the increasing demand for packaged food and pharmaceutical products in growing economies, along with the rise in customized packaging solutions for microwave food, snack foods, and frozen foods. The use of plastic processing aids in these applications enhances the efficiency and quality of production, further supporting the industry's expansion.

Understand The Key Trends Shaping This Market

Download PDF

Usage of PVC and HDPE in the Building and Infrastructure Sector

The construction and infrastructure sector continues to be a major driver for polymer processing, particularly in PVC and HDPE applications for pipes, profiles, and construction materials. China's construction sector exemplifies this trend, with the country implementing significant infrastructure investments, including an annual limit for new infrastructure bonds worth CNY 3.85 trillion (approximately USD 572.49 billion) in 2022, representing an increase from CNY 3.65 trillion in the previous year. The extensive use of PVC and HDPE in construction applications such as pipes, window frames, flooring, roofing foils, wall coverings, and cables has created sustained demand for polymer processing aids to enhance processing efficiency and product quality.

The growing urbanization and infrastructure development across regions have further intensified the demand for PVC and HDPE products in the construction sector. These materials are preferred for their durability, cost-effectiveness, low maintenance requirements, safety features, enhanced aesthetics, and high strength-to-weight ratio. The application of plastic processing aids in these materials has become crucial for improving surface characteristics, eliminating melt fractures, and reducing die deposits during the manufacturing process. This is particularly important in the production of pipes and tubing systems, where surface quality and dimensional stability are critical factors. The construction industry's focus on sustainable and long-lasting materials has also contributed to the increased adoption of processed PVC and HDPE products, further driving the demand for process aid additives in this sector.

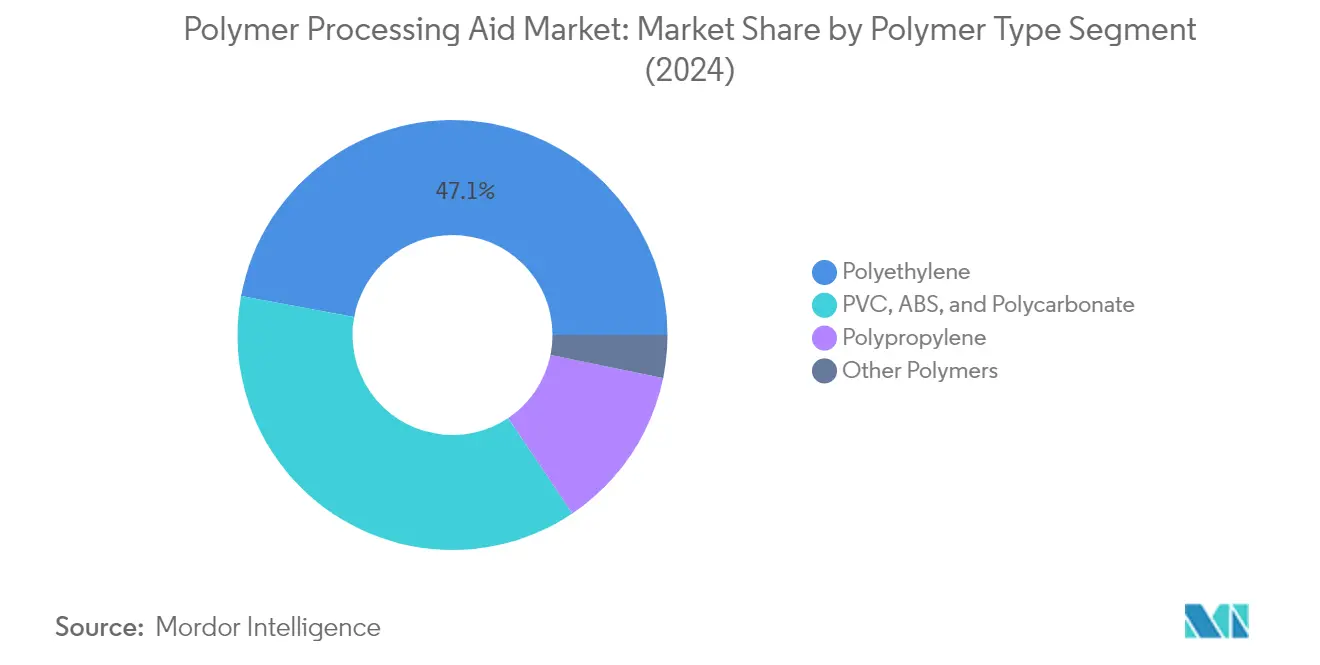

Segment Analysis: Polymer Type

Polyethylene Segment in Polymer Processing Aid Market

The polyethylene segment dominates the global polymer processing aid market, commanding approximately 47% of the total market revenue in 2024. This significant market share is driven by the extensive use of polyethylene in various applications, including blown film, cast film, wire and cable, extrusion blow molding, fibers and raffia, and pipe and tube manufacturing. The segment encompasses different grades like LLDPE, LDPE, and HDPE, each serving specific industrial needs. The segment is also experiencing the fastest growth rate in the market, projected to expand at around 4% CAGR from 2024 to 2029, primarily due to increasing demand from the packaging industry and the growing adoption of processing aid for polyethylene in construction applications. The segment's growth is further supported by technological advancements in processing techniques and the rising demand for high-quality plastic products across various end-user industries.

Remaining Segments in Polymer Type

The polymer processing aid market also includes significant segments such as PVC, ABS, and polycarbonate, which collectively form a substantial portion of the market, particularly in volume terms. These materials are extensively used in construction, automotive, and consumer goods applications. The polypropylene segment represents another important category, finding widespread use in packaging and automotive applications due to its excellent mechanical properties and processability. The other polymers segment, which includes materials like PEX, PET, PBT, and PA, serves specialized applications in various industries. Each of these segments contributes uniquely to the market's dynamics, with their demand being driven by specific end-user requirements and technological advancements in polymers for processing aids.

Segment Analysis: Application

Blown Film and Cast Film Segment in Polymer Processing Aid Market

The blown film and cast film segment dominates the global polymer processing aid market, commanding approximately 54% of the total market share in 2024. This significant market position is primarily driven by the extensive use of polymer processing additives in manufacturing various types of films for packaging applications, including industrial packaging, food packaging, and agricultural films. The segment's dominance is further strengthened by the increasing demand for high-quality films with enhanced surface properties, improved clarity, and better processability. The growing packaging industry, particularly in emerging economies, coupled with the rising demand for flexible packaging solutions across various end-user industries, continues to fuel the segment's growth and market leadership position.

Pipe and Tube Segment in Polymer Processing Aid Market

The pipe and tube segment is emerging as the fastest-growing application segment in the polymer processing aid market, with a projected growth rate of approximately 5% during the forecast period 2024-2029. This robust growth is primarily attributed to the increasing construction activities and infrastructure development projects worldwide. The segment's growth is further propelled by the rising demand for PVC pipes in building and construction applications, coupled with the growing adoption of HDPE pipes in water supply and sewage systems. The expansion of telecommunication networks, particularly the implementation of 5G infrastructure, is also contributing significantly to the segment's rapid growth as polymer processing additives are essential in manufacturing high-quality cables and conduits.

Remaining Segments in Application Segmentation

The other significant segments in the polymer processing aid market include wire and cable, extrusion blow molding, fibers and raffia, and other applications. The wire and cable segment plays a crucial role in the telecommunications and automotive industries, while extrusion blow molding is essential in producing various containers and packaging products. The fibers and raffia segment serves the textile and agricultural sectors, providing materials for various applications, including synthetic fibers and packaging materials. These segments collectively contribute to the market's diversity and overall growth, each serving specific industrial applications and end-user requirements while benefiting from technological advancements and increasing demand for high-performance plastic products.

Segment Analysis: End-User Industry

Packaging Segment in Polymer Processing Aid Market

The packaging segment continues to dominate the global polymer processing aid market, holding approximately 46% of the total market share in 2024. This significant market position is driven by the extensive use of polymer processing additives in various packaging applications, including food and beverage packaging, consumer packaged goods, pharmaceutical packaging, and other industrial packaging solutions. The segment's dominance is particularly notable in the production of blown films, cast films, and other flexible packaging materials where polymer processing aid plays a crucial role in improving processability and surface quality. The growing demand for sustainable packaging solutions, increased focus on food safety, and the expanding e-commerce sector have further strengthened the packaging segment's position in the market. Additionally, the rising consumption of packaged food and beverages across developing economies has created substantial opportunities for acrylic processing aid market manufacturers in this segment.

Transportation Segment in Polymer Processing Aid Market

The transportation segment is emerging as the fastest-growing segment in the polymer processing aid market, projected to grow at approximately 4% CAGR during 2024-2029. This growth is primarily driven by the increasing adoption of polymer processing aid in the manufacturing of automotive wire and cable jacketing, particularly in electric vehicles. The segment's growth is further supported by the global transition towards electric mobility, with major automotive manufacturers expanding their electric vehicle production capacities. The use of polymer processing aid in transportation applications has become increasingly important due to the growing demand for high-performance materials that can withstand various environmental conditions while maintaining optimal electrical insulation properties. The segment is also benefiting from technological advancements in automotive wire and cable manufacturing processes, where polymer processing aid plays a crucial role in improving production efficiency and product quality.

Remaining Segments in End-User Industry

The building and construction segment represents another significant portion of the market, primarily driven by the use of polymer processing aid in PVC pipes, profiles, and other construction materials. The IT and telecommunication segment is gaining prominence due to the increasing demand for high-quality cables and wires in network infrastructure development, particularly with the ongoing expansion of 5G networks globally. The textiles segment utilizes polymer processing aid in the production of synthetic fibers and technical textiles, while other end-user industries encompass various applications, including consumer goods and industrial products. Each of these segments contributes uniquely to the market's dynamics, with their demand patterns influenced by regional infrastructure development, technological advancement, and industrial growth trends.

Polymer Processing Aid Market Geography Segment Analysis

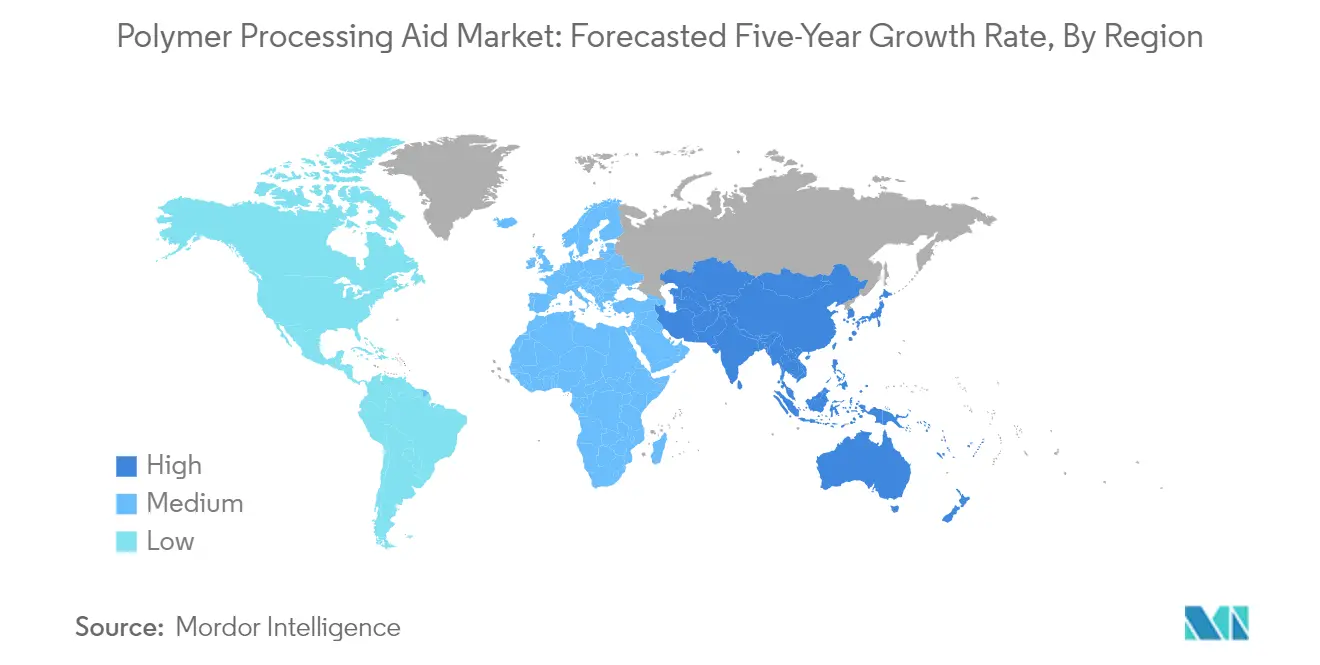

Polymer Processing Aid Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic polymer processing aid market, driven by rapid industrialization and expanding manufacturing capabilities across multiple countries. China leads the regional market, followed by significant contributions from India, Japan, South Korea, and the ASEAN countries. The region's growth is primarily supported by increasing demand from packaging, construction, and automotive industries, particularly in emerging economies. The presence of major manufacturing facilities, coupled with growing investment in infrastructure development and rising consumer goods production, continues to drive market expansion in this region.

Polymer Processing Aid Market in China

China dominates the Asia-Pacific polymer processing aid market, holding approximately 64% share of the regional market. The country's market leadership is reinforced by its massive manufacturing base, particularly in the plastics processing and packaging industries. China's polymer processing industry benefits from the country's position as the world's largest plastics producer and consumer. The government's focus on infrastructure development, coupled with growing domestic consumption and export-oriented manufacturing, continues to drive demand. The country's robust supply chain infrastructure and presence of both domestic and international manufacturers further strengthen its market position, with notable contributions from China polymer processing aids suppliers networks.

Polymer Processing Aid Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 5% during 2024-2029. The country's rapid market expansion is driven by increasing investments in manufacturing capabilities and growing demand from end-use industries such as packaging and construction. India's polymer processing industry is benefiting from government initiatives promoting domestic manufacturing and infrastructure development. The country's growing middle class, urbanization trends, and expanding industrial base are creating substantial opportunities for market growth. Additionally, increasing adoption of advanced manufacturing technologies and rising demand for high-quality plastic products are contributing to market expansion.

Polymer Processing Aid Market in North America

The North American polymer processing aid market demonstrates strong market fundamentals, supported by advanced manufacturing capabilities and technological innovation across the United States, Canada, and Mexico. The region's market is characterized by high adoption rates of advanced polymer processing technologies and stringent quality standards in plastic manufacturing. The presence of major industry players, coupled with robust research and development activities, continues to drive market growth. The region's focus on sustainable and efficient manufacturing processes has led to increased adoption of high-performance polymer processing aids.

Polymer Processing Aid Market in United States

The United States maintains its position as the largest market in North America, commanding approximately 71% of the regional market share. The country's market leadership is supported by its advanced manufacturing infrastructure and strong presence in key end-use industries such as packaging and automotive. The United States benefits from continuous technological advancements in polymer processing and a robust innovation ecosystem. The country's focus on high-performance materials and sustainable manufacturing practices further strengthens its market position. Additionally, the presence of major industry players and their ongoing research and development activities contribute to market growth.

Polymer Processing Aid Market in Canada

Canada emerges as the fastest-growing market in North America, with an expected growth rate of approximately 4% during 2024-2029. The country's market growth is driven by increasing investments in manufacturing capabilities and rising demand from various end-use industries. Canada's polymer processing companies benefit from its strong focus on technological innovation and sustainable manufacturing practices. The country's expanding industrial base and growing emphasis on high-quality plastic products contribute to market growth. Additionally, supportive government policies and increasing adoption of advanced manufacturing technologies are driving market expansion.

Polymer Processing Aid Market in Europe

The European polymer processing aid market demonstrates strong market fundamentals, supported by advanced manufacturing capabilities and technological innovation across Germany, the United Kingdom, France, Italy, and Russia. The region's market is characterized by stringent quality standards and an increasing focus on sustainable manufacturing practices. The presence of established industry players and ongoing research and development activities continues to drive market growth. The region's emphasis on the circular economy and environmental regulations shapes market dynamics and product development.

Polymer Processing Aid Market in Germany

Germany maintains its position as the largest market in Europe, driven by its robust manufacturing infrastructure and strong presence in key end-use industries. The country's leadership in the automotive and packaging sectors, coupled with its advanced technological capabilities, supports market growth. Germany's focus on Industry 4.0 and sustainable manufacturing practices further strengthens its market position. The presence of major chemical companies and their research facilities contributes to continuous innovation in polymer processing aids.

Polymer Processing Aid Market in Russia

Russia emerges as the fastest-growing market in Europe, driven by increasing investments in manufacturing capabilities and rising demand from various end-use industries. The country's market growth is supported by its expanding industrial base and growing emphasis on domestic manufacturing. Russia's polymer processing aid market benefits from its strong petrochemical industry and increasing focus on value-added products. The country's ongoing infrastructure development and modernization of manufacturing facilities contribute to market expansion.

Polymer Processing Aid Market in South America

The South American polymer processing aid market demonstrates steady growth potential, with Brazil and Argentina as key contributing countries. The region's market dynamics are influenced by increasing industrialization and growing demand from end-use sectors such as packaging and construction. Brazil emerges as both the largest and fastest-growing market in the region, driven by its robust manufacturing base and expanding industrial infrastructure. The region's market growth is supported by increasing investments in plastic processing capabilities and rising demand for high-quality plastic products. Despite economic challenges, the market continues to evolve, supported by growing domestic consumption and industrial development initiatives.

Polymer Processing Aid Market in Middle East & Africa

The Middle East & Africa polymer processing aid market shows promising growth potential, with Saudi Arabia and South Africa as key contributing countries. The region's market is driven by increasing investments in manufacturing capabilities and growing demand from various end-use industries. Saudi Arabia emerges as both the largest and fastest-growing market in the region, supported by its strong petrochemical industry and ongoing industrial diversification initiatives. The region's market benefits from growing infrastructure development and increasing focus on domestic manufacturing capabilities. Rising investments in plastic processing facilities and growing emphasis on quality improvement in plastic products continue to drive market growth.

Get Analysis on Important Geographic Markets

Download PDF

Polymer Processing Aid Industry Overview

Top Companies in Polymer Processing Aid Market

The polymer processing aid market features prominent players like The Chemours Company, Arkema Group, 3M, Solvay, and Avient Corporation leading the fluoropolymer-based segment, while Mitsubishi Chemical, Kaneka, Arkema, and LG Chem dominate the lubricant-based segment. Companies are increasingly focusing on product innovation through substantial R&D investments, with many players maintaining dedicated research centers and technical facilities across global locations. Operational agility is demonstrated through strategic capacity expansions, particularly in high-growth regions like Asia-Pacific. Market leaders are strengthening their positions through strategic acquisitions and collaborations, as evidenced by Avient Corporation's acquisition of Clariant's color masterbatch business. Companies are also expanding their manufacturing footprints across multiple continents while developing specialized distribution networks to enhance market penetration and customer service capabilities.

Market Structure Shows Mixed Consolidation Patterns

The polymer processing aids market exhibits a unique structure with varying levels of consolidation across different segments. The fluoropolymer-based segment demonstrates fragmentation with multiple players holding significant market shares, while the lubricant-based segment shows relatively higher consolidation with fewer dominant players. Global chemical conglomerates maintain strong positions through their extensive research capabilities and established distribution networks, while specialized manufacturers carve out niches through focused product development and technical expertise. The market features a mix of multinational corporations with diverse product portfolios and regional specialists with deep local market understanding.

Merger and acquisition activity in the sector reflects strategic efforts to enhance technological capabilities and expand geographical reach. Companies are increasingly pursuing vertical integration strategies to secure raw material supplies and strengthen their market positions. The competitive landscape is characterized by a combination of long-established chemical companies and emerging specialists, with many players expanding their presence through joint ventures and strategic partnerships. Market participants are also focusing on developing region-specific product portfolios to address varying customer requirements across different geographical markets.

Innovation and Sustainability Drive Future Success

Success in the polymer processing aid market increasingly depends on companies' ability to innovate while meeting sustainability requirements. Market leaders are strengthening their positions through investments in advanced manufacturing technologies and the development of eco-friendly products. Companies are focusing on building strong relationships with end-users in key industries like packaging and construction, while also expanding their presence in emerging applications. The ability to provide technical support and customized solutions is becoming increasingly crucial for maintaining market share, as is the development of efficient distribution networks and local manufacturing capabilities.

For new entrants and smaller players, success lies in identifying and serving niche markets while developing innovative solutions for specific applications. Companies must navigate evolving regulatory landscapes, particularly regarding environmental regulations and plastic usage restrictions. The development of sustainable products and processes is becoming a key differentiator in the market. Players are also focusing on building strong technical service capabilities and maintaining close relationships with key customers to protect against substitution risks. The ability to adapt to changing market conditions and maintain cost competitiveness while ensuring product quality remains crucial for long-term success in the polymer materials market segmentation.

Polymer Processing Aid Market Leaders

-

3M

-

KANEKA CORPORATION

-

The Chemours Company

-

Mitsubishi Chemical Corporation

-

Arkema

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Polymer Processing Aid Market News

- January 2023: Ampacet Corporation has introduced PFAS free polymer processing aid 1001316-N which can be utilized in blown film extrusion for numerous end use applications.

- October 2022: Clariant introduces new polymer processing additives at K 2022 to support the long-term evolution of polymers. This new product facilitates the reuse of plastic in numerous consumer applications.

Polymer Processing Aid Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Demand for Polypropylene from the Packaging Industry

- 4.1.2 Usage of PVC and HDPE in the Building and Infrastructure Industry

- 4.1.3 Other Drivers

-

4.2 Restraints

- 4.2.1 Quality Difficulties and High Product Costs due to Polymer Processing Aid

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value

-

5.1 Polymer Type

- 5.1.1 Polyethylene

- 5.1.1.1 LLDPE

- 5.1.1.2 LDPE

- 5.1.1.3 HDPE

- 5.1.2 Polypropylene

- 5.1.3 PVC, ABS, and Polycarbonate

- 5.1.4 Other Polymer Types

-

5.2 Application

- 5.2.1 Blown Film and Cast Film

- 5.2.2 Wire and Cable

- 5.2.3 Extrusion Blow Molding

- 5.2.4 Fibers and Raffia

- 5.2.5 Pipe and Tube

- 5.2.6 Other Applications

-

5.3 End-user Industry

- 5.3.1 Packaging

- 5.3.2 Building and Construction

- 5.3.3 Transportation

- 5.3.4 Textiles

- 5.3.5 IT and Telecommunication

- 5.3.6 Other End-user Industries

-

5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 UK

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Abalysis (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Ampacet Corporation

- 6.4.3 Arkema

- 6.4.4 Avient Corporation

- 6.4.5 BASF SE

- 6.4.6 Clariant

- 6.4.7 DAIKIN INDUSTRIES, Ltd.

- 6.4.8 Dow

- 6.4.9 Evonik Industries AG

- 6.4.10 Fine Organic Industries Limited

- 6.4.11 Guangzhou Shine Polymer Technology Co. Ltd

- 6.4.12 Gujarat Fluorochemicals Limited (GFL)

- 6.4.13 HANNANOTECH CO., LTD.

- 6.4.14 Kaneka Corporation

- 6.4.15 LG Chem

- 6.4.16 MicroMB (INDEVCO Group)

- 6.4.17 Mitsubishi Chemical Corporation

- 6.4.18 Mitsui Chemicals Inc.

- 6.4.19 Nouryon

- 6.4.20 Plastiblends

- 6.4.21 PMC Group, Inc.

- 6.4.22 Shanghai Lanpoly Polymer Technology Co. Ltd

- 6.4.23 Solvay

- 6.4.24 The Chemours Company

- 6.4.25 Tosaf Compounds Ltd

- 6.4.26 WSD CHEMICAL COMPANY

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Electric Vehicles Penetration

- 7.2 Upcoming Projects in the Telecommunication Sector

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Polymer Processing Aid Industry Segmentation

Polymer Processing Aids (PPAs) are additives added to the base polymer to improve the material's processability, processing properties, and the end product's quality. The polymer processing aid market is segmented based on polymer type, application, end-user industry, and geography. The market is segmented by polymer type into polyethylene, polypropylene, PVC, ABS, polycarbonate, and other polymer types. The market is segmented by application into blown film & cast film, wire & cable, extrusion blow molding, fibers & raffia, pipe & tube, and other applications. By end-user industry, the market is segmented into packaging, building and construction, transportation, textiles, IT and telecommunication, and other end-user industries. The report also covers the size and forecasts for the polymer processing aid market in 16 countries across major regions. Each segment's market sizing and forecasts are based on revenue (USD).

| Polymer Type | Polyethylene | LLDPE | |

| LDPE | |||

| HDPE | |||

| Polypropylene | |||

| PVC, ABS, and Polycarbonate | |||

| Other Polymer Types | |||

| Application | Blown Film and Cast Film | ||

| Wire and Cable | |||

| Extrusion Blow Molding | |||

| Fibers and Raffia | |||

| Pipe and Tube | |||

| Other Applications | |||

| End-user Industry | Packaging | ||

| Building and Construction | |||

| Transportation | |||

| Textiles | |||

| IT and Telecommunication | |||

| Other End-user Industries | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| UK | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Polymer Processing Aid Market Research FAQs

What is the current Polymer Processing Aid Market size?

The Polymer Processing Aid Market is projected to register a CAGR of 4.76% during the forecast period (2025-2030)

Who are the key players in Polymer Processing Aid Market?

3M, KANEKA CORPORATION, The Chemours Company, Mitsubishi Chemical Corporation and Arkema are the major companies operating in the Polymer Processing Aid Market.

Which is the fastest growing region in Polymer Processing Aid Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Polymer Processing Aid Market?

In 2025, the Asia-Pacific accounts for the largest market share in Polymer Processing Aid Market.

What years does this Polymer Processing Aid Market cover?

The report covers the Polymer Processing Aid Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Polymer Processing Aid Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Polymer Processing Aid Market Research

Mordor Intelligence provides a comprehensive analysis of the polymer processing aid market. We leverage our extensive experience in polymer industry trends and global market research. Our detailed examination of the global polymer market offers crucial insights into polymer processing aids and their applications across various industries. The report covers polymer processing additives and developments in process aid additive, focusing particularly on processing aid for polyethylene and other key materials in the polymer processing industry.

Stakeholders in the PPA market will benefit from our thorough analysis of plastic processing aids and their impact on manufacturing efficiency. The report, available as an easy-to-download PDF, provides valuable insights into polymer processing technologies and emerging opportunities. Our research covers fluoropolymer processing aid market dynamics and polymer materials market segmentation, equipping decision-makers with actionable intelligence for strategic planning. The analysis includes detailed profiles of leading polymer processing company operations and examines critical factors influencing the global polymer market size.