Platinum Group Metals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

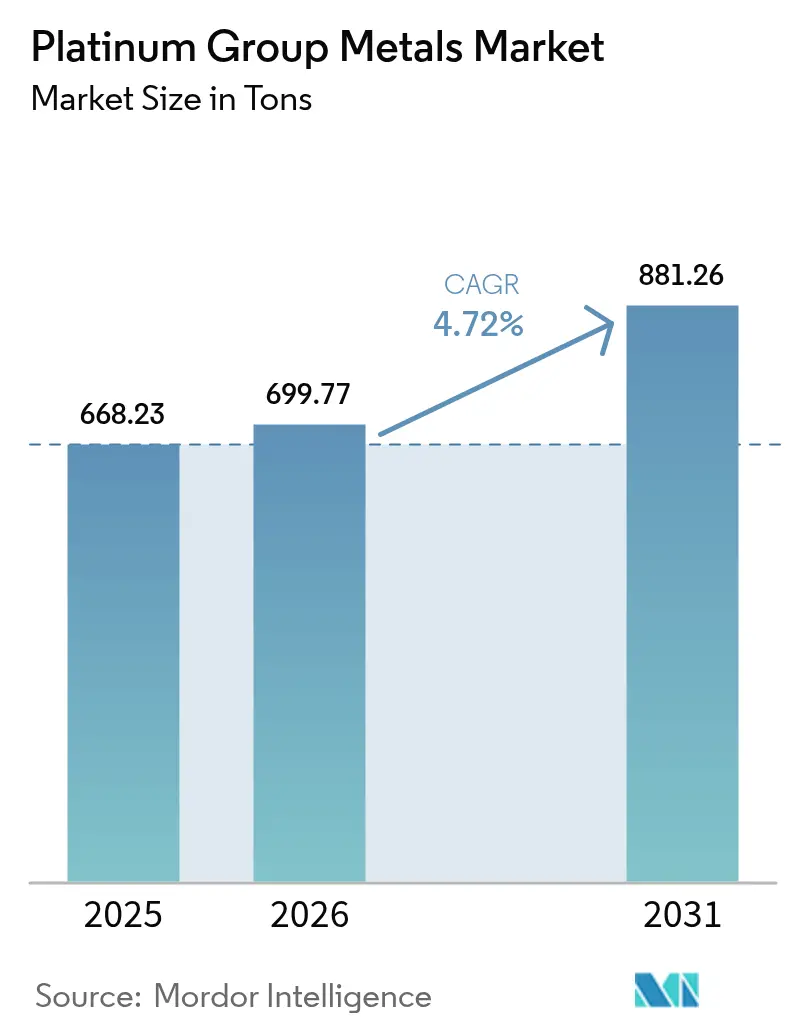

| Market Volume (2026) | 699.77 tons |

| Market Volume (2031) | 881.26 tons |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

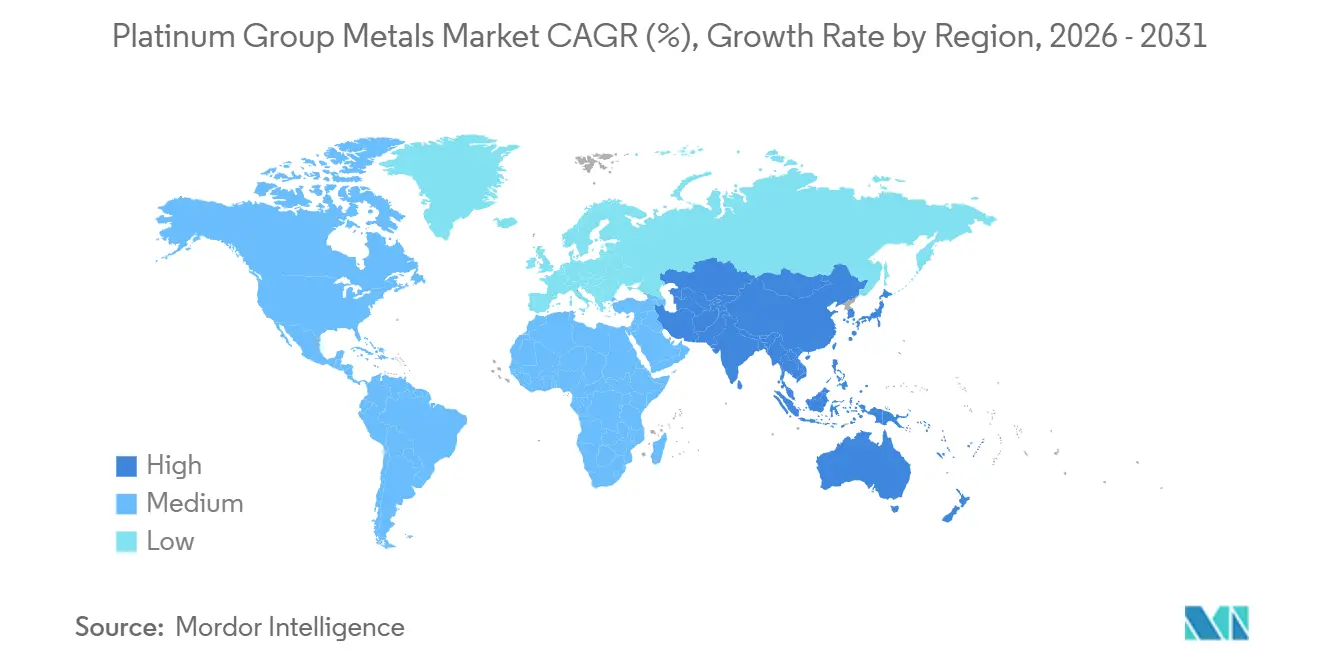

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Platinum Group Metals Market Analysis by Mordor Intelligence

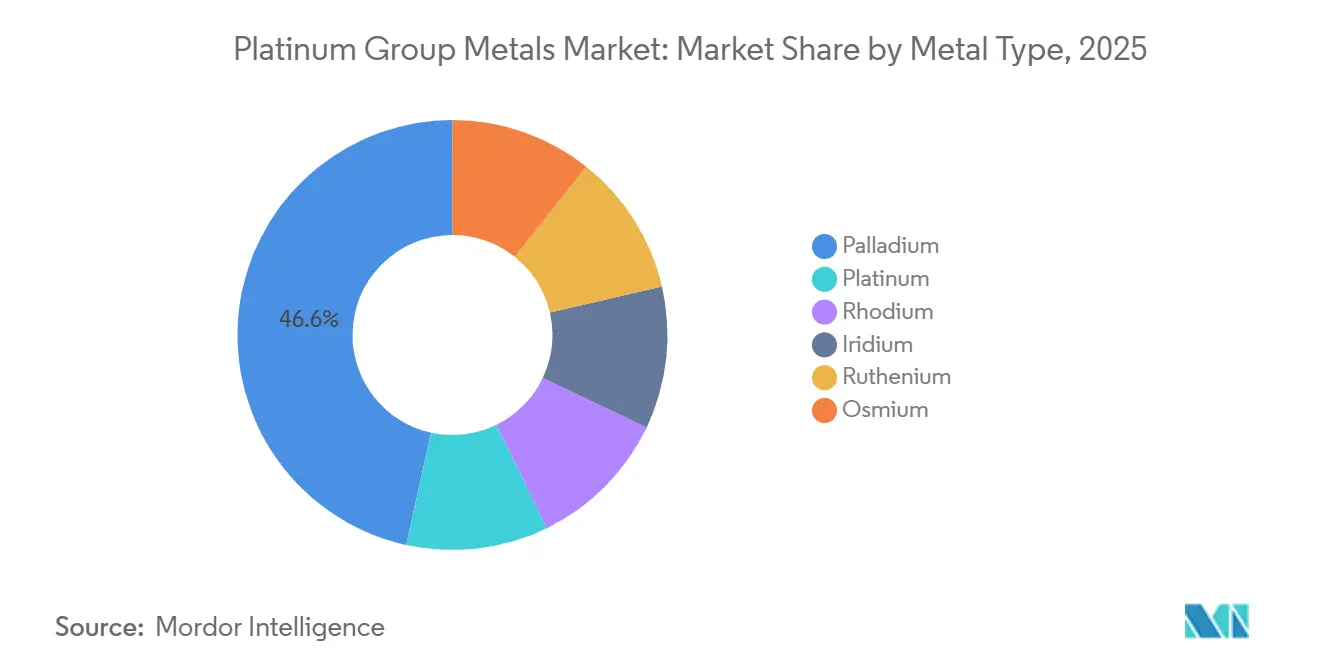

The Platinum Group Metals Market size was valued at 668.23 tons in 2025 and is estimated to grow from 699.77 tons in 2026 to reach 881.26 tons by 2031, at a CAGR of 4.72% during the forecast period (2026-2031). Demand keeps tilting away from legacy autocatalysts toward low-carbon technologies, especially hydrogen infrastructure, while advanced electronics unlock new use cases for ruthenium and iridium. Palladium’s 46.55% share in 2025 is slipping because gasoline-vehicle makers are engineering platinum-rich catalysts, whereas iridium’s 8.92% CAGR reflects proton-exchange-membrane (PEM) electrolyser growth in North America and Europe. Rhodium and ruthenium prices remain volatile, so original-equipment manufacturers (OEMs) are striking shorter offtake contracts to hedge exposure. Recycling economics are tightening the cost curve, secondary material already meets 57% of European Union demand and is forecast to capture more than one-third of global supply by 2031.

Key Report Takeaways

- By metal type, palladium led with 46.55% revenue share in 2025, whereas iridium is projected to expand at an 8.92% CAGR through 2031.

- By application, jewelry held 28.75% of the Platinum group metals market size in 2025, while fuel cells are advancing at a 28.47% CAGR to 2031.

- By source, primary mining supplied 71.40% of volume in 2025; secondary recycling is the fastest-growing source at a 7.08% CAGR through 2031.

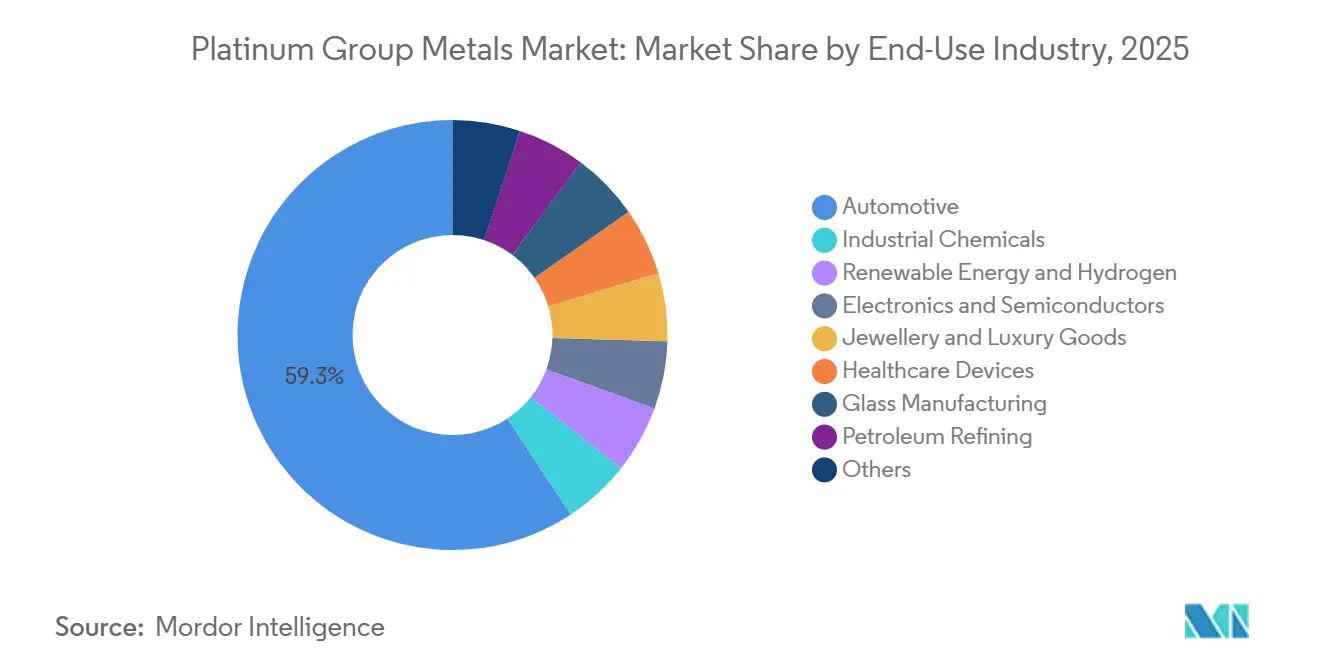

- By end-use industry, automotive accounted for 59.25% of the Platinum group metals market size in 2025; renewable energy and hydrogen applications are set to grow at a 9.32% CAGR between 2026-2031.

- By geography, Asia-Pacific commanded 51.60% of the Platinum group metals market share in 2025, and is projected to expand at a 5.03% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Platinum Group Metals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for autocatalysts in emerging-market ICE vehicles | +1.2% | Asia-Pacific (India, ASEAN), South America (Brazil, Argentina) | Medium term (2-4 years) |

| PEM-electrolyser build-out across North America and EU hydrogen hubs | +1.8% | North America, Europe | Long term (≥4 years) |

| IC substrate plating boom in high-end electronics (Ruthenium focus) | +0.9% | Global, concentrated in Asia-Pacific semiconductor hubs | Medium term (2-4 years) |

| Dual-metal upswing from Pd-for-Pt catalyst substitution | +0.6% | Global, strongest in North America and Europe automotive | Short term (≤2 years) |

| Platinum-based ammonia cracking solutions for maritime e-fuels | +0.4% | Europe, Asia-Pacific maritime corridors | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Autocatalysts in Emerging-Market ICE Vehicles

India produced 4.2 million passenger vehicles in 2024, and BS-VI Phase 2 rules raised platinum group metal loadings more than 60% per unit to hit stringent nitrogen-oxide caps[1]International Council on Clean Transportation, “Global Vehicle Emissions Standards,” theicct.org. Thailand, Indonesia, and Vietnam together assembled about 4 million vehicles in 2024, and flex-fuel cars in Brazil added rhodium-rich catalysts to withstand higher combustion temperatures. Mexico’s 3.5 million-unit production for U.S. exports faces Tier 3 Bin 70 rules that prompt over-specification of metal content. The International Council on Clean Transportation foresees 12 million extra light-vehicle sales across emerging markets between 2026 and 2031, with internal-combustion engines still holding more than 70% share in price-sensitive segments.

PEM-Electrolyser Build-Out Across Hydrogen Hubs

Platinum demand for hydrogen climbed from 40 thousand ounces in 2023 to an expected 476 thousand ounces by 2028, with PEM systems contributing most of the rise. The US Inflation Reduction Act earmarked USD 7 billion for regional hubs that will consume 200-250 g of platinum and 15-20 g of iridium per MW by 2027. Europe’s Fit for 55 package targets 10 million t of renewable hydrogen by 2030, but iridium scarcity could cap PEM capacity at roughly 45 GW unless alternative electrolysis technologies scale.

IC Substrate Plating Boom in Advanced Electronics

Applied Materials and imec showed in 2024 that ruthenium liners improve resistance–capacitance by up to 71% in sub-5 nm interconnects, unlocking ruthenium demand of 18-22 t by 2026 as TSMC and Samsung shift to 3 nm logic[2]Applied Materials, “Ruthenium Barriers for Advanced Nodes,” appliedmaterials.com. Ruthenium’s 4.7 eV work function cuts leakage 40% against cobalt, critical for power-dense chiplet designs. Hard-disk drives released 8-10 t of platinum annually as shipments slowed, and semiconductor fabs absorbed the freed metal without supply strains.

Dual-Metal Upswing from Pd-for-Pt Catalyst Substitution

Palladium’s price collapse from USD 3,000 / oz in 2022 to USD 1,000 / oz in 2024 triggered 540-700 k oz of switching into platinum-heavy catalysts. Further substitution will be modest until the 2027-2028 model-year refreshes because formulations are frozen two years before launch. Diesel oxidation catalysts are already platinum-rich, and delayed Euro 7 rules will lift metal loadings another 10-15% from 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent PGM price volatility constraining OEM offtake contracts | -0.8% | Global, acute in automotive and electronics | Short term (≤2 years) |

| Escalating energy and water intensity of deep-level South African mines | -1.1% | South Africa, spillover to global supply | Medium term (2-4 years) |

| Closed-loop recycling growth reducing primary metal demand | -0.7% | Europe, North America, Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Persistent PGM Price Volatility Constraining OEM Contracts

Rhodium plunged 85% from USD 29,800 / oz in 2021 to USD 4,500 / oz in 2024, squeezing tier-one supplier margins by up to 500 bps as fixed contracts matured. Palladium’s 40% intrayear swings forced Japanese and German automakers to shorten hedge horizons to six-nine months, shifting inventory risk to refiners. Iridium lacks a deep futures curve, so price discovery depends on thin bilateral trades, deterring long-run capacity investment.

Escalating Energy and Water Intensity of South African Mines

Sibanye-Stillwater, Impala Platinum, and Anglo American Platinum saw 2024 output drop 11-14% as shafts descended beyond 3 km, where cooling absorbs up to 30% of operating costs. Eskom’s 12.74% tariff hike, rolling blackouts, and water deficits in the Bushveld Complex lifted cash costs by USD 80-120 / oz. Zimbabwe added 450 k oz in 2024, but logistics bottlenecks limit its ability to offset South African declines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Metal Type: Iridium Leads Growth as Electrolyser Economics Tighten

Iridium’s 8.92% CAGR positions it as the fastest-growing element inside the platinum group metals market, even though it accounted for only 3-4 t in 2025. PEM electrolyser makers are slicing coating thickness from 3 µm to 1 µm, which halves iridium intensity while still demanding more tonnage than the 2023 baseline. Palladium’s 46.55% share is receding as battery-electric sales rise in China and substitution into platinum accelerates across US and EU gasoline platforms. Rhodium’s volatility spurs OEMs to engineer palladium-rhodium blends that trade 5-8% conversion efficiency for cost predictability. Ruthenium’s move into sub-5 nm interconnects lifts yearly demand by 10-12 t, while osmium stays a sub-500 kg niche. Combined, these shifts redistribute platinum group metals market share toward a more diversified mix.

By Application: Fuel Cells Surge as Jewelry Plateaus

Fuel cells are projected to climb at a 28.47% CAGR and could top 10% of the platinum group metals market size by 2031 as Toyota, Hyundai, and Chinese truck makers roll out PEM drivetrains and data-center backup systems. Jewelry, with a share of 28.75% in 2025, stagnates because Chinese and Indian consumers pivot to gold and synthetics when platinum breaches USD 1,000 / oz. Autocatalysts still dominate volume, but their share declines as battery-electric models take up a quarter of new-car sales in major markets by 2026. Electronics gain incremental lift from ruthenium interconnects, while medical and chemical catalysts provide a steady baseline demand.

By Source: Secondary Recycling Gains as Primary Output Stagnates

Primary mines supplied 71.40% of 2025 tonnage, but secondary flows are climbing 7.08% annually, driven by mandatory EU take-back laws, the UK’s 300 k-unit Johnson Matthey plant, and US autocatalyst feedstock captured by the new Montana JV between Sibanye-Stillwater and Glencore. China’s aging vehicle parc will add 180-220 k oz of recoverable metals yearly after 2027. Deep-level cost inflation and power shortages in South Africa leave recycling as the low-cost swing supplier within the platinum group metals market.

By End-Use Industry: Automotive Dominates, Renewable Energy Surges

The automotive industry commanded 59.25% of end-use volume in 2025, yet renewable energy and hydrogen will grow at 9.32% through 2031 as proton-exchange membrane electrolysers convert policy commitments into gigawatt-scale installations and fuel-cell electric vehicles expand beyond niche deployments. Electronics now absorb the incremental ruthenium flow, whereas industrial chemicals and glass act as slow-growth pillars. Jewelry’s softness and refining’s plateau create a future landscape where hydrogen value chains, data centers, and healthcare consume a higher share of the platinum group metals market size.

Geography Analysis

Asia Pacific owns 51.60% of the platinum group metals market volume and is set to grow 5.03% annually. India’s BS-VI Phase 2 standards, ASEAN’s 4 million-vehicle assembly base, and South Korea’s semiconductor expansions underpin demand. North America leverages USD 7 billion in hydrogen-hub incentives and produces 10.5 million light vehicles, which hold high catalyst loadings to satisfy Tier 3 standards. Europe’s Fit for 55 plan and postponed Euro 7 rules raise both hydrogen and autocatalyst requirements, yet recycling already meets 57% of its needs. South Africa provides more than 70% of the world's platinum, but power, water, and depth constraints cut 2024 output by double digits, while Zimbabwe’s incremental 450 k oz cannot fully offset losses. These dynamics keep regional supply-demand balances tight and reinforce the strategic value of recycling in the platinum group metals market.

Value Chain Analysis

The platinum group metals (PGM) value chain begins with primary supply from deep-level mining and concentration, anchored by producers such as Anglo American Platinum, Impala Platinum, Sibanye-Stillwater, Northam Platinum, and MMC Norilsk Nickel. Concentrate is smelted and refined into high-purity metals and salts, with availability sensitive to power, water, maintenance outages, and weather disruptions in Southern Africa, alongside operational restructuring at mature assets. Pricing and contracting flow through established trading venues and a growing Asia-based pricing ecosystem, including the Guangzhou Futures Exchange (GFEX) introduction of platinum and palladium futures, which has been highlighted as a structural shift in how Chinese demand interfaces with global pricing.

Downstream, fabricators convert refined PGMs into autocatalysts, chemical catalysts, electronics and semiconductor materials, and hydrogen-related components (fuel cells and PEM electrolysers), then sell into OEM and industrial end markets. End-of-life collection and recycling increasingly tighten this loop, especially in regions with mandatory take-back regimes and established catalytic-converter collection networks; the report context notes that secondary material already meets 57% of European Union demand. With tightening scrap availability and volatile rhodium and ruthenium pricing, buyers are leaning toward shorter offtake terms and more active inventory management across refiners, catalyst makers, and OEM supply chains.

Competitive Landscape

The Platinum Group Metals market is highly consolidated. Vertical integration shields miners like Sibanye-Stillwater, which couples South African shafts with Montana refining. Technology leadership, iridium-saving coatings, mechanochemical recycling, and ruthenium interconnect IP define value capture as the platinum group metals market transitions toward hydrogen and electronics. Patent filings on iridium-free anodes and ruthenium barriers surged in 2024-2025, pointing to supply-constrained metals as R&D hotspots. Start-ups focusing on plasma-assisted refining and low-temperature leaching aim to undercut incumbent tolling fees, intensifying competition downstream.

Platinum Group Metals Industry Leaders

Anglo American plc

Norilsk Nickel

Impala Platinum Holdings Ltd

Sibanye-Stillwater Limited

Northam Platinum Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The main opportunity sits where the market is re-weighting from legacy autocatalyst demand toward hydrogen and advanced electronics that require tight specifications and secure sourcing. In hydrogen value chains, policy-led build-outs such as the US Inflation Reduction Act funding for regional hydrogen hubs (USD 7 billion) are anchoring near-term procurement programs for platinum and iridium in PEM systems. At the same time, iridium-thrifting coatings and thinner catalyst layers are creating whitespace for catalyst IP, coating services, and qualified recycling of electrolyser and fuel-cell stacks. In electronics, the shift to sub-5 nm interconnects has pulled ruthenium into next-generation metallization and plating, which raises qualification and supply-chain needs around high-purity ruthenium compounds and sputtering targets.

On the supply side, brownfield and phased mine expansions, along with new projects, are creating openings for toll refining, regional processing, and structured offtake that reduces volatility exposure. Recent company actions reinforce this investment pipeline: Ivanhoe Mines reported major milestones at its Platreef development, including hoisting-capacity progress, with Phase 2 framed to lift production capacity by the end of 2027, and Northam Platinum approved a capital program at Zondereinde to expand production to above 400,000 ounces per annum. The launch of platinum and palladium futures on the Guangzhou Futures Exchange also provides a more localized hedging and procurement pathway in Asia, supporting increased trading, inventory financing, and risk-management services tied to physical flows.

Recent Industry Developments

- July 2026: Northam Platinum reported full-year production and sales performance for the financial year ended June 2026, including record refined metal production of 938,754 oz of 4E PGMs. The update reinforces the role of large, operationally stable South African producers in balancing near-term refined availability amid broader cost and power constraints in the region.

- May 2026: Sibanye-Stillwater released production results for the first quarter ended March 31, 2026, reporting a year-on-year increase in 4E PGM output. The results highlight the continuing focus on operating discipline and incremental productivity gains as customers push for shorter contract cycles and tighter working-capital exposure during periods of price volatility.

- November 2024: Industry coverage noted that low PGM prices were constraining ESG spend and capital flexibility across PGM miners, even as core programs continued. The environment increased emphasis on cost, water, and power resilience at deep-level operations, shaping how new projects, sustaining capital, and recycling investments compete for funding.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the platinum group metals market is defined as the global supply and demand of platinum, palladium, rhodium, ruthenium, iridium, and osmium that are traded and consumed across industrial and investment-linked value chains, measured as metal volume (tons).

Scope exclusions: Pricing-only benchmarks and derivatives trading activity are excluded unless they translate into physical metal movement and end-use consumption.

Segmentation Overview

- By Metal Type

- Platinum

- Palladium

- Rhodium

- Iridium

- Ruthenium

- Osmium

- By Application

- Auto Catalysts

- Electrical and Electronics

- Fuel Cells

- Glass, Ceramics and Pigments

- Jewellery

- Medical (Dental and Pharma)

- Chemical Industry

- Other (Aerospace, Sensors, Water, Forensics)

- By Source

- Primary (Mined)

- Recycled/Secondary

- By End-Use Industry

- Automotive

- Industrial Chemicals

- Renewable Energy and Hydrogen

- Electronics and Semiconductors

- Jewellery and Luxury Goods

- Healthcare Devices

- Glass Manufacturing

- Petroleum Refining

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean picture of physical PGM flow, where production, recycling, and trade are reconciled into one consistent dataset. We rely on public and official sources such as USGS minerals data, UN Comtrade trade statistics, national geological agencies, customs and tariff schedules, and peer-reviewed metallurgy and recycling journals to understand how ounces convert into industrial-grade supply.

On top of this, we cross-check assumptions using company annual reports, investor presentations, exchange filings, and reputable industry press to understand operating changes, shutdowns, and project ramps that can shift availability. When needed, we also reference paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export views to reduce data gaps around recycling routes and cross-border metal movements. These sources are illustrative, and many other references are used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating how supply is actually entering the market and how demand is being pulled by end users like auto catalyst value chains, chemical processing, electronics, and emerging hydrogen use cases. We speak with a balanced mix of producers, recyclers, traders, and downstream users across APAC, EMEA, and the Americas so that volume assumptions, scrap return rates, and application mix can be checked and corrected where secondary data is thin.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 45% |

| Mid tier: 49% | Functional/Unit leaders: 36% | EMEA: 30% |

| Smaller Players: 20% | Managers: 52% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down model where mined output, secondary supply from recycling, and net trade are used to reconstruct the physical metal availability by year, which is then aligned to end-use pull. To keep the numbers practical, we corroborate the totals with selective bottom-up checks such as sampled producer and recycler volume roll-ups, channel discussions on tightness and inventory, and spot checks of typical metal intensity by application.

Key inputs used in the model include mined production volumes by region, recycling rates and scrap return timing, automotive catalyst build and substitution patterns between platinum and palladium, industrial and chemical catalyst demand signals, and the pace of capacity additions or curtailments that change supply availability. For forecasting, scenario analysis is applied around a base case, where the forward view is shaped by expected vehicle production trends, emissions compliance intensity, recycling economics, and project pipeline realism validated by primary inputs. Where bottom-up inputs are missing for smaller flows, conservative proxy ratios are used and then corrected through expert feedback before final totals are locked.

Data Validation & Update Cycle

Validation is done through multiple passes so that outliers get caught early and the final number stays consistent with real market signals. We compare the model output against independent indicators such as published production series, trade movements, and known supply disruptions, and then investigate any large variance that cannot be explained by demand shifts or recycling changes.

Before sign-off, the work is reviewed by another analyst who checks formulas, conversions, and year-on-year movements for consistency. Reports are refreshed annually, and interim updates are made when material events occur such as major mine outages, policy-driven demand changes, or large recycling flow shifts. Right before delivery, a fresh review is completed so clients receive the most current view available.

Mordor Intelligence's Platinum Group Metals Market Sizing Compared With Other Published Estimates

Published market sizes for platinum group metals can look far apart because the underlying unit, scope, and conversion logic are not always the same. Some sources report value in USD, others report physical volume, and a few blend investment-driven pricing swings into what is meant to be an industrial consumption view.

The main gap comes from mixing price-based revenue with physical metal flow, where Mordor Intelligence keeps the sizing in tons and counts supply and demand only when it maps to mined output, recycling return, and net trade aligned to end-use pull, instead of using a USD price deck to inflate or compress the market in volatile years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 699.77 M (2026) | |

| Global Consultancy A | USD 26.81 B (2024) | Reported in USD revenue terms, which can move sharply with metal prices even if physical tons are stable, and the base year is set to 2023 with a 2024 value estimate. |

| Industry Publisher B | USD 40.20 B (2023) | Uses USD valuation with a 2023 base, and the implied pricing assumptions and currency timing are not transparent, which can widen the gap versus a volume-led model. |

The table shows that most of the spread is explained by unit choice and whether pricing is treated as the core driver of market size. By anchoring the calculation to measurable physical flow variables and then validating key assumptions through interviews, the final number stays easier to trace and repeat year after year.

Key Questions Answered in the Report

What is the projected volume for platinum group metals in 2031?

The market is forecast to reach 881.26 tons by 2031, up from 699.77 tons in 2026, reflecting a 4.72% CAGR.

Which segment adds the most incremental growth by 2031?

Fuel cells expand at a 28.47% CAGR, becoming the fastest-growing application as hydrogen infrastructure scales.

Why is iridium demand rising so quickly?

PEM electrolysers for green hydrogen need iridium-coated anodes, so capacity additions drive an 8.92% CAGR.

How will recycling influence future supply balances?

Secondary material is expected to meet 40-45% of total demand by 2031 as EU and U.S. collection rates climb.

Which region leads consumption today?

Asia accounts for 51.60% of 2025 volume and remains the largest regional consumer through the forecast period.

Page last updated on: