Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 509.4 Billion |

| Market Size (2031) | USD 597.43 Billion |

| Growth Rate (2026 - 2031) | 3.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Plastic Packaging Market Analysis by Mordor Intelligence

plastic packaging market size in 2026 is estimated at USD 509.4 billion, growing from 2025 value of USD 493.42 billion with 2031 projections showing USD 597.43 billion, growing at 3.24% CAGR over 2026-2031. Robust e-commerce activity, rising convenience-food consumption, and cost-competitive advantages over alternate substrates underpin sustained demand even as regulatory scrutiny intensifies. Incumbents able to fund chemical-recycling lines, redesign packs for tethered-cap rules, and meet high recycled-content thresholds secure competitive insulation while smaller converters confront escalating compliance costs. Concurrently, logistics inflation elevates the value proposition of lightweight flexible formats that trim freight bills, strengthening supplier contracts in e-commerce, food, and healthcare channels. Consolidation accelerates as scale becomes prerequisite for funding advanced R&D and closed-loop supply agreements.

Key Report Takeaways

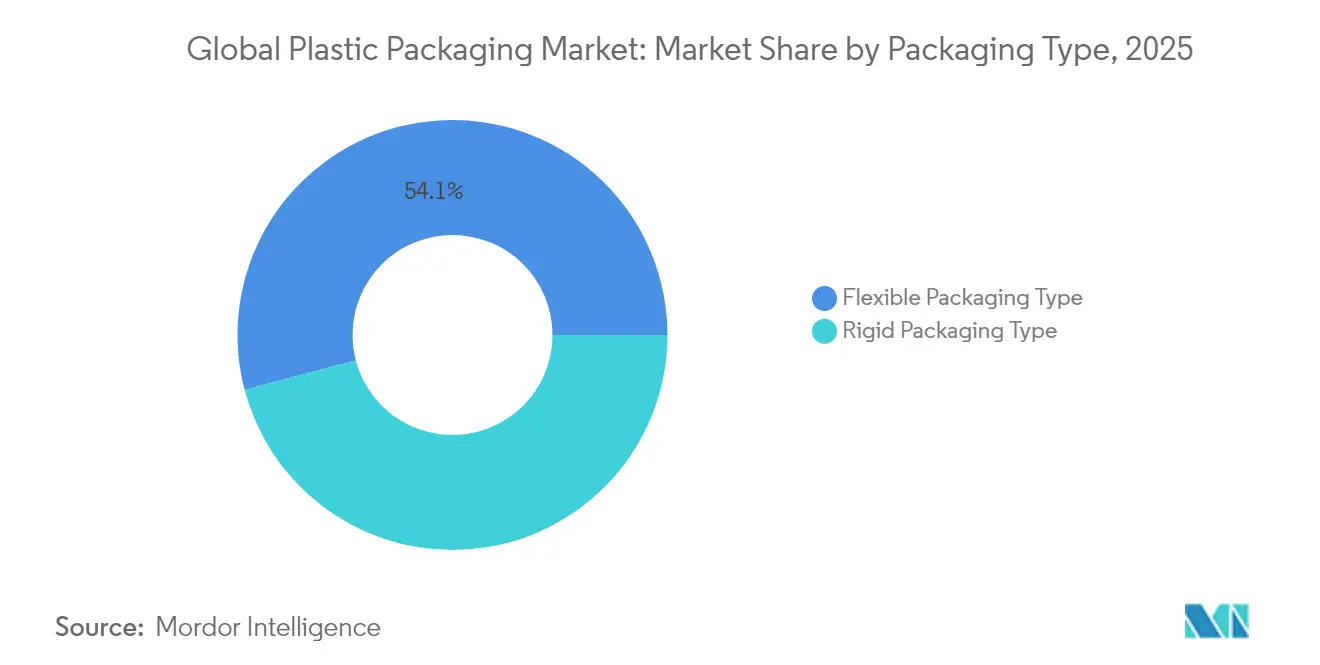

- By packaging type, flexible formats led with 54.10% revenue share in 2025; the segment is also the fastest growing at a 4.41% CAGR to 2031.

- By material, polyethylene accounted for 41.85% of plastic packaging market share in 2025, but polypropylene records the highest projected CAGR at 5.55% through 2031.

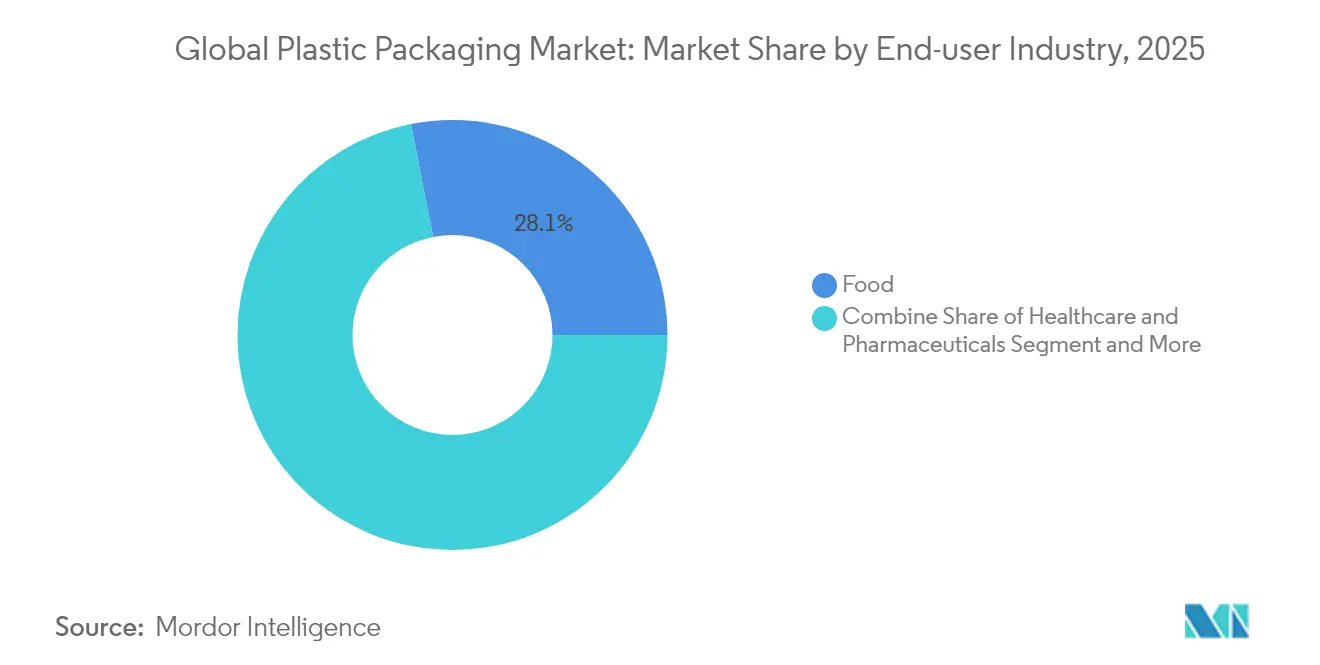

- By end-user industry, food commanded 28.10% share of the plastic packaging market size in 2025, whereas healthcare and pharmaceuticals are forecast to expand at a 6.29% CAGR to 2031.

- By distribution channel, direct sales captured 64.70% share of the plastic packaging market size in 2025, while indirect channels are advancing at a 4.64% CAGR through 2031.

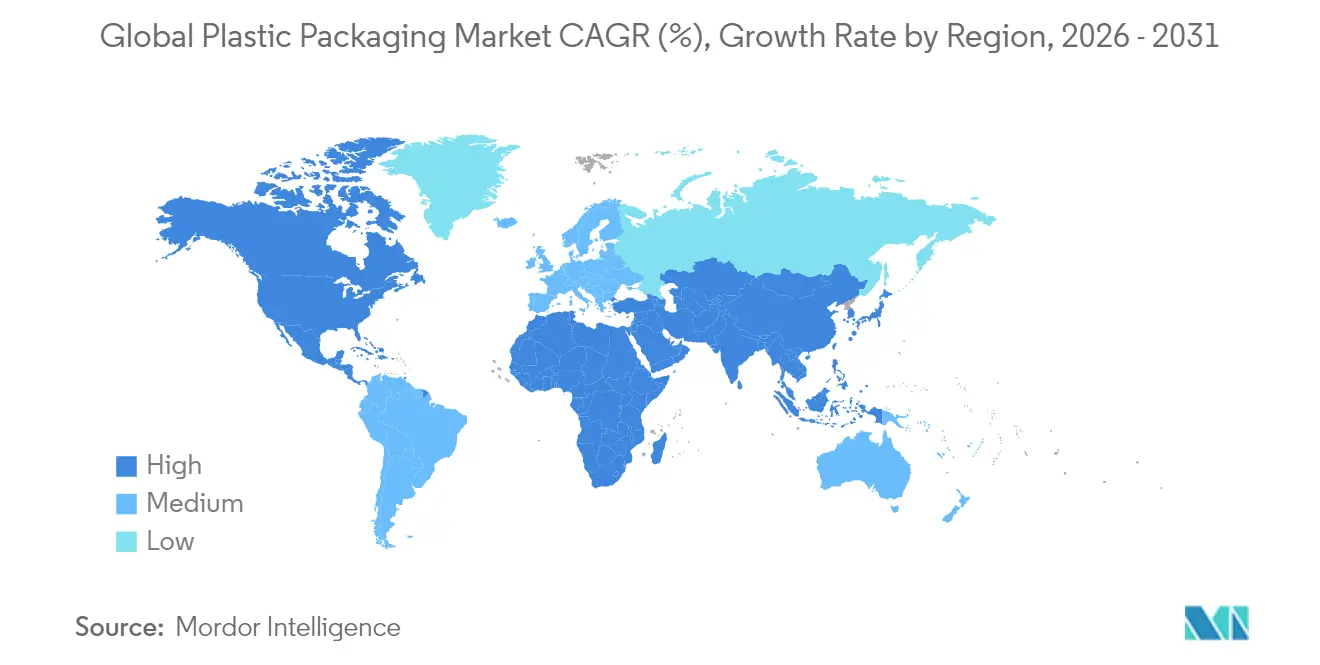

- Regionally, Asia-Pacific held 40.80% of global revenue in 2025 and is growing at a 6.78% CAGR, outpacing all other geographies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom demanding durable last-mile packs | +0.8% | Global, strongest in APAC & North America | Medium term (2-4 years) |

| Surge in convenience-food and beverage consumption | +0.6% | Global, strongest in emerging markets | Long term (≥ 4 years) |

| Cost-competitive performance versus alternate substrates | +0.4% | Global, particularly cost-sensitive markets | Short term (≤ 2 years) |

| Expansion of chemical-recycling infrastructure | +0.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Shift to mono-material films for EPR compliance | +0.3% | EU core, spill-over to developed markets | Medium term (2-4 years) |

| EU tethered-cap rule driving specialty closures volume | +0.2% | EU primary, adoption spreading | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

E-commerce Boom Demanding Durable Last-Mile Packs

Last-mile delivery models expose packages to multiple handling events and dimensional weight billing, prompting brand owners to favor films, pouches, and mailers that shrink void space by up to 75% versus rigid alternatives. Amazon’s frustration-free packaging protocol, now covering more than 300,000 SKUs, shapes de facto industry specifications and pushes SME sellers toward compliant polyethylene and polypropylene solutions. Automated sortation lines require mono-material constructions that withstand optical detection; mixed-material packs risk rejection and costly rework. A 15% reduction in package volume translates to 12% lower freight expenditure, more than offsetting the 8-10% material premium for high-performance flexible films. Barrier-coated flexibles also extend protection to electronics and temperature-sensitive pharmaceuticals, broadening addressable segments beyond food.

Surge in Convenience-Food and Beverage Consumption

Urbanization, smaller household sizes, and longer working hours spur demand for single-portion, shelf-stable meals. Processed-food uptake among urban consumers rose 8.2% year-on-year in 2024, the fastest climb on record.[1]U.S. Department of Agriculture, “Vegetables and Pulses Outlook April 2024,” usda.govMultilayer flexibles combining oxygen and moisture barriers plus microwave compatibility outperform paper-based options on shelf-life and safety. Beverage innovators add tethered closures and tamper-evident features, absorbing EUR 0.02–0.04 extra per unit in manufacturing cost to avoid regulatory penalties. [2]ALPLA Group, “Tethered Caps,” alpla.com Extended shelf-life packs enable dairy and juice brands to reach rural areas lacking cold chains, further cementing flexible dominance in emerging markets.

Cost-Competitive Performance Versus Alternate Substrates

Even after resin inflation, plastic packs retain a 25-40% material-cost edge over paper-based substitutes and weigh 3–5 times less, translating to sizable logistics savings. Plastic’s superior oxygen and moisture barrier properties extend food shelf life by 40-60%, reducing spoilage-generated greenhouse emissions. Glass incurs 200–300% higher freight costs and breakage losses, while metal affords favorable economics primarily in beverage cans where closed-loop recycling is well established. Carbon taxes would need to surpass USD 100 t/CO₂e to materially shift the cost curve in favor of paper, a threshold unlikely near-term.

Expansion of Chemical-Recycling Infrastructure

LyondellBasell and ExxonMobil together committed more than USD 245 million to advanced-recycling plants in Germany and Texas that will yield virgin-grade polymers from post-consumer waste. These projects address mechanical-recycling limits, producing feedstock suitable for food-grade applications with 100% recycled content. Early movers negotiate preferential resin supply at 10–15% discounts versus prime material and secure long-term brand contracts. Clustering near petrochemical hubs reduces feedstock logistics costs, reinforcing regional production advantages.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global single-use plastic bans and taxes | –0.7% | Global, varying intensity by region | Medium term (2-4 years) |

| Volatile petro-feedstock prices | –0.5% | Global, cost-sensitive markets most exposed | Short term (≤ 2 years) |

| Brand owners pivoting to paper-based flexibles | –0.3% | Developed markets, consumer goods focus | Medium term (2-4 years) |

| Refill/reuse models cannibalising volume growth | –0.2% | EU & North America urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Single-Use Plastic Bans and Taxes

California’s bag prohibitions, the UK’s wet-wipe ban, and South Australia’s EPS restrictions remove entire product categories virtually overnight. Enforcement includes import restrictions and stiff fines, driving emergency reformulations and CapEx outlays. Academic work on Ghana’s proposed bag bans estimates weekly tax-revenue losses of USD 0.34 million, underscoring broader economic spillovers. Multinationals grapple with divergent definitions of “single-use” across jurisdictions, complicating global SKU harmonization. As legislators widen scope beyond obvious disposable items, additional volume risks emerge for food-service and secondary-packaging formats.

Volatile Petro-Feedstock Prices

Polyethylene and polypropylene contract prices spiked 4–5 cents/lb in early 2025 amid geopolitical tension and refinery outages. US converters with fixed-price contracts absorbed margin erosion, while spot buyers deferred purchases, exacerbating volatility. Proposed 15% tariffs on Middle-Eastern feedstocks could inflate US resin costs by 12–20%, propelling substitution into recycled grades where quality allows. Smaller converters lacking hedging or captive resin supply face working-capital strains, hastening industry consolidation.

Segment Analysis

By Packaging Type: Flexible Dominance Accelerates

Flexible formats commanded 54.10% of 2025 sales and are forecast to grow at 4.41% annually through 2031, expanding the plastic packaging market far faster than rigid alternatives. Fuel cost inflation and dimensional-weight freight tariffs reinforce a structural migration toward pouches, mailers, and wrap films that cut outbound logistics charges. Films and wraps gain further traction as converters deploy mono-material options that satisfy EPR frameworks without compromising shelf life. Rigid bottles, jars, and trays retain indispensability where structure or premium shelf presence is paramount, yet their share gradually declines as resealable zippers, spouts, and stand-up formats erode historical feature advantages. Integrated suppliers offering both formats secure higher wallet share as brand owners streamline vendor bases.

Rigid-package sub-segments confront margin pressure when resin spikes outpace pass-through ability, whereas flexible peers mitigate exposure through lighter gram-weight per unit. Glass and metal replacements remain niche, limited to beverages and canned foods. Tray makers preserve relevance in food-service channels where oven-safe or microwave-ready features command price premium. Overall, flexibles’ dual leadership in volume and growth cements their central role in driving the plastic packaging market over the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Polypropylene Gains on Performance

Although polyethylene held 41.85% plastic packaging market share in 2025, polypropylene’s superior 5.55% CAGR positions it as the fastest-advancing resin family. PP’s higher heat resistance, improved clarity, and better seal integrity facilitate mono-material solutions that meet recyclability mandates while safeguarding food safety. PET protects its beverage stronghold owing to established bottle-to-bottle recycling loops, yet mechanical-recycling limitations cap recycled content without costly chemical-recycling capacity additions. PVC, polystyrene, and other styrenics retreat under stricter environmental rules and brand-owner deselection, opening space for bio-based and specialty co-polymer niches.

Chemical-recycling economics further favor resins with stable depolymerization pathways; hence PET and PP attract greater capex, while PS and PVC projects struggle to clear investment hurdles. Resin suppliers differentiate through application engineering teams that guide converters during material transitions, a service highly prized amid evolving EPR frameworks and FDA food-contact rules.

By End-User Industry: Healthcare Leads Growth

Food retained a dominant 28.10% share of the plastic packaging market size in 2025, yet healthcare and pharmaceuticals dominate growth charts with a 6.29% CAGR through 2031. Aging populations, rising chronic-disease drug regimens, and biotech cold-chain requirements elevate demand for blister packs, IV bags, and prefilled syringes with stringent sterility and barrier specifications. Regulatory-approval cycles lock in incumbent materials and vendors, enabling premium pricing that offsets resin inflation. Beverage packaging follows food in volume but secures margin uplift via specialty closures and on-the-go formats. Cosmetics and personal-care hold steady as premiumization allows pass-through of higher material costs.

Industrial users such as electronics and automotive represent niche value pools where electrostatic and chemical-resistance properties justify specialized resin blends. Across sectors, value creation shifts from volume to technical performance, favoring suppliers with deep application knowledge and regulatory affairs support.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Direct Sales Maintain Control

Direct contracts between resin producers or large converters and brand owners constituted 64.70% of 2025 turnover. Complex regulatory, barrier, and recyclability requirements necessitate tight collaboration on pack design and resin selection, reinforcing direct engagement. Distributors, however, grow faster at 4.64% CAGR by aggregating demand from SME converters and servicing emerging markets where manufacturers lack in-country presence. Digital platforms blur channel lines, enabling manufacturers to reach small buyers online while outsourcing fulfillment.

Omnichannel approaches gain favor as consolidated suppliers rationalize sales resources post-merger, increasingly leaning on distributors for geographic reach. Technical service remains direct-sales’ differentiator, particularly for pharmaceutical and food safety-critical accounts. Distributors, in response, invest in application-development centers to avoid commoditization.

Geography Analysis

Asia-Pacific controlled 40.80% of global revenue in 2025 and is expanding at 6.78% CAGR, making it the undisputed engine of plastic packaging market growth. China accounts for the lion’s share, though stricter waste-import rules and carbon-neutrality pledges compel local producers to invest in recycling capacity. India, Vietnam, and Indonesia record double-digit volume gains as organized retail and e-commerce penetration deepens. Currency volatility and geopolitics prompt multinational brand owners to diversify sourcing into ASEAN nations, reducing overreliance on any single country.

North America manifests steady mid-single-digit expansion underpinned by pharmaceutical demand, fresh-produce logistics, and the build-out of advanced-recycling hubs. State-level plastic-waste legislation adds complexity, yet it simultaneously opens opportunities for recycled and mono-material innovators. Canada’s forthcoming nationwide EPR framework accelerates shift toward recyclable packs, encouraging cross-border partnerships.

Europe, the epicenter of EPR and tethered-cap mandates, experiences modest value growth but exerts outsized influence on global design standards. High labor and energy costs incentivize process automation and resin lightweighting, while regulators push recycled-content thresholds that drive chemical-recycling investments. Eastern European converters attract reshoring projects as brands seek regional proximity without Western Europe’s cost base, spurring capital inflows into Poland and Hungary.

Latin America and the Middle East & Africa trail in share but register pockets of rapid expansion. Brazil benefits from agrifood exports that require barrier packaging, whereas GCC nations leverage petrochemical integration to export competitively priced resin. African markets begin to legislate single-use bans, creating fertile terrain for flexible producers that can deliver low-gram-weight, high-barrier solutions at affordable price points.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Industry concentration edges upward as scale economies in R&D and recycling elevate barriers to entry. Amcor’s USD 8.43 billion acquisition of Berry Global created the world’s largest diversified converter, targeting USD 650 million in annual synergy by integrating extrusion, lamination, and printing assets. The combined entity channels expanded cash flow into mono-material film R&D and global healthcare-packaging capacity, strengthening negotiating leverage with resin suppliers.

Technology arms races extend beyond converters. Resin producers accelerate investments in pyrolysis and depolymerization plants to secure closed-loop feedstock and lock in strategic customers. Patent filings for barrier-coating chemistries and compatibilizer additives grew 40% in 2024, reflecting intensified intellectual-property battles. Integrated players able to internalize both resin and converting operations capture margin at multiple value-chain nodes, while smaller converters without proprietary formulations face commoditization.

Bio-based start-ups and chemical-recycling specialists attract venture funding but confront commercialization hurdles such as feedstock aggregation and scale economics. Partnership models emerge, with large converters taking equity stakes in disruptive recyclers to guarantee offtake. Equipment suppliers like Husky Technologies and Sidel embed tethered-cap tooling capabilities into new mold platforms, creating switching costs for converters considering alternative OEMs. Overall, competitive advantage pivots on the ability to provide turnkey solutions that satisfy regulatory, sustainability, and performance requirements.

Global Plastic Packaging Industry Leaders

Mondi plc

Huhtamaki Oyj

Amcor plc

Sealed Air Corporation

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Amcor completed its USD 8.43 billion merger with Berry Global, aiming for USD 650 million in annual synergies.

- November 2024: ExxonMobil announced a USD 200 million expansion of advanced-recycling capacity at its Baytown and Beaumont sites targeting 1 billion lb annual output by 2027.

- October 2024: Klöckner Pentaplast introduced recyclable barrier flow-wrap films with 95% single-material content.

- October 2024: Accredo Packaging unveiled a 100% bio-based resin pouch derived from sugarcane for food applications.

Global Plastic Packaging Market Report Scope

The plastic packaging market is segmented into rigid plastic packaging (by material type [polyethylene (PE), polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS) and expanded polystyrene (EPS), polyvinyl chloride (PVC), and other material types), product (bottles and jars, trays and containers, and other products], end-user industry [food, beverage, healthcare, cosmetics and personal care, and other end-user industries] and geography (North America {Material, End User- Industry, Countries[United States, Canada]}, Europe {Material, End User- Industry, Countries [United Kingdom, Germany, France, Italy, Spain, Rest of Europe]}, Asia-Pacific {Material, End User- Industry, Countries[China, India, Japan, Australia and New Zealand, Rest of Asia-Pacific]}, Latin America {Material, End User- Industry, Countries [Brazil, Argentina, Mexico, Rest of Latin America]}, and Middle East and Africa {Material, End User- Industry, Countries [United Arab Emirates, South Africa, Saudi Arabia, Egypt, Rest of Middle East and Africa]}). It is also segmented into flexible plastic packaging (by material type [polyethylene (PE), bi-orientated polypropylene (BOPP), cast polypropylene (CPP), polyvinyl chloride (PVC), ethylene vinyl alcohol (EVOH), and other material types], product type [pouches, bags, films and wraps, and other product types], end-user industry [food, beverage, cosmetics and personal care, healthcare, and other end-user industry] and geography (North America {Material, End User- Industry, Countries [United States, Canada]}, Europe {Material, End User- Industry, Countries[United Kingdom, Germany, France, Italy, Spain, Rest of Europe], Asia-Pacific {Material, End User- Industry, Countries[China, India, Japan, Australia and New Zealand, Rest of Asia-Pacific]}, Latin America {Material, End User- Industry, Countries [Brazil, Argentina, Mexico, Rest of Latin America]}, and Middle East and Africa{Material, End User- Industry, Countries[United Arab Emirates, South Africa, Saudi Arabia, Egypt, Rest of Middle East and Africa]}. The Industry size and market forecasts are provided in terms of volume (tonnes) for all the above-mentioned segments.

By Packaging Type

| Rigid Packaging Type | Bottles and Jars |

| Caps and Closures | |

| Trays and Containers | |

| Other Product Types | |

| Flexible Packaging Type | Pouches and Bags |

| Films and Wraps | |

| Other Product Types |

By Material

| Polyethylene (HDPE, LDPE, LLDPE) |

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP) |

| Polystyrene and EPS |

| Polyvinyl Chloride (PVC) |

| Others (EVOH, Bioplastics, etc.) |

By End-user Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Cosmetics and Personal Care |

| Other End-user Industry |

By Distribution Channel

| Direct Sales |

| Indirect Sales |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Packaging Type | Rigid Packaging Type | Bottles and Jars | |

| Caps and Closures | |||

| Trays and Containers | |||

| Other Product Types | |||

| Flexible Packaging Type | Pouches and Bags | ||

| Films and Wraps | |||

| Other Product Types | |||

| By Material | Polyethylene (HDPE, LDPE, LLDPE) | ||

| Polyethylene Terephthalate (PET) | |||

| Polypropylene (PP) | |||

| Polystyrene and EPS | |||

| Polyvinyl Chloride (PVC) | |||

| Others (EVOH, Bioplastics, etc.) | |||

| By End-user Industry | Food | ||

| Beverage | |||

| Healthcare and Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| Other End-user Industry | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the plastic packaging market?

The market is valued at USD 509.4 billion in 2026 and is forecast to reach USD 597.43 billion by 2031.

Which segment is growing fastest within the plastic packaging market?

Flexible packaging is expanding at a 4.41% CAGR, leading growth among all packaging-type segments through 2031.

Why is polypropylene gaining share against polyethylene?

Polypropylene offers better heat resistance, clarity, and barrier properties, enabling mono-material solutions that comply with strict recyclability mandates.

How are regulations influencing packaging design in Europe?

EU rules on tethered caps and EPR recycling targets push manufacturers toward specialty closures and mono-material films that meet recyclability thresholds.

What role does chemical recycling play in future supply chains?

Chemical recycling produces virgin-quality polymer from post-consumer waste, unlocking 100% recycled-content packs for food and healthcare applications and lowering resin procurement costs for early adopters.