| Study Period | 2019 - 2030 |

| Market Volume (2025) | 4.69 Million tons |

| Market Volume (2030) | 5.71 Million tons |

| CAGR | 4.00 % |

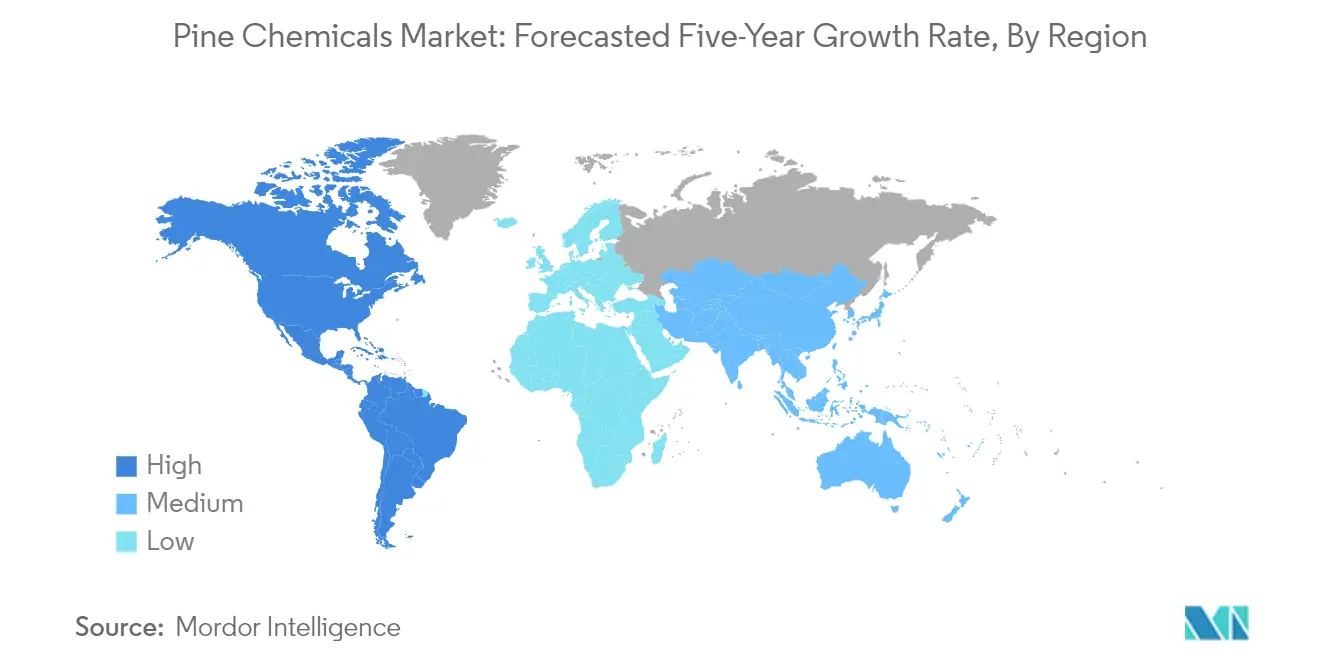

| Fastest Growing Market | North America |

| Largest Market | Europe |

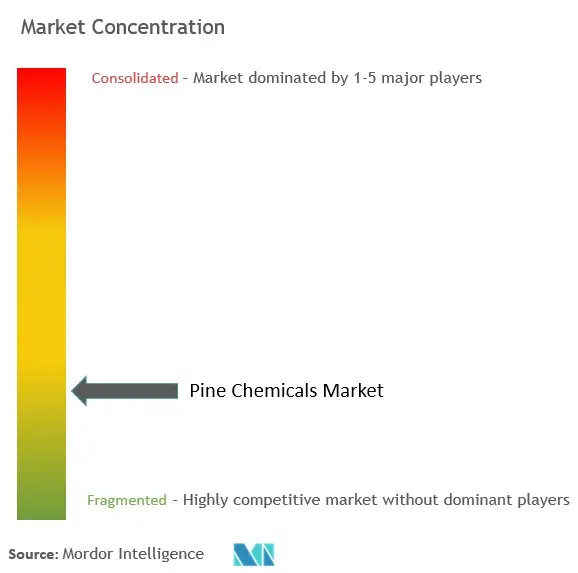

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Pine Chemicals Market Analysis

The Pine Chemicals Market size is estimated at 4.69 million tons in 2025, and is expected to reach 5.71 million tons by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The pine chemicals industry is experiencing significant transformation through strategic consolidation and partnerships, as companies seek to strengthen their market positions and expand their product portfolios. This trend is exemplified by several major transactions in recent years, including Synthomer Plc's acquisition of Eastman Chemical's adhesive resins business for USD 1 billion in December 2021, and the landmark acquisition of Kraton Corporation by DL Chemical Co. Ltd. for approximately USD 2.5 billion in September 2021. These strategic moves are reshaping the competitive landscape and driving innovation in sustainable chemical solutions.

The industry is witnessing a pronounced shift towards sustainable and bio-based alternatives, particularly in response to stringent environmental regulations and changing consumer preferences. This transition is particularly evident in the biofuels sector, where production capacity has expanded significantly. In the United States alone, biofuel plant production capacity reached 21 billion gallons per year in early 2021, with biodiesel production capacity reaching 2,244 million gallons per year by December 2021. This growth in bio-based applications is creating new opportunities for pine-derived chemicals across various end-use sectors.

End-user industries are increasingly adopting pine chemicals in their manufacturing processes, driven by the growing emphasis on environmental sustainability and performance requirements. The synthetic rubber industry, for instance, has shown remarkable growth, with China's production reaching 8,117 kilotons in 2021, representing a 9.1% increase compared to the previous year. This growth in end-user industries is creating new applications for pine chemicals, particularly in adhesives, coatings, and rubber processing.

Supply chain optimization and production efficiency have become critical focus areas for industry participants, leading to increased investments in technology and infrastructure. Companies are establishing strategic partnerships to enhance their distribution networks, as evidenced by DRT's new distribution partnership with IMCD Italy in November 2021 to market its products across industrial segments. These developments are strengthening the industry's ability to meet growing demand while maintaining cost competitiveness and ensuring reliable supply to customers across various regions. The role of the Pine Chemicals Association in promoting industry standards and practices is also noteworthy in this context.

Pine Chemicals Market Trends

Increasing Demand for Pine Chemicals in Mining and Flotation Chemicals and Lubricants

Mining chemicals play an instrumental role in mineral ore processing, with pine chemicals, particularly tall oil fatty acids (TOFA), emerging as crucial collector chemicals in mining operations. These derivatives are extensively utilized as frothing agents in the flotation process for reclaiming low-grade copper, lead, and zinc-bearing ores, offering enhanced recovery and selectivity in the beneficiation of phosphate, fluorspar, and copper ores. The growing mining activities globally, coupled with increasing investments in infrastructure development, have significantly boosted the demand for these specialty chemicals. For instance, OleoFlot, a major brand of industrial oleochemical products comprising tall oil fatty acids, has gained substantial traction as a mining chemical due to its superior performance characteristics.

The lubricants sector represents another significant growth driver for pine chemicals, particularly in the development of bio-based and sustainable solutions. Tall oil fatty acids are increasingly being employed as base materials for lubricating greases, providing excellent anti-corrosive and lubricity properties. The demand for high-performance greases in wind energy turbines and environmentally friendly hydraulic fluids for heavy-duty equipment machinery has witnessed substantial growth, driven by global carbon-neutrality initiatives. Additionally, cutting fluids formulated with pine chemical derivatives are gaining prominence in metalworking operations, where they serve as effective emulsifiers in aqueous emulsions of lubricating oils and additives, demonstrating superior performance in boundary lubrication needs and enhanced hard-water tolerance compared to traditional fatty acids.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Demand from the Flavors and Fragrances Industry

Pine oleoresin has emerged as a significant source of valuable terpenes, with its two major fractions - turpentine (volatile fraction) and rosin (solid fraction) - finding extensive applications in the flavors and fragrances industry. Turpentine, obtained through steam distillation or extraction of pine stumps, serves as a versatile raw material for chemical isolates used in producing a wide range of products, including synthetic pine oil, which represents the largest single turpentine derivative in the flavors and fragrances sector. The applications span across multiple industries, including confectionery, dairy products, bakery and processed foods, the feed industry, pharmaceutical products, and oral care products, demonstrating the versatility and growing importance of pine-derived chemicals.

The industry's increasing focus on sustainability has positioned pine-derived chemicals as a crucial raw material source for the flavors and fragrances sector. These chemicals can be converted into various valuable compounds such as camphor, citral, linalool, and menthol, which are essential components in fragrance formulation and food additives. The hydrogenation and pyrolysis of turpentine produce multiple derivatives including terpinyl dihydroacetate, geraniol, ocimene, myrcene, and dihydroterpineol, all of which are vital ingredients in fragrance formulation. Furthermore, the growing consumer preference for natural and sustainable ingredients has led to increased adoption of pine chemicals in personal care products, household cleaners, air fresheners, and fine fragrances, establishing them as indispensable components in modern fragrance development.

Segment Analysis: Product Type

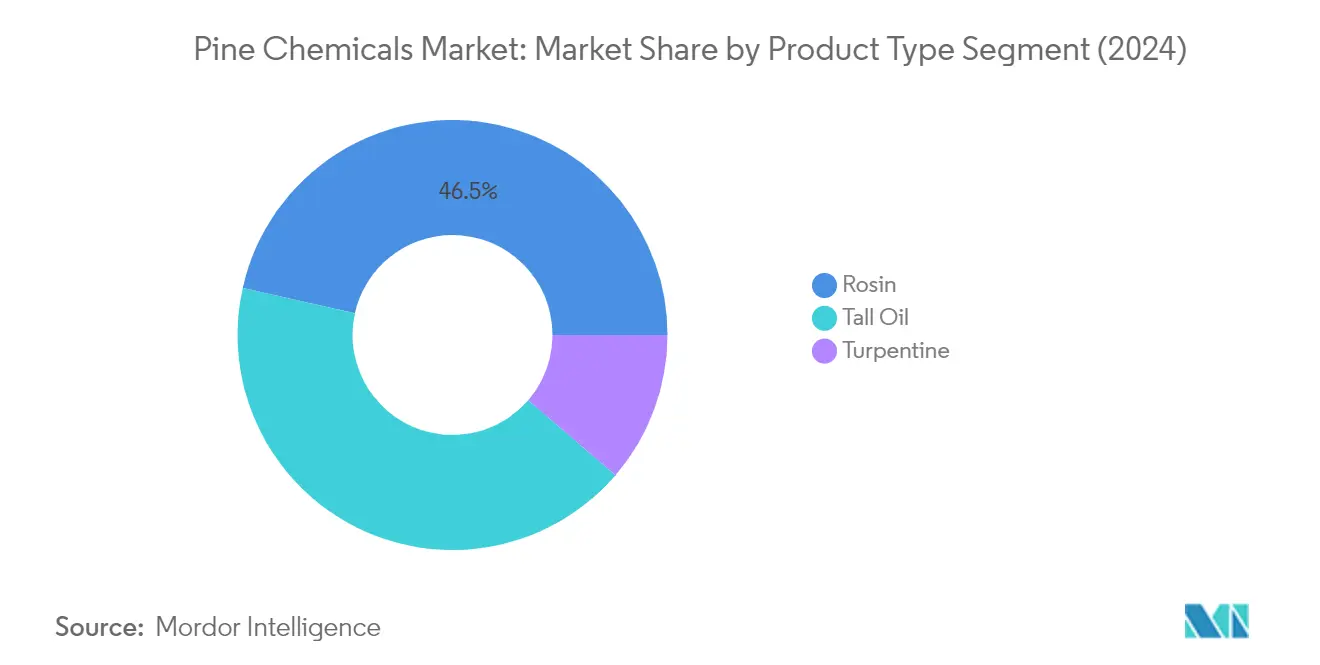

Rosin Segment in Pine Chemicals Market

The rosin segment dominates the pine chemicals market, accounting for approximately 47% of the total market volume in 2024. Rosin, which includes tall oil rosin, gum rosin, and wood rosin, serves as a critical component in various applications, including adhesives, printing inks, paper sizing, and rubber processing. The segment's leadership position is primarily driven by its extensive use in the manufacturing of adhesives and sealants, where it functions as an excellent tackifier. Additionally, the segment is experiencing the fastest growth trajectory in the market, supported by increasing demand from emerging applications in packaging, construction adhesives, and road marking materials. The growing adoption of bio-based chemicals across industries and the shift towards sustainable raw materials, particularly in developing economies, has further strengthened rosin's market position.

Remaining Segments in Product Type

The tall oil and turpentine segments complete the pine chemicals market landscape, each serving distinct industrial applications. Tall oil derivatives, including crude tall oil (CTO), tall oil fatty acid (TOFA), distilled tall oil (DTO), and tall oil pitch (TOP), are extensively utilized in lubricants, mining chemicals, and biofuels. The segment's growth is supported by increasing demand for bio-based alternatives in industrial applications. The turpentine segment, comprising gum/wood turpentine, crude sulphate turpentine, and other variants, plays a crucial role in the flavors and fragrances industry, as well as in the production of resins and solvents. The segment's development is driven by the growing preference for natural and sustainable raw materials in consumer products and industrial applications.

Segment Analysis: By Application

Adhesives and Sealants Segment in Pine Chemicals Market

The adhesives and sealants segment dominates the pine chemicals market, accounting for approximately 23% of the total market volume in 2024. Pine chemicals have become vital components in the adhesives and sealants industry value chain, with tall oil products (TOFA, DTO) and rosin products (TOR and gum rosin) serving as excellent tackifiers. These products offer three key benefits: compatibility with various polymers providing flexibility in formulation, ability for chemical tailoring to deliver unique adhesive performance, and their derivation from natural and renewable sources. The segment's growth is primarily driven by increasing environmental concerns and the ability to tailor TOR resin according to desired properties of adhesives. Additionally, the Pine Chemicals Association (PCA) actively seeks collaboration opportunities with the adhesives and sealants industry, particularly focusing on food and packaging safety requirements worldwide.

Remaining Segments in Pine Chemicals Market by Application

The pine chemicals market encompasses several other significant application segments, including coatings, printing inks, lubricants, biofuels, paper sizing, rubber, and soaps and detergents. The coatings segment represents the second-largest application, where TOFAs and TORs are widely used as drying agents and for improving properties of paints, varnishes, and coatings. The printing inks segment utilizes pine chemicals extensively for producing various types of inks, while the lubricants segment benefits from pine chemicals' excellent lubricity and anti-corrosive properties. Biofuels represent an emerging application area, particularly in regions with strong environmental regulations. Paper sizing applications leverage pine chemicals for their excellent sizing properties, while the rubber industry uses pine tar and modified tall oil pitch as softeners and plasticizers. The soaps and detergents segment utilizes pine chemicals for their dual-purpose functionality in both cleaning and disinfecting applications.

Pine Chemicals Market Geography Segment Analysis

Pine Chemicals Market in Asia-Pacific

The Asia-Pacific region represents a diverse and dynamic pine chemicals market, with Japan leading regional consumption, followed by China, ASEAN countries, India, and South Korea. The region's growth is primarily driven by increasing industrial activities, rapid urbanization, and growing environmental awareness, leading to higher adoption of pine chemicals. The automotive, construction, and packaging industries serve as major end-users, while the expanding manufacturing sector continues to create new opportunities for market growth.

Pine Chemicals Market in Japan

Japan dominates the Asia-Pacific pine chemicals market, leveraging its advanced manufacturing capabilities and strong presence in key end-use industries. The country holds approximately 38% of the regional market share, supported by its robust automotive sector, sophisticated packaging industry, and significant investments in sustainable technologies. Japan's market leadership is further strengthened by the presence of major manufacturers and continuous technological advancements in pine chemical applications, particularly in the adhesives, coatings, and printing inks sectors.

Pine Chemicals Market in China

China emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 5% during 2024-2029. The country's rapid industrial expansion, particularly in the construction and automotive sectors, drives this growth. China's commitment to environmental sustainability and increasing focus on bio-based materials has created favorable conditions for pine chemicals market expansion. The country's robust manufacturing infrastructure and growing emphasis on domestic production capabilities further support this growth trajectory.

Pine Chemicals Market in North America

North America represents a mature and well-established pine chemicals market, with the United States, Canada, and Mexico as key contributors. The region benefits from abundant raw material resources, advanced manufacturing capabilities, and a strong presence of major industry players. The market is characterized by high technological adoption, stringent environmental regulations promoting bio-based materials, and significant research and development activities in sustainable chemical solutions.

Pine Chemicals Market in United States

The United States maintains its position as the dominant force in North America's pine chemicals market, commanding approximately 74% of the regional market share. The country's leadership is supported by its extensive forest resources, advanced manufacturing infrastructure, and strong presence in key end-use industries such as adhesives, paints, and coatings. The robust domestic demand, coupled with significant export capabilities, reinforces the United States' position as the regional market leader.

Pine Chemicals Market in Mexico

Mexico demonstrates strong growth potential in the North American pine chemicals market, with an expected growth rate of approximately 5% during 2024-2029. The country's expanding manufacturing sector, particularly in the automotive and construction industries, drives this growth. Mexico's strategic geographical location, improving infrastructure, and increasing focus on sustainable materials contribute to its emergence as a high-growth market in the region.

Pine Chemicals Market in Europe

Europe maintains a significant presence in the global pine chemicals market, with Germany, France, the United Kingdom, and Italy as key markets. The region's strong focus on environmental sustainability, circular economy initiatives, and strict regulations regarding chemical usage shapes market dynamics. The presence of established manufacturers, advanced research facilities, and growing emphasis on bio-based materials characterizes the European market landscape.

Pine Chemicals Market in Germany

Germany leads the European pine chemicals market, driven by its robust industrial base, particularly in the automotive, construction, and chemical sectors. The country's leadership in sustainable technologies and strong manufacturing capabilities supports its position as the regional market leader. Germany's commitment to environmental protection and circular economy principles further strengthens its market position.

Pine Chemicals Market in Italy

Italy demonstrates strong market potential in Europe's pine chemicals sector, supported by its growing industrial base and increasing focus on sustainable materials. The country's well-established manufacturing sector, particularly in adhesives and coatings, drives market growth. Italy's strategic focus on environmental sustainability and growing adoption of bio-based materials in various industries contributes to its market development.

Pine Chemicals Market in South America

The South American pine chemicals market, primarily led by Brazil and Argentina, shows promising growth potential despite economic challenges. Brazil emerges as both the largest and fastest-growing market in the region, supported by its extensive forest resources and growing industrial base. The region's market development is driven by increasing environmental awareness, growing demand from end-use industries, and government initiatives promoting sustainable materials.

Pine Chemicals Market in Middle East & Africa

The Middle East & Africa region represents an emerging pine chemicals market, with Saudi Arabia and South Africa as key markets. Saudi Arabia leads the regional market in terms of size, while South Africa shows the fastest growth potential. The region's market development is driven by increasing industrialization, growing construction activities, and rising awareness about sustainable materials. The expanding manufacturing sector and government initiatives supporting industrial diversification contribute to market growth.

Get Analysis on Important Geographic Markets

Download PDF

Pine Chemicals Industry Overview

Top Companies in Pine Chemicals Market

The pine chemicals market is characterized by continuous innovation and strategic developments among major players. Companies are increasingly focusing on developing bio-based and environmentally sustainable products, particularly in response to growing environmental regulations and consumer preferences. Operational agility is demonstrated through the establishment of robust supply chain networks and long-term agreements with raw material suppliers, particularly kraft pulp mills. Strategic moves in the industry are centered around expanding product portfolios through acquisitions and partnerships, as evidenced by significant deals like DL Chemical's acquisition of Kraton Corporation and Synthomer's acquisition of Eastman's adhesive resins business. Geographic expansion remains a key focus, with companies establishing distribution partnerships to penetrate new markets and strengthen their presence in existing ones.

Fragmented Market with Strong Regional Players

The global pine chemicals market exhibits a partially fragmented structure, with the top five to six players holding a significant market share while numerous regional manufacturers compete intensely for the remaining portion. Major global players like Kraton Corporation, Ingevity Corporation, and DRT have established themselves through extensive product portfolios, technological innovation, and strong distribution networks. These companies typically operate integrated facilities and maintain strategic relationships with raw material suppliers, giving them a competitive advantage in terms of supply chain security and cost efficiency.

The market is witnessing increased consolidation through mergers and acquisitions, particularly as companies seek to strengthen their market position and expand their product offerings. This trend is evident in recent strategic moves by major players to acquire complementary businesses and technologies. Regional players, particularly in Asia-Pacific, are gaining prominence by offering competitive pricing and focusing on local market needs, while established players are responding through strategic partnerships and localized production facilities to maintain their market share.

Innovation and Sustainability Drive Future Success

Success in the pine chemicals industry increasingly depends on companies' ability to develop sustainable products and maintain reliable raw material supply chains. Incumbent players must focus on research and development to create innovative applications and improve production efficiency, while also strengthening their relationships with kraft pulp mills to ensure consistent raw material supply. Environmental regulations and growing customer preference for bio-based products are reshaping the competitive landscape, making sustainability initiatives and eco-friendly product development crucial for maintaining market position.

For new entrants and smaller players, success lies in identifying and serving niche market segments while building strong distribution networks. The ability to offer competitive pricing while maintaining product quality is crucial, particularly in regions with high price sensitivity. Companies must also consider the impact of potential regulatory changes, particularly regarding the use of crude tall oil in biofuels, and develop strategies to address these challenges. Building strong relationships with end-users and offering technical support services can help companies differentiate themselves in this competitive market, while also helping to mitigate the risk of substitution from petroleum-based alternatives. The role of the Pine Chemicals Association is pivotal in guiding industry standards and promoting sustainable practices.

Pine Chemicals Market Leaders

-

KRATON CORPORATION

-

Ingevity Corporation

-

Harima Chemicals Group, Inc.

-

Pine Chemical Group

-

DRT

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Pine Chemicals Market News

- March 2024: Brazilian pine chemicals group agrees to take over Pinopine, Portugal, gum rosin derivatives manufacturer. Grupo Resinas brasil (RB), one of the largest Brazilian pine chemicals producers, takes the majority share in derivatives producer Pinopine, located in Portugal.

- September 2023: DRT (Les Dérives Résiniques Et Terpéniques) invested in the construction of its production facility at the Vielle-Saint-Girons site in France. This plant will produce hydrogenated rosin and resin derivatives and is expected to be completed in mid-2024.

- June 2022: DRT (Les Dérives Résiniques Et Terpéniques) launched DERTOPHALT. It is a plant-based binder obtained by distilling pulp and paper industry co-products. It is composed of rosin and fatty acids and is 100% natural.

Pine Chemicals Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Demand for Pine Chemicals in Mining and Flotation Chemicals and Lubricants

- 4.1.2 Increasing Demand from the Flavors and Fragrances Industry

-

4.2 Restraints

- 4.2.1 Diversion of CTO to Biofuels due to Government Incentives

- 4.2.2 Increase in the Availability of Cheaper Substitutes

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Threat of New Entrants

- 4.4.3 Threat of Substitute Products and Services

- 4.4.4 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 Product Type

- 5.1.1 Tall Oil

- 5.1.1.1 Crude Tall Oil (CTO)

- 5.1.1.2 Tall Oil Fatty Acid (TOFA)

- 5.1.1.3 Distilled Tall Oil (DTO)

- 5.1.1.4 Tall Oil Pitch (TOP)

- 5.1.2 Rosin

- 5.1.2.1 Tall Oil Rosin

- 5.1.2.2 Gum Rosin

- 5.1.2.3 Wood Rosin

- 5.1.3 Turpentine

- 5.1.3.1 Gum/Wood Turpentine

- 5.1.3.2 Crude Sulphate Turpentine

- 5.1.3.3 Other Turpentines

- 5.1.4 Application

- 5.1.4.1 Adhesives and Sealants

- 5.1.4.2 Coatings

- 5.1.4.3 Printing Inks

- 5.1.4.4 Lubricants and Lubricity Additives

- 5.1.4.5 Biofuels

- 5.1.4.6 Paper Sizing

- 5.1.4.7 Rubber

- 5.1.4.8 Soaps and Detergents

- 5.1.4.9 Other Applications (Oil Field Chemicals, Chemical additives, Chewing Gums, and Food Additives)

-

5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles(Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 Arakawa Chemical Industries Ltd

- 6.4.2 DRT (Dérivés Résiniques et Terpéniques)

- 6.4.3 Forchem Oyj

- 6.4.4 Harima Chemicals Group Inc.

- 6.4.5 Ingevity Corporation

- 6.4.6 Kraton Corporation

- 6.4.7 Mercer International

- 6.4.8 OOO Torgoviy Dom Lesokhimik

- 6.4.9 Pine Chemical Group

- 6.4.10 Respol Resinas SA

- 6.4.11 Sunpine AB

- 6.4.12 Synthomer Plc.

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications of Pine Chemicals (DTO, TOFA, CTO, TOP, and Wood Rosin)

- 7.2 Food and Packaging Safety Regulations of Adhesives and Sealants

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Pine Chemicals Industry Segmentation

Pine chemicals are a group of organic compounds derived from pine trees, primarily extracted from the resin or sap of pine species. These chemicals include rosin, tall oil, turpentine, and their derivative. They find a wide range of applications due to their adhesive, tackifying, solvency, fragrance, and other functional properties.

The pine chemicals market is segmented by product type, application, and geography. By product type, the market is segmented into tall oil, rosin, and turpentine. By application, the market is segmented into adhesives and sealants, coatings, printing inks, lubricants and lubricity additives, biofuels, paper sizing, rubber, soaps and detergents, and other applications (oil field chemicals, chemical additives, chewing gum, food additives). The report also covers the market size and forecasts for pine chemicals in 27 countries across major regions. For each segment, the market sizing and forecasts are done on the basis of volume (tons).

| Product Type | Tall Oil | Crude Tall Oil (CTO) | |

| Tall Oil Fatty Acid (TOFA) | |||

| Distilled Tall Oil (DTO) | |||

| Tall Oil Pitch (TOP) | |||

| Rosin | Tall Oil Rosin | ||

| Gum Rosin | |||

| Wood Rosin | |||

| Turpentine | Gum/Wood Turpentine | ||

| Crude Sulphate Turpentine | |||

| Other Turpentines | |||

| Application | Adhesives and Sealants | ||

| Coatings | |||

| Printing Inks | |||

| Lubricants and Lubricity Additives | |||

| Biofuels | |||

| Paper Sizing | |||

| Rubber | |||

| Soaps and Detergents | |||

| Other Applications (Oil Field Chemicals, Chemical additives, Chewing Gums, and Food Additives) | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Pine Chemicals Market Research FAQs

How big is the Pine Chemicals Market?

The Pine Chemicals Market size is expected to reach 4.69 million tons in 2025 and grow at a CAGR of greater than 4% to reach 5.71 million tons by 2030.

What is the current Pine Chemicals Market size?

In 2025, the Pine Chemicals Market size is expected to reach 4.69 million tons.

Who are the key players in Pine Chemicals Market?

KRATON CORPORATION, Ingevity Corporation, Harima Chemicals Group, Inc., Pine Chemical Group and DRT are the major companies operating in the Pine Chemicals Market.

Which is the fastest growing region in Pine Chemicals Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Pine Chemicals Market?

In 2025, the Europe accounts for the largest market share in Pine Chemicals Market.

What years does this Pine Chemicals Market cover, and what was the market size in 2024?

In 2024, the Pine Chemicals Market size was estimated at 4.50 million tons. The report covers the Pine Chemicals Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Pine Chemicals Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Pine Chemicals Market Research

Mordor Intelligence provides a comprehensive analysis of the pine chemicals market, built on decades of expertise in industrial chemical research. Our extensive coverage includes the global pine chemicals market, with a detailed examination of pine derivatives and their applications. By collaborating with the Pine Chemicals Association and industry leaders, we offer in-depth analysis of pine-derived chemicals across various sectors, from manufacturing to end-use applications. The report explores the entire value chain of pine products and their industrial applications, offering stakeholders crucial insights into market dynamics.

Our detailed market analysis benefits stakeholders across the pine chemicals industry by providing actionable intelligence and growth opportunities. The report, available as an easy-to-download PDF, includes comprehensive forecasts for the pine derived chemicals market. It places special focus on key segments like turpentine rosin and specialized pine oil applications. Stakeholders gain access to detailed regional analyses, emerging technology assessments, and strategic insights that support informed decision-making in the expanding pine market. The report's data-driven approach ensures that businesses can effectively navigate market challenges while capitalizing on growth opportunities in this dynamic sector.