Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

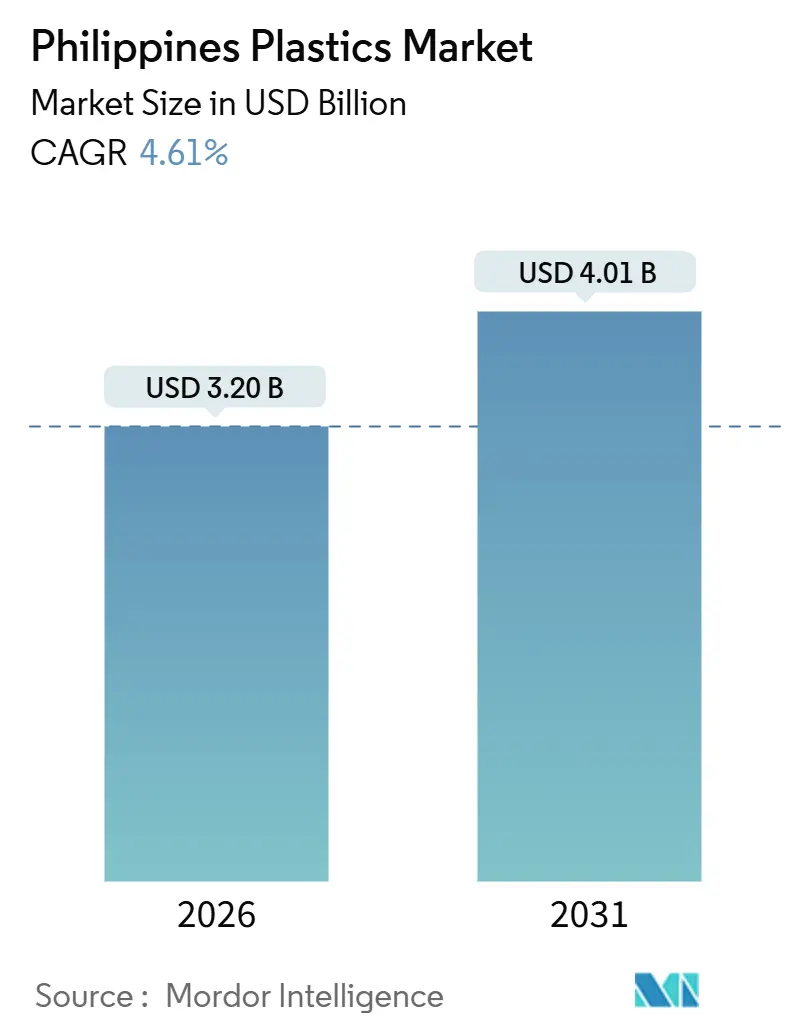

| Market Size (2026) | USD 3.20 Billion |

| Market Size (2031) | USD 4.01 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Plastics Market Analysis by Mordor Intelligence

The Philippines Plastics Market size is estimated at USD 3.20 billion in 2026, and is expected to reach USD 4.01 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031). Packaging demand linked to e-commerce growth, infrastructure‐led construction activity, and resurgent automotive wire-harness exports are combining to lift domestic resin off-take despite limited upstream capacity. Extended Producer Responsibility (EPR) targets that rise from 20% recovery in 2025 to 80% in 2028 are accelerating capital flows into recycling, particularly food-grade recycled PET and plant-fiber composites. PEZA’s 5% special corporate income tax and duty-free resin imports continue to attract compounders that balance imported feedstocks with local fillers to serve the Philippines plastics market profitably. At the same time, high electricity tariffs and patchwork single-use-plastic bans are forcing converters to adopt energy-efficient equipment and certified traceability systems to protect margins within the Philippines plastics market.

Key Report Takeaways

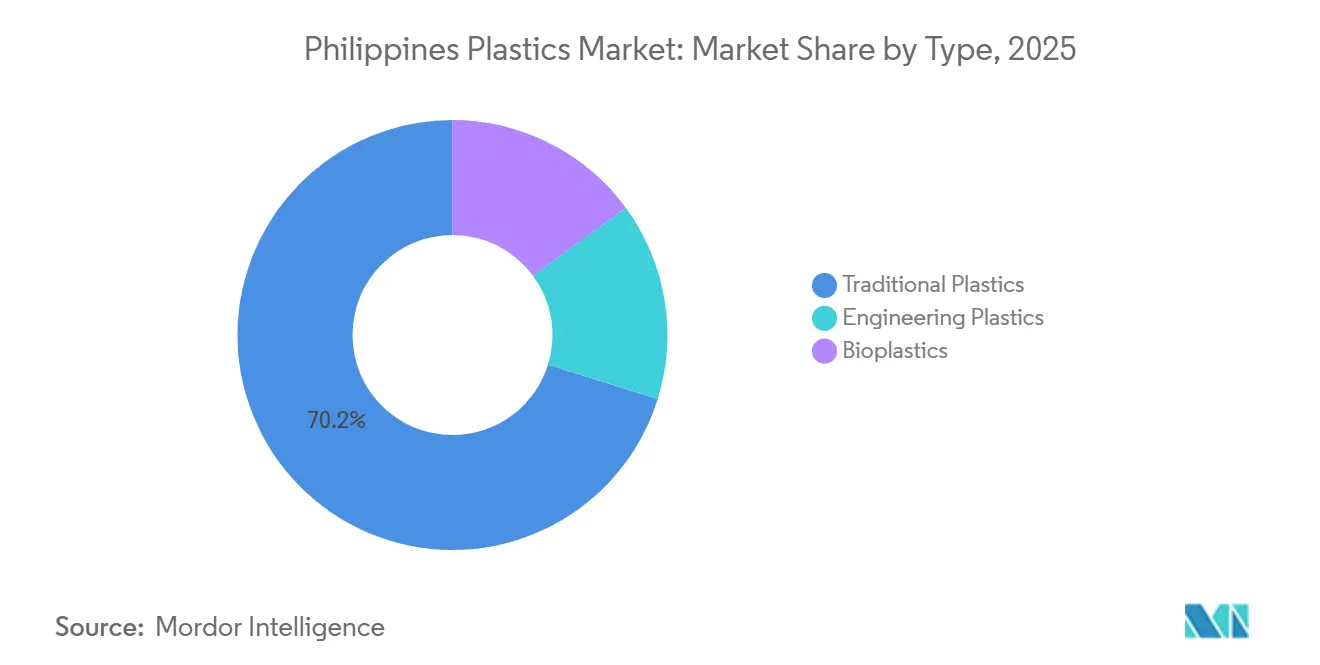

- By type, traditional plastics captured 70.18% of the Philippines plastics market share in 2025, while bioplastics are forecast to have a 5.06% CAGR through 2031.

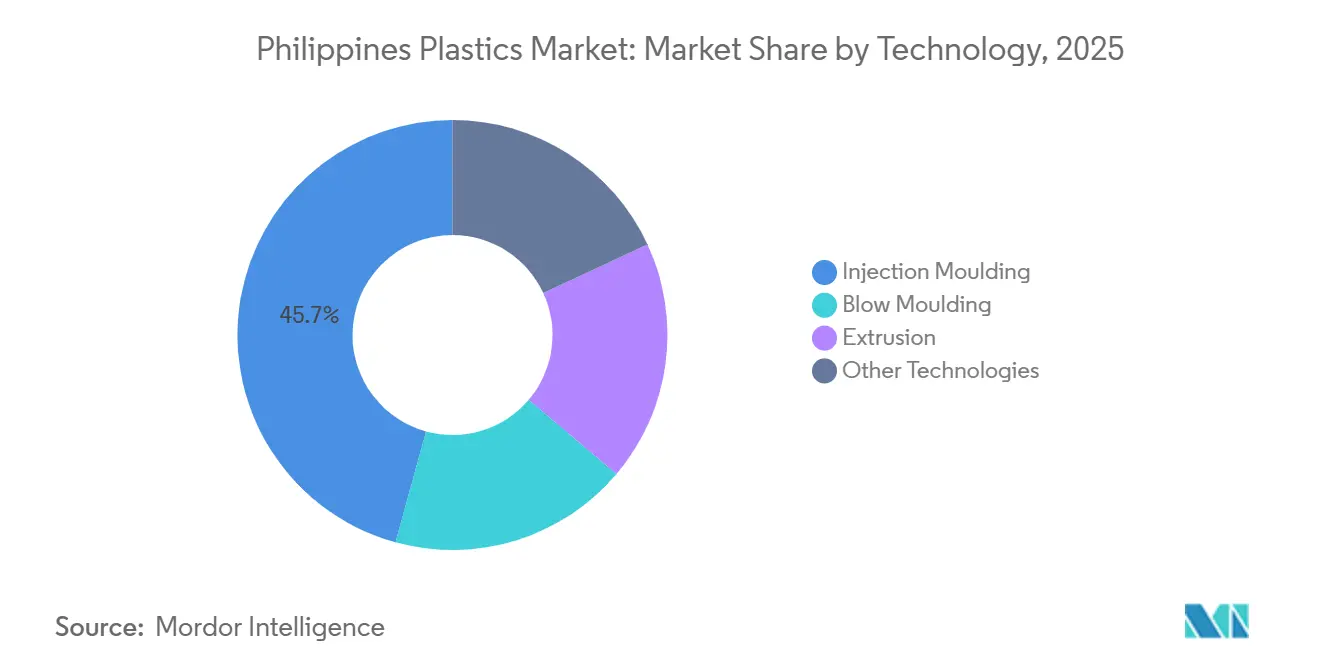

- By technology, injection molding led with 45.72% share of the Philippines plastics market size in 2025; rotational molding and thermoforming are expected to expand at a 4.97% CAGR to 2031.

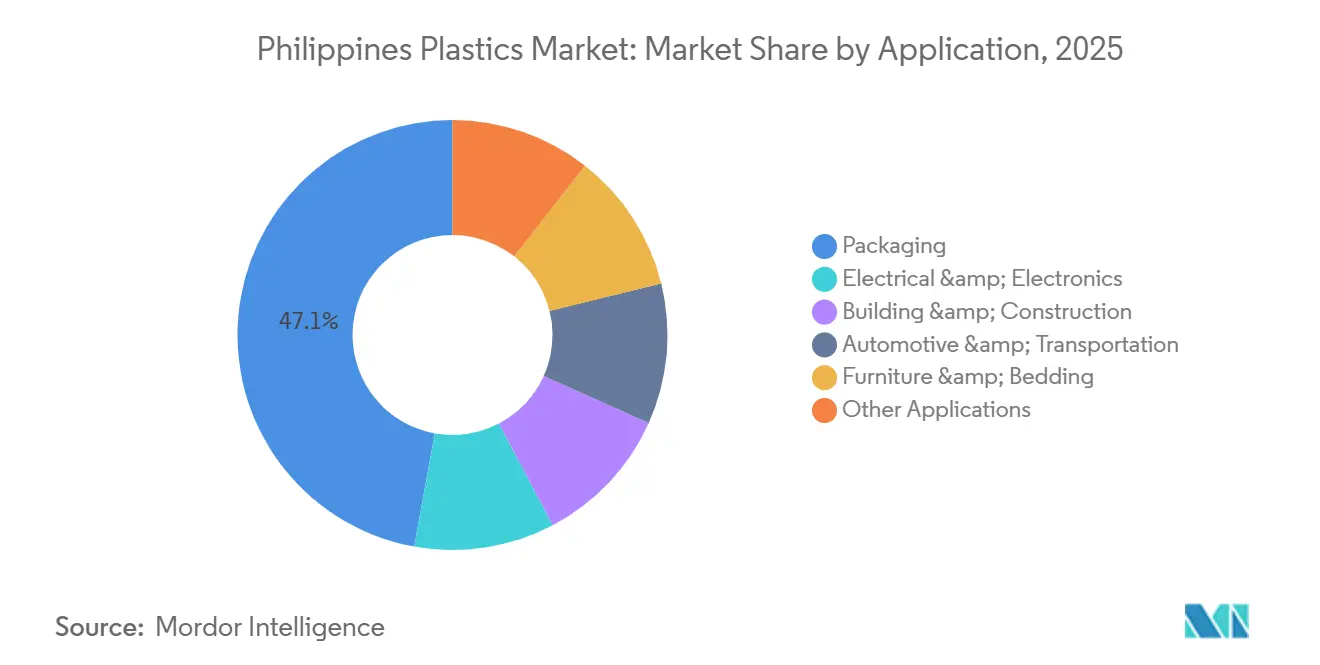

- By application, packaging accounted for 47.14% of the Philippines plastics market share in 2025, whereas automotive & transportation applications are on track for the fastest 5.19% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Plastics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging packaging & e-commerce demand | +1.2% | National, concentrated in Metro Manila, Calabarzon | Short term (≤ 2 years) |

| Government infrastructure build-out boosts construction plastics | +1.0% | National, priority corridors in Luzon, Visayas, Mindanao | Medium term (2-4 years) |

| Rising automotive wire-harness exports need engineering plastics | +0.8% | PEZA zones in Laguna, Cavite, Batangas | Medium term (2-4 years) |

| PEZA tax incentives favour local compounders | +0.6% | PEZA-registered zones nationwide | Long term (≥ 4 years) |

| Brand commitments spur PCR-grade resin demand | +0.5% | National, led by Metro Manila FMCG hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Packaging & E-commerce Demand

E-commerce penetration reached 15% in 2024 and continues to climb, pushing parcel volumes that favor light-weight, flexible films over rigid formats. Leading platforms now embed recycled-content guidelines into seller scorecards, encouraging the shift from virgin polypropylene mailers to recycled LDPE or rPET films. FMCG brands responding to EPR quotas have doubled take-back budgets for sachet and bottle collection, which increases demand for locally sourced PCR-grade pellets. As payment failures trigger repeat shipments, more bubble-wrap and corrugated liners are used per successful delivery, enlarging the overall packaging footprint that feeds directly into the Philippines plastics market. This cycle of volume growth, platform‐led sustainability, and regulatory pressure is steering converters toward certified recycled materials that command premiums yet still widen the Philippines plastics market.

Government Infrastructure Build-Out Boosts Construction Plastics

The national budget allocated PHP 1.545 trillion (USD 27.5 billion) to infrastructure in 2024, equivalent to 5.8% of GDP, channeling orders for HDPE and uPVC pipe, geotextiles, and EPS insulation into large public works. Contractors prefer corrosion-resistant plastic pipe over ductile iron to lower freight costs across the archipelago’s 7,641 islands. Climate-resilient design standards now specify UV-stabilized polypropylene geotextiles to protect flood-prone highways, nudging the replacement of sand-filled sacks with longer-lasting plastic alternatives. The Advanced Manufacturing Center recorded 79 client engagements in additive manufacturing, signaling that 3D-printed fittings and couplings could localize value within the Philippines plastics market. Sustained capital expenditure keeps construction grades at the core of domestic resin demand, underpinning stable volumes even when consumer spending softens.

Rising Automotive Wire-Harness Exports Need Engineering Plastics

Wire-harness shipments from PEZA zones to Japanese and Korean OEMs rose on contracts for EV models that demand flame-retardant nylon and PBT housings. Calamba-based Techno MoldPlas operates 29 injection machines to ±0.05 mm tolerances, validating the capability window local molders must hit to win higher-margin orders. The Comprehensive Automotive Resurgence Strategy extends fiscal credits for lightweighting, which motivates substitution of metal clips with glass-fiber-reinforced polyamide, raising the engineering share of the Philippines plastics market. EV battery enclosure prototypes using plant-fiber plastics point to incremental demand for heat-stable composites that also meet OEM carbon scoring. As volume migrates from commodity interiors to functional safety parts, domestic converters realize better yields and resilient pricing.

PEZA Tax Incentives Favor Local Compounders

Enterprises that locate inside economic zones secure a four- to seven-year income tax holiday, followed by a 5% tax on gross income in lieu of the 25% standard rate, plus duty-free equipment imports[2]Philippine Economic Zone Authority, “2025 Investment Guide,” peza.gov.ph. This structure lowers landed cost for compounded pellets by as much as 8% versus non-PEZA operations, encouraging mid-sized firms to scale blending lines and color masterbatch capacity. D&L Industries’ Batangas site exceeded its 2024 export target by 175%, demonstrating that PEZA incentives translate to global competitiveness even when utilities are expensive. Gross-income taxation minimizes disputes over transfer pricing, giving multinational suppliers the confidence to consolidate regional formulation work inside Philippine zones. Predictable taxation thus anchors investment that broadens the Philippines plastics market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on imported naphtha & polymers | -0.9% | National, acute in non-PEZA zones | Long term (≥ 4 years) |

| Single-use-plastic bans & EPR law compliance costs | -0.7% | Metro Manila, expanding to provincial cities | Medium term (2-4 years) |

| High energy & domestic logistics expenses | -0.5% | National, most severe in Visayas, Mindanao | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported Naphtha & Polymers

Plastics import value jumped 24.75% year-on-year to USD 288.57 million in January 2025, underscoring near-total reliance on foreign feedstocks[1]Philippine Statistics Authority, “Trade Performance January 2025,” psa.gov.ph. Only one local cracker—JG Summit’s Batangas complex—converts naphtha into olefins, and its 480,000-tonne ethylene output covers a fraction of domestic demand. Spot PP and PE prices track China’s export swings, so converters struggle to forecast margins and must pre-pay resin 60-90 days before collecting from FMCG buyers, tightening working capital. Currency volatility amplifies cost uncertainty because resin is invoiced in USD while most finished goods sell in PHP. These dynamics keep upstream risk a persistent drag on the Philippines plastics market.

Single-Use-Plastic Bans & EPR Law Compliance Costs

Republic Act 11898 compels 917 registered companies to recover 80% of plastic packaging by 2028 or face fines up to PHP 20 million. Local ordinances in Quezon City, Marikina, and Makati already ban common items such as straws and shopping bags, forcing converters to retool lines toward compostable or mono-material alternatives that cost 20%-40% more. Annual third-party audits inflate overhead, and EPR credits must be secured in advance or offset through co-processing contracts, adding complexity for small manufacturers. If House Bill 6470 passes, nationwide harmonization will remove patchwork rules but raise the baseline compliance load, squeezing operators with limited capex. Compliance investments are therefore a near-term restraint on the Philippines plastics market, although recyclers able to certify traceability will gain pricing power.

Segment Analysis

By Type: Fiber Blends Challenge Commodity Dominance

Traditional plastics generated 70.18% of Philippines plastics market size in 2025, anchored by polyethylene and polypropylene used in flexible packaging, pipes, and household goods. Commodity margins remain thin as Chinese oversupply keeps regional prices subdued, motivating converters to look for differentiation. D&L Polymer & Colours’ January 2025 launch of plant-fiber plastics replaced up to 40% of virgin resin with abaca and pineapple fibers, reducing weight and improving stiffness in appliance housings. Engineering grades, including nylon 66 and PBT, maintain a smaller share yet yield premiums of 50%-100% over PE, cushioning producers from spot volatility.

Bioplastics lead growth at a 5.06% CAGR through 2031. Local producers OIKOS and EcoNest currently import starch pellets, but feasibility work for a 30,000-tonne PLA line suggests that cassava feedstock from Northern Mindanao and BARMM could localize supply, trimming import bills and boosting the Philippines plastics market. However, bioplastic resin still costs 40%-100% more than conventional polymers, and EPR regulations do not yet provide explicit price offsets, limiting near-term penetration. Continued R&D by the Industrial Technology Development Institute on nanocellulose and PHA could narrow that gap and diversify raw-material options, but scale-up hinges on electricity pricing and credit access.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Injection Precision Meets Rotomolding Versatility

Injection molding held 45.72% Philippines plastics market share in 2025 and remains the workhorse for electronics casings, connector housings, and medical devices, where dimensional tolerances below 0.05 mm are routine. Investments in servo-hydraulic machines with energy-recovery modules partially offset high electricity tariffs, and certified mold shops inside PEZA zones shorten lead times for OEM changes. Extrusion lines feed film and profile markets but face headwinds from anti-sachet legislation, prompting upgrades to multi-layer lines capable of running recycled content at high throughput.

Rotomolding, thermoforming, and compression molding together posted the fastest 4.97% CAGR and now capture niche furniture, agricultural, and specialty container applications. Resorts specify UV-stabilized rotomolded seating, while agricultural co-ops order thermoformed seedling trays made from post-consumer polypropylene, demonstrating end-use diversity that expands the Philippines plastics market. Blow molding benefits from PETValue’s bottle-to-bottle loop, ensuring steady preform demand even as beverage brands introduce light-weight neck finishes that cut resin per bottle by up to 10%.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Sachets Drive Packaging, Harnesses Pull Automotive

Packaging commanded 47.14% of the Philippines plastics market share in 2025, fueled by rising parcel counts, single-serve sachets, and the mainstreaming of video commerce that favors smaller pack sizes. Nestlé’s plastic-neutrality milestone of 79,559 tonnes collected by July 2023 shows how brands take-back schemes now feed recycled resin directly into film extrusion. Compostable film lines certified under TÜV Austria’s Compostaflex create further segment diversification and support higher unit margins.

Automotive & transportation applications are projected to expand at a 5.19% CAGR, the fastest within the Philippines plastics market, as EV components such as battery enclosures and lightweight connectors migrate to Philippine sourcing hubs. Building & construction follows infrastructure outlays with steady demand for pipe and geotextile, while electrical & electronics stay resilient on semiconductor packaging trays and appliance housings that require electrostatic discharge protection. Furniture, bedding, and miscellaneous uses—including toys and agricultural films—round out demand and often adopt lower-grade recycled resins, supporting the circular economy narrative.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Calabarzon forms the core manufacturing corridor for the Philippines plastics market, hosting JG Summit’s cracker, D&L’s Batangas specialty plant, PETValue’s bottle-to-bottle line, and dozens of precision molders all within 150 km of Manila ports. Metro Manila concentrates downstream conversion and waste collection to minimize transport costs on both virgin pellets and baled post-consumer plastics, enabling large FMCG users to secure just-in-time deliveries.

Visayas and Mindanao lag on energy and freight economics, confining most processors to low-value agricultural films and simple containers, yet high cassava output in Northern Mindanao positions the region as a logical site for future PLA fermentation or starch-based polymer blending. Infrastructure disbursements tilt toward Luzon, but planned airports and roads in Cebu and Davao could stimulate regional conversion if energy reforms materialize.

Export orientation remains essential: JG Summit ships polyolefins to more than 30 countries, and D&L’s Batangas plant sends specialty compounds across Asia and Europe, validating that economies of scale require offshore demand to absorb incremental capacity additions. The forthcoming National Plastics Action Roadmap aims to spread collection and recycling infrastructure beyond Metro Manila, potentially balancing geographic demand by 2030.

Competitive Landscape

The Philippines Plastics market is moderately concentrated. The upstream segment is concentrated around JG Summit Petrochemicals, which runs the only naphtha cracker but reported a PHP 3.8 billion EBITDA loss in the first nine months of 2024 due to record-low spreads, prompting a PHP 17.1 billion recapitalization. Midstream competition intensifies as D&L Industries commercializes fiber-reinforced resins that sell at a 20% premium to virgin PP while cutting weight by 8%-12% in appliance parts. Philippine Resins Industries leverages a chlor-alkali integration model, feeding PVC into water-pipe demand linked to Build Better More projects.

Philippines Plastics Industry Leaders

JG Summit Petrochemicals Group

Chemrez Technologies

Petron Corporation

NPC Alliance Corporation

Philippine Resins Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Paintplas Global Corporation unveiled its plans to invest over P350 million (USD 6.09 million) in a new manufacturing facility in Batangas. The facility is slated to commence commercial operations by September 2026. The plastic manufacturer aims to produce and assemble components for toys, vending machines, and motorcycle parts.

- February 2025: JG Summit Petrochemicals Group indefinitely shuttered its petrochemical plant in response to economic challenges. The company's operations encompass a naphtha cracker that produces ethylene and propylene and an aromatics unit. Downstream facilities, including plants for polypropylene, linear low-density polyethylene, high-density polyethylene, and polyethylene.

Philippines Plastics Market Report Scope

Plastics are one of the most traded commodity products globally. Most manufacturers in the country produce resins and plastic products for different applications, such as packaging, automotive, construction, electronics, furniture, and other applications. The market is segmented by type, technology, and application. By type, the market is segmented into traditional plastics, engineering plastics, and bioplastics. By technology, the market is segmented into blow molding, extrusion, injection molding, and other technologies. By application, the market is segmented into packaging, electrical and electronics, building and construction, automotive and transportation, furniture and bedding, and other applications. For each segment, the market sizing and forecast have been done based on revenue (USD million).

By Type

| Traditional Plastics |

| Engineering Plastics |

| Bioplastics |

By Technology

| Blow Moulding |

| Extrusion |

| Injection Moulding |

| Other Technologies |

By Application

| Packaging |

| Electrical & Electronics |

| Building & Construction |

| Automotive & Transportation |

| Furniture & Bedding |

| Other Applications |

| By Type | Traditional Plastics |

| Engineering Plastics | |

| Bioplastics | |

| By Technology | Blow Moulding |

| Extrusion | |

| Injection Moulding | |

| Other Technologies | |

| By Application | Packaging |

| Electrical & Electronics | |

| Building & Construction | |

| Automotive & Transportation | |

| Furniture & Bedding | |

| Other Applications |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value for plastics demand in the Philippines by 2031?

The Philippines Plastics market share in 2026 is estimated around USD 3.2 billion and is expected to reach USD 4.01 billion by 2031 with a CAGR of 4.61%

Which end-use segment is set for the quickest growth to 2031?

Automotive & transportation, expanding at a projected 5.19% CAGR as wire-harness and EV components gain share.

How large was packaging’s share of total resin use in 2025?

The packaging application contributed to 47.14% of national consumption in 2025.

What fiscal benefits come from locating inside a PEZA zone?

Firms receive a 4–7 year income-tax holiday, then pay a 5% tax on gross income instead of 25%, plus duty-free import of equipment and resins.

Which region offers feedstock potential for cassava-based biopolymers?

Northern Mindanao and BARMM, which together account for 70% of national cassava output offers feedstock potential for cassava-based biopolymers.