Market Overview

| Study Period | 2019 - 2030 |

|---|---|

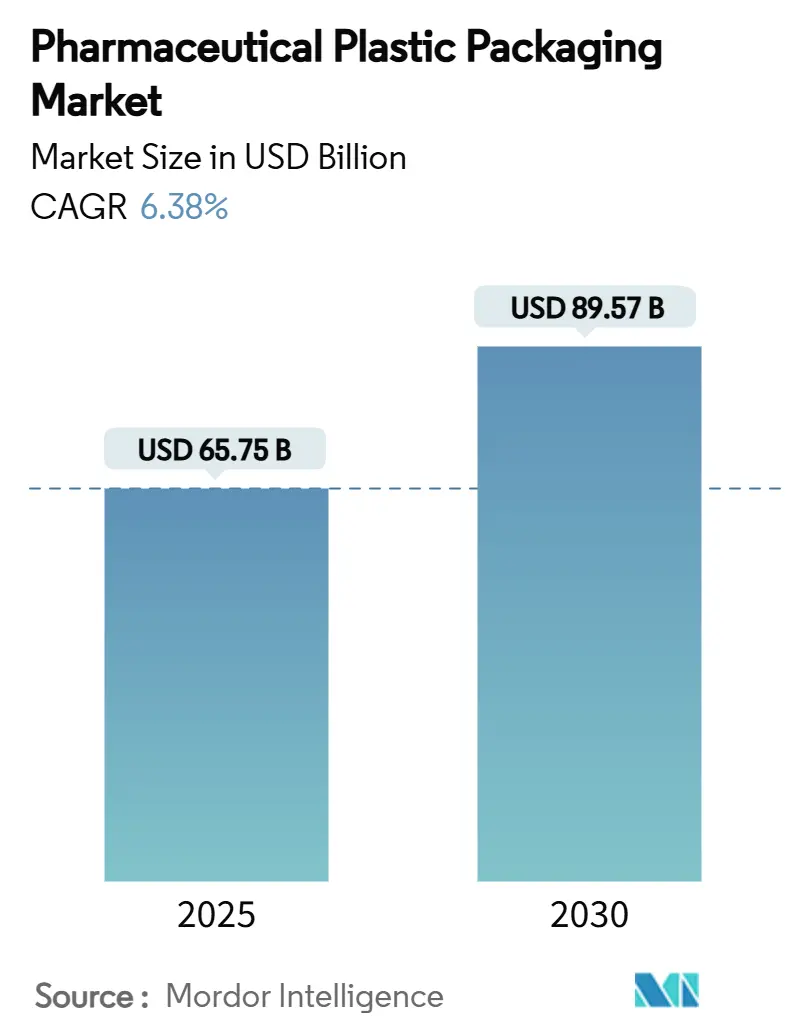

| Market Size (2025) | USD 65.75 Billion |

| Market Size (2030) | USD 89.57 Billion |

| Growth Rate (2025 - 2030) | 6.38% CAGR |

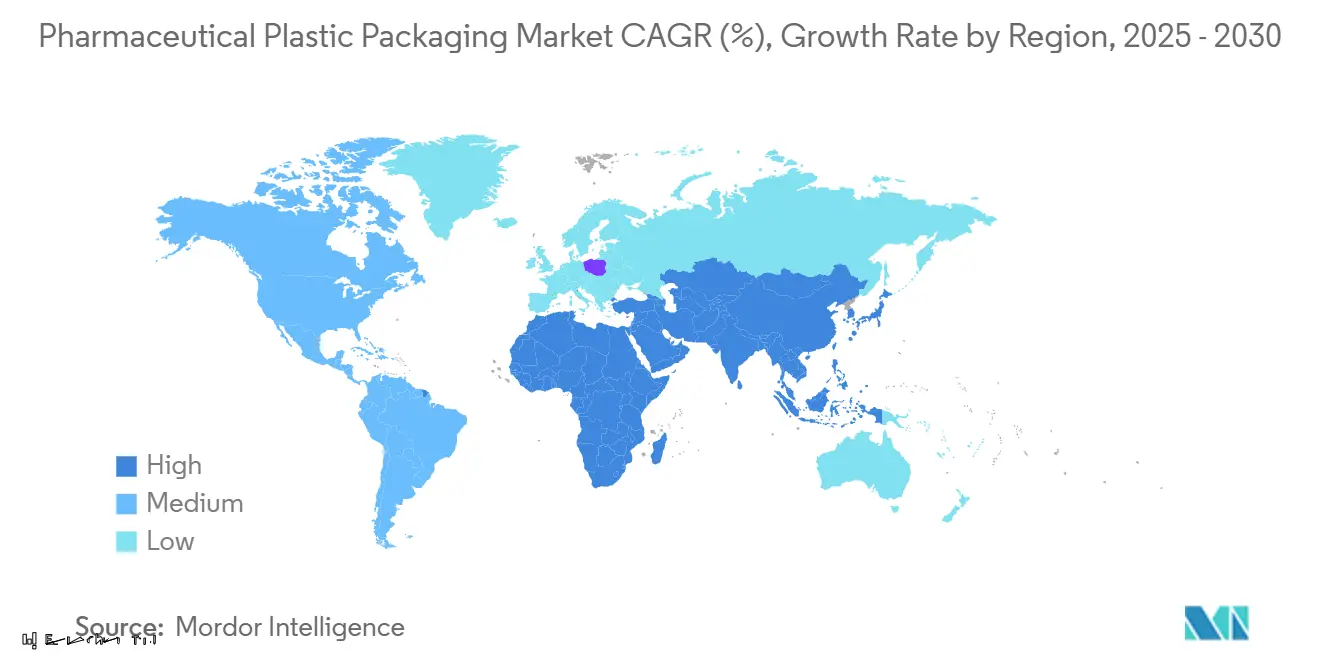

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pharmaceutical Plastic Packaging Market Analysis by Mordor Intelligence

The pharmaceutical plastic packaging market size stood at USD 65.75 billion in 2025 and is forecast to expand to USD 89.57 billion by 2030, reflecting a 6.38% CAGR. Growth rests on the rising share of biologics and injectables, stricter traceability rules, and fast-maturing sustainability mandates that reward recyclable and bio-based polymers. In February 2025 the EU’s Packaging and Packaging Waste Regulation (PPWR) entered into force, requiring full recyclability by 2030 and accelerating material substitution programs.[1]European Parliament, “Packaging and Packaging Waste Regulation,” europarl.europa.euNorth American demand benefits from the Drug Supply Chain Security Act (DSCSA) deadline in November 2025, which pushes smart, serialization-ready formats. Asia-Pacific manufacturers leverage regulatory harmonization and surging generic output, lifting the region’s growth prospects. Consolidation among mid-tier converters, exemplified by Amcor’s USD 13.5 billion merger with Berry Global, brings scale to tackle PFAS-free formulations and circular-economy investments.

Key Report Takeaways

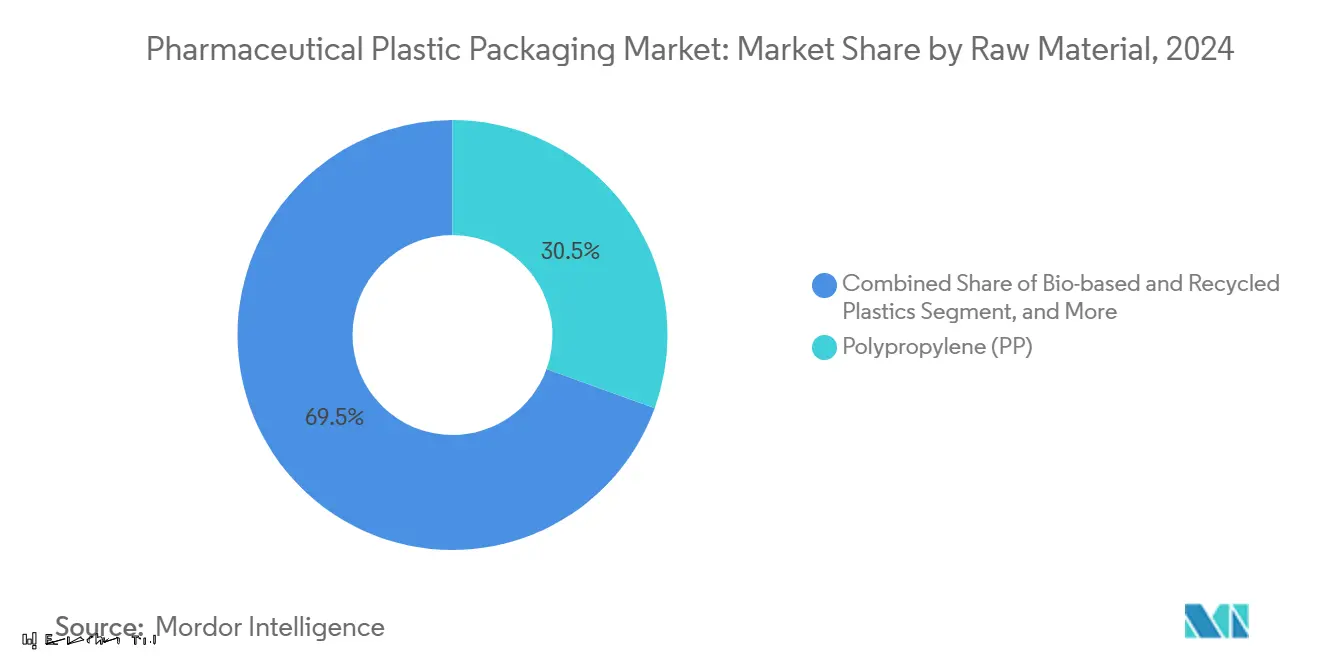

- By raw material, polypropylene led with 30.53% of pharmaceutical plastic packaging market share in 2024, while bio-based and recycled plastics are set to grow at 9.32% CAGR through 2030.

- By product type, bottles and solid containers held 26.44% share of the pharmaceutical plastic packaging market size in 2024; pre-fillable syringes and cartridges are projected to expand at 8.53% CAGR to 2030.

- By packaging format, rigid solutions captured 65.32% share in 2024, whereas flexible formats are advancing at a 7.43% CAGR through 2030.

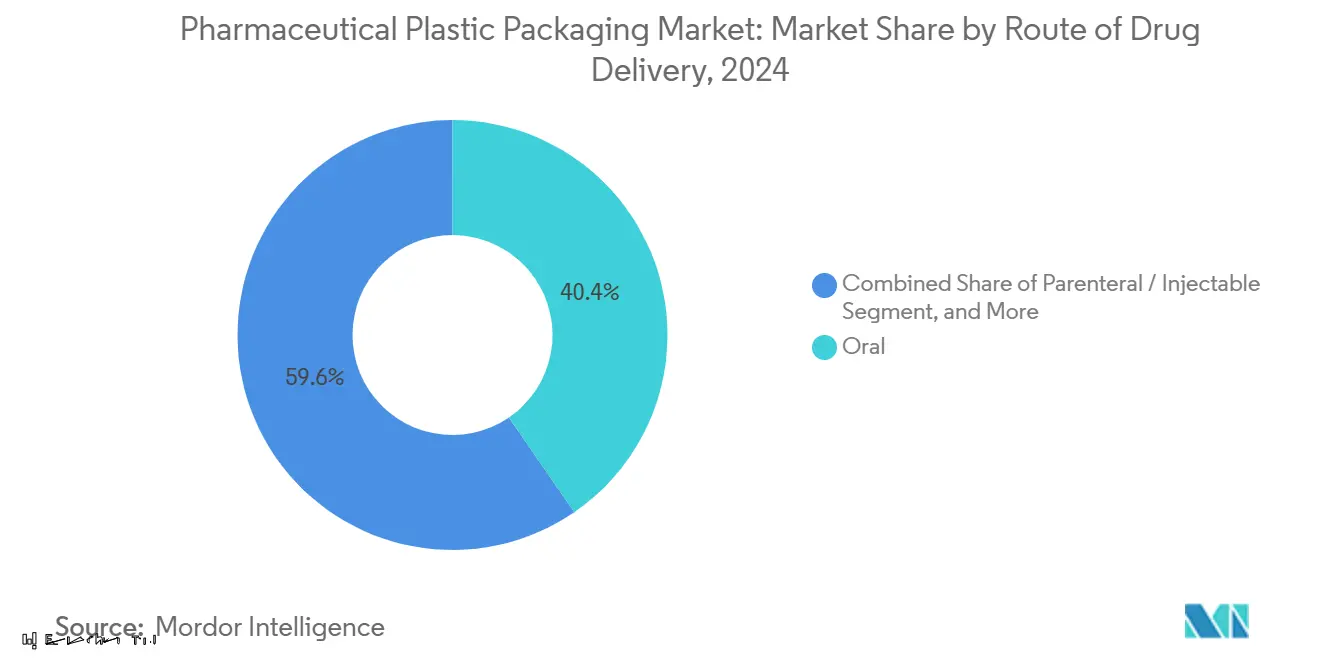

- By route of drug delivery, oral formulations accounted for 40.43% of the pharmaceutical plastic packaging market size in 2024, while parenteral/injectable formats will rise at 8.56% CAGR.

- By end-user, pharmaceutical manufacturers represented 50.32% share in 2024; home-care settings register the fastest expansion at 10.43% CAGR.

- By geography, North America dominated with 36.43% share in 2024, whereas Asia-Pacific records the highest 9.98% CAGR through 2030.

Global Pharmaceutical Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for plastic packs for biologics and injectables | +1.8% | North America & Europe core; global spill-over | Medium term (2-4 years) |

| Expansion of generic drug production in emerging markets | +1.2% | Asia-Pacific core; MEA & South America spill-over | Long term (≥ 4 years) |

| Lightweight, shatter-proof logistics advantage | +0.9% | Global | Short term (≤ 2 years) |

| Home-health and e-commerce unit-dose adoption | +1.1% | North America & Europe; expanding to Asia-Pacific | Medium term (2-4 years) |

| On-site BFS and 3-D printed molds for personalized meds | +0.7% | North America & Europe | Long term (≥ 4 years) |

| Antimicrobial / smart-polymer enabled packs | +0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand for Plastic Packs for Biologics and Injectables

Biologics now account for a rising share of new drug approvals, and their sensitivity to alkali leaching, delamination, and breakage positions advanced polymers as preferred primary containers. Cyclic olefin polymer syringes from Gerresheimer combine glass-like transparency with superior break resistance, helping minimize costly biologic losses. The global biopharmaceutical sector is expected to reach USD 856.1 billion by 2030, reinforcing demand for high-integrity parenteral packaging. Validated blow-fill-seal containers show no potency or pH drift for monoclonal antibodies over nine months, broadening polymer uptake in sterile applications. During the pandemic, shortages of glass vials highlighted supply-chain risks, prompting dual-sourcing policies that now favor plastic options with equivalent regulatory acceptance.

Expansion of Generic Drug Production in Emerging Markets

Regulatory reforms in China, notably the Marketing Authorization Holder system, shorten approval cycles and attract contract manufacturing alliances that boost packaging volumes. Beijing’s 2025 guidance contains 24 measures to modernize drug oversight by 2027, creating clear targets for compliant packaging lines. India and ASEAN mutual recognition programs further harmonize specifications, letting converters scale a single design across multiple markets. Price-sensitive generics also prioritize cost-efficient plastics that remain robust during long-distance export shipments.

Lightweight, Shatter-Proof Logistics Advantage

Compliance with DSCSA serialization by November 2025 requires robust, data-enabled packs. Plastics withstand impact and temperature swings better than glass, reducing returns and cold-chain spoilage. IoT-linked Saga cards from Avery Dennison pair sensors with durable plastic enclosures for real-time shipment visibility. With 10% tariffs on Chinese resins and 15% tariffs on Middle-East feedstocks effective in 2025, converters intensify weight-reduction programs to offset input inflation.

Home-Health and E-Commerce Unit-Dose Adoption

The aging population and payers’ push toward home treatment spur unit-dose blister and stick-pack demand. Blistering chronic meds has proven cost-effective despite higher dispensing fees, improving long-term adherence. QR-code labels link patients to dosage reminders and telehealth portals, addressing the 50% non-adherence challenge. NFC-enabled autoinjector labels from Schreiner Group add temperature indicators that guard biologic potency during mail-order shipments. Forecasts place the repackaging segment above USD 3 billion by 2034, aligning with double-digit growth in home-care infusions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended plastics-waste regulation (EU SUP, EPR) | -0.8% | Europe core; global spill-over | Short term (≤ 2 years) |

| Volatile polymer feedstock pricing | -1.1% | Global | Short term (≤ 2 years) |

| Biologic-glass policy shift toward COP vials | -0.4% | North America & Europe | Medium term (2-4 years) |

| Scarcity of pharma-grade recycled resin supply | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extended Plastics-Waste Regulation (EU SUP, EPR etc.)

The PPWR obliges all packs sold in the EU to be recyclable by 2030 and introduces EPR fees plus recycled-content thresholds—30% for PET food packs—adding capital and compliance burdens. Healthcare exemptions exist for immediate drug containers, yet brand owners must still fund collection schemes, redesign multilayer laminates, and phase out PFAS in contact materials by 2026. Harmonized symbols due in 2028 compel artwork changes, while the 5% material-reduction target squeezes already lean wall-thickness specs.

Volatile Polymer Feedstock Pricing

Global resin markets have swung sharply; PE and PC values climbed, PP and PET retreated, disrupting budget baselines. Pharmaceutical packagers operate under fixed supply contracts with payers, limiting price-pass-through flexibility. Energy volatility, labor shortages, and rising adoption of post-consumer recycled resin further destabilize cost forecasts, prompting hedging and dual-sourcing strategies.

Segment Analysis

By Raw Material: Bio-Based Innovation Drives Transformation

Polypropylene retained leadership with 30.53% of pharmaceutical plastic packaging market share in 2024 thanks to its sterilization tolerance and regulatory familiarity. Yet bio-based and recycled grades are set to outpace all incumbents at 9.32% CAGR, reshaping the pharmaceutical plastic packaging market through 2030. Avient’s Mevopur range delivers up to 120% carbon-footprint reduction while keeping ISO 10993 and USP VI credentials, illustrating how circularity and compliance now co-exist.[2]Avient Corporation, “Bio-based Polymer Solutions,” avient.com EU recycled-content quotas and the FDA’s looming dye phase-out intensify demand for renewable feedstocks. UPM’s wood-based bottle launch underscores commercial feasibility of lignin-rich chemistries.

Second-generation bio-polyolefins and chemically recycled PET now reach pharmaceutical purity, unlocking drop-in substitution without retooling. However, limited pharma-grade recyclate supplies restrain immediate scale, creating price premiums. Resin majors ramp capacity near European and North American hubs to shorten logistics, while Asian players eye export-grade r-resin certification to capture surging orders. The pharmaceutical plastic packaging market therefore balances legacy PP dominance with measured yet accelerating penetration of renewable polymers that align with PPWR and corporate net-zero pledges.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Pre-Fillable Systems Lead Innovation

Bottles and solid containers captured 26.44% of the pharmaceutical plastic packaging market in 2024 owing to oral solid dosage prevalence. Yet pre-fillable syringes and cartridges headline the growth story, advancing at 8.53% CAGR as biologics, GLP-1 injectables, and home-administered drugs proliferate. BD’s RFID-enabled iDFill syringe merges device and pack, supplying real-time traceability that dovetails with DSCSA needs.

Digital connectivity, higher viscosity tolerances, and on-body injector compatibility move these containers from commodity to high-value engineered systems. Conversely, vials and ampoules remain essential for hospital compounding, though dose-banded biologics see a shift to polymer-based EZ-fill Smart vials from Gerresheimer that streamline fill-finish operations. Stick packs, sachets, and pouches gain foothold in tele-pharmacy mailers where postage and cushioning costs punish rigid lines.

By Packaging Format: Flexible Solutions Gain Momentum

Rigid formats still held 65.32% of the pharmaceutical plastic packaging market size in 2024, favored for moisture and gas barriers. Flexible solutions, however, will climb at 7.43% CAGR, shrinking the gap. TekniPlex’s transparent mid-barrier blister with 30% PCR content debuts a recyclable platform that meets child-resistance and unit-dose accuracy. Dai Nippon Printing’s polypropylene press-through film replaces aluminum, enabling mono-material blister cards aligned with PPWR recyclability targets.

Flexibles lower carbon footprints by reducing gram weight, cut inbound transport emissions, and improve line speeds via rollstock formats. Yet achieving class-leading oxygen and moisture ingress rates without aluminum remains technically demanding, preserving rigid’s edge for ultra-sensitive lyophilized or dry-powder biologics. As copolymer barrier layers mature, the pharmaceutical plastic packaging industry anticipates broader rigid-to-flexible migration, especially in high-volume OTC and mail-order channels.

By Route of Drug Delivery: Parenteral Growth Accelerates

The oral segment retained 40.43% share of the pharmaceutical plastic packaging market in 2024 because tablets remain convenient and low-cost. Parenteral or injectable formats will, however, post an 8.56% CAGR as mRNA therapies, oncology biologics, and depot injections expand. SCHOTT Pharma’s TOPPAC Freeze syringe guards lipid-nanoparticle vaccines down to −80 °C, highlighting material evolution to serve cold-chain extremes.

Ophthalmic packs also modernize: Berry Global’s easy-squeeze bottle joined with Aptar’s preservative-free dropper meets stricter ocular-toxicity thresholds while aiding arthritis patients’ grip strength. Nasal and transdermal systems gain traction as needle-free alternatives that still rely on high-barrier polymers to protect volatile actives.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Home-Care Settings Drive Transformation

Pharmaceutical manufacturers commanded 50.32% of pharmaceutical plastic packaging market share in 2024 because most companies still self-package at scale. Home-care settings are poised for 10.43% CAGR, creating fresh design imperatives. Allegheny Health Network’s pilot of the paper-based Tully Tube underscores sustainability and child-resistance progress in prescription retail. DosePacker’s QR-coded sleeve links to adherence apps and dosage timers, embedding digital therapy support into everyday packs.

Contract Development and Manufacturing Organizations (CDMOs) scale bespoke fill-finish lines for small-batch personalized medicines, leveraging 3-D printed molds and BFS pockets to cut tooling lead-times. Hospitals still specify tamper-evident IV bags and unit-dose oral syringes that reduce medication errors at bedside. The pharmaceutical plastic packaging industry therefore balances high-volume plant orders with nimble home-care SKUs that fuse smart features and green credentials.

Geography Analysis

North America held 36.43% of the pharmaceutical plastic packaging market in 2024, supported by advanced GMP plants, DSCSA serialization deadlines, and reshoring incentives. FDA guidance endorses continuous manufacturing and smart sensors, pushing local converters to embed RFID in pack walls and qualify PFAS-free films.[3]FDA, “Adoption of Advanced Manufacturing,” fda.govTariffs on imported resins raise domestic capacity utilization and spur investment in bio-based feedstocks, stabilizing supply chains vulnerable to geopolitical shocks.

Europe combines regulatory stringency with sustainability leadership, forging a robust yet evolving market base. The PPWR enforces recyclability, EPR fees, and PFAS bans, forcing redesigns that stimulate R&D budgets among regional converters. Single-Use Plastics Directive restrictions encourage mono-material blister films, while national eco-modulation schemes reward low-carbon formats. Nordic and DACH states lead pilot take-back schemes for used inhalers and injectors, offering closed-loop polypropylene pathways.

Asia-Pacific delivers the highest 9.98% CAGR for the pharmaceutical plastic packaging market through 2030. China accelerates under its 2025 action plan, aligning packaging quality audits with ICH Q9 while funding green factories. India tightens pharmacopoeial tests and digital traceability, creating opportunities for smart-label suppliers. ASEAN mutual recognition saves months of dossier work, letting exporters ship compliant packs across member borders. Japanese EPR schemes extend to medical packs, catalyzing PCR-grade PP sourcing. Together, these tailwinds strengthen the pharmaceutical plastic packaging market across developing and mature APAC nations.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The pharmaceutical plastic packaging market remains fragmented, with regional specialists coexisting alongside global majors. Amcor’s all-stock combination with Berry Global forms a USD 25 billion sales powerhouse that allocates USD 180 million annually to R&D, chasing 650 million in synergies and sharpening focus on healthcare polymers. The merger widens its flexible footprint in Asia through Phoenix Flexibles, aligning with the fastest-growing regional demand.

Gerresheimer differentiates through digitally enabled primary packaging, such as the Gx Cap smart bottle that logs trial subject adherence, and the EZ-fill Smart sterile vial platform that slashes filling line changeovers . TekniPlex targets sustainability white-spots with PCR-rich blister webs that meet USP <661.1> extractables limits . Medium-sized converters pursue niche wins—Nutra-Med’s acquisition of Legacy Pharma Solutions expands high-speed blistering for nutraceutical clients entering Rx-to-OTC switches.

Competitors pivot R&D to PFAS-free barrier coatings, antimicrobial masterbatches, and blockchain-ready NFC tags. Capital intensity rises as lines upgrade to handle recycled resin variability, pushing collaboration through joint-development agreements. Market entrants differentiate via agile 3-D printed tooling for personalized medicines packaging, whereas incumbents leverage volume contracts with top 20 pharma companies, underpinning moderate concentration within the pharmaceutical plastic packaging market.

Pharmaceutical Plastic Packaging Industry Leaders

-

Aptar Group Inc.

-

Plastipak Holdings

-

Amcor PLC

-

Klöckner Pentaplast Group

-

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2024: Dai Nippon Printing introduced a polypropylene press-through film to replace aluminum foil, targeting JPY 1 billion (USD 6.7 million) sales by 2030.

- June 2025: FDA confirmed a phase-out of petroleum-based synthetic dyes in food-contact polymers by end-2026, prompting pack reformulations.

- May 2025: Gerresheimer unveiled the Gx Cap smart tablet container and EZ-fill Smart platform at Pharmapack 2025.

- April 2025: Amcor finalized its USD 13.5 billion merger with Berry Global, creating a global healthcare-packaging leader.

Global Pharmaceutical Plastic Packaging Market Report Scope

Pharmaceutical plastic packaging involves using plastic materials to package pharmaceutical drugs. Pharmaceutical plastic bottles, tailored for storing and distributing pharmaceutical products, are pivotal in upholding the safety, efficacy, and integrity of medications and pharmaceutical items. Pharmaceutical plastic packaging products are designed to protect the contents from contamination, moisture, and light, ensuring the drugs remain effective throughout their shelf life. Additionally, plastic packaging offers lightweight, durability, and cost-effectiveness benefits, making it a preferred choice in the pharmaceutical industry.

The pharmaceutical plastic packaging market is segmented by raw material (polypropylene (PP), polyethylene terephthalate (PET), low-density polyethylene (LDPE), high-density polyethylene (HDPE), and other raw materials), product type (solid containers, dropper bottles, nasal spray bottles, liquid bottles, oral care, pouches, vials, and ampoules, cartridges, syringes, caps and closures, and other product types), and geography (North America (the United States and Canada), Europe (United Kingdom, Germany, France, Spain, Italy, and Rest of Europe), Asia Pacific (China, India, Japan, and Rest of Asia Pacific), Latin America (Brazil, Argentina, Mexico, and Rest of Latin America), and Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa)). The report offers market forecasts and size in value (USD) for all the above segments.

By Raw Material

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) |

| Cyclic Olefin Polymer / Copolymer (COP/COC) |

| Bio-based and Recycled Plastics |

By Product Type

| Bottles and Solid Containers |

| Vials and Ampoules |

| Pre-fillable Syringes and Cartridges |

| Blister Packs and Strip Packs |

| Pouches / Stick Packs / Sachets |

| Closures, Caps and Lids |

| IV Bags and Flexible Bags |

By Packaging Format

| Rigid |

| Flexible |

By Route of Drug Delivery

| Oral |

| Parenteral / Injectable |

| Ophthalmic / Nasal |

| Topical / Transdermal |

By End-User

| Pharma Manufacturers |

| Contract Development and Manufacturing Orgs (CDMOs) |

| Hospitals and Clinics |

| Home-care Settings |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Raw Material | Polypropylene (PP) | ||

| Polyethylene Terephthalate (PET) | |||

| High-Density Polyethylene (HDPE) | |||

| Low-Density Polyethylene (LDPE) | |||

| Cyclic Olefin Polymer / Copolymer (COP/COC) | |||

| Bio-based and Recycled Plastics | |||

| By Product Type | Bottles and Solid Containers | ||

| Vials and Ampoules | |||

| Pre-fillable Syringes and Cartridges | |||

| Blister Packs and Strip Packs | |||

| Pouches / Stick Packs / Sachets | |||

| Closures, Caps and Lids | |||

| IV Bags and Flexible Bags | |||

| By Packaging Format | Rigid | ||

| Flexible | |||

| By Route of Drug Delivery | Oral | ||

| Parenteral / Injectable | |||

| Ophthalmic / Nasal | |||

| Topical / Transdermal | |||

| By End-User | Pharma Manufacturers | ||

| Contract Development and Manufacturing Orgs (CDMOs) | |||

| Hospitals and Clinics | |||

| Home-care Settings | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the pharmaceutical plastic packaging market?

The pharmaceutical plastic packaging market size reached USD 65.75 billion in 2025 and is projected to hit USD 89.57 billion by 2030.

Which raw material dominates the pharmaceutical plastic packaging market?

Polypropylene remains dominant with 30.53% market share in 2024 due to its sterilization compatibility and regulatory acceptance.

Why are pre-fillable syringes growing faster than bottles?

The rise of biologics and home-administered injectables drives an 8.53% CAGR for pre-fillable syringes, outpacing bottles’ growth.

How will EU regulations impact pharmaceutical plastic packaging?

The PPWR mandates full recyclability by 2030 and introduces EPR fees, pushing companies to adopt mono-material designs and recycled content.

What region offers the fastest growth opportunity?

Asia-Pacific leads with a projected 9.98% CAGR, powered by expanding generic drug manufacturing and regulatory harmonization.

How are companies addressing sustainability?

Firms invest in bio-based polymers, PCR-rich films, and PFAS-free coatings, while collaborations aim to secure pharma-grade recycled resin streams.

Page last updated on: