Market Size of Pharmaceutical Packaging Industry

| Study Period | 2019 - 2029 |

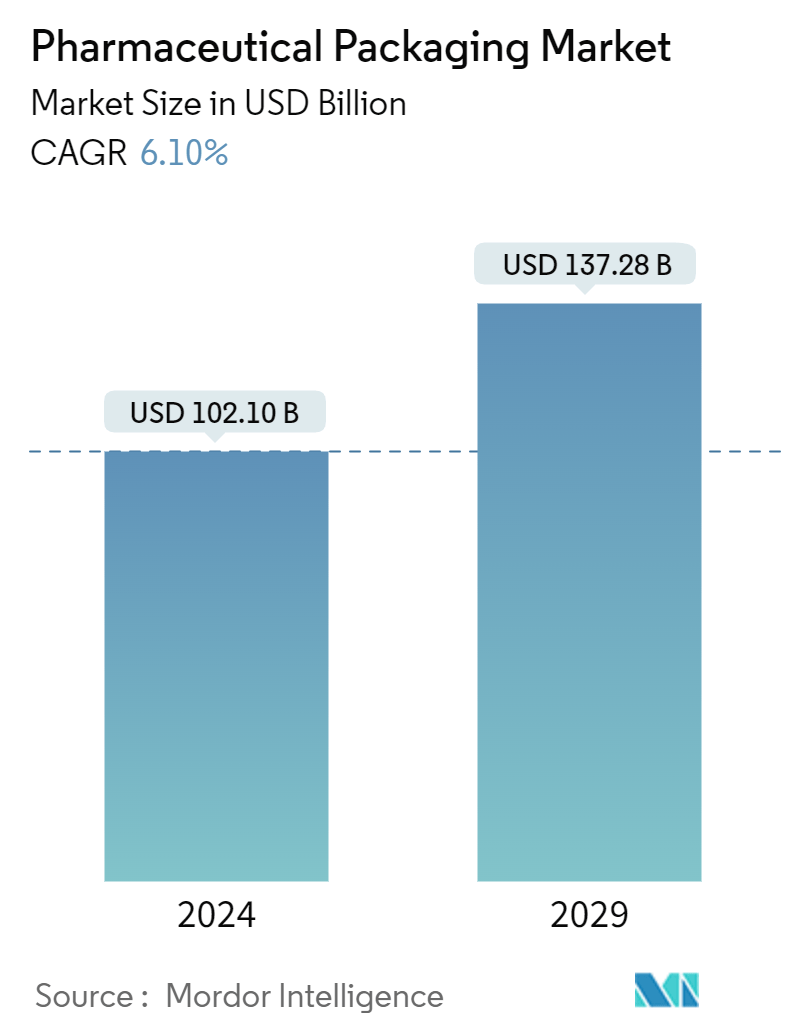

| Market Size (2024) | USD 102.10 Billion |

| Market Size (2029) | USD 137.28 Billion |

| CAGR (2024 - 2029) | 6.10 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Pharmaceutical Packaging Market Analysis

The Pharmaceutical Packaging Market size is estimated at USD 102.10 billion in 2024, and is expected to reach USD 137.28 billion by 2029, growing at a CAGR of 6.10% during the forecast period (2024-2029).

Regulatory Landscape Shapes Packaging Innovation:

The pharmaceutical packaging market is experiencing significant growth driven by stringent regulatory standards and anti-counterfeit measures. Governments worldwide are implementing strict regulations to ensure product safety and combat counterfeit drugs. The European Union's Directive mandates serialization numbers on all pharmaceutical products, while similar regulations exist in the United States, China, India, and Turkey. These measures are propelling the adoption of advanced packaging solutions.

- FDA Guidelines: The FDA has established guidelines for child-resistant packaging and tamper-resistant packaging for OTC products.

- Authentication Technologies: Pharmaceutical companies are investing in authentication technologies like holograms and hidden batch numbers.

- Serialization Methods: Serialization methods include linear barcodes, two-dimensional barcodes, and radio frequency identification (RFID).

- Smart Packaging: Smart packaging with RFID and NFC tags is gaining traction for product tracking and patient engagement.

Nanotechnology Revolutionizes Packaging Solutions:

The impact of nanotechnology on pharmaceutical packaging is transforming the industry with innovative and new-generation solutions. These advancements not only combat counterfeiting but also enhance product safety and traceability throughout the supply chain.

- Tracking Capability: Nanotechnology enables the creation of smart packaging that can track products from manufacturing to end-user.

- Smart Packaging Development: Companies like Schott AG are developing smart packaging containment solutions for clear container-based traceability.

- Product Launches: ENTOD Pharmaceuticals launched a nanotechnology-based ocular aesthetic range in India, showcasing the versatility of nano-packaging.

- Biomedicine Applications: Nanoparticles are being utilized in biomedicine for disease detection, prevention, and drug delivery.

Market Drivers and Growth Trends:

The pharmaceutical packaging market is witnessing robust growth, fueled by several key drivers. The expansion of the pharmaceutical industry in emerging economies, coupled with increasing healthcare spending, is propelling market growth.

- Plastics Segment: The plastics segment is expected to reach USD 54.45 billion by 2028, growing at a CAGR of 6.17%.

- Bottles Segment: The bottles segment was valued at USD 18.24 billion in 2022 and is projected to reach USD 27.30 billion by 2028.

- FDI Growth: Emerging economies like India are experiencing significant growth, with a 200% increase in FDI in the pharmaceutical industry in 2020-2021.

- Asia-Pacific Growth: The Asia-Pacific region is expected to grow at a CAGR of 6.99% from 2023 to 2028, reaching USD 54.59 billion by 2028.

Competitive Landscape and Key Players:

The pharmaceutical packaging market is fragmented, with several major players dominating the industry. These companies are focusing on innovation, sustainability, and strategic expansions to maintain their market positions.

- Amcor PLC: Established in 1860, Amcor offers a wide range of packaging solutions, including oral dose formats and medical device packaging.

- Schott AG: Founded in 1853, Schott specializes in pharmaceutical tubing and drug containment solutions.

- Berry Global Group: Established in 1967, Berry Global provides medical packaging, bottles, and vials.

- Gerresheimer AG: Gerresheimer AG announced a USD 94 million investment in a US production facility to increase its vial production capacity.

Sustainability and Future Trends:

The pharmaceutical packaging industry is increasingly focusing on sustainability and eco-friendly solutions. This trend is driven by both regulatory pressures and consumer demand for more environmentally responsible packaging.

- GSK's Initiative: GlaxoSmithKline Consumer Healthcare joined the Pulpex paper bottle partner consortium to explore recyclable paper bottles.

- Bioplastics Investment: Companies are investing in bioplastics and other biodegradable materials as alternatives to traditional plastics.

- Advanced Printing Technologies: Advanced printing technologies, such as Essentra Packaging's Landa S10 Nanographic Printing Machine, are enhancing packaging capabilities.

- 3-D Visualization: The adoption of 3-D visualization and printing strategies is pushing the boundaries of both primary and secondary packaging design.

Pharmaceutical Packaging Industry Segmentation

The packages and packing procedures for pharmaceutical preparations are referred to as pharmaceutical packaging (or medication packaging). It involves every stage of the process, from drug production to the final consumer, via various distribution routes. The study considers revenues from the sales of different pharmaceutical packaging products offered by various vendors operating in the market. The market scope considers product types, including bottles, vials and ampoules, Syringes, caps and closures, labels, and others. The consumption value (USD) of pharmaceutical packaging is considered for the market size and forecasts. The market study factors the impact of COVID-19 on the overall pharmaceutical glass packaging market based on the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The pharmaceutical packaging market is segmented by material (plastic, glass), product type (bottles, syringes, vials and ampoules, tubes, caps and closures, and labels), and geography (North America (United States and Canada), Europe (Germany, United Kingdom, France, Italy, Spain, and rest of Europe), Asia-Pacific (China, Japan, India, South Korea, and rest of Asia-Pacific), Latin America (Brazil, Mexico, and rest of Latin America), and Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and rest of Middle East and Africa)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Material | |

| Plastics | |

| Glass | |

| Other Materials |

| By Product Type | |

| Bottles | |

| Syringes | |

| Vials and Ampoules | |

| Tubes | |

| Caps and Closures | |

| Labels | |

| Other Product Types |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Pharmaceutical Packaging Market Size Summary

The pharmaceutical packaging market is poised for steady growth, driven by the expanding global pharmaceutical industry and the increasing demand for effective packaging solutions. This growth is fueled by the need to protect pharmaceuticals from damage, biological contamination, and external influences, as well as the rising demand for injectables and high-potency drugs. Technological advancements in the industry are further propelling the demand for various packaging solutions, including bottles and vials. The market is also experiencing a shift towards more sustainable and eco-friendly packaging options, with plastics and polymers being widely used due to their durability, flexibility, and compliance with regulatory standards. The COVID-19 pandemic has accelerated the demand for sterilized packaging, prompting investments in packaging technology and infrastructure.

The competitive landscape of the pharmaceutical packaging market is characterized by intense rivalry among key players such as Amcor PLC, Schott AG, and WestRock Company, who are actively expanding their portfolios through strategic acquisitions and collaborations. The market is fragmented, with companies focusing on innovation and sustainability to meet emerging consumer demands. Regions like China, Japan, India, and South Korea are witnessing significant growth, driven by advancements in healthcare and pharmaceutical sectors. The Chinese government's policies and the rapid development of the pharmaceutical industry in South Korea are creating new opportunities for packaging firms. Additionally, the market is seeing increased adoption of advanced packaging technologies, such as nano-enabled and blow-fill-seal packaging, which are expected to shape the future dynamics of the industry.

Pharmaceutical Packaging Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Buyers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitutes

-

1.3.5 Degree of Competition

-

-

1.4 Assessment of Impact of the COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Material

-

2.1.1 Plastics

-

2.1.2 Glass

-

2.1.3 Other Materials

-

-

2.2 By Product Type

-

2.2.1 Bottles

-

2.2.2 Syringes

-

2.2.3 Vials and Ampoules

-

2.2.4 Tubes

-

2.2.5 Caps and Closures

-

2.2.6 Labels

-

2.2.7 Other Product Types

-

-

2.3 By Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

-

2.3.2 Europe

-

2.3.2.1 Germany

-

2.3.2.2 United Kingdom

-

2.3.2.3 France

-

2.3.2.4 Italy

-

2.3.2.5 Spain

-

2.3.2.6 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 Japan

-

2.3.3.3 India

-

2.3.3.4 South Korea

-

2.3.3.5 Rest of Asia-Pacific

-

-

2.3.4 Latin America

-

2.3.4.1 Brazil

-

2.3.4.2 Mexico

-

2.3.4.3 Rest of Latin America

-

-

2.3.5 Middle East and Africa

-

2.3.5.1 United Arab Emirates

-

2.3.5.2 Saudi Arabia

-

2.3.5.3 South Africa

-

2.3.5.4 Rest of Middle East and Africa

-

-

-

Pharmaceutical Packaging Market Size FAQs

How big is the Pharmaceutical Packaging Market?

The Pharmaceutical Packaging Market size is expected to reach USD 102.10 billion in 2024 and grow at a CAGR of 6.10% to reach USD 137.28 billion by 2029.

What is the current Pharmaceutical Packaging Market size?

In 2024, the Pharmaceutical Packaging Market size is expected to reach USD 102.10 billion.