Market Size of Pharmaceutical Contract Packaging Industry

| Study Period | 2019 - 2029 |

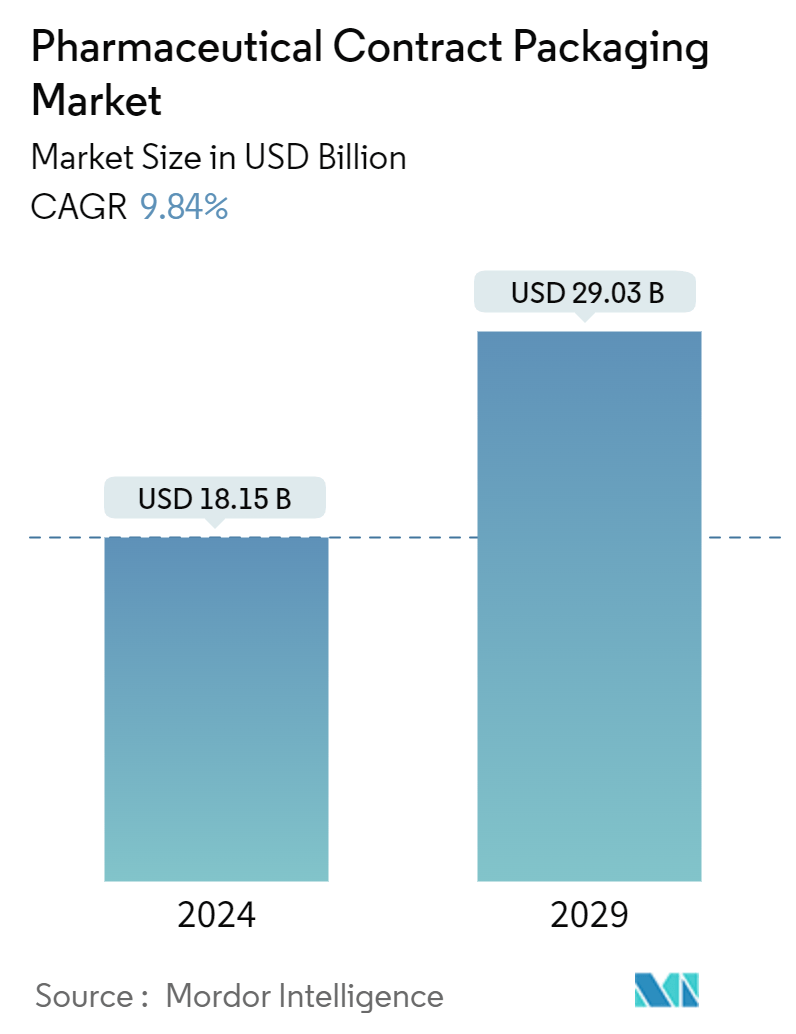

| Market Size (2024) | USD 18.15 Billion |

| Market Size (2029) | USD 29.03 Billion |

| CAGR (2024 - 2029) | 9.84 % |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Pharmaceutical Contract Packaging Market Analysis

The Pharmaceutical Contract Packaging Market size is estimated at USD 18.15 billion in 2024, and is expected to reach USD 29.03 billion by 2029, at a CAGR of 9.84% during the forecast period (2024-2029).

The pharmaceutical industry is growing exponentially, driven by global economic growth, an aging population, and new product launches. The increasing sales of pharmaceuticals are driving the logistics and warehousing requirements as vendors in the market are constantly expanding their facilities. With the understanding that pharmaceutical companies can boost their profits by outsourcing the packaging of their products, there has been a noticeable rise in the use of pharmaceutical contractors for commercial and clinical packaging.

Continued Endeavors to Implement Serialization to Support Market Expansion

- The pharmaceutical packaging market's key factors are growth in self-medication and multi-drug protocols, safety and compliance, product and patient engagement, and serialization. Packaging that helps and engages patients via ease of managing doses and drug compliance is among the foremost trends.

- Technological and innovative packaging is critical to protecting the integrity of the supply chain and ensuring that consumers have access to safe and reliable medicines and medical devices. Serialization and tracking capabilities not only help brands fight off counterfeit goods but can also be used to generate more value by creating new channels for revenue generation. Because these approaches are essential in the fight to protect patients from counterfeit medicines, the printing and packaging industry must stay ahead of illicit manufacturers and prevent potentially dangerous counterfeits from falling into the hands of unsuspecting patients.

Competition from In-house Packaging Key Verticals to Restrict the Market Growth

- Contract packaging can be time-consuming, as products are transported several times between manufacturers and packagers, thus increasing the potential for damage. In the case of a liquid product, the percentage will be higher since damage to one bottle can destroy multiple units. Many companies may choose to handle packaging in-house because it can be more cost-effective for them. By doing so, they can have more control over the entire packaging process, including material sourcing, design, and production, potentially reducing costs compared to outsourcing to a contract packaging provider.

- Factors such as unwillingness to share information with contract packagers, availability of in-house machinery, and high switching costs encourage in-house packaging and act as a restraining factor for contract packagers.

In the pharmaceutical contract packaging market, microeconomic factors like surging input costs, escalating labor expenses, and mounting pressures from regulatory compliance are driving up business costs. Concurrently, there's a rising demand for intricate and tailored packaging solutions spurred by technological advancements and a wave of competitive consolidations. These dynamics present lucrative opportunities for firms adept at innovation and efficient scaling. Companies that navigate these challenges through strategic tech investments, forging partnerships, and emphasizing sustainability are poised to excel in this fiercely competitive landscape.

Pharmaceutical Contract Packaging Industry Segmentation

The study on the Pharmaceutical Contract Packaging market tracks demands in terms of revenue for vendors who are offering pureplay outsourcing pharmaceutical contract packaging services across major segments such as Primary, Secondary, and Tertiary. The study also delves into the major trends, regulatory landscape, and key factors shaping the trends related to the contract pharmaceutical packaging market. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the pharmaceutical contract packaging market in terms of drivers and restraints.

The pharmaceutical contract packaging market is segmented by service type (primary [bottles, vials, ampoules, and blister packs, other primary types], secondary, and tertiary) and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Service Type | |||||||

| |||||||

| Secondary | |||||||

| Tertiary |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Pharmaceutical Contract Packaging Market Size Summary

The pharmaceutical contract packaging market is experiencing significant growth, driven by the expanding global pharmaceutical industry and the increasing trend of outsourcing packaging processes. The market is benefiting from the rising demand for efficient and scalable packaging solutions, particularly in the wake of the COVID-19 pandemic, which highlighted the need for rapid and flexible manufacturing capabilities. The shift towards contract packaging is further fueled by the growing number of new drug approvals and the increasing demand for injectables, which are expected to capture a larger market share. This trend is prompting major pharmaceutical companies to invest in expanding their packaging capabilities, particularly in the injectable solutions space, to meet the evolving needs of the market.

In North America, the pharmaceutical contract packaging market is witnessing a surge in the adoption of sustainable and automated packaging solutions, driven by changing consumer preferences and environmental concerns. The region's market growth is also supported by the expansion of biologics and the presence of prominent pharmaceutical vendors and packaging solution providers. Companies are actively investing in expanding their facilities and enhancing their geographical presence through strategic acquisitions and partnerships. The competitive landscape remains fragmented, with numerous vendors vying for market share, leading to strategic collaborations and investments aimed at increasing capacity and improving service offerings. These developments underscore the dynamic nature of the market and the ongoing efforts by key players to capitalize on emerging opportunities.

Pharmaceutical Contract Packaging Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Drivers

-

1.1.1 Ongoing Efforts Toward Serialization to Aid the Market's Growth

-

1.1.2 Recent Capacity Expansions and Investments in Expanding Bottling and Filling Services

-

-

1.2 Market Challenges

-

1.2.1 Stringent Regulatory Requirements

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Service Type

-

2.1.1 Primary

-

2.1.1.1 Bottles

-

2.1.1.2 Vials

-

2.1.1.3 Ampoules

-

2.1.1.4 Blister Packs

-

2.1.1.5 Other Primary Types

-

-

2.1.2 Secondary

-

2.1.3 Tertiary

-

-

2.2 By Geography***

-

2.2.1 North America

-

2.2.2 Europe

-

2.2.3 Asia

-

2.2.4 Australia and New Zealand

-

2.2.5 Latin America

-

2.2.6 Middle East and Africa

-

-

Pharmaceutical Contract Packaging Market Size FAQs

How big is the Pharmaceutical Contract Packaging Market?

The Pharmaceutical Contract Packaging Market size is expected to reach USD 18.15 billion in 2024 and grow at a CAGR of 9.84% to reach USD 29.03 billion by 2029.

What is the current Pharmaceutical Contract Packaging Market size?

In 2024, the Pharmaceutical Contract Packaging Market size is expected to reach USD 18.15 billion.