Market Overview

| Study Period | 2020 - 2031 |

|---|---|

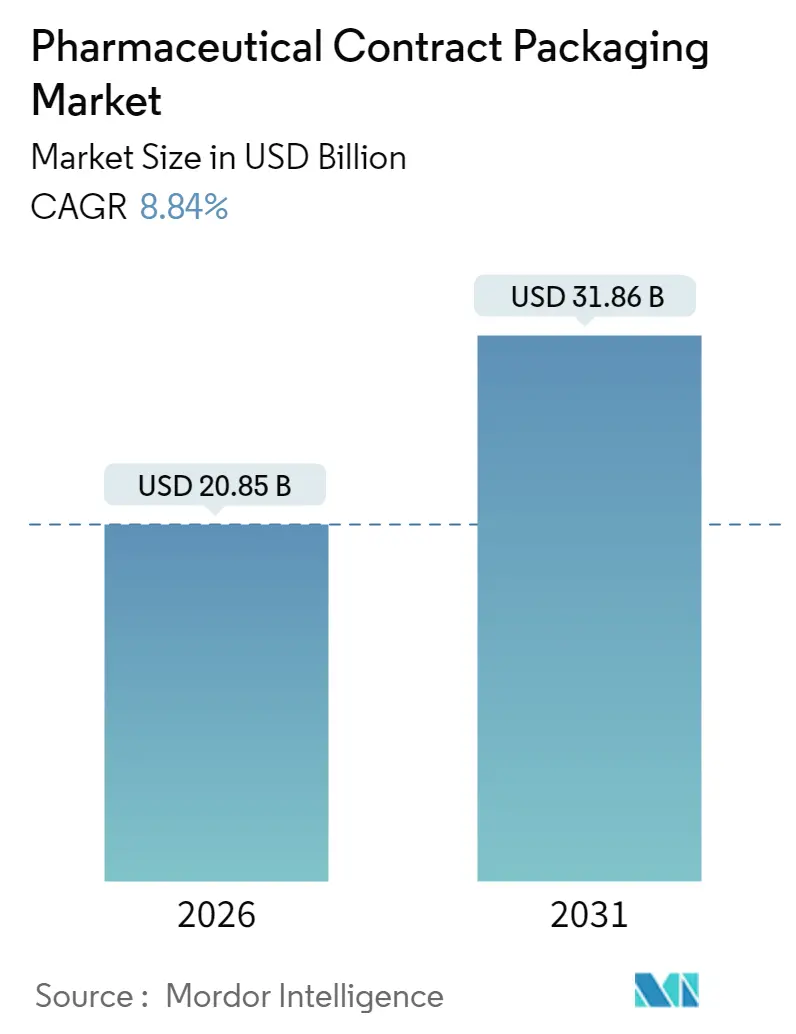

| Market Size (2026) | USD 20.85 Billion |

| Market Size (2031) | USD 31.86 Billion |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

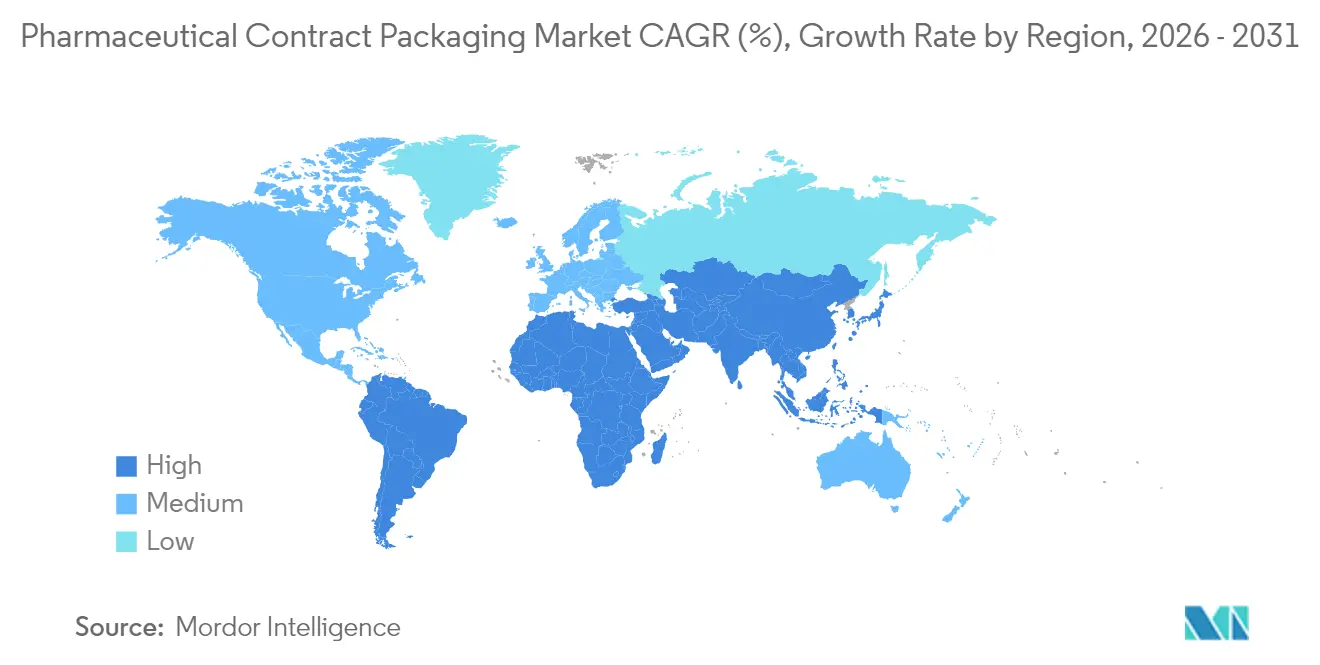

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

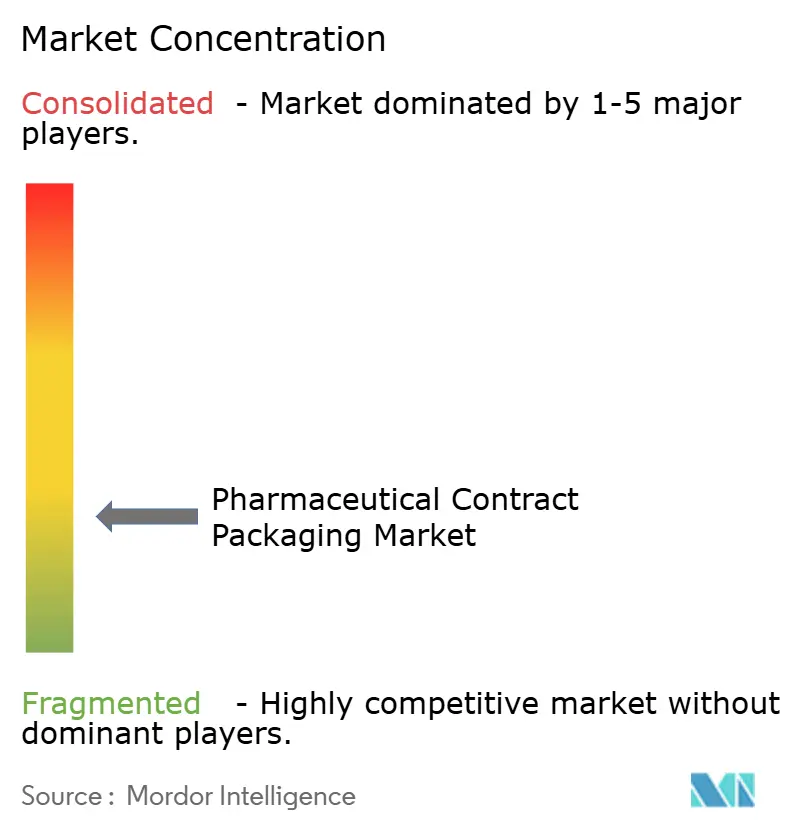

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Contract Packaging Market Analysis by Mordor Intelligence

pharmaceutical contract packaging market size in 2026 is estimated at USD 20.85 billion, growing from 2025 value of USD 19.16 billion with 2031 projections showing USD 31.86 billion, growing at 8.84% CAGR over 2026-2031. Rising serialization mandates, a booming biologics pipeline and growing preference for integrated CDMO models are steering pharmaceutical companies toward outsourced packaging partners that offer deep technical know-how and capital-intensive capabilities. Demand is particularly strong for sterile primary containers, pre-filled delivery devices and track-and-trace ready secondary packs, while AI-enabled changeover systems are trimming validation cycles and boosting line productivity. Regional near-shoring programs in the United States and the European Union are shifting investment priorities, and Asia–Pacific suppliers are scaling capacity to meet export-oriented generic drug growth.

Key Report Takeaways

- By service type, primary packaging held 45.10% of the pharmaceutical contract packaging market share in 2025 and is expanding at a 10.05% CAGR through 2031.

- By packaging format, pre-filled syringes and cartridges recorded the fastest 11.05% CAGR through 2031, while bottles retained 32.10% revenue share in 2025.

- By drug formulation, injectable products captured 10.30% CAGR through 2031, whereas solid dosage forms represented 49.80% of the pharmaceutical contract packaging market size in 2025.

- By End-user, Emerging Biotech and Start-ups recorded the fastest 11.00% CAGR through 2031, while Big Pharma retained 40.05% revenue share in 2025.

- By therapeutic area, oncology packaging commanded 30.20% share and led growth at 12.05% CAGR in 2025.

- By geography, North America accounted for 39.10% share in 2025, but Asia–Pacific is set to grow the fastest at 10.10% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pharmaceutical Contract Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Serialization mandates & anti-counterfeit regulation surge | +2.1% | Global (early gains in US & EU) | Medium term (2–4 years) |

| Biologic & specialty-drug boom amplifying sterile packaging demand | +1.8% | North America & EU; spill-over to APAC | Long term (≥ 4 years) |

| CDMO one-stop-shop preference | +1.4% | Global, strong in North America & APAC | Medium term (2–4 years) |

| Supply-chain near-shoring by Big Pharma | +1.2% | North America & EU | Long term (≥ 4 years) |

| AI-enabled line-changeover efficiency | +0.9% | US, Germany, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Serialization Mandates Drive Unprecedented Packaging Transformation

Full DSCSA enforcement in November 2024 forced contract packagers to embed unique serial numbers, barcodes and aggregation data at every packaging level, transforming legacy lines into data-rich operations that manage and reconcile millions of serial numbers daily. Error-rate spikes of 30% in early roll-outs underscored the need for “Serialization 2.0” platforms with open architectures that remove proprietary hardware lock-ins. Investments in edge-to-cloud line controllers accelerated, and vendors now bundle real-time EPCIS data exchange, enabling downstream wholesalers to verify pack authenticity in seconds. As compliance windows tighten in Italy, Canada and Gulf states, global packagers with harmonized systems gain a competitive edge.

Biologics Surge Reshapes Sterile Packaging Infrastructure

World-wide sterile medicinal product output is climbing at 15% CAGR to 2027, and Annex 1 revisions have elevated contamination control to an enterprise-wide priority. Ready-to-use nested vials, ampoules and polymer syringes eliminate glass washing steps, while modern container-closure integrity testing replaces destructive sterility sampling with helium mass-spectrometry and vacuum decay methods. Automated settle-plate changers, such as Syntegon’s SPC 1000, cut manual interventions by 80% and drive faster batch-release timelines.

CDMO Integration Accelerates End-to-End Service Adoption

The global CDMO market is fueled by brand owners seeking seamless formulation-to-packaging workflows that compress tech-transfer risk CHEManager. PCI Pharma’s USD 365 million multi-site expansion adds high-speed isolator lines and on-body injector assembly cells that enable complex drug-device combination projects PCI Services. Vertical integration pairs formulation scale-up, fill-finish and finishing under one quality system, giving sponsors single-pane-of-glass oversight of CMC milestones.

Supply-Chain Near-Shoring Transforms Geographic Manufacturing Patterns

US federal incentives and bipartisan legislation encourage localized production of essential medicines as pandemic disruptions exposed offshore supply gaps. Novo Nordisk and Eli Lilly together pledged over USD 6 billion for North Carolina expansions that include advanced filling, inspection and carton serialization suites, adding more than 1,600 regional jobs. Similar momentum is evident in Europe, where Vetter’s EUR 1.5 billion dual-site program doubles injectable capacity and embeds cold-chain qualified secondary packaging cells.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving global track-and-trace standards raise compliance costs | –1.6% | Global, highest in regulated markets | Medium term (2–4 years) |

| Poly-material sustainability rules squeeze margin on plastics | –1.2% | EU; expanding to North America & APAC | Long term (≥ 4 years) |

| Qualified labor shortage for high-speed sterile lines | –0.8% | Advanced manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Track-and-Trace Compliance Costs Strain Operational Margins

Divergent serial data formats across markets oblige packagers to operate multi-schema IT stacks, inflating validation and support budgets by up to 20% per multi-market SKU. Italy’s February 2025 go-live for EU FMD aggregation illustrates the continuing regulatory drumbeat that forces line retrofits and warehouse upgrades.

Skilled Labor Shortage Constrains Sterile Manufacturing Expansion

ISPE surveys show 80% of facilities struggle to recruit validation engineers, microbiologists and automation specialists, delaying new line qualifications. [1]ISPE Authors, “Futureproofing US Pharma Manufacturing Jobs,” ispe.org NIIMBL warns of a 35% talent deficit by 2030, prompting firms to deploy collaborative robots and digital twin training platforms to bridge gaps.

Segment Analysis

By Service Type: Primary Packaging Commands Regulatory Focus

Primary packaging held a 45.10% share of the pharmaceutical contract packaging market in 2025 and is expanding at 10.05% CAGR as drug-contact materials face tighter leachables and extractables scrutiny.Type I borosilicate glass vials, cyclic olefin polymer cartridges and high-barrier blister films dominate investment plans because they assure chemical compatibility for biologics. Growth momentum also reflects mandatory unit-level serialization, which starts at the primary layer in many jurisdictions.

Sterile container-closure innovation is redefining competitive positioning. Contract packagers now validate package integrity using laser-based headspace analysis and helium mass-spectrometry, reducing destructive testing waste while meeting Annex 1 expectations. Secondary and tertiary services continue to add value through late-stage custom kitting and specialty cold-chain logistics, yet regulatory complexity keeps the revenue center anchored in the primary tier.

By Packaging Format: Pre-Filled Systems Lead Patient-Centric Shift

Bottles remain the largest format owing to oral solid dosage dominance. However, pre-filled syringes and cartridges show 11.05% CAGR through 2031, making them the fastest-expanding slice of the pharmaceutical contract packaging market. Demand is fuelled by self-injection biologics, pen-injector proliferation and hospital safety mandates that curb needle handling.

Technical advances in cyclic olefin polymer barrels improve drug stability and window clarity, while needle-safety shields and electronic dose counters embed usability features once reserved for device makers. Contract packagers offering integrated plunger placement, nitrogen purging and auto-injector assembly services secure long-term supply agreements with specialty-pharma clients seeking turnkey solutions.

By Drug Formulation: Injectables Accelerate on Specialty Therapy Wave

Solid dosage products represented 49.80% of the pharmaceutical contract packaging market size in 2025, yet injectable formulations are climbing at 10.30% CAGR through 2031. Complex biologics, radioligand therapies and GLP-1 agonists dominate the NME pipeline, steering capex toward glass-to-polymer conversion projects and 100% in-line visual inspection upgrades.

Cold-chain intensity and sterility standards raise entry barriers, prompting sponsors to outsource fill-finish to experienced sites with isolator lines, grade A-RABS zones and redundant freeze-dryers. Emerging laser-etched 2D barcodes on vial bottoms enable end-to-end traceability without label obfuscation, further differentiating premium service providers.

By Therapeutic Area: Oncology Packaging Outpaces All Segments

Oncology commanded 30.20% share and posted a 12.05% CAGR in 2025, topping both revenue and growth charts. Cytotoxic handling protocols, time-sensitive radiopharmaceuticals and cold-chain biologics elevate packaging complexity, making specialized barrier isolators and rapid logistics indispensable.

High-value individualized therapies, such as CAR-T cells, demand frozen shippers with real-time GPS-temperature telemetry and tamper-evident seals. Contract packagers with integrated labeling, kitting and last-mile distribution solutions capture premium margins by ensuring chain-of-identity and chain-of-custody compliance across global study sites.

By End-User: Emerging Biotech Fuels Outsourcing Momentum

Large pharmaceutical companies retained 40.05% revenue in 2025, yet emerging biotech firms are the fastest-growing customer class at 11.00% CAGR through 2031. Venture-backed innovators leverage outsourced models to preserve cash while accessing GMP infrastructure on demand.

Hybrid CDMO platforms bundle formulation development, toxicology batch production and commercial packaging under one QMS, reducing hand-offs that can extend timelines. Flexible capacity, pay-as-you-grow pricing and regulatory mentoring appeal to small teams navigating first-in-human studies. Generics players also tap contract packaging to streamline multi-market launches amid tightening cost controls.

Geography Analysis

North America generated 39.10% of 2025 revenue, supported by FDA serialization mandates, strong biologics pipelines and sizeable near-shoring capital flows. Investments such as Novo Nordisk’s USD 4.1 billion Clayton complex embed fill-finish, inspection and final assembly under one roof, shortening supply lines and augmenting domestic resiliency. Canada’s sterile-drug corridor in Ontario and Mexico’s maquiladora expansions complement US capacity, enabling duty-efficient cross-border flows that satisfy regional content stipulations.

Europe remains an innovation hub, driven by PPWR sustainability rules that accelerate material R&D and by Annex 1 sterile guidelines demanding best-in-class cleanroom performance. Germany’s engineering ecosystem anchors high-precision equipment supply, while Italy and France host seasoned fill-finish sites catering to orphan-drug runs. United Kingdom packagers pivot toward advanced therapy applications, leveraging MHRA agility post-Brexit to attract global clinical programs.

Asia–Pacific shows the fastest 10.10% CAGR as Chinese and Indian CDMOs scale capacities that align with generics booms and biosimilar roll-outs. Japan pioneers high-speed robotics in vial filling, South Korea spearheads antibody-drug conjugate projects and Singapore extends tax incentives for cell-therapy facilities. Regional governments nurture GMP convergence under PIC/S, easing multi-country approvals and encouraging cross-border supply networks. Australia and New Zealand contribute niche sterile development services, reinforcing the region’s climb up the value chain.

Competitive Landscape

Moderate fragmentation defines the pharmaceutical contract packaging market as scale and technology requirements intensify. Novo Holdings’ USD 16.5 billion Catalent takeover, paired with Novo Nordisk’s USD 11 billion site purchase, created the sector’s largest vertically aligned entity and signaled rising appetite for integrated capacity. PCI Pharma’s facility roll-outs and acquisition of Ajinomoto Althea underscore a race to build drug-device combination depth.

Technology differentiation widens competitive gaps. Syntegon’s AI-driven aseptic lines cut touchpoints by 80%, boosting uptime for cytotoxic fills. Vetter’s dual-continent expansion embeds redundant lines for GLP-1 agonist auto-injectors, attracting blockbuster sponsors seeking risk-shared supply continuity. Niche CDMOs carve white-space in radioligand therapy packs, where six-hour isotope half-lives reward hyper-responsive logistics setups.

Price competition is giving way to capability-based selection as sponsors prioritize compliance assurance, injectables expertise and digital supply-chain visibility. Mid-tier players leverage flexible batch sizes and high-mix agility to court emerging biotechs, while global conglomerates invest in data lakes and predictive analytics to anchor multi-year master-service agreements.

Pharmaceutical Contract Packaging Industry Leaders

Ropack Inc.

Reed-Lane Inc.

PCI Pharma Services

Silgan Unicep (Silgan Dispensing Systems)

Sharp Services, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Novo Holdings completed the USD 16.5 billion acquisition of Catalent, while Novo Nordisk bought three Catalent fill-finish sites for USD 11 billion.

- October 2024: Syntegon finalized its merger with Telstar, integrating aseptic processing and packaging equipment portfolios.

- September 2024: PCI Pharma Services announced a USD 365 million US–EU expansion focused on advanced injectables and drug-device systems.

- June 2024: Vetter Pharma disclosed EUR 1.5 billion investments in Illinois and Saarlouis to double injectable capacity

Global Pharmaceutical Contract Packaging Market Report Scope

The study on the Pharmaceutical Contract Packaging market tracks demands in terms of revenue for vendors who are offering pureplay outsourcing pharmaceutical contract packaging services across major segments such as Primary, Secondary, and Tertiary. The study also delves into the major trends, regulatory landscape, and key factors shaping the trends related to the contract pharmaceutical packaging market. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the pharmaceutical contract packaging market in terms of drivers and restraints.

The pharmaceutical contract packaging market is segmented by service type (primary [bottles, vials, ampoules, and blister packs, other primary types], secondary, and tertiary) and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Primary | Bottles |

| Vials and Ampoules | |

| Blister Packs | |

| Secondary | Cartons |

| Labels and Inserts | |

| Tertiary |

By Packaging Format

| Bottles | Plastic Bottles |

| Glass Bottles | |

| Vials and Ampoules | |

| Blister Packs | |

| Sachets and Stick Packs | |

| Pre-filled Syringes and Cartridges |

By Drug Formulation

| Solid Dosage | Tablets |

| Capsules | |

| Oral Liquids | |

| Injectable | Small-volume Parenterals |

| Large-volume Parenterals |

By Therapeutic Area

| Oncology |

| Cardiovascular |

| CNS |

| Infectious Disease |

| Other Therapeutic Areas |

By End-user

| Big Pharma (>USD 10 bn revenue) |

| Generics/Biosimilar Companies |

| Emerging Biotech and Start-ups |

| CRO/CDMO Partners |

| Others End-user |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Service Type | Primary | Bottles | |

| Vials and Ampoules | |||

| Blister Packs | |||

| Secondary | Cartons | ||

| Labels and Inserts | |||

| Tertiary | |||

| By Packaging Format | Bottles | Plastic Bottles | |

| Glass Bottles | |||

| Vials and Ampoules | |||

| Blister Packs | |||

| Sachets and Stick Packs | |||

| Pre-filled Syringes and Cartridges | |||

| By Drug Formulation | Solid Dosage | Tablets | |

| Capsules | |||

| Oral Liquids | |||

| Injectable | Small-volume Parenterals | ||

| Large-volume Parenterals | |||

| By Therapeutic Area | Oncology | ||

| Cardiovascular | |||

| CNS | |||

| Infectious Disease | |||

| Other Therapeutic Areas | |||

| By End-user | Big Pharma (>USD 10 bn revenue) | ||

| Generics/Biosimilar Companies | |||

| Emerging Biotech and Start-ups | |||

| CRO/CDMO Partners | |||

| Others End-user | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current pharmaceutical contract packaging market size?

The pharmaceutical contract packaging market size stood at USD 20.85 billion in 2026 and is projected to reach USD 31.86 billion by 2031.

Which segment is growing the fastest within the pharmaceutical contract packaging market?

Pre-filled syringes and cartridges lead with an 11.05% CAGR through 2031 due to the rise of self-administered biologics.

Why are serialization mandates important to the pharmaceutical contract packaging industry?

Global track-and-trace laws such as the US DSCSA require unique serial numbers on every saleable unit, driving investment in sophisticated data-ready packaging lines.

Which region shows the highest future growth for pharmaceutical contract packaging services?

Asia–Pacific is forecast to grow at 10.10% CAGR through 2031 as China and India expand generic and biosimilar output.

How are sustainability regulations affecting pharmaceutical contract packaging?

EU PPWR 2025/40 requires full recyclability by 2030, pushing converters toward mono-material designs and recycled-content plastics.

What is the outlook for oncology packaging within the pharmaceutical contract packaging market?

Oncology holds the largest revenue share at 30.20% and is advancing at a 12.05% CAGR, driven by specialized handling needs for cytotoxic and radioligand therapies.

Page last updated on: