Market Size of Pharmaceutical CMO Industry

| Study Period | 2019 - 2029 |

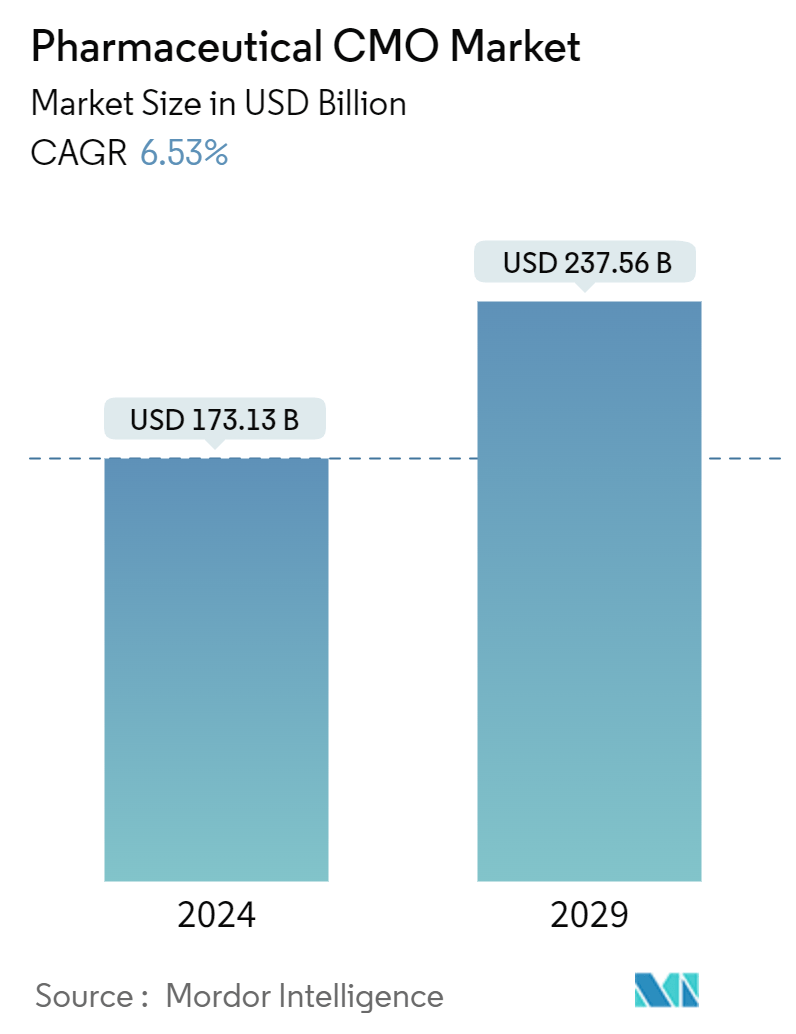

| Market Size (2024) | USD 173.13 Billion |

| Market Size (2029) | USD 237.56 Billion |

| CAGR (2024 - 2029) | 6.53 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Pharmaceutical CMO Market Analysis

The Pharmaceutical CMO Market size is estimated at USD 173.13 billion in 2024, and is expected to reach USD 237.56 billion by 2029, growing at a CAGR of 6.53% during the forecast period (2024-2029).

Advanced manufacturing technologies and processes are expected to contribute to the growth of the CMO market. CMOs can optimize their manufacturing processes and reduce waste and costs through new operational strategies, including continuous manufacturing. Small and mid-sized pharma companies, which account for an increasing share of new drug approvals and often lack manufacturing capacity, are expected to drive CMOs to adopt new manufacturing technologies.

- One of the main reasons for outsourcing pharmaceuticals is cost. Outsourcing gives companies access to specialized knowledge and tools at a fraction of the cost of maintaining internal capabilities, lowering operating costs and capital expenditures. Also, CMOs are expanding their capacity by purchasing manufacturing facilities from drug manufacturers, owing to the increasing demand.

- CMOs can scale up the expansion of their capabilities quickly through acquisitions. This shift in focus was accompanied by a change in the market's M&A landscape. For instance, developing novel therapeutic modalities (such as cell, gene, or mRNA therapies) and advanced vaccines over the past decade necessitated a sizable investment in new manufacturing facilities for nucleic acids, lipid-based formulations, viral vectors, and cell manipulation.

- For instance, FUJIFILM Diosynth Biotechnologies, a contract development and manufacturing organization for biologics and advanced therapies, recently held a ceremony to mark the beginning of its single-use manufacturing campus expansion project in Texas. The expansion will add a cGMP production facility that will be operational by 2024. The growth will double the Company's advanced therapy and vaccine manufacturing capacity in the United States.

- Additionally, pharmaceutical companies have been directing their priorities toward the core areas of competency. Hence, they prefer not to dispense available resources, expertise, and technology in formulating the final dose of medicines. The increased competition and shrinking profit margins compelled the pharmaceutical companies to revisit their production processes and R&D activities instead of manufacturing the formulated drug to stay competitive in the market.

- The growing geriatric population and increasing development and investment in the active pharmaceutical ingredients (APIs) market are propelling the growth of the biopharmaceutical industry. The prevalence of chronic diseases such as cardiovascular disease and cancer will also contribute to API growth. With the ongoing growth in the pharmaceutical sector, pharmaceutical innovator companies need to stock their pipelines with new drugs. However, they do not have the resources to discover, develop, and manufacture products. Hence, the requirement for CMOs is quite significant.

- Further, countries, such as China, India, and Japan, hold a significant share of the pharmaceutical CMO market, owing to low labor costs, low capital and overhead costs (compared to that of the United States and Europe), tax incentives, and undervalued currency combine that provides a significant cost advantage for pharmaceutical companies outsourcing to these countries.

- Investing in research and development (R&D) is becoming expensive, but the valuable outcomes are becoming less and less common. Many companies realize that outsourcing this part of their business while capitalizing on emerging pharmaceutical markets is the best way to reduce costs. Despite all the evidence of cost savings and the skills that can be gained, many companies don’t want to give up control. However, the situation is changing. The pressure to shorten supply chains and optimize lead time is forcing companies to take a variety of measures to meet demand, making contract manufacturing a bottleneck in their supply chain.

Pharmaceutical CMO Industry Segmentation

The study tracks and analyzes the demand for outsourcing CMO activities within the pharmaceutical industry based on current trends and market dynamics. The market numbers are derived by tracking the revenue generated by the players operating in the market who are providing CMO services. The study provides a detailed breakdown of the various types of service types. This report analyzes the factors based on the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The pharmaceutical CMO market is segmented by service type (active pharmaceutical ingredient (API) manufacturing (small molecule, large molecule, and high potency API (HPAPI)), finished dosage formulation (FDF) development and manufacturing (solid dose formulation (tablets and others), liquid dose formulation, and injectable dose formulation), and secondary packaging) and geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, Italy, Spain, and Rest of Europe), Asia Pacific (China, India, Japan, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, Argentina, and Rest of Latin America), Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Service Type | ||||||||

| ||||||||

| ||||||||

| Secondary Packaging |

| By Geography*** | |||||||

| |||||||

| |||||||

| |||||||

| Australia and New Zealand | |||||||

| |||||||

|

Pharmaceutical CMO Market Size Summary

The Pharmaceutical CMO market is poised for significant growth, driven by advancements in manufacturing technologies and processes. Contract Manufacturing Organizations (CMOs) are increasingly adopting new operational strategies, such as continuous manufacturing, to optimize processes and reduce costs. This trend is particularly beneficial for small and mid-sized pharmaceutical companies that are gaining a larger share of new drug approvals but often lack the necessary manufacturing capacity. The outsourcing of pharmaceutical production is primarily motivated by cost efficiency, as it allows companies to leverage specialized knowledge and tools without the overhead of maintaining internal capabilities. The expansion of CMO capacities through acquisitions and the development of new manufacturing facilities are key strategies to meet the rising demand, especially in the biopharmaceutical sector.

The market landscape is characterized by a shift towards high-potency active pharmaceutical ingredients (APIs) and biologics innovation, driven by the increasing prevalence of chronic diseases and a growing geriatric population. Countries like China, India, and Japan are significant players in the CMO market due to their cost advantages, including low labor and capital costs. The United States remains a major market, with CMOs expanding their capabilities to meet the demands of a robust pharmaceutical industry. However, regulatory challenges in regions like Europe could impact market growth. The competitive landscape is fragmented, with major players focusing on providing comprehensive services to maintain a competitive edge. Recent mergers and acquisitions, such as Catalent Inc.'s acquisition by Novo Holdings, highlight the ongoing consolidation and strategic partnerships within the industry.

Pharmaceutical CMO Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness-Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Intensity of Competitive Rivalry

-

1.2.5 Threat of Substitute Products

-

-

1.3 Industry Value Chain Analysis

-

1.4 Industry Policies

-

-

2. MARKET SEGMENTATION

-

2.1 By Service Type

-

2.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

-

2.1.1.1 Small Molecule

-

2.1.1.2 Large Molecule

-

2.1.1.3 High Potency API (HPAPI)

-

-

2.1.2 Finished Dosage Formulation (FDF) Development and Manufacturing

-

2.1.2.1 Solid Dose Formulation

-

2.1.2.1.1 Tablets

-

2.1.2.1.2 Other Types (Capsules, Powders, etc.)

-

-

2.1.2.2 Liquid Dose Formulation

-

2.1.2.3 Injectable Dose Formulation

-

-

2.1.3 Secondary Packaging

-

-

2.2 By Geography***

-

2.2.1 North America

-

2.2.1.1 United States

-

2.2.1.2 Canada

-

-

2.2.2 Europe

-

2.2.2.1 United Kingdom

-

2.2.2.2 Germany

-

2.2.2.3 France

-

2.2.2.4 Italy

-

2.2.2.5 Spain

-

-

2.2.3 Asia

-

2.2.3.1 China

-

2.2.3.2 India

-

2.2.3.3 Japan

-

2.2.3.4 Australia

-

-

2.2.4 Australia and New Zealand

-

2.2.5 Latin America

-

2.2.5.1 Brazil

-

2.2.5.2 Mexico

-

2.2.5.3 Argentina

-

-

2.2.6 Middle East and Africa

-

2.2.6.1 United Arab Emirates

-

2.2.6.2 Saudi Arabia

-

2.2.6.3 South Africa

-

-

-

Pharmaceutical CMO Market Size FAQs

How big is the Pharmaceutical CMO Market?

The Pharmaceutical CMO Market size is expected to reach USD 173.13 billion in 2024 and grow at a CAGR of 6.53% to reach USD 237.56 billion by 2029.

What is the current Pharmaceutical CMO Market size?

In 2024, the Pharmaceutical CMO Market size is expected to reach USD 173.13 billion.