| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| CAGR | 13.49 % |

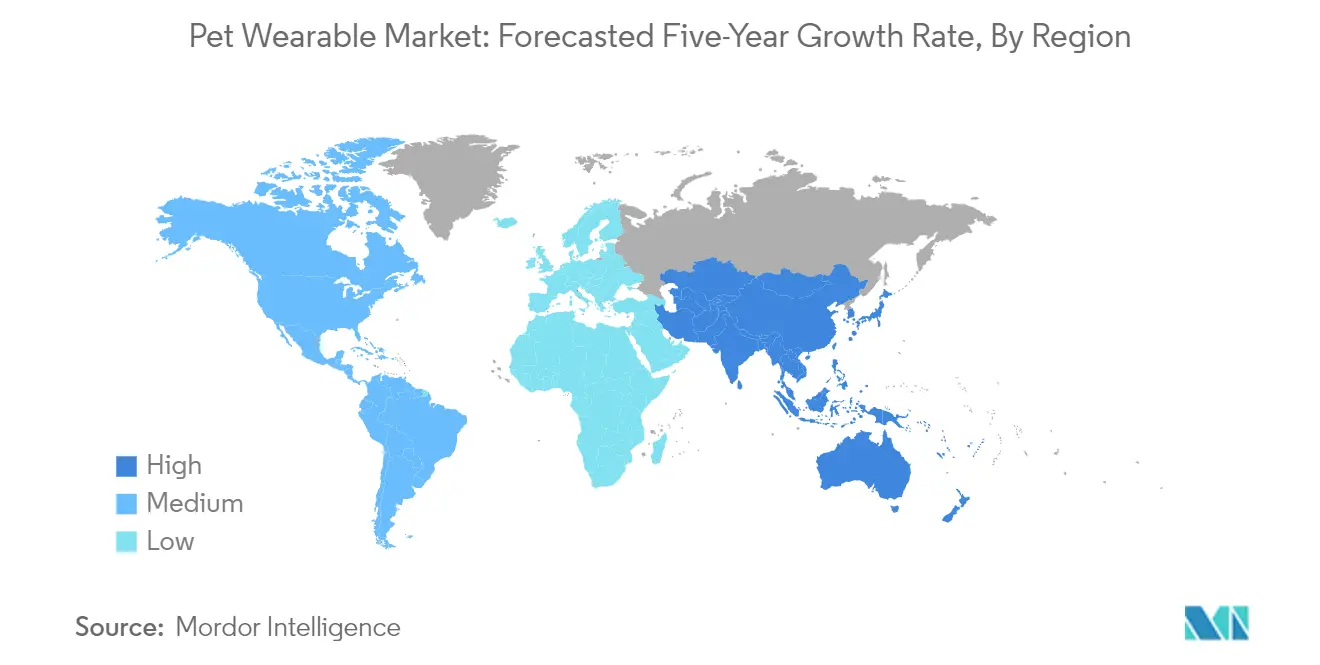

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Pet Wearable Market Analysis

The Pet Wearable Market is expected to register a CAGR of 13.49% during the forecast period.

The Security Challenge Creating Opportunities in Pet Wearable Technology

The pet wearable industry faces a pressing security challenge: as devices become more advanced, they create new privacy risks for pet owners. A 2022 study across three countries involving 593 participants showed significant gaps in how users understand and implement security measures for their pet tech devices. This gap between technological advancement and security awareness creates a market vulnerability that companies need to address. A related 2023 study found that 521 participants recognized potential security threats but often didn't take proper precautions. For manufacturers, this presents both a problem and an opportunity - they can develop better security features while helping consumers understand how to use them. The solution requires both technical improvements and better consumer education, with companies creating user-friendly security systems and being transparent about how they handle data. The future success of the pet wearable market depends not just on what devices can do but on building consumer trust through a demonstrated commitment to privacy and security. Companies that tackle these concerns head-on will likely gain more market share as security-conscious consumers become more deliberate in their purchasing decisions.

New Business Opportunities Beyond Traditional Pet Care

The pet wearable market is expanding beyond its original boundaries, creating new partnership opportunities across previously separate industries. The PETBIZ G1 tracker gained over 50,000 customers worldwide within just one year after its development, showing strong market demand for multi-purpose solutions. This integration is changing business models across several sectors: insurance companies now offer discounts for owners using approved pet health monitoring devices, veterinary practices incorporate wearable data into health records, and retail chains develop connected product ecosystems. Forward-thinking companies are now creating comprehensive pet care platforms instead of standalone products. Subscription models that combine hardware, software, and services are proving attractive to both consumers and investors. The key lesson for businesses is clear: success in the pet wearable industry requires looking beyond manufacturing to build partnerships across the broader pet care landscape. Companies that can create seamless experiences across different pet care services will secure leading positions as the market develops beyond its current product focus.

Innovation in Pet Health Monitoring is Reshaping the Market

The pet wearable market is evolving from simple location tracking to advanced health management systems. This shift is backed by growing evidence highlighting the importance of proactive health monitoring. A 2023 study found that obesity in dogs reduces life expectancy by approximately 1.5 years compared to dogs with healthy weight - exactly the type of condition that modern pet health monitoring devices can help manage through activity tracking and feeding guidance. Research about breed-specific health issues - such as the 2024 United Kingdom study of 584,734 dogs that challenged traditional beliefs about mixed-breed longevity - is leading to more specialized features in new devices. These health insights are pushing product development beyond one-size-fits-all approaches, with manufacturers increasingly designing smart-connected pet collars for specific health conditions, breed characteristics, and age-related needs. The key takeaway for industry players is clear: health-focused features offer the best opportunity for standing out in a crowded market. Companies that can translate veterinary knowledge into practical, actionable insights for pet owners will establish premium market positions while helping improve the quality of life for pets.

Pet Wearable Market Trends

The Wellness Wave: Pet Parents Embrace Tech-Driven Health Monitoring

Today's pet owners have evolved beyond basic care, increasingly viewing themselves as holistic guardians of their companions' physical and mental well-being. This shift has created fertile ground for pet wearable devices that monitor everything from activity levels to sleep patterns. The innovation trajectory is evident in recent technological breakthroughs, such as the 2024 patent from Shenzhen Diai Intelligence Technology for advanced dog training devices that integrate with broader health monitoring ecosystems. These developments aren't merely gadgets but comprehensive wellness solutions that connect directly to the wider Internet of Things (IoT) landscape, allowing pet parents to make data-driven decisions about exercise, diet, and behavioral interventions.

The convergence of pet wellness awareness and IoT adoption has fundamentally altered consumer expectations across the pet wearable industry. Modern pet parents now demand devices that not only track location but provide actionable insights into their companions' health metrics. This dual-focused approach—physical tracking coupled with behavioral analysis—addresses the growing recognition that pets, like humans, benefit from preventative health monitoring and early intervention. Companies that successfully bridge this gap between fitness tracking and mental wellness monitoring while maintaining seamless IoT integration will capture the most valuable segments of this growing market, particularly among millennial and Gen Z (Generation Z or Zoomer) pet parents who prioritize comprehensive health solutions.

Always Connected: The Rising Demand for Round-the-Clock Pet Visibility

The contemporary pet owner's desire to maintain a constant connection with their companions has catalyzed unprecedented growth in monitoring solutions. This trend reflects more profound societal shifts toward viewing pets as family members deserving of the same care and attention as human dependents. Pet tracking systems have become essential tools for this new generation of owners, with companies like Tractive expanding operations to over 175 countries and partnering with more than 500 connectivity providers to ensure global coverage. This extensive infrastructure development underscores how monitoring has transitioned from luxury to necessity as pet parents increasingly expect uninterrupted visibility into their companions' whereabouts and activities.

The monitoring revolution extends beyond simple location tracking to encompass comprehensive surveillance solutions. The pet monitoring camera industry has responded with increasingly sophisticated offerings that provide not just visual confirmation but interpretive data about animal behavior and wellbeing. Manufacturers are addressing the primary barriers to adoption by focusing on core consumer pain points, as evidenced by innovations like the PETBIZ G1 GPS (Global Positioning System) Pet Tracker with its industry-leading 30-day battery life. This performance breakthrough resolves one of the most persistent frustrations for users of pet health monitoring devices while simultaneously increasing the practical utility of continuous monitoring. Companies that can further extend battery life while adding meaningful monitoring capabilities will capture significant market share in this rapidly expanding sector.

Engineering the Future: How Technical Innovation Propels Pet Wearables Forward

The pet wearable market is experiencing an innovation surge driven by rapid advancements in sensor technology, connectivity standards, and data analytics capabilities. This technical evolution is transforming basic tracking devices into sophisticated health management platforms. Patent developments highlight this acceleration, with innovations like the wireless remote control dog training devices (Patent USD963966S1) published in 2022 illustrating how quickly technology is advancing in response to consumer demand. These technical leaps have enabled manufacturers to create increasingly multifunctional devices that combine tracking, training, and health monitoring in single, user-friendly packages that offer unprecedented value to pet owners.

Battery performance and data efficiency have emerged as critical competitive differentiators in the pet tech market. Innovative systems now offer selectable check-in intervals of 3, 6, 10, or 30 minutes, allowing users to balance real-time monitoring needs with power conservation. This flexibility represents a significant advance in device usability, addressing the fundamental tension between information density and operational longevity. The technical challenges of miniaturization while maintaining battery capacity continue to drive research and development priorities across the industry. Manufacturers who successfully navigate the trade-offs between form factor, functionality, and power requirements will establish themselves as leaders in the next generation of pet wearable devices market, particularly as consumers increasingly expect performance parity with human wearable technology.

Segment Analysis: By Product

Smart Collar: The Cornerstone of Pet Wearable Technology

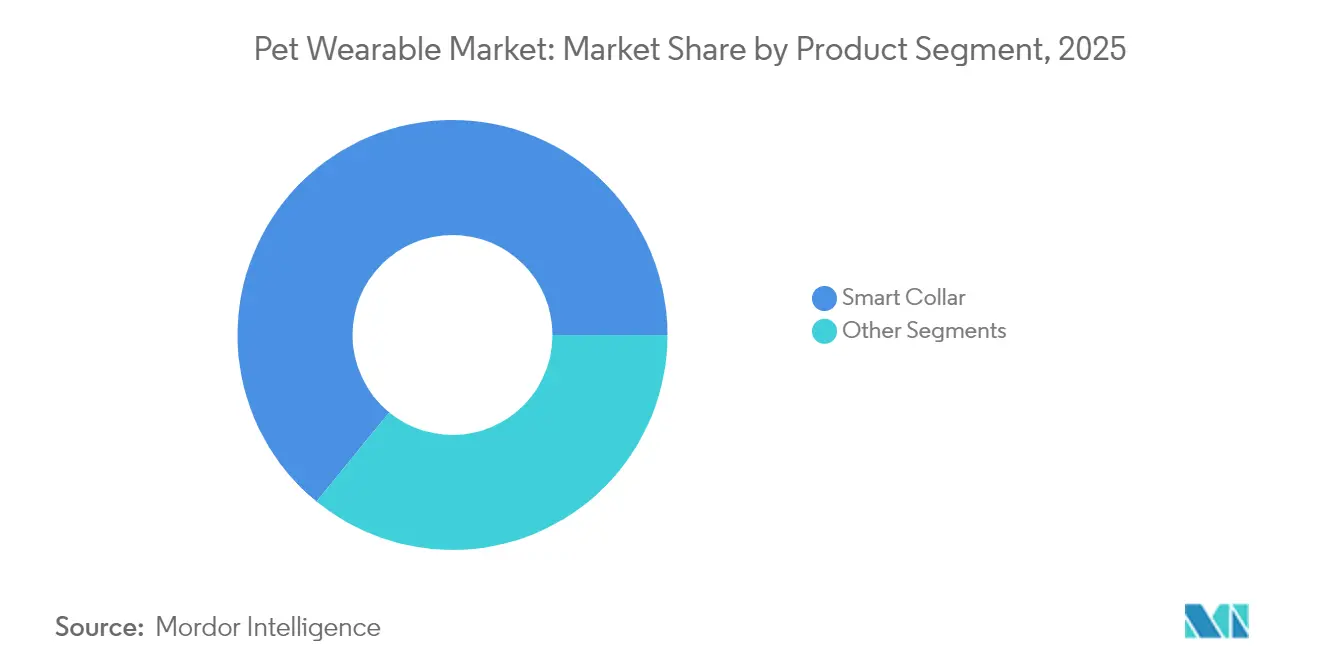

Smart collars dominate the pet wearable landscape with a commanding 64.10% market share, reflecting their position as the cornerstone technology in pet monitoring solutions. These devices have evolved from simple identification tools to sophisticated health and location tracking platforms that resonate with pet owners seeking comprehensive oversight. The Fi smart collar exemplifies this evolution, offering an impressive two-month battery life alongside IP68 dust and water resistance and a chew-proof stainless steel design that withstands the rigors of active pet lifestyles. For manufacturers, this overwhelming market preference signals the critical importance of investing in collar-based innovation—particularly in extending battery performance and enhancing durability—as the foundation for capturing market share in the expanding pet wearable market ecosystem.

Smart Cameras: Visual Monitoring Driving Next-Generation Growth

Smart cameras are rapidly transforming the pet monitoring landscape, advancing at a CAGR of 15.93% as pet owners increasingly seek comprehensive visual oversight of their companions while away. This accelerated growth stems from technological innovations like the SMARTPAW Pet Camera Eyepet3, which delivers FHD (Full High-definition) 1980 x 1080 resolution with effective night vision capability, ensuring clear monitoring regardless of lighting conditions. The combination of 140° wide-angle lenses with full 360° horizontal rotation and 90° vertical tilt functionality offers unprecedented coverage that addresses the fundamental anxiety of pet parents—the need to maintain visual connection with their animals throughout the day. Companies that prioritize advanced imaging capabilities, seamless mobile integration, and pet-specific AI (artificial intelligence) features will be best positioned to capitalize on this high-growth segment that bridges technology and emotional reassurance.

Diversified Wearable Solutions: Harnesses, Vests, and Specialized Designs

The diversity beyond primary tracking devices reveals a maturing ecosystem adapting to specialized pet needs and owner preferences. Smart harnesses and vests offer alternatives for pets that may not tolerate collars, while enabling more comprehensive biometric monitoring through increased body contact. The innovation in these supplementary categories often focuses on solving specific challenges—whether addressing the unique physiology of certain breeds or enabling data collection for veterinary purposes. The Tractive platform demonstrates this specialized approach, offering distinct solutions optimized for different animals, with the DOG tracker providing up to 14 days of battery life while the CAT tracker is designed with a 7-day battery life in a smaller form factor suited to feline comfort. For industry stakeholders, these emerging niches represent strategic opportunities to develop purpose-built solutions that complement the mainstream market while addressing unmet needs that traditional products overlook.

Segment Analysis: By Application

Identification and Tracking: The Foundation of Pet Wearable Adoption

Identification and tracking applications command 64.10% of the pet wearable market, establishing themselves as the foundational use case driving consumer adoption across the ecosystem. This dominance reflects the primal concern of pet owners—preventing loss and facilitating recovery—that motivates initial purchases before owners explore additional functionalities. The Tabcat Cat Tracker V2 illustrates this focused approach, offering location tracking accuracy within an inch while maintaining a lightweight design of just 0.2 ounces that prioritizes feline comfort. The sustained market leadership of this application category signals to manufacturers and developers that while diversification into health monitoring and behavior analysis creates differentiation, the core tracking functionality remains the essential purchase driver—suggesting that innovations enhancing location accuracy, expanding range, and improving reliability will continue to yield the most significant market returns.

Medical Diagnosis: Healthcare Applications Accelerating Market Evolution

Medical diagnosis and treatment applications are experiencing remarkable momentum, achieving a CAGR of 16.66% as the pet wearable industry evolves beyond basic tracking toward comprehensive health monitoring. This acceleration stems from the convergence of veterinary expertise with consumer technology, creating devices that can detect subtle physiological changes before visible symptoms appear. The Pawfit 3 exemplifies this evolution, offering advanced health monitoring capabilities in a 100% waterproof design that ensures continuous data collection regardless of environmental conditions. For stakeholders across the value chain—from device manufacturers to veterinary services—this growth trajectory signals the critical importance of developing clinical-grade sensors and establishing partnerships with veterinary professionals to validate measurement accuracy and develop actionable health insights that transform raw data into preventative care recommendations.

Behavioral Management and Interactive Control Features

Beyond the primary use cases, monitoring and control applications along with emerging specialized functions are expanding the value proposition of pet wearable devices. These applications transform passive data collection into active management tools that shape pet behavior, optimize feeding schedules, and facilitate remote interaction. The ability to create virtual boundaries, as demonstrated by the Pawfit 3's capability to set up 10 invisible fences, illustrates how these applications bridge digital monitoring with physical space management—a particularly valuable feature for urban pet owners with limited outdoor areas. For manufacturers, these supplementary applications represent crucial opportunities for differentiation in an increasingly crowded market, where the integration of multiple functionalities within a single device ecosystem creates compelling upgrade paths for existing customers while attracting new segments previously unconvinced by single-purpose solutions.

Segment Analysis: By Animal Type

Canine Solutions: Dogs Lead Market Size and Growth Trajectory

Dogs represent both the most prominent segment at 62.46% market share and the fastest-growing category with a 17.70% CAGR in the pet wearable market, reflecting both their prevalence in households and their owners' greater propensity to invest in technological solutions. This dual dominance stems from canines' more active outdoor lifestyles that heighten loss concerns, coupled with broader size ranges that accommodate larger devices with enhanced capabilities and battery performance. The market has responded with dog-specific innovations like the Tractive DOG XL tracker, designed to operate for up to a month on a single charge—significantly outperforming standard pet wearables and addressing a critical pain point for active dog owners. For industry players, this concentration of market value and growth potential indicates that dog-focused product development should remain the strategic priority, with emphasis on ruggedized designs, outdoor performance, and activity-specific features that align with the diverse activities dogs engage in with their owners.

Specialized Design for Cats and Exotic Companions

Cats and exotic pets present distinct challenges and opportunities that require fundamentally different approaches to pet wearable design and functionality. The feline segment demands miniaturization and ultra-lightweight construction, exemplified by the Tractive CAT Mini priced at 49 €—designs that prioritize comfort and minimal interference with natural behaviors over extended feature sets. This balance between functionality and form factor reflects cats' notorious sensitivity to wearing devices and their smaller frames that cannot accommodate the larger batteries and sensors used in dog products. For manufacturers targeting these specialized segments, success hinges on addressing species-specific behaviors and physiological characteristics rather than downsizing existing dog-oriented solutions. Companies that develop intuitive interfaces tailored to indoor monitoring (for cats) or specialized environmental tracking (for exotic pets) can establish defensible positions in these underserved niches where generic solutions consistently fall short of owner expectations.

Geography Analysis

North America: Command Central of Pet Tech Innovation

North America will lead the pet wearable market with a dominant 39.56% share of the global market in 2025. This region's success stems from high pet ownership rates, tech-savvy consumers, and substantial spending on pet health and wellness. The region's strong pet humanization trend—where pets are increasingly treated as family members—drives demand for advanced monitoring solutions. Garmin's strategic expansion of its Alpha LTE coverage to North America in July 2024 underscores the region's importance to major manufacturers. For companies looking to maximize returns, North America provides a well-established ecosystem of specialty retailers, veterinary partnerships, and digital platforms that can accelerate market entry for innovative pet wearable products. The region's blend of consumer willingness to spend and technological infrastructure creates an ideal testing ground for advanced features before a global rollout.

United States: Where Pet Tech Goes Mainstream

The United States (U.S.) dominates the North American pet wearable market with over 80% of the region's total share. This leadership position stems from the country's robust pet insurance market, extensive veterinary network, and technology-forward pet owners. The U.S. market benefits from a supportive regulatory environment, with nearly 110 million Americans living in states that allow pet owners to establish telemedicine relationships with licensed veterinarians through video consultations. This creates a complementary ecosystem where pet health monitoring devices can integrate with virtual vet services, providing real-time health insights. For manufacturers, the U.S. offers both scale and sophistication, making it the ideal launching pad for premium pet wearable innovations that can later be adapted for more price-sensitive markets.

Mexico: The Growth Engine to Watch

Mexico shows promising growth dynamics in the pet wearable space. The country's expanding middle class, increasing pet ownership rates, and growing awareness of pet health monitoring create fertile ground for market expansion. Unlike the highly competitive U.S. market, Mexico presents opportunities for more affordable entry-level pet wearables that serve as gateway products for first-time buyers. The country's improving cellular infrastructure also supports better connectivity for dog GPS tracker devices in urban centers. For companies seeking growth markets with less competitive pressure than the U.S., Mexico offers an attractive combination of lower market entry barriers and rising consumer interest in pet technology solutions. Success here depends on balancing affordability with functionality while establishing strong distribution through both modern and traditional retail channels.

Canada: The Specialized Market

Canada presents unique characteristics in the pet wearable market landscape. Canadian pet owners show particular interest in outdoor activity tracking for pets, reflecting the country's emphasis on outdoor lifestyles. The market demands durable, weather-resistant devices that can withstand everything from snowy winters to summer heat. Major urban centers like Toronto, Vancouver, and Montreal serve as adoption hubs for pet tech market products. The Canadian consumer's emphasis on preventative healthcare extends to pets, with a strong interest in health monitoring devices. For pet wearable industry companies, Canada offers a sophisticated market with specific seasonal and environmental requirements that reward thoughtful product design. Successful brands here focus on durability messaging and often leverage Canada's outdoor recreation retailers as distribution partners.

Asia-Pacific: Tomorrow's Market Leader

Asia-Pacific is growing faster than any other region in the pet wearable market, with an impressive 17.70% CAGR through 2025. This accelerated growth stems from rapidly increasing pet ownership across significant economies, tech-embracing consumers, and expanding veterinary care infrastructure. Unlike North America's established market, Asia-Pacific presents a dynamic landscape where consumer education and category development happen simultaneously. The region's high smartphone penetration creates a ready platform for pet wearable app ecosystems. For companies planning global expansion, Asia-Pacific offers not just growth numbers but the opportunity to shape emerging consumer behaviors in the pet wearable market category before preferences become entrenched.

China: The Volume Powerhouse

China represents the largest market within Asia-Pacific for pet wearables. The country's dramatic rise in pet ownership among urban millennials and Gen Z consumers, combined with its manufacturing prowess in consumer electronics, creates a uniquely advantageous market position. China's pet wearable ecosystem benefits from seamless integration with popular super-apps and payment systems, reducing friction in consumer adoption. The market shows particular strength in smart collar adoption, reflecting urban pet owners' concerns about lost pets in densely populated areas. For global manufacturers, understanding China's distinct e-commerce ecosystem and local competition is essential for capturing market share in this critical growth market. Success depends on balancing competitive pricing with features that appeal to China's increasingly sophisticated pet owners.

India: The High-Growth Opportunity

India emerges as a particularly dynamic growth story within the Asia-Pacific pet wearable landscape. The country's rising affluent class, increasing pet adoption rates in metropolitan areas, and expanding veterinary services create multiple growth drivers. India's pet wearable market shows specific characteristics, including a strong interest in affordable health monitoring devices and pet tracking systems that address concerns about stray animals and traffic safety. The country's robust mobile infrastructure enables even entry-level pet wearable devices to leverage cloud connectivity for enhanced functionality. For companies seeking early-mover advantage in emerging markets, India offers scale potential combined with less entrenched competition than more developed regions, making it an attractive target for strategic market entry through partnerships with the country's growing network of pet specialty retailers.

The Rest of Asia-Pacific: A Mosaic of Opportunity

Beyond the major markets, the rest of Asia-Pacific presents diverse opportunities for pet wearable manufacturers. Japan offers a sophisticated market with aging pet populations driving interest in pet health monitoring devices. South Korea combines high technological acceptance with strong pet humanization trends. Australia shows particular receptivity to premium pet wearable offerings. Meanwhile, emerging Southeast Asian markets like Thailand, Malaysia, and Vietnam present early-stage opportunities where localized approaches can build category awareness. For companies taking a portfolio approach to international expansion, these diverse markets allow for targeted strategies that align with each country's unique pet ownership patterns and technological infrastructure.

Europe: The Precision Market

Europe presents a sophisticated pet wearable market characterized by strong regulatory frameworks and mature pet ownership patterns. The region shows particular strength in medical diagnosis and treatment applications, reflecting European pet owners' emphasis on preventative health care. Unlike North America's more uniform market, Europe features distinct country-specific preferences—German consumers prioritize precision engineering and battery longevity, while United Kingdom buyers show greater interest in stylish designs that complement pet aesthetics. The region's stringent data privacy regulations shape product development, with manufacturers focusing on secure local data storage options. For companies entering the European market, navigating this complex regulatory landscape while addressing country-specific consumer preferences is essential to building a sustainable market presence in the smart pet wearable product market.

Middle East and Africa: The Emerging Frontier

The Middle East and Africa region represents an emerging frontier for pet wearables, characterized by sharp market contrasts between affluent urban centers and developing areas. In wealthy Gulf Cooperation Council (GCC) countries, premium pet wearable adoption follows global luxury consumption patterns, with an emphasis on stylish designs and premium materials. South Africa serves as the region's growing market, with established veterinary infrastructure supporting medical-focused pet wearable device adoption. The region shows particular interest in dog GPS tracker devices that address concerns about pets in unfenced properties or rural areas. For manufacturers considering this market, a tiered product strategy that addresses both premium and entry-level segments can capture the region's diverse opportunity landscape while building category awareness in less developed markets.

South America: The Value-Conscious Innovator

South America's pet wearable market demonstrates promising growth dynamics driven by Brazil and Argentina's expanding pet ownership and increasing disposable income. The region shows particular strength in basic identification and tracking applications, with smart collar products serving as the dominant category. Local factors shape adoption patterns—for example, awareness of pet health issues like Leishmaniasis in Brazil drives interest in insect-repellent pet wearables with monitoring capabilities. The region's uneven cellular infrastructure creates demand for devices with offline functionality. For companies entering South America, understanding these distinct regional requirements and adapting products accordingly will be critical to capturing market share in this vibrant growth opportunity. The region's community-oriented approach to pet care also suggests a potential for products with shared monitoring capabilities among family members.

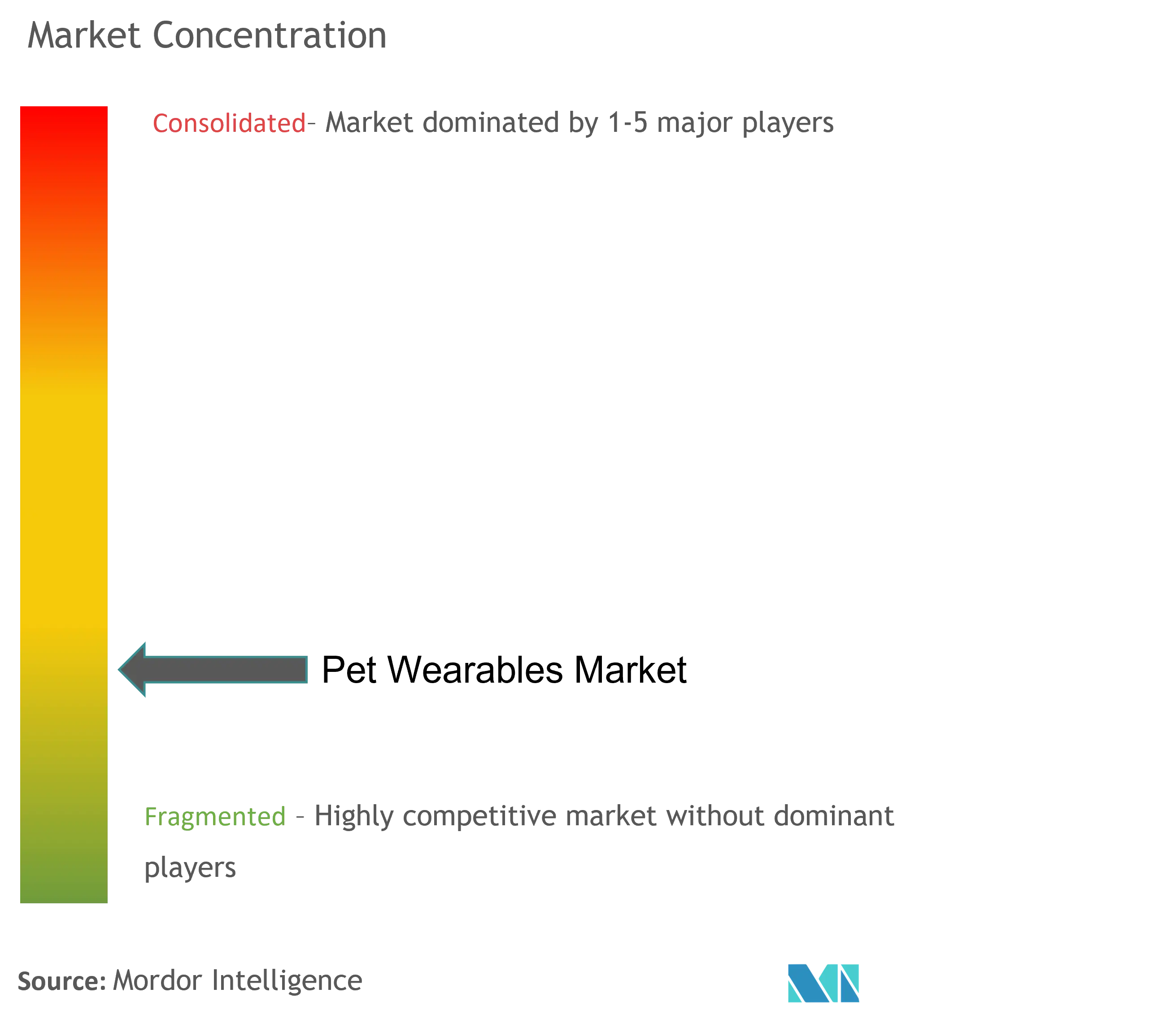

Pet Wearable Industry Overview

From Collars to Ecosystems: How Market Leaders Are Expanding Their Competitive Footprint

The pet wearable industry is evolving beyond standalone devices into integrated ecosystems where competitive advantage stems from comprehensive solutions rather than individual products. While smart collars represent the dominant segment, leading players are strategically expanding into complementary services to create sustainable competitive advantages. Companies like Tractive are building subscription-based business models that deliver recurring revenue while providing enhanced value through data analytics. This ecosystem approach creates significant barriers to entry for newcomers who lack established user bases, making customer experience a crucial competitive lever that established pet wearable market participants can exploit. Market leaders who successfully build these comprehensive solutions can sustain premium pricing and higher customer lifetime values, allowing them to maintain profitability even as hardware margins face pressure from emerging low-cost alternatives.

Beyond Features: The Race for User Engagement and Data Supremacy

In the maturing pet wearable market, forward-thinking companies recognize that the battle for market share increasingly hinges on user engagement rather than feature parity. While hardware capabilities remain important, successful competitors are distinguishing themselves through superior data collection and actionable insights that translate into tangible pet health benefits. Companies effectively harnessing pet health data gain advantages in product development cycles, identifying emerging needs before competitors and iterating faster. This explains why identification and tracking applications remain dominant while medical diagnosis capabilities show accelerated growth - consumers want platforms that not only locate pets but provide comprehensive health monitoring. Players in the pet tech market who prioritize building robust data foundations today will establish competitive advantages that become increasingly difficult for followers to overcome, especially as AI begins transforming raw data into predictive insights.

Strategic Partnerships: The Multiplier Effect Reshaping Competitive Hierarchies

The competitive landscape of the pet wearable market is being quietly reshaped by strategic partnerships that extend reach and capabilities beyond any single company's resources. With promotional strategies, including multi-year subscription discounts, players are clearly prioritizing long-term customer relationships over one-time sales. Forward-thinking companies are forging alliances across previously separate domains - pet insurers, veterinary networks, retail channels, and pet service providers - creating integrated offerings that address multiple consumer needs simultaneously. These partnerships are particularly vital for expansion in the rapidly growing Asia-Pacific region, where local market knowledge and established distribution can accelerate adoption. Companies in the pet wearable market that master this partnership-driven approach gain multiple advantages: reduced customer acquisition costs, enhanced value propositions, and defense against potential category disruptors. The most successful players will be those who view their competitive position not through internal capabilities alone but through their entire partnership ecosystem and its collective strength in delivering comprehensive pet care solutions.

Pet Wearable Market Leaders

-

Dogtra

-

Fitbark Inc.

-

Mars, Incorporated (Whistle)

-

Loc8tor Ltd.

-

Garmin Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Pet Wearable Market News

- May 2022: PurrSong, Inc. launched its LavvieTag, a cat smart-care fitness tracker. It enables pet owners to collect their cat's daily walking, running, sleep, and calorie consumption with LavvieTAG's Activity Analysis Sensor.

- January 2022: Invoxia, a United States-based tech company, introduced a smart dog collar named Invoxia Smart Dog Collar, which is made to monitor a pet dog's vitals, activity, and location 24/7 and has become the first biometric health collar for dogs.

Pet Wearable Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increase in Awareness about Pet's Physical and Mental Fitness and Rising Adoption of IoT

- 4.2.2 Growth in Demand for Pet Monitoring

- 4.2.3 Technological Advancements

-

4.3 Market Restraints

- 4.3.1 Battery Life Issues of Devices

- 4.3.2 High Cost of Products

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Product

- 5.1.1 Smart Collar

- 5.1.2 Smart Camera

- 5.1.3 Smart Harness and Vest

- 5.1.4 Other Products

-

5.2 By Application

- 5.2.1 Identification and Tracking

- 5.2.2 Monitoring and Control

- 5.2.3 Medical Diagnosis and Treatment

- 5.2.4 Other Applications

-

5.3 By Animal Type

- 5.3.1 Dogs

- 5.3.2 Cats

- 5.3.3 Other Animals

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

6. COMPANY PROFILES AND COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Latsen Technology Limited (Pawfit)

- 6.1.2 Tractive

- 6.1.3 FitBark Inc.

- 6.1.4 Garmin Ltd.

- 6.1.5 Loc8tor Ltd.

- 6.1.6 Dogtra

- 6.1.7 PetPace Ltd.

- 6.1.8 Mars Incorporated (Whistle Labs Inc.)

- 6.1.9 Pod Trackers

- 6.1.10 DogTelligent Inc.

- 6.1.11 GoPro Inc.

- 6.1.12 DogTelligent Inc.

- 6.1.13 Otto Petcare Systems

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape Covers - Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Pet Wearable Industry Segmentation

As per the scope of the report, "pet wearables" refer to devices worn on the pet's body to serve various purposes, such as identification, tracking, monitoring, controlling, medical diagnosis, treatment, facilitation, safety, and security. The pet wearable market is segmented by product (smart collars, smart cameras, smart harnesses, and smart vests), application (identification and tracking, monitoring and control, medical diagnosis and treatment, and other applications), animal type (dogs, cats, and other animals), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers a value (USD million) for the above segments.

| By Product | Smart Collar | ||

| Smart Camera | |||

| Smart Harness and Vest | |||

| Other Products | |||

| By Application | Identification and Tracking | ||

| Monitoring and Control | |||

| Medical Diagnosis and Treatment | |||

| Other Applications | |||

| By Animal Type | Dogs | ||

| Cats | |||

| Other Animals | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Pet Wearable Market Research Faqs

What is the current Pet Wearable Market size?

The Pet Wearable Market is projected to register a CAGR of 13.49% during the forecast period (2025-2030)

Which is the fastest growing region in Pet Wearable Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Pet Wearable Market?

In 2025, the North America accounts for the largest market share in Pet Wearable Market.

What years does this Pet Wearable Market cover?

The report covers the Pet Wearable Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Pet Wearable Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Pet Wearable Industry Report

The global pet wearable market is experiencing robust growth, attributed to increasing awareness among pet owners about their pets' health and safety. Enhancements in technology such as IoT, RFID, and GPS are essential, enriching the functionalities of pet wearables to include features like real-time health monitoring and location tracking. The market segments various products such as smart collars, smart cameras, and smart harnesses, all contributing to the pet wearable market size and its expansion. Notably, pet owners are actively utilizing these wearables to track their pets’ fitness and health metrics, including heart rate, calorie intake, and activity levels, further propelling the pet wearable market growth. The pet wearable market analysis indicates that the market is highly competitive, with numerous key players focusing on product innovation, technological advancements, and forming strategic partnerships to consolidate their positions in the market. For a deeper understanding of market dynamics, current trends, and future projections, stakeholders and potential investors can access a sample of this industry analysis as a free report PDF download.