PET Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 78.48 Billion |

| Market Size (2031) | USD 102.42 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

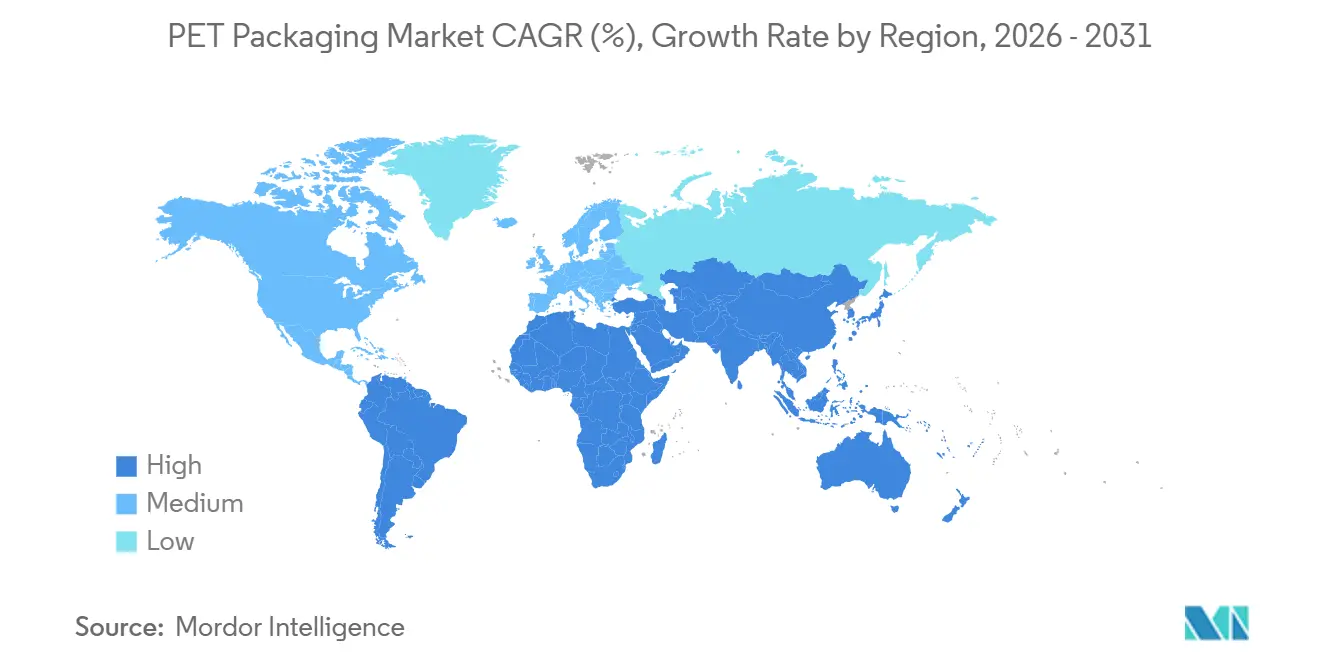

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PET Packaging Market Analysis by Mordor Intelligence

The PET packaging market size is expected to increase from USD 74.41 billion in 2025 to USD 78.48 billion in 2026 and reach USD 102.42 billion by 2031, growing at a CAGR of 5.47% over 2026-2031. Rigid bottles continue to set the commercial baseline, yet flexible pouches, sachets, and thermoformed trays are extending adoption into e-commerce-ready formats that optimize dimensional weight, lower logistics costs, and support circular design targets. Brand-owner pledges to embed 25-50% recycled content are synchronizing with regulatory mandates in the European Union and United States, accelerating demand for food-grade rPET and rewarding converters that control integrated mechanical or chemical recycling assets. Consolidation is reshaping bargaining power, as Amcor’s purchase of Berry Global and Novolex’s merger with Pactiv Evergreen create balanced portfolios covering rigid, flexible, and closure systems. Regionally, Asia-Pacific accounts for nearly half of revenue and remains the supply chain’s manufacturing hub, while Africa is forecast to post the fastest growth, driven by infrastructure build-out and expanding middle-class consumption.

Key Report Takeaways

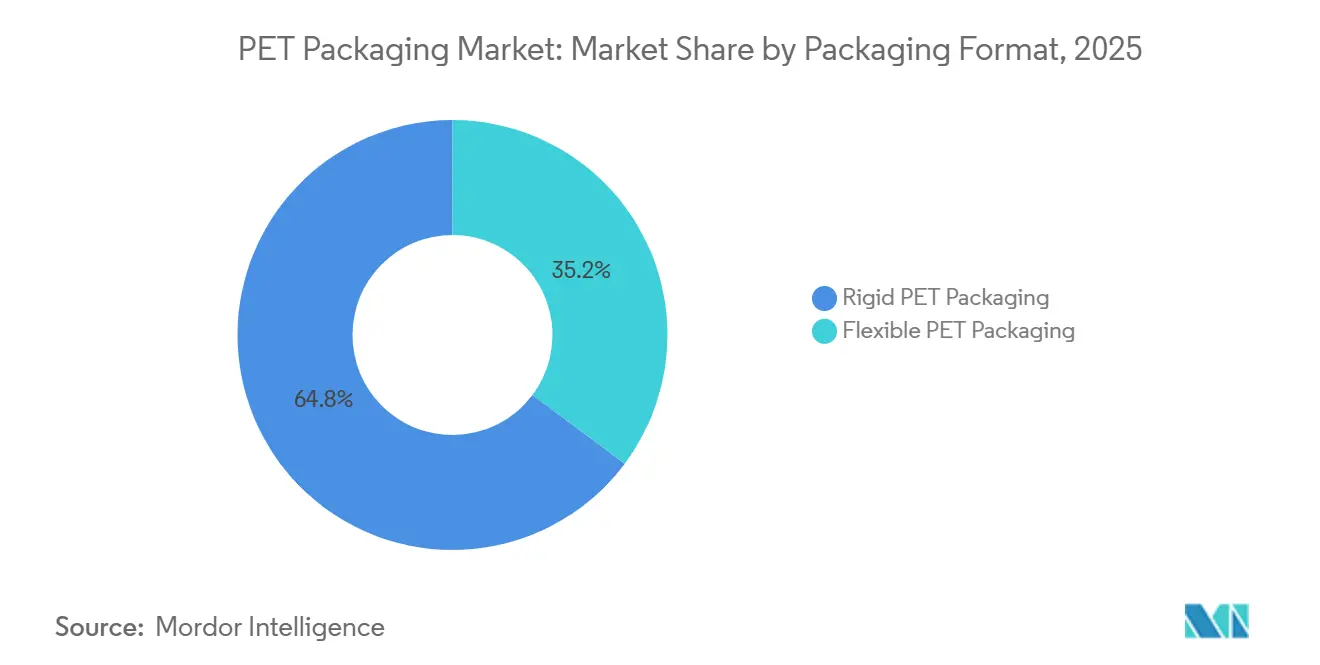

- By packaging format, rigid containers led with 64.78% of 2025 revenue, while flexible formats are advancing at a 5.89% CAGR to 2031.

- By product type, bottles and jars held 68.91% of the PET packaging market share in 2025, whereas pouches and sachets are on track for a 6.46% annual rise through 2031.

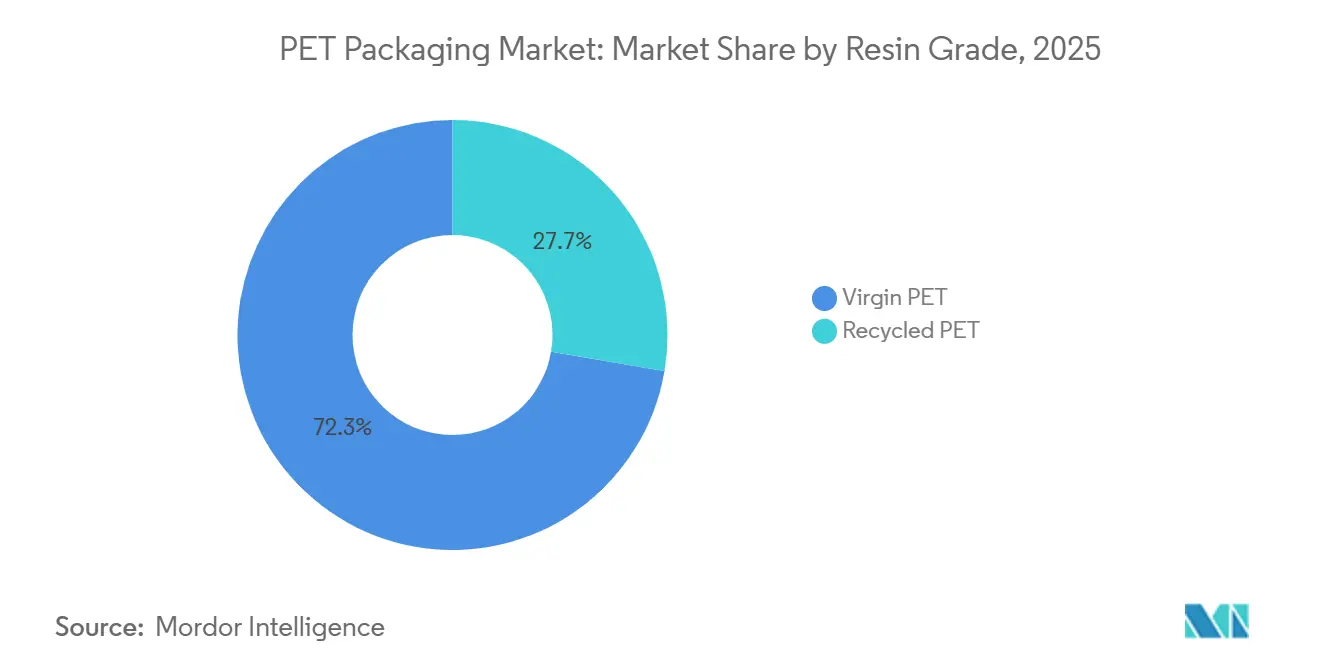

- By resin grade, virgin resin accounted for 72.33% of the 2025 volume, and recycled grades are expanding at a 5.83% CAGR to 2031.

- By end-user industry, food and beverage captured 59.74% of the 2025 value, while personal care and cosmetics are forecast to grow at a 6.68% CAGR during 2026-2031.

- By geography, Asia-Pacific commanded 47.38% of 2025 revenue, and Africa is projected to register a 6.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global PET Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Recyclability and Light-Weighting Advantage | +1.2% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Food-Grade rPET Mandates in EU and US | +1.0% | Europe and United States, spillover to Canada and Asia-Pacific | Short term (≤ 2 years) |

| Increased Adoption in Hot-Fill and CSD Lines | +0.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Growth of E-Commerce Ready Packaging Formats | +0.7% | North America, Europe and urban Asia-Pacific hubs | Short term (≤ 2 years) |

| Deployment of Chemical Recycling Infrastructure | +0.6% | Europe, United States and emerging in China | Long term (≥ 4 years) |

| Brand-Owner Commitments to 25-50% rPET Content | +0.5% | Global, concentrated in multinational consumer goods companies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Recyclability and Light-Weighting Advantage

PET’s low density and easy sortation are displacing glass and aluminum across beverage, food, and personal care applications. Gerolsteiner’s 1-liter reusable PET bottle, launched in 2026, raises refill cycles to 25 and cuts carbon dioxide by 1,900 tonnes per year, validating that light-weighting can coexist with durability.[1]Gerolsteiner Brunnen, “Gerolsteiner Presents New Reusable PET Bottle,” PETnology, petnology.com Converters are now molding ultra-thin walls measuring 0.32 millimeters, resulting in significant logistics savings. ALPLA’s rePETec system achieves 2.7-second cycles and delivers oxygen barriers 20 times better than those of polypropylene, enabling PET to enter dairy, ready meal, and pharmaceutical niches where clarity and shelf life converge. These technical gains strengthen PET’s position against substrate bans that often exempt mono-material, widely recycled formats.

Food-Grade rPET Mandates in EU and US

California Senate Bill 54 and the European Union’s Packaging and Packaging Waste Regulation require increasing recycled content, compelling converters to lock in long-term rPET offtake and to certify mass balance under ISCC PLUS. Amcor sourced 218,000 metric tons of recycled plastic across 34 certified sites in fiscal 2025, already hitting a 10% content milestone.[2]Amcor, “Q4 2025 Results,” sec.gov Eastman and Doloop showcased a bottle made with 100% chemically recycled resin at Drinktec 2025, proving parity with virgin performance. Mandates are therefore bifurcating the converter universe into firms that control feedstock and those exposed to volatile spot markets.

Increased Adoption in Hot-Fill and CSD Lines

Advanced heat-set resins and base designs allow PET to withstand up to 85 °C filling temperatures without deformation. Faerch introduced a hot drink lid made from 85% rPET, fully recyclable back into food-grade loops, illustrating a cost-efficient displacement of polystyrene in coffee service.[3]Faerch, “Faerch Unveils Hot Drinking Lid Made From Recycled PET,” faerch.com Carbonated soft drink bottlers in Asia-Pacific have switched to thin-wall PET with pressurized base geometries, cutting grams per container while sustaining shelf life. These line-upgrade investments expand PET’s accessible volume, especially where refillable glass had been entrenched.

Growth of E-Commerce Ready Packaging Formats

Direct-to-consumer shipping is propelling demand for impact-resistant PET that limits breakage and chargeable weight. Deloitte’s Q3 2025 packaging brief noted that retailers are mandating recycle-ready mono-material formats, compressing design cycles, and favoring agile converters. Pouches and sachets are gaining traction in subscription models that require premium graphics and tamper-evidence at small volumes. Converters wielding short-run digital printing and rapid prototyping are capturing these micro-brand opportunities ahead of aluminum or paper formats that struggle with moisture barrier and line speed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin PET Resin Prices | -0.9% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Emerging Plastic Bans on Single-Use Sachets | -0.6% | Europe, parts of Asia-Pacific and African coastal cities | Medium term (2-4 years) |

| Bottle-to-Bottle Loop Supply Gap | -0.4% | North America and Europe | Medium term (2-4 years) |

| Consumer Perception Shift Toward “Plastic-Free” | -0.3% | Developed markets in Europe and North America, urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin PET Resin Prices

Feedstock swings tied to crude oil and paraxylene tighten converter margins and delay capital deployment. Amcor calculated that each 1% increase in resin costs adds USD 97 million to the annual cost of sales before pass-through. During 2025, Western Europe experienced periods when virgin resin undercut recycled grades, undermining rPET adoption and pressuring sustainability targets. Hedging only partially offsets this exposure, and tariff escalations, such as the 39% Swiss duty applied in August 2025, further distort import economics for equipment and feedstock.

Emerging Plastic Bans on Single-Use Sachets

Legislation in the Philippines, India, and several African nations targets sachets under defined size thresholds, often without material-specific carve-outs. Although mono-material PET sachets are theoretically recyclable, blanket bans neutralize their market potential, pushing brands toward larger pack sizes or refill platforms that carry a higher capital and distribution burden. Deloitte’s survey of Pack Expo 2025 exhibitors showed accelerated R&D spending on refill systems and multi-serve pouches to pre-empt such regulatory risk. Converters operating in sachet-reliant regions must now recalibrate order books and invest in molding capacity for alternative formats.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Format: Rigid Share Leads While Flexible Gains Momentum

The PET packaging market for rigid formats was USD 48.24 billion in 2025, accounting for 64.78% of overall revenue. Rigid bottles, jars, and pharmaceutical containers remain irreplaceable where transparency, gas barrier, and shelf impact command premium shelf space. Yet flexible formats are growing 5.89% yearly, driven by lighter pouches and sachets tailored for e-commerce and on-the-go consumption. Rigid lines benefit from existing high-speed blow-molding infrastructure, integrated collection systems, and consumer familiarity, but cost pressures from competition in commoditized beverages are tightening margins. Flexible specialists push ultrathin laminates with mono-PET structures that meet recyclability guidelines, integrating digital printing to enable SKU proliferation and fast design cycles. The divergence is spawning two supply chains: vertically integrated rigid majors are adding preform and recycling assets, while flexible players are investing in coating, lamination, and pouch-forming technologies that amplify barrier performance without sacrificing circularity.

Second paragraph continues: Flexible PET is penetrating the personal care and household cleaning markets, where refill pouches can reduce resin usage by up to 70% compared to rigid equivalents, cutting transport emissions and warehousing costs. ALPLA’s rePETec platform confirms that 0.32-millimeter walls meet oxygen transmission requirements, allowing yogurt cups and ready-meal trays to transition from polypropylene to PET with superior shelf life. The format shift intensifies demand for food-grade recycled resin to achieve brand recycling pledges. Meanwhile, rigid containers leverage ISCC PLUS mass-balance certificates to lock in long-term contracts with beverage majors that prize consistent resin quality. This strategic split underscores why converters are balancing capital between high-volume rigid lines and nimble, value-added flexible assets.

By Product Type: Bottles and Jars Anchor Revenue, Pouches Accelerate

Bottles and jars delivered 68.91% of 2025 sales, totaling USD 51.27 billion, and secured entrenched routes to market in carbonated soft drinks, bottled water, and edible oils, where clarity, stackability, and product protection hold sway. However, pouches and sachets are expanding at 6.46% annually, driven by consumer appetite for single-serve convenience and retailer demand for shelf-efficient packaging. The PET packaging market share for pouches remains small today, but brand focus on format diversification makes this the fastest-moving product category. Trays and clamshells in fresh produce and bakery harness PET’s thermoformability to extend shelf life and cut food waste, while lids, caps, and closures are witnessing material convergence as brands seek mono-material solutions. Origin Materials’ 1881 PET cap, commercialized in Q2 2025, eliminates the need for cap removal during mechanical recycling, raising yield and purity.

Follow-on paragraph elaborates: Bottle demand is plateauing in mature markets where per-capita beverage consumption has stabilized, and refill programs gain traction, as evidenced by Gerolsteiner’s 25-cycle reuse bottle. Pouches outpace this maturity, finding white space in nutraceutical drink concentrates, cosmetic refills, and dry grocery sectors that crave lightweight packaging. Trays are growing in premium chilled meals as retailers pivot to high visual appeal and extended shelf life, yet they face scrutiny for multilayer structures. Closure innovation is a battleground, with PET able to match bottle resin, erasing sortation losses and improving color consistency in recycled streams. Preforms, although an intermediate, acts as a strategic buffer for converters, allowing quick redeployment across geographies to manage volatile demand.

By Resin Grade: Virgin Dominates but Recycled Content Surges

Virgin resin accounted for 72.33% of 2025 consumption, primarily because of its stable melt consistency suited for 2,000-plus bottle-per-minute filling lines and its lower price during periods of subdued crude oil prices. Yet the PET packaging market share allocated to recycled grades is projected to advance at a 5.83% CAGR, driven by legally binding targets. CARBIOS and Wankai’s planned 50,000-tonnes-per-year enzymatic depolymerization plant in Haining, China, due online in 2027 at an investment of EUR 115 million (USD 129.95 million), signals confidence in the economics of chemical recycling. Recycled PET bifurcates into clear food contact streams and non-food applications where mechanical properties can deviate. Converters with captive recycling or secure offtake contracts capture price premiums and shield margins from virgin price spikes.

Second paragraph explains: Amcor’s 218,000-ton volume of recycled procurement delivered a 10% portfolio content ratio in fiscal 2025, underpinned by 34 ISCC PLUS certified sites. ALPLA pledged EUR 15 million (USD 16.95 million) annually from 2026 to raise installed recycling capacity to 700,000 tonnes over the decade. Mechanical b-t-b loops service clear beverage bottles, whereas chemical routes reclaim opaque, multilayer, and contaminated streams. Quality specifications differ: pharmaceuticals often require virgin or chemically recycled grades for absolute purity, while household cleaners can accept higher mechanical content. As mandates ratchet, virgin share will shrink even as absolute volume grows, making the security of recycled feedstock supply the critical differentiator.

By End-User Industry: Food and Beverage Prevails, Personal Care Outpaces

Food and beverage accounted for 59.74% of 2025 demand, equating to roughly USD 44.5 billion, driven by bottled water, carbonated drinks, and dairy. North American beverage volumes fell mid-single digits for Amcor in 2025, while Latin America posted price- and mix-led gains, illustrating divergent regional trajectories. Personal care and cosmetics, with a 6.68% CAGR, are the fastest-growing segment, spurred by premium product launches and regulatory preference for recyclable mono-material containers. Pharmaceutical uptake is climbing as PET meets child-resistant and tamper-evident requirements while offering clarity advantages over polypropylene blisters. Household cleaners and industrial lubricants value chemical resistance and compatibility with trigger sprayers, enabling higher recycled percentages that lower costs.

Second paragraph delves deeper: Brands in personal care are swapping multilayer tubes for PET pump bottles that sustain aesthetics across refill cycles and integrate PCR without yellowing. In pharmaceuticals, serialization-ready PET vials facilitate track-and-trace, while humidity-sensitive drugs leverage a superior moisture barrier compared to PVC. Household categories embrace dilution-at-home concentrates in PET pouches, cutting fleet mileage. Industrial goods shift toward PET jerrycans, where transparency aids level checking. End-user penetration mirrors geography: Asia-Pacific’s growing middle class lifts packaged foods fastest, Europe nurtures cosmetics and pharmaceuticals, and North America skews toward household cleaners as sustainability labeling tightens.

Geography Analysis

Asia-Pacific accounted for 47.38% of global revenue in 2025, led by China, India, and Southeast Asia, where urbanization drives per-capita beverage consumption. The planned Haining biorecycling facility will provide 50,000 tonnes of rPET, underscoring regional appetite for circular feedstock. India is localizing preform production to dodge tariff exposure, and Southeast Asian converters are adding high-speed stretch-blow lines to meet chilled ready-to-drink tea demand. Japan and South Korea prioritize deposit return and ISCC PLUS certification to secure the supply of premium rPET for beverage majors.

Europe and North America post slower tonnage growth but higher revenue per tonne due to legal recycled-content thresholds. Evertis committed USD 100 million to a new multilayer film site in South Carolina that will add 30,000 tonnes in 2026 and another 30,000 tonnes by 2028, offering domestic converters lower freight risk and assured food-grade film supply. Deposit return systems in the Nordics enhance feedstock purity, allowing Eastman and Doloop to commercialize 100% chemically recycled bottles. In North America, beverage volumes dipped amid weak consumption, while Latin America logged mid-single-digit growth, showing price and mix resilience.

Africa, while accounting for only 5% of today’s revenue, is forecast to grow 6.49% annually through 2031 as water security initiatives and middle-class expansion lift demand for bottled water and edible oil packaging. South Africa’s PETCO model showcases effective voluntary collection, and Egypt’s Nestlé Waters initiative demonstrates 100% rPET bottles in a developing context. Middle Eastern producers such as Borouge integrate petrochemical feedstock to supply regional converters, planning to raise capacity to 6.6 million tonnes by 2028. South America grows in mid-single digits, anchored by Brazilian beverage consumption but moderated by currency volatility.

Competitive Landscape

The market is concentrating as multibillion-dollar mergers create diversified packaging houses. Amcor’s USD 15 billion amalgamation with Berry Global closed in April 2025, unlocking USD 650 million in projected earnings by fiscal 2028 and combining more than 400 plants across 40 nations. Novolex’s USD 6.7 billion union with Pactiv Evergreen unites 250 brands and 39,000 SKUs, assembling rigid, flexible, and closure capabilities that elevate one-stop sourcing for foodservice chains. These integrations raise barriers for mid-tier converters, pushing them toward specialty niches such as pharmaceutical blisters or ultrathin dairy cups.

Emerging disruptors bank on enzymatic and chemical recycling. CARBIOS’s joint venture grants three-year Asian exclusivity and contingent licensing of an additional 100,000 tonnes, potentially seeding a regional rPET megahub. Origin Materials commercialized the first PET water cap, tackling a USD 65 billion closures space and promising full bottle-and-cap circularity, though tariff delays pushed EBITDA breakeven to 2027. Incumbents react by backward integrating into recycling: ALPLA will invest EUR 15 million annually from 2026 to raise recycling capacity to 700,000 tonnes. The battlefield now pits fully integrated giants that promise price stability and material security against agile innovators that trade on intellectual property in advanced recycling or design.

Strategic moves span technology licensing, deposit-system partnerships, and mono-material cap rollouts. Partnerships between resin producers and converters, such as Eastman-Doloop, are accelerating the commercialization of chemical recycling feedstock. Retailers increasingly demand proof of chain of custody, making ISCC PLUS certification a ticket to bid on high-volume private-label contracts. Competitive differentiation tilts toward recyclate availability, light-weighting technology, and the ability to supply matching resin and closure systems.

PET Packaging Industry Leaders

Amcor plc

Resilux NV

ALPLA Werke Alwin Lehner GmbH and Co KG

Silgan Holdings Inc.

Graham Packaging Company LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Gerolsteiner Brunnen launched a 1-liter reusable PET bottle with 50% rPET, extending refill cycles to 25 and saving 1,900 tonnes of CO₂ annually.

- January 2026: ALPLA reported EUR 5.2 billion (USD 5.88 billion) turnover for fiscal 2025 and committed EUR 15 million (USD 16.95 million) annually from 2026 to lift recycling capacity to 700,000 tonnes.

- December 2025: CARBIOS and Wankai New Materials finalized a shareholders’ agreement for a EUR 115 million (USD 129.95 million) 50,000-tonne PET biorecycling plant in Haining, China, slated for Q1 2027.

- September 2025: Eastman and Doloop unveiled a 100% rPET bottle at Drinktec 2025, produced from chemically recycled Eastar Renew EN031 resin.

Global PET Packaging Market Report Scope

The PET Packaging Market Report is Segmented by Packaging Format (Rigid PET Packaging, and Flexible PET Packaging), Product Type (Bottles and Jars, Pouches and Sachets, Trays and Clamshells, Lids-Caps and Closures, Preforms and Other Product Types), Resin Grade (Virgin PET, Recycled PET), End-User Industry (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, Household, Industrial Goods, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Rigid PET Packaging |

| Flexible PET Packaging |

| Bottles and Jars |

| Pouches and Sachets |

| Trays and Clamshells |

| Lids-Caps and Closures |

| Preforms and Other Product Types |

| Virgin PET |

| Recycled PET |

| Food and Beverage |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Household |

| Industrial Goods |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Packaging Format | Rigid PET Packaging | ||

| Flexible PET Packaging | |||

| By Product Type | Bottles and Jars | ||

| Pouches and Sachets | |||

| Trays and Clamshells | |||

| Lids-Caps and Closures | |||

| Preforms and Other Product Types | |||

| By Resin Grade | Virgin PET | ||

| Recycled PET | |||

| By End-User Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Household | |||

| Industrial Goods | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will global demand for recycled PET become by 2031?

Recycled grades are forecast to grow at a 5.83% CAGR, narrowing the virgin share from today’s 72.33% as mandates and brand pledges harden.

Why are flexible PET pouches growing faster than bottles?

Pouches reduce material weight, travel efficiently through parcel networks and meet consumer demand for single-serve convenience, driving a 6.46% annual growth rate.

Which region is set to lead PET packaging capacity expansion?

Asia-Pacific remains the manufacturing nucleus, supported by a planned 50,000-tonne biorecycling plant in China and rapid bottle line investments across India and Southeast Asia.

What impact do resin price swings have on converters?

A 1% rise in resin cost can add USD 97 million to Amcor’s annual cost of sales, highlighting the margin sensitivity of high-volume converters.

How are closures evolving to improve recycling yields?

PET caps that match bottle resin, such as Origin’s 1881 design, remove polymer cross-contamination, allowing complete bottle-and-cap recovery in mechanical streams.

Are single-use plastic bans affecting PET sachets?

Yes, blanket sachet bans in parts of Asia-Pacific and Africa target size thresholds regardless of material, forcing brands to shift toward refill or larger pack formats.

Page last updated on: