| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 13.67 Billion |

| Market Size (2030) | USD 18.64 Billion |

| CAGR (2025 - 2030) | 6.40 % |

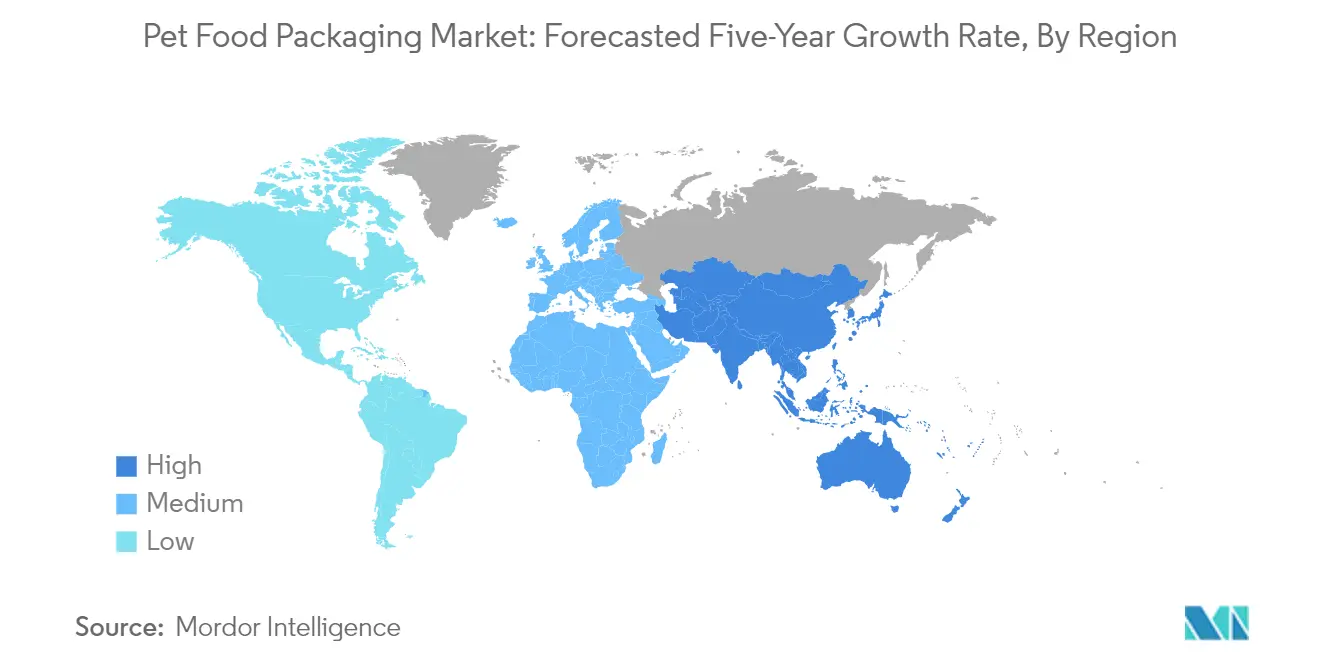

| Fastest Growing Market | Asia |

| Largest Market | North America |

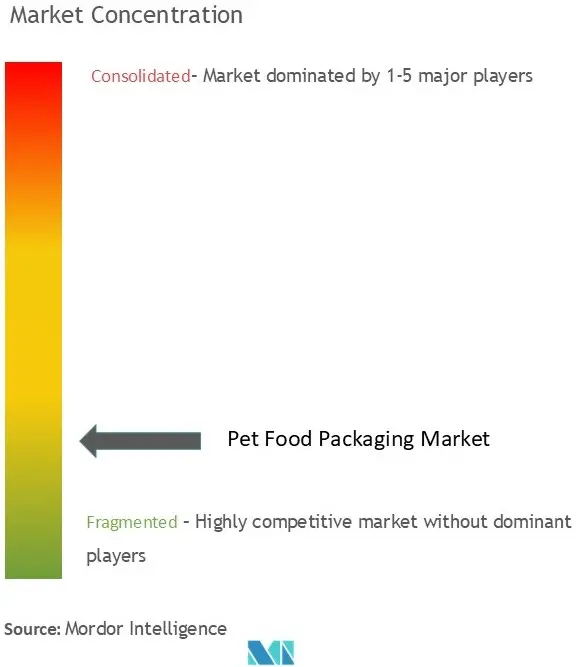

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Pet Food Packaging Market Analysis

The Pet Food Packaging Market size is worth USD 13.67 Billion in 2025, growing at an 6.40% CAGR and is forecast to hit USD 18.64 Billion by 2030.

The pet food packaging market is experiencing significant transformation driven by changing consumer preferences and lifestyle patterns. According to recent data from the American Pet Products Association, approximately 65.1 million households in the United States owned at least one dog in 2023/24, highlighting the substantial consumer base for pet food products. This surge in pet ownership has led manufacturers to develop innovative pet food packaging solutions that focus on convenience, freshness preservation, and portion control features. The industry is witnessing a notable shift toward sustainable pet food packaging alternatives, with companies investing in research and development to create recyclable and biodegradable packaging materials.

The premiumization trend in pet food packaging trends continues to gain momentum, reflecting the evolving relationship between pet owners and their animals. The UK pet food market value for dogs reached GBP 1,840 million (USD 2,303 million) in 2023, demonstrating the robust growth in premium pet food segments. Packaging manufacturers are responding by developing sophisticated designs that incorporate high-quality pet food packaging materials, enhanced barrier properties, and premium finishing options. These advanced packaging solutions not only protect product quality but also serve as effective marketing tools through improved shelf presence and brand differentiation.

The industry is witnessing a significant shift toward flexible packaging solutions, particularly in the dry pet food segment. A Mondi survey revealed that 75% of respondents feel more favorable toward brands with sustainable pet food packaging, driving manufacturers to innovate in this direction. This has led to the development of new packaging technologies such as recyclable pet food packaging barrier films, paper-based alternatives, and mono-material solutions that maintain product freshness while reducing environmental impact. Companies are increasingly investing in advanced manufacturing capabilities to produce these sustainable packaging options without compromising functionality.

The market is experiencing rapid technological advancement in packaging materials and design. The American pet industry expenditure reached USD 147 billion in 2023, indicating substantial investment potential in innovative pet food packaging solutions. Manufacturers are incorporating features such as easy-open mechanisms, resealable closures, and smart packaging elements that can monitor freshness and provide product information. The integration of digital printing technologies has enabled more sophisticated graphics and branding opportunities, while advancements in material science have led to the development of packaging solutions with enhanced barrier properties and extended shelf life capabilities.

Pet Food Packaging Market Trends

Increased Demand for Premium and Branded Products

The pet food industry has experienced seismic packaging shifts due to the explosive growth of the premiumization trend and the entry of new brand players. As consumers learn about the science behind pet nutrition, brands are offering more premium, fresh ingredients, with numerous new SKUs now available in mass grocery stores and premium pet retailers. This evolution has naturally led to the development of premium pet food categories, requiring sophisticated packaging solutions that reflect the product's quality and value proposition.

The growing humanization of animal companions is being led by Gen Z and Millennial consumers who are hyper-focused on their pets' health and wellness. Premium packaging plays a crucial role in communicating product quality and brand values to these conscious consumers. For instance, in August 2023, WholeHearted Fresh Recipes was announced by Petco Health and Wellness Company Inc., featuring premium packaging designed to showcase the human-grade quality ingredients. Graphics play a significant role in differentiating products, with an increase in paper-touch and soft-touch treatments providing consumers with distinctive looks and better sensory experiences.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Awareness About Maintaining Pets' Health

With increasing disposable income, more people are focusing on maintaining a better lifestyle for their pets, particularly in terms of their diet and nutrition. The awareness of pets' health has increased due to the growing knowledge about animal welfare and well-being. Important businesses that produce animal food, like Mars Incorporated, Nestle SA, and others, are concentrating on including nutritional and calorific value information in their packaging, driving the need for more informative and transparent packaging solutions.

The trend among modern pet owners is to provide their animals with wholesome, nutritionally balanced food products, and they tend to use more premium and specialized products. Packaging for premium and ultra-premium pet foods typically consists of high-barrier materials with vibrant graphic printing. In the pet food industry, ingredient information is crucial, and packaging plays an essential role in displaying all the necessary information. Most brands use ideal nutrition and premium ingredients messaging in their packaging, with call-outs like "all-natural," "gluten-free," "non-GMO," and "organic" occupying significant space on the packaging as pet trends 2024 continue to reflect consumer food trends.

Segment Analysis: By Material

Plastic Segment in Pet Food Packaging Market

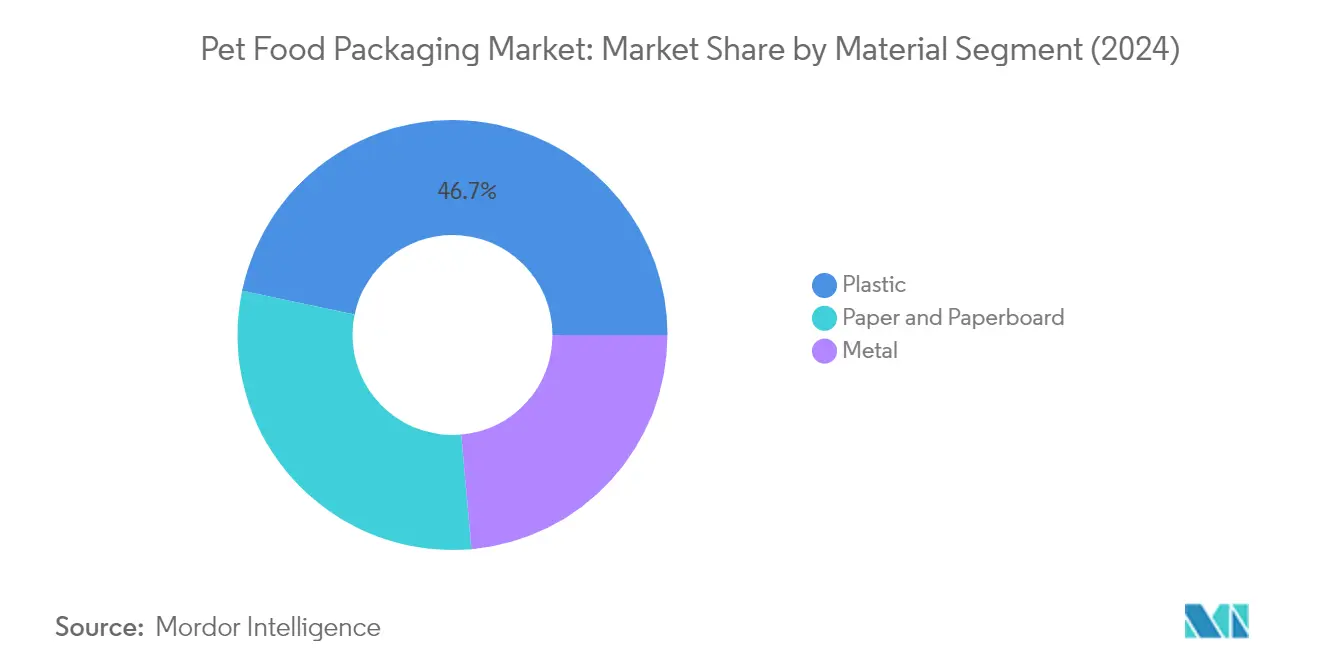

The plastic segment dominates the global pet food packaging market, holding approximately 47% market share in 2024. This significant market position is driven by plastic's superior graphics capabilities, barrier properties, durability, and often the convenience of resealable openings. The segment's prominence is further strengthened by the increasing adoption of flexible plastic pet food packaging materials that are becoming more environmentally friendly and biodegradable while maintaining shelf stability and integrity. Major companies like Mars Petcare and Nestlé Purina are actively deploying food-safe recycled plastic in wet pet food packaging, demonstrating the industry's commitment to sustainable solutions while maintaining plastic's market leadership. The segment's growth is also supported by innovations in flexible packaging and the development of recyclable mono-material structures that offer improved sustainability credentials while maintaining the functional benefits that have made plastic the preferred material choice.

Paper and Paperboard Segment in Pet Food Packaging Market

The paper and paperboard segment is experiencing the fastest growth in the pet food packaging market, with a projected growth rate of approximately 8% during 2024-2029. This accelerated growth is driven by increasing environmental concerns and the rising demand for sustainable pet food packaging material solutions. Multiwall paper bags are gaining significant traction, especially for bulk and larger-sized packages of cat and dog food, due to their relatively good performance and cost-effectiveness. The segment's growth is further propelled by innovations in paper-based packaging solutions, with companies like Mondi introducing recyclable paper-based bags with plastic barriers for premium pet food brands. The smooth surface of paper bags enables high-quality printing, giving packages improved visual appeal, while the development of extensible and high-performance kraft papers has helped improve the strength of such bags, making them increasingly attractive to environmentally conscious consumers and brands.

Remaining Segments in Pet Food Packaging Market

The metal segment continues to play a crucial role in the pet food packaging market, particularly in the wet pet food category. Metal packaging provides superior barrier properties against light and oxygen, offering extended shelf life and protecting flavor longer than any other packaging material. The segment's significance is enhanced by metal's infinite recyclability and its ability to withstand various processing conditions. The rigidity of food cans ensures product protection during distribution, while features like easy-open ends have improved consumer convenience. Metal packaging's sustainability credentials, particularly aluminum and steel's high recyclability rates, make it an increasingly attractive option for brands looking to enhance their environmental profile while maintaining product quality and safety.

Segment Analysis: By Product Type

Bags Segment in Pet Food Packaging Market

The pet food bag segment dominates the pet food packaging market, commanding approximately 41% market share in 2024. This significant market position is driven by the increased demand for airtight sealing and high barrier properties that help retain pet food quality for extended periods. The segment's growth is supported by innovations in re-sealability and re-closable packaging features, particularly bags with zippers that are increasingly popular among consumers. Companies are focusing on developing bags with space-saving formats and enhanced structural integrity through features like four sealed corners, which improve product protection and shelf appeal. The adoption of sustainable materials and mono-material structures in bag manufacturing has also contributed to maintaining its market leadership, as pet food manufacturers increasingly prioritize environmentally friendly packaging solutions.

Pouches Segment in Pet Food Packaging Market

The pet food pouch segment is experiencing the highest growth rate in the pet food packaging market, with an expected growth rate of approximately 8% during 2024-2029. This accelerated growth is driven by the segment's versatility in offering both retort and non-retort packaging solutions for wet and dry pet food products. The increasing adoption of stand-up pouches with clear side panels allows product visibility while maintaining strong barrier properties. Manufacturers are investing heavily in developing recyclable pouch options, with innovations in mono-material structures that maintain the necessary barrier properties while improving environmental sustainability. The segment's growth is further supported by advancements in spouted pouches and shaped pouches that offer enhanced convenience features and premium shelf appeal.

Remaining Segments in Pet Food Packaging Market

The metal cans segment maintains its strong position in the wet pet food category, offering superior barrier properties and extended shelf life capabilities. Folding cartons are gaining traction as an eco-friendly alternative, particularly in premium pet food packaging, while providing excellent branding opportunities through high-quality printing capabilities. The other types segment, which includes bottles, jars, and cups, serves specific niches in the market, particularly in the premium and specialty pet food categories. These segments collectively contribute to the market's diversity by offering various packaging solutions that cater to different pet food types, storage requirements, and consumer preferences, while increasingly incorporating sustainable materials and innovative design features.

Segment Analysis: By Type of Food

Dry Food Segment in Pet Food Packaging Market

The dry pet food packaging segment continues to dominate the pet food packaging market, commanding approximately 63% of the total market share in 2024. This significant market position is driven by the widespread adoption of dry pet food due to its convenience, longer shelf life, and cost-effectiveness compared to other formats. The segment's dominance is further strengthened by the increasing demand for premium and branded dry pet food products, particularly in developed markets. Manufacturers are focusing on innovative packaging solutions like multiwall paper bags, stand-up pouches, and recyclable materials to meet the growing consumer demand for sustainable packaging options. The dry food packaging segment has also witnessed significant technological advancements in barrier properties and resealability features, ensuring product freshness and consumer convenience.

Wet Food Segment in Pet Food Packaging Market

The wet food segment is emerging as the fastest-growing category in the pet food packaging market, with an expected growth rate of approximately 8% during 2024-2029. This remarkable growth is primarily attributed to the increasing awareness about pet nutrition and the rising preference for premium wet pet food products. The segment is witnessing significant innovations in packaging solutions, particularly in retort pouches and metal cans that ensure longer shelf life and maintain product freshness. Manufacturers are increasingly investing in sustainable packaging solutions for wet pet food, with a focus on recyclable materials and reduced environmental impact. The growth is further supported by the rising trend of pet humanization, where pet owners are seeking high-quality, protein-rich wet food options for their pets.

Remaining Segments in Pet Food Market by Type of Food

The chilled and frozen segment represents an emerging niche in the pet food packaging market, catering to the growing demand for fresh and natural pet food options. This segment requires specialized packaging solutions that can maintain product integrity under specific temperature conditions. The packaging solutions in this segment focus on moisture control, temperature resistance, and barrier properties to prevent freezer burn and maintain product quality. The segment is particularly gaining traction among premium pet food manufacturers who are targeting health-conscious pet owners seeking fresh, minimally processed options for their pets. Innovations in this segment include advanced materials that can withstand temperature fluctuations while maintaining package integrity and product freshness.

Segment Analysis: By Animal

Dog Food Segment in Pet Food Packaging Market

The dog food segment continues to dominate the pet food packaging market, commanding approximately 63% of the total market share in 2024. This substantial market presence is driven by the increasing adoption of dogs as pets across various regions, particularly in North America and Europe. The segment's growth is further supported by the rising demand for premium and specialized dog food products that require high-quality, protective packaging solutions. Manufacturers are focusing on developing innovative packaging formats including recyclable materials, easy-open features, and resealable options to meet the evolving needs of dog owners. The trend toward humanization of pets has led to increased spending on high-quality dog food products, which in turn drives the demand for sophisticated packaging solutions that can preserve food freshness and extend shelf life.

Cat Food Segment in Pet Food Packaging Market

The cat food segment is experiencing significant growth in the pet food packaging market, with projections indicating robust expansion from 2024 to 2029. This growth is primarily driven by the increasing adoption of cats as pets, particularly in urban areas where smaller living spaces make cats a more practical pet choice. The segment is witnessing substantial innovations in packaging solutions, particularly in the development of portion-controlled pouches and recyclable materials. Manufacturers are increasingly focusing on convenient, single-serve packaging formats that cater to the specific feeding habits of cats. The trend toward premium cat food products has also led to the development of high-barrier packaging materials that ensure product freshness and extend shelf life, while meeting the growing demand for sustainable packaging solutions.

Remaining Segments in Pet Food Packaging Market by Animal

The other animal food segment encompasses packaging solutions for a diverse range of pets including fish, birds, small mammals, and reptiles. This segment is characterized by specialized packaging requirements that cater to unique product formulations and serving sizes specific to different pet types. The packaging solutions in this segment often feature innovative designs to accommodate various food forms, from flakes for fish to seed mixes for birds. Manufacturers are developing customized packaging solutions that focus on preserving nutritional value while ensuring ease of use for pet owners. The segment also reflects the growing trend toward premium and specialized pet food products, driving the need for high-quality packaging materials that can maintain product freshness and appeal to discerning pet owners.

Pet Food Packaging Market Geography Segment Analysis

Pet Food Packaging Market in North America

The North American pet food packaging market maintains its dominant position, commanding approximately 37% of the global market share in 2024. The region's leadership is primarily driven by the high rate of pet ownership, particularly in the United States, where there is a strong culture of pet humanization and premium pet food consumption. The market is characterized by sophisticated consumer preferences, with a growing demand for sustainable and convenient packaging solutions. Manufacturers in the region are increasingly focusing on eco-friendly materials and innovative packaging designs to meet evolving consumer expectations. The presence of major pet food packaging companies and packaging companies, coupled with advanced manufacturing capabilities, continues to strengthen the region's market position. The trend toward premium pet food products has led to increased demand for high-quality packaging solutions that ensure product freshness and extended shelf life. Additionally, the region's robust retail infrastructure and growing e-commerce channels for pet food products have created new opportunities for packaging innovations, particularly in terms of durability and convenience features.

Pet Food Packaging Market in Europe

The European pet food packaging market has demonstrated robust growth, recording approximately 8% growth annually from 2019 to 2024. The region's market is characterized by stringent regulations regarding packaging materials and sustainability initiatives, which have shaped industry development. European consumers show a strong preference for environmentally responsible packaging solutions, driving manufacturers to invest in recyclable and biodegradable materials. The market benefits from high pet ownership rates across various countries, particularly in Western Europe, where pets are increasingly considered family members. The region's packaging industry has responded to this trend by developing premium packaging solutions that emphasize convenience, freshness preservation, and aesthetic appeal. The market is also witnessing significant innovations in smart packaging technologies and sustainable materials, reflecting the region's leadership in environmental consciousness. The presence of established pet food packaging manufacturers and ongoing investments in research and development continue to drive market evolution, while the growing focus on premium pet food products has created demand for sophisticated packaging solutions.

Pet Food Packaging Market in Asia-Pacific

The Asia-Pacific pet food packaging market is positioned for substantial growth, with projections indicating approximately 8% annual growth from 2024 to 2029. The region's market dynamics are shaped by rapid urbanization, increasing disposable incomes, and growing pet ownership across major economies like China, Japan, and India. The market is witnessing a significant shift in consumer preferences, with a growing emphasis on packaged pet food over traditional feeding methods. Urban consumers are increasingly seeking convenient and hygienic packaging solutions, driving innovations in the sector. The region's packaging industry is adapting to these changing demands by introducing modern packaging formats that cater to various portion sizes and storage requirements. Local manufacturers are investing in advanced packaging technologies to meet international standards while maintaining cost-effectiveness. The market is also seeing increased attention to sustainable packaging solutions, though at a more gradual pace compared to Western markets. The growing middle-class population and changing lifestyles continue to drive market expansion, particularly in emerging economies.

Pet Food Packaging Market in Latin America

The Latin American pet food packaging industry is experiencing significant transformation driven by changing consumer preferences and increasing pet ownership rates. The region's market is characterized by a growing shift from traditional loose pet food sales to packaged products, particularly in urban areas. Brazil and Mexico lead the regional market, with substantial investments in packaging infrastructure and technology. The market is witnessing increased adoption of modern packaging solutions, particularly in premium pet food segments. Local manufacturers are focusing on developing cost-effective yet quality packaging solutions to cater to diverse consumer segments. The region's packaging industry is gradually embracing sustainable practices, though at a pace aligned with local market conditions and consumer purchasing power. The growing influence of international pet food brands has raised packaging quality standards across the region, while local players are innovating to maintain competitiveness. The market continues to evolve with increasing emphasis on convenience features and portion control options in packaging design.

Pet Food Packaging Market in Middle East & Africa

The Middle East and African pet packaging market represents an emerging opportunity with unique regional characteristics and growing potential. The market is witnessing gradual transformation, particularly in urban centers where pet ownership is becoming more common and accepted. Premium packaging solutions are gaining traction in Gulf Cooperation Council countries, where higher disposable incomes drive demand for quality pet food products. The region's packaging industry is adapting to meet international standards while considering local market conditions and consumer preferences. South Africa leads the market on the African continent, with increasing adoption of modern packaging solutions. The market is characterized by a mix of international brands offering premium packaging solutions and local players providing more affordable alternatives. Sustainability initiatives are gradually gaining importance, though economic considerations remain primary drivers of packaging choices. The region's packaging industry is investing in modern technologies to improve product protection and shelf life, particularly important in challenging climatic conditions.

Get Analysis on Important Geographic Markets

Download PDF

Pet Food Packaging Market Overview

Top Companies in Pet Food Packaging Market

The pet food packaging companies market features several prominent players, including Amcor PLC, American Packaging Corporation, Crown Holdings, ProAmpac LLC, Constantia Flexibles, Coveris Holdings, Polymerall LLC, Mondi Group, Sonoco Products Company, and Berry Global Inc. These companies are driving innovation through sustainable packaging solutions, with a strong focus on recyclable materials and eco-friendly alternatives like paper-based packaging and mono-material solutions. Operational agility is demonstrated through the vertical integration of supply chains and investment in advanced manufacturing technologies. Strategic moves in the industry are centered around expanding production capacities, particularly in Europe and North America, while forming partnerships for technological advancement in recyclable packaging solutions. Companies are also focusing on premium packaging solutions with enhanced barrier properties, convenient features like resealability, and improved shelf presence through innovative designs and printing capabilities.

Consolidation and Strategic Partnerships Drive Growth

The pet food packaging market is characterized by a mix of global conglomerates and specialized pet food packaging manufacturers, with larger players leveraging their extensive R&D capabilities and global presence to maintain market dominance. Market consolidation is actively occurring through strategic acquisitions and partnerships, particularly in developing regions, as companies seek to expand their geographical footprint and enhance their technological capabilities. The industry has witnessed numerous collaborations between packaging manufacturers and pet food brands to develop innovative, sustainable solutions that meet evolving consumer demands.

The competitive landscape is marked by significant investments in manufacturing facilities and technology upgrades, with companies focusing on expanding their production capabilities in key markets. Major players are establishing strategic alliances with raw material suppliers and technology providers to ensure consistent supply and innovation capabilities. The market also sees active participation from regional players who leverage their local market knowledge and specialized product offerings to maintain their competitive position in specific geographical areas.

Innovation and Sustainability Define Future Success

For established players to maintain and increase their market share, focus needs to be placed on developing sustainable packaging solutions that align with growing environmental concerns while maintaining product protection and convenience features. Companies must invest in research and development to create innovative materials that meet both sustainability goals and performance requirements. The ability to offer comprehensive pet food packaging services, including design services and technical support, while maintaining cost competitiveness through operational efficiency, will be crucial for market leadership.

New entrants and challenger brands can gain ground by focusing on specialized market segments and developing innovative solutions for specific packaging challenges. Success factors include building strong relationships with pet food manufacturers, offering flexible production capabilities to accommodate varying order sizes, and developing sustainable packaging solutions that meet regulatory requirements. The increasing focus on food safety regulations and sustainability mandates presents both challenges and opportunities for market participants, while the growing trend of premium pet food products creates opportunities for high-value packaging solutions.

Pet Food Packaging Market Leaders

-

American Packaging Corporation

-

ProAmpac LLC

-

Constantia Flexibles Group GmbH

-

Amcor Group GmbH

-

Crown Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Pet Food Packaging Market News

- April 2024: ProMach unveiled its Pet Care Solutions division, catering to the needs of pet food manufacturers. This new division addresses critical industry challenges, emphasizing the importance of product freshness, flavor retention, and extended shelf life.

- February 2024: Targeted Pet Care (TPC) bolstered its position in the pet treats market by acquiring Pet Brands, a leading name in the sector. This acquisition expanded TPC's portfolio and enhanced its sourcing, design, and packaging expertise.

- October 2023: In collaboration with Tetra Pak, Prime100 debuted a new line of sustainably packaged pet food. Prime100 teamed up with Tetra Pak, a frontrunner in food and beverage packaging and processing, to introduce a premium dog food range that's delightful for pets and environmentally conscious.

Pet Food Packaging Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increased Demand for Premium and Branded Products

- 5.1.2 Increasing Awareness about Maintaining Pet's Health

-

5.2 Market Restraints

- 5.2.1 Increasing Adoption of Food Safety Regulations

6. PET FOOD MARKET LANDSCAPE

- 6.1 Pet Food Industry Overview

- 6.2 Types of Pet Food

- 6.3 Pet Food by Animal Type

7. MARKET SEGMENTATION

-

7.1 By Material

- 7.1.1 Paper and Paperboard

- 7.1.2 Metal

- 7.1.3 Plastic

-

7.2 By Product Type

- 7.2.1 Pouches

- 7.2.2 Folding Cartons

- 7.2.3 Metal Cans

- 7.2.4 Bags

- 7.2.5 Other Product Types

-

7.3 By Type of Food

- 7.3.1 Dry Food

- 7.3.2 Wet Food

- 7.3.3 Chilled and Frozen

-

7.4 By Animal

- 7.4.1 Dog Food

- 7.4.2 Cat Food

- 7.4.3 Other Animal

-

7.5 By Geography

- 7.5.1 North America

- 7.5.2 Europe

- 7.5.3 Asia-Pacific

- 7.5.4 Latin America

- 7.5.5 Middle East and Africa

8. COMPETITIVE LANDSCAPE

-

8.1 Company Profiles

- 8.1.1 American Packaging Corporation

- 8.1.2 ProAmpac LLC

- 8.1.3 Constantia Flexibles Group GmbH

- 8.1.4 Amcor Group GmbH

- 8.1.5 Crown Holdings Inc.

- 8.1.6 Coveris Holdings

- 8.1.7 Polymerall LLC

- 8.1.8 Mondi PLC

- 8.1.9 Sonoco Products Company

- 8.1.10 Berry Global Inc.

- 8.1.11 Ardagh Group SA

- 8.1.12 Wipak

- 8.1.13 Silgan Holdings Inc.

- *List Not Exhaustive

9. INVESTMENT ANALYSIS

10. FUTURE OF THE MARKET

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Pet Food Packaging Market Industry Segmentation

Pet food packaging ensures products remain fresh, durable, and contamination-free. As pet owners grow increasingly concerned about their pets' nutritional intake, there has been a surge in the production of diverse pet foods. This, in turn, amplifies the demand for innovative materials in pet food packaging. The study meticulously monitors fundamental demand-side dynamics, leveraging a comprehensive set of base indicators, including pet food demand and local production trends.

The pet food packaging market is segmented by material (paper and paperboard, metal, and plastic), product type (pouches, folding cartons, metal cans, bags, and other product types), type of food (dry food, wet food, and chilled and frozen food), animal (dog food, cat food, and other animal), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for the above-mentioned segments.

| By Material | Paper and Paperboard |

| Metal | |

| Plastic | |

| By Product Type | Pouches |

| Folding Cartons | |

| Metal Cans | |

| Bags | |

| Other Product Types | |

| By Type of Food | Dry Food |

| Wet Food | |

| Chilled and Frozen | |

| By Animal | Dog Food |

| Cat Food | |

| Other Animal | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Pet Food Packaging Market Research FAQs

How big is the Pet Food Packaging Market?

The Pet Food Packaging Market size is worth USD 13.67 billion in 2025, growing at an 6.40% CAGR and is forecast to hit USD 18.64 billion by 2030.

What is the current Pet Food Packaging Market size?

In 2025, the Pet Food Packaging Market size is expected to reach USD 13.67 billion.

Which is the fastest growing region in Pet Food Packaging Market?

Asia is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Pet Food Packaging Market?

In 2025, the North America accounts for the largest market share in Pet Food Packaging Market.

What years does this Pet Food Packaging Market cover, and what was the market size in 2024?

In 2024, the Pet Food Packaging Market size was estimated at USD 12.80 billion. The report covers the Pet Food Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Pet Food Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Pet Food Packaging Market Research

Mordor Intelligence provides comprehensive industry analysis and market outlook for the pet food packaging sector, offering detailed insights into market size, growth trends, and competitive landscape. Our research encompasses various segments including dog food packaging, cat food packaging, pet food pouches, and sustainable pet food packaging solutions. The report pdf includes valuable data on market leaders, emerging technologies, and future market potential, helping stakeholders make informed decisions about their business strategies in the pet food packaging market.

Our consulting expertise extends beyond traditional market research to provide actionable intelligence for the pet food packaging industry. We assist clients with regulatory assessment crucial for pet food packaging regulations compliance, technology scouting for innovative packaging solutions, and competition assessment to identify market opportunities. Our team conducts extensive B2B surveys with pet food packaging manufacturers and suppliers, analyzing customer needs and market trends. We also provide support in product claims assessment, particularly for biodegradable pet food packaging and recyclable pet food packaging solutions, helping companies align their offerings with evolving consumer preferences and sustainability requirements.