Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

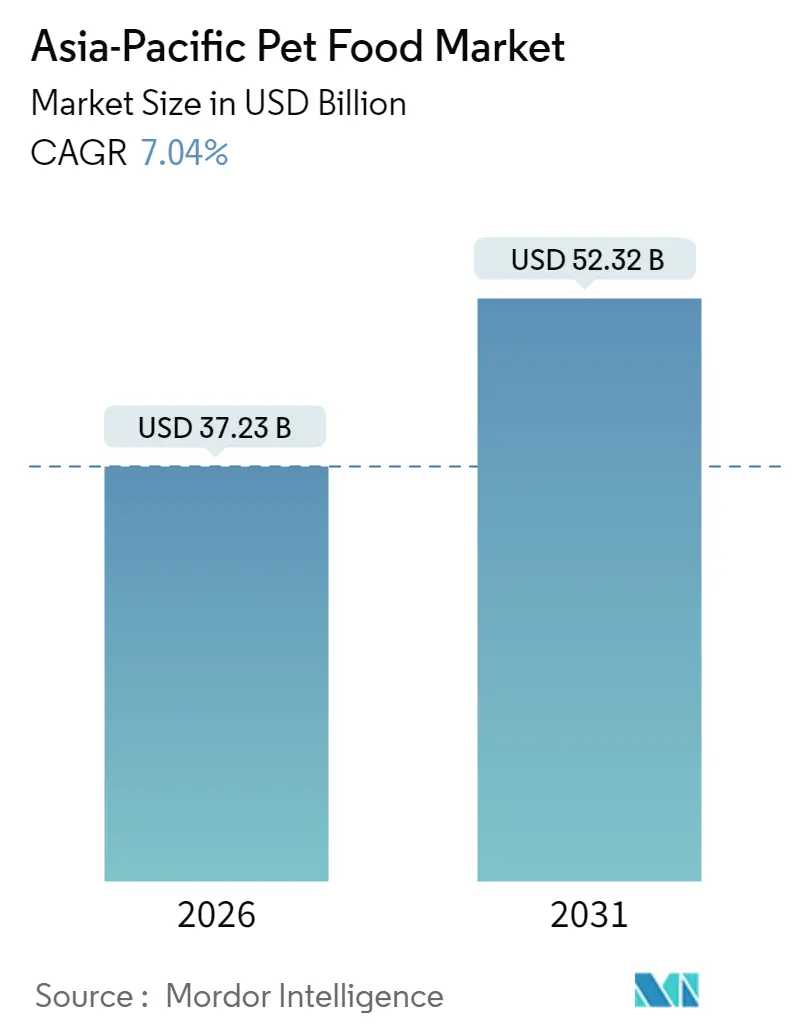

| Market Size (2026) | USD 37.23 Billion |

| Market Size (2031) | USD 52.32 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Pet Food Market Analysis by Mordor Intelligence

The Asia-Pacific pet food market is expected to grow from USD 34.78 billion in 2025 to USD 37.23 billion in 2026 and is forecast to reach USD 52.32 billion by 2031 at 7.04% CAGR over 2026-2031. Rising pet ownership, rapid urbanization, and growing disposable incomes underpin steady volume gains, while premiumization lifts average unit values. Across the region, functional formulations, clean-label positioning, and alternative proteins spur brand differentiation. Digital commerce accelerates consumer reach, and subscription models deepen loyalty as logistics investments improve last-mile reliability. Competitive intensity remains fragmented, though private-equity capital and multinational partnerships signal an emerging consolidation wave in core markets such as China and Australia.

Key Report Takeaways

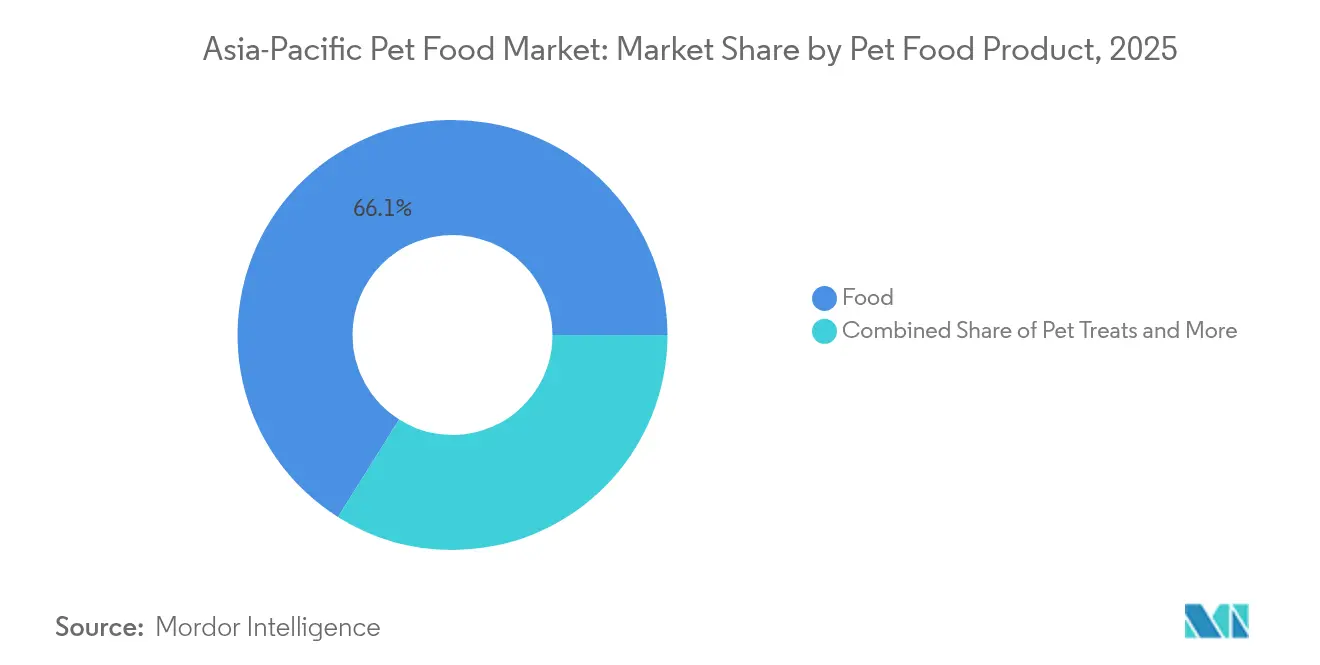

- By pet food product, food captured 66.05% of the Asia-Pacific pet food market share in 2025. Pet veterinary diets are projected to register the fastest 8.27% CAGR through 2031.

- By pets, dogs held a 47.15% share of the Asia-Pacific pet food market size in 2025. Cats are forecast to advance at a 7.78% CAGR to 2031.

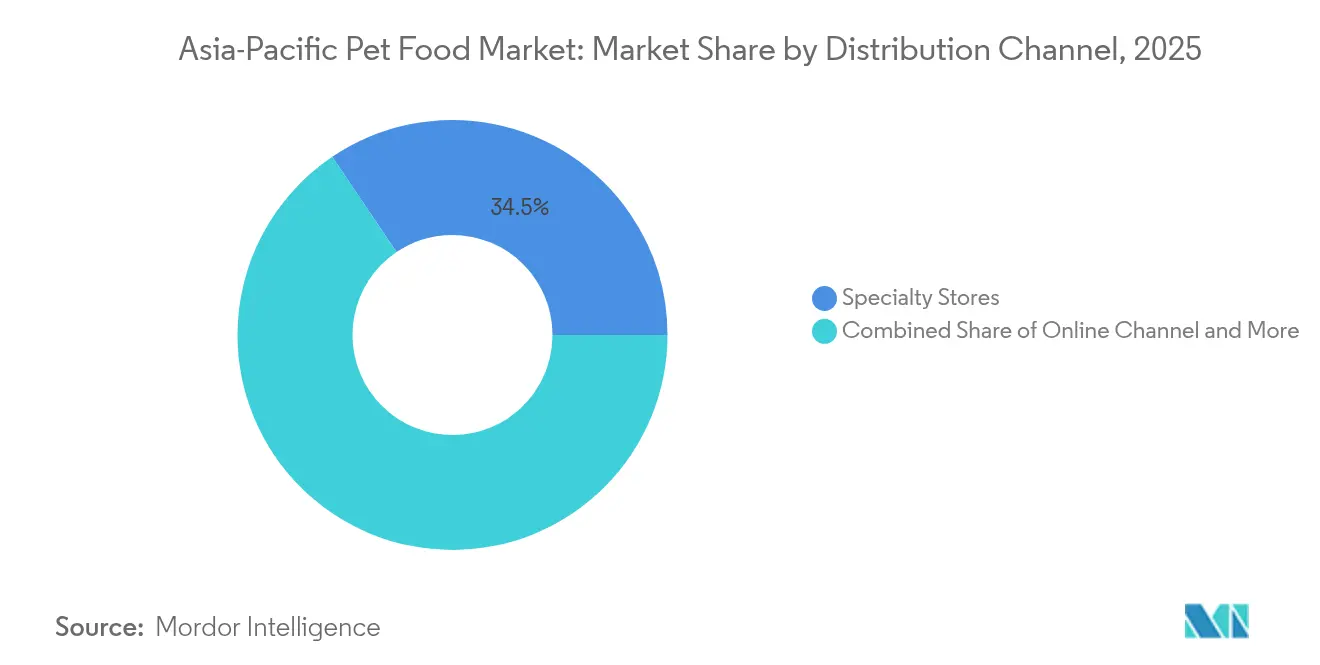

- By distribution channel, specialty Stores led with 34.45% market size share in 2025. Online Channels are projected to expand at a 9.22% CAGR between 2026 and 2031.

- By geography, China led with 35.30% revenue share in 2025. India is projected to expand at a 11.38% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Pet Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Humanization of pets boosts premium food demand | +1.8% | Japan, Australia, and urban China | Medium term (2-4 years) |

| Rising disposable income in key Asian economies | +2.1% | China, India, Indonesia, and Vietnam | Long term (≥ 4 years) |

| Rapid e-commerce and last-mile logistics penetration | +1.4% | Asia-Pacific core and spill-over to Southeast Asia | Short term (≤ 2 years) |

| Functional and clean-label ingredient adoption | +0.9% | Japan, Australia, and expanding to China | Medium term (2-4 years) |

| Insect-based proteins gain regulatory green lights | +0.6% | Australia, Thailand, and Singapore | Long term (≥ 4 years) |

| AI-driven personalized nutrition subscription models | +0.5% | Urban centers across China, Japan, and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Humanization of Pets Boosts Premium Food Demand

Pet humanization is fundamentally reshaping purchasing decisions across the Asia-Pacific region, with companion animals increasingly being treated as family members rather than utility animals. This behavioral shift drives the adoption of premium products, as pet owners seek nutrition solutions that mirror human food quality standards, including organic ingredients, grain-free formulations, and therapeutic benefits. Mars Inc.'s commissioned survey across 20 markets revealed that over one-third of dog and cat owners consider pets "the most important thing in their lives," with Generation Z (45%) and millennials (40%) leading this trend. Regulatory influence from nutritional standards and local food safety certifications increasingly validates premium positioning claims, enabling brands to justify higher price points through scientific backing.

Rising Disposable Income in Key Asian Economies

Economic expansion across emerging Asian markets is creating a widening middle class with discretionary spending power, which is being directed toward pet care. The Philippines exemplifies this trend, with the country moving toward upper-middle income status while the pet food market value approaches PHP 24 billion (USD 430 million), driven by households allocating substantial budgets to pet nutrition[1]Source: Jasper Emmanuel Arcalas, “Feed makers tap thriving pet food market,” The Philippine Star, philstar.com. The trend accelerates in urban centers where dual-income households and delayed family formation redirect traditional child-rearing expenditures toward pet care, establishing sustainable demand foundations that transcend economic cycles.

Rapid E-Commerce and Last-Mile Logistics Penetration

Digital commerce transformation is revolutionizing pet food distribution across the Asia-Pacific region, with online channels, despite traditional specialty stores maintaining their current market leadership. E-commerce penetration, particularly in subscription-based nutrition models, benefits from recurring delivery schedules that align with pet feeding routines, while also reducing customer acquisition costs for manufacturers. Logistics infrastructure investments enable cold-chain distribution for premium wet foods and fresh diet categories, previously constrained by refrigeration limitations in developing markets. This distribution evolution creates competitive advantages for brands that master omnichannel strategies, combining online convenience with offline product discovery and veterinary channel credibility.

Functional and Clean-Label Ingredient Adoption

Consumer demand for transparency and functional benefits drives ingredient innovation toward clean-label formulations that eliminate artificial preservatives, colors, and by-products. BENEO's survey across Asia-Pacific revealed that 73% of pet owners actively seek natural ingredients, while 68% prioritize products with clear health benefits for their animals. Regulatory frameworks are increasingly supporting functional claims when backed by clinical evidence, allowing manufacturers to differentiate themselves through science-based marketing rather than purely emotional appeals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile meat and grain input prices | -1.2% | Global and particularly affecting import-dependent markets | Short term (≤ 2 years) |

| Lengthy product registration and import approvals | -0.8% | China, India, and Indonesia regulatory bottlenecks | Medium term (2-4 years) |

| Weak refrigerated logistics for wet/fresh diets | -0.6% | Infrastructure gaps in developing markets | Long term (≥ 4 years) |

| Pet-obesity concerns curbing caloric volume growth | -0.4% | Developed markets awareness (Japan, Australia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Meat and Grain Input Prices

Raw material cost fluctuations create margin pressure across the pet food value chain, particularly affecting manufacturers with limited pricing power in price-sensitive market segments. Import-dependent markets face additional currency exchange risks, as local currency depreciation amplifies input cost inflation beyond the underlying movements in commodity prices. This volatility forces manufacturers to choose between margin compression and frequent price adjustments that risk customer defection to lower-cost alternatives. Supply chain diversification strategies become essential, though geographic concentration of quality ingredient sources limits manufacturers' ability to achieve true cost stability through supplier diversification.

Lengthy Product Registration and Import Approvals

Regulatory complexity in key markets creates barriers to entry and delays product launches, particularly affecting international brands seeking to capitalize on premium market opportunities. China's product registration process can extend 12-18 months for new formulations, while India's import approval procedures create similar delays for foreign manufacturers. Compliance costs disproportionately impact smaller manufacturers who lack dedicated regulatory affairs capabilities, contributing to market concentration among larger players with regulatory expertise.

Segment Analysis

By Pet Food Product: Premium categories drive value growth

Food products accounted for a 66.05% share of the Asia-Pacific pet food market size in 2025, and pet veterinary diets are projected to register the fastest CAGR of 8.27% through 2031. Dry kibble remains the volume staple, though wet formats post faster gains as humanization encourages fresh-like textures. Nutraceuticals and supplements are gaining momentum due to the demand for probiotics and omega-3 fatty acids. The freeze-dried treat niche is experiencing double-digit expansion due to its high protein content and convenience. Veterinary diets, although smaller in scale, deliver the highest margins through clinically validated formulations.

Ongoing premiumization prompts manufacturers to prioritize functional claims over sheer volume. Regional innovators, such as Singapore’s Majes, introduced climate-specific recipes in 2024, showcasing micro-segmentation strategies. Costlier ingredients and advanced processing raise unit values, sustaining revenue momentum even as mature urban markets approach pet saturation.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Pets: Cats emerge as the growth engine

Dogs retained 47.15% of the Asia-Pacific pet food market share in 2025, yet cats lead future gains with a 7.78% CAGR during the forecast period. Apartment living and lifestyle convenience favor feline companionship in densely populated metros like Tokyo, Shanghai, and Seoul. Moisture-rich wet and pouch foods gain traction, supported by formulations that address hairball control and urinary health. Manufacturers bundle multi-pack wet assortments with dry kibble to drive cross-category spend per cat.

Other Pets, such as birds, fish, and small mammals, remain niche but provide white space for specialized diets. The cat segment’s rapid advance encourages brands to recalibrate marketing budgets toward feline-centric innovation, seeking early adopter loyalty before ownership parity with dogs is reached region-wide.

By Distribution Channel: Digital transformation accelerates

Specialty Stores led the 2025 market size value at 34.45%, leveraging staff expertise and curated assortments. Online Channels chart a 9.22% CAGR through 2026-2031, propelled by auto-replenishment, social-commerce engagement, and broader SKU breadth. Asia-Pacific pet food market size for online orders continues to widen as logistics investors enhance cold-chain nodes, unlocking direct-to-consumer wet food delivery.

Supermarkets and Hypermarkets retain relevance for mainstream shoppers, though limited shelf space constrains premium assortment depth. Convenience Stores cater to impulse purchases. Omnichannel models emerge, with specialty chains launching branded e-stores and leveraging store-pickup to offset last-mile costs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

China accounted for 35.30% of 2025 sales, underpinned by a sizeable pet population, rising middle-class income, and a sophisticated e-commerce ecosystem. Market fragmentation prevails, with the top 10 players controlling a modest market size value, creating opportunities for consolidation. Advent International’s investment in Seek Pet Food illustrates private-equity appetite for scalable manufacturing.

India registers the fastest 11.38% CAGR, driven by accelerating pet adoption in tier-one and tier-two cities. Growel Group’s investment in pet treats underscores its domestic capacity build-out. Low processed-food penetration suggests a multi-year runway as consumers shift from table scraps to commercial diets. Japan and Australia exhibit mature, high-value profiles. Professional veterinary influence and aging pet demographics sustain demand for therapeutic diets and functional treats. SunRice’s acquisition of SavourLife reflects strategic expansion into premium dog food.

Southeast Asian markets, including Indonesia, Vietnam, Thailand, Malaysia, and the Philippines, show varied growth trajectories. Indonesia and Vietnam benefit from rising urban pet ownership but face infrastructure constraints that favor shelf-stable formats. These emerging markets create entry opportunities for both premium international brands and value-oriented regional manufacturers targeting price-sensitive consumer segments.

Competitive Landscape

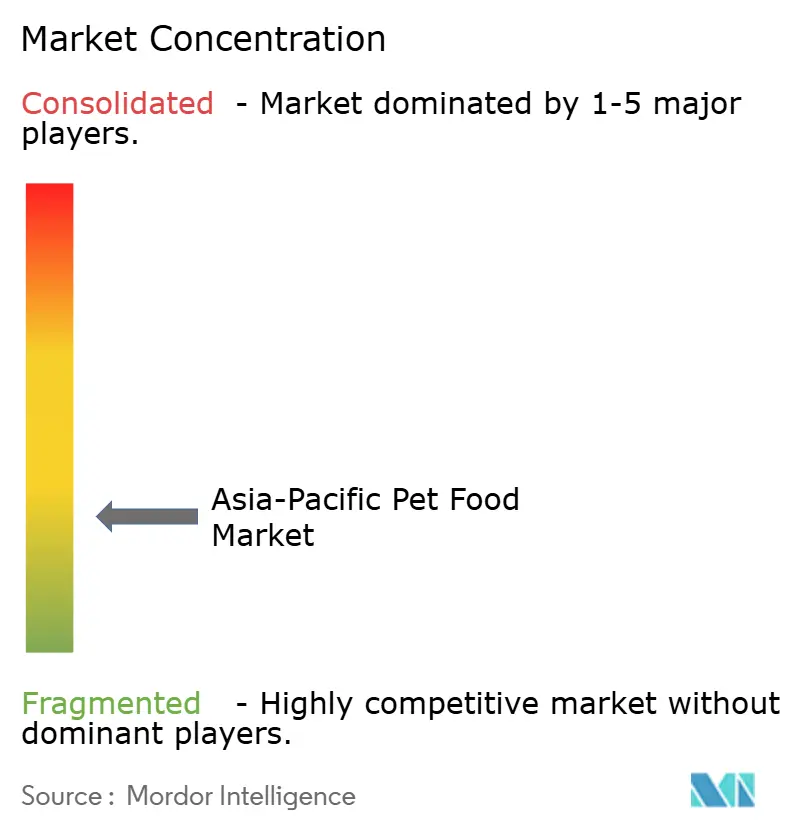

The Asia-Pacific pet food market remains fragmented, with top players seldom exceeding double-digit shares outside Japan and Australia. Mars, Nestlé Purina, Archer Daniels Midland (ADM), General Mills Inc., and Colgate-Palmolive Company (Hill's Pet Nutrition Inc.) lead premium dog and cat categories in specific markets, leveraging multi-tiered brand portfolios. Regional champions, such as Unicharm in Japan and Perfect Companion Group in Thailand, defend their domestic strongholds with localized flavors and price tiers.

Private capital accelerates consolidation. Sixteen pet-related investments closed in the first half of 2024 compared with 13 during all of 2023, highlighting an active deal pipeline. Technology adoption emerges as a competitive differentiator, with AI-driven personalization platforms enabling faster product development cycles and subscription-based revenue models that create customer switching costs.

Strategically, leading firms pursue channel diversification, emphasizing online engagement, veterinary recommendation, and subscription models. Supply-chain localization mitigates currency and tariff risks, while sustainability commitments around packaging and alternative proteins address emerging consumer values. White-space opportunities exist in therapeutic nutrition categories and subscription-based personalized nutrition services, where regulatory barriers and technical expertise requirements limit competitive intensity while enabling premium pricing strategies.

Asia-Pacific Pet Food Industry Leaders

-

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

-

General Mills Inc.

-

Mars Incorporated

-

Nestle (Purina)

-

Archer Daniels Midland (ADM)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2024: SunRice Group acquired Australian premium dog food company SavourLife through its animal nutrition division CopRice. The acquisition expands SunRice's presence in the branded companion animal market while maintaining SavourLife's social mission of donating 50% of profits to dog rescue organizations, demonstrating how purpose-driven positioning creates acquisition value.

- July 2023: Hill's Pet Nutrition introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products for pets with sensitive stomachs and skin lines. They contain vitamins, omega-3 fatty acids, and antioxidants.

- May 2023: Nestle Purina launched new cat treats under the Friskies "Friskies Playfuls - treats" brand. These treats are round in shape and are available in chicken and liver and salmon and shrimp flavors for adult cats.

Asia-Pacific Pet Food Market Report Scope

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. Australia, China, India, Indonesia, Japan, Malaysia, Philippines, Taiwan, Thailand, Vietnam are covered as segments by Country.

Pet Food Product

| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft and Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | ||

| Diabetes | ||||

| Digestive Sensitivity | ||||

| Obesity Diets | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary tract disease | ||||

| Other Veterinary Diets |

Pets

| Cats |

| Dogs |

| Other Pets |

Distribution Channel

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

Geography

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| Philippines |

| Taiwan |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft and Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | |||

| Diabetes | |||||

| Digestive Sensitivity | |||||

| Obesity Diets | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary tract disease | |||||

| Other Veterinary Diets | |||||

| Pets | Cats | ||||

| Dogs | |||||

| Other Pets | |||||

| Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

| Geography | Australia | ||||

| China | |||||

| India | |||||

| Indonesia | |||||

| Japan | |||||

| Malaysia | |||||

| Philippines | |||||

| Taiwan | |||||

| Thailand | |||||

| Vietnam | |||||

| Rest of Asia-Pacific | |||||

Need A Different Region or Segment?

Customize Now

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF