Market Size of PET Bottles Industry

| Study Period | 2019 - 2029 |

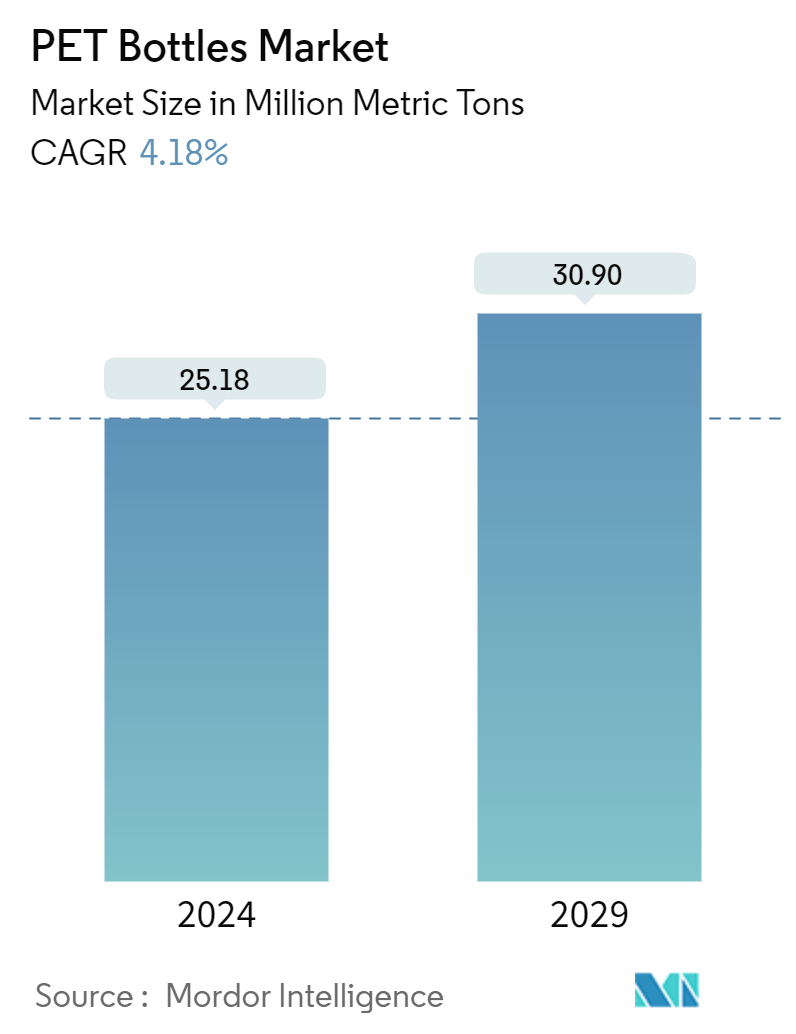

| Market Volume (2024) | 25.18 Million metric tons |

| Market Volume (2029) | 30.90 Million metric tons |

| CAGR (2024 - 2029) | 4.18 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

PET Bottles Market Analysis

The PET Bottles Market size is estimated at 25.18 Million metric tons in 2024, and is expected to reach 30.90 Million metric tons by 2029, growing at a CAGR of 4.18% during the forecast period (2024-2029).

- Plastic bottles and containers, primarily made of polyethylene terephthalate, are widely used because they are lightweight and durable, facilitating easier handling. Manufacturers prefer plastic packaging because of its lower production costs. During the forecast period, the market studied is poised for growth, propelled by the cost-effectiveness of plastic packaging and the rising demand for packaged food and beverages. Furthermore, polyethylene terephthalate (PET) containers are favored for their durability, versatility, and cost-effectiveness. As end-user industries such as food, beverage, and pharmacy expand and innovate, the demand for plastic bottles and container packaging grows. The introduction of new drinks with various flavors and packaging formats in the industry continues to drive the need for rigid plastic bottles.

- PET bottles are increasingly replacing glass bottles due to their lightweight and durable nature. These bottles can be used to pack mineral water and other beverages, enabling more cost-effective transportation. PET's transparency and inherent CO2 barrier properties suit it for various applications. PET can readily be molded into different shapes or blown into bottles. Manufacturers can customize PET's properties by incorporating additives like colorants, UV blockers, and oxygen barriers, enabling the creation of bottles tailored to specific brand needs.

- The PET packaging market faces significant challenges due to evolving regulatory standards, primarily driven by growing environmental concerns. Governments worldwide are responding to public apprehension about plastic packaging waste by implementing regulations to minimize environmental impact and improve waste management processes. These regulatory changes often include restrictions on single-use plastics, increased recycling targets, and extended producer responsibility programs. As a result, PET packaging manufacturers adapt their production processes, invest in eco-friendly alternatives, and develop more sustainable packaging solutions to comply with these new standards. This regulatory landscape affects the industry's operational costs and influences consumer preferences as environmentally conscious consumers increasingly demand sustainable packaging options.

- Sustainable packaging solutions have gained prominence due to increased consumer awareness regarding the environmental benefits of eco-friendly packaging. PET has become an essential resin among eco-friendly packaging materials due to its recyclability and potential for circularity. Closed-loop recycling, where plastic is recycled and used to create new products in the same category, is often applied to PET bottles. This approach has led businesses to prioritize PET over other resin materials. As a result, the recycling of plastic bottles is expected to impact the market positively.

- Companies are innovating to meet the increasing demand for rPET across end-user segments. The surge in sustainable packaging is propelled by consumer preferences and regulatory mandates to curb plastic waste. For instance, in June 2024, Kraft Heinz introduced 100% recycled PET bottles for its 12- and 22-oz Kraft Real Mayo and Miracle Whip sizes. This move followed the company's 2023 announcement of a goal to reduce virgin plastic use in its global packaging portfolio by 20% by 2030. Adopting rPET in food packaging demonstrates the material's versatility and growing acceptance in the industry. Other companies are likely to follow suit, potentially leading to a significant increase in rPET demand and further innovations in recycling technologies to meet this demand.

PET Bottles Indusrry Segmentation

Polyethylene terephthalate (PET) is used in plastic bottle production. Its popularity stems from its durability, cost-effectiveness, and high recyclability, making it practical and environmentally responsible. PET bottles are characterized by their transparency, lightweight nature, and flexibility. They effectively preserve the quality of their contents, maintaining taste and odor. After use, PET bottles can be easily recycled through dedicated collection systems. The beverage industry widely adopts PET because it can withstand various temperatures and pressures, ensuring product safety and quality. The material's lightweight nature reduces transportation costs and energy consumption, enhancing its environmental benefits. PET's recyclability contributes to a circular economy model, promoting material reuse, waste reduction, and resource conservation.

The PET bottles market is segmented by end-user vertical (beverages [packaged water, carbonated soft drinks, fruit juice, energy drinks, and other beverages], food, personal care, household care, pharmaceuticals, and other end-user verticals) and geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, Italy, and Rest of Europe], Asia [China, India, Japan, Australia and New Zealand, and Rest of Asia], Latin America [Mexico, Brazil, Columbia, and Rest of Latin America], and Middle East and Africa [Saudi Arabia, South Africa, United Arab Emirates, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of volume (tonnes) for all the above segments.

| By End-user Vertical | |||||||

| |||||||

| Food | |||||||

| Personal Care | |||||||

| Household Care | |||||||

| Pharmaceuticals | |||||||

| Other End-user Verticals |

| By Geography*** | ||||||

| ||||||

| ||||||

| ||||||

| ||||||

|

PET Bottles Market Size Summary

The PET bottles market is poised for significant growth, driven by the material's advantageous properties such as lightweight, transparency, and resistance to moisture and chemicals. These characteristics make PET an ideal choice for various applications, particularly in the beverage and food industries, where it is increasingly replacing traditional packaging materials like glass, metal, and cardboard. The versatility of PET, enhanced by the use of additives like colorants and UV blockers, allows for customization to meet specific brand requirements. The market is witnessing a surge in demand for PET bottles, especially in bottled water and soft drinks, as consumer preferences shift towards convenient and high-quality packaging solutions. The ongoing innovation in sustainable packaging, such as the development of 100% plant-based PET bottles, further underscores the industry's commitment to meeting environmental standards and consumer expectations.

Despite the promising growth trajectory, the PET bottles market faces challenges from regulatory changes aimed at reducing plastic waste and improving recycling processes. The impact of global events, such as the COVID-19 pandemic and geopolitical tensions, has also affected supply chains and market dynamics. However, the industry's response includes strategic partnerships and investments in recycling technologies, such as the establishment of bottle-to-bottle recycling plants and the use of ocean-bound PET for resin production. Major players in the market, including SABIC, Amcor, and Indorama Ventures, are actively pursuing strategies like mergers, acquisitions, and product innovation to maintain competitiveness and expand their market presence. These efforts, coupled with the growing consumer demand for sustainable and recyclable packaging, are expected to drive the market forward in the coming years.

PET Bottles Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

1.4 Assessment of the Impact of Geopolitical Developments on the Industry

-

-

2. MARKET SEGMENTATION

-

2.1 By End-user Vertical

-

2.1.1 Beverages

-

2.1.1.1 Packaged Water

-

2.1.1.2 Carbonated Soft Drinks

-

2.1.1.3 Fruit Juice

-

2.1.1.4 Energy Drinks

-

2.1.1.5 Other Beverages

-

-

2.1.2 Food

-

2.1.3 Personal Care

-

2.1.4 Household Care

-

2.1.5 Pharmaceuticals

-

2.1.6 Other End-user Verticals

-

-

2.2 By Geography***

-

2.2.1 North America

-

2.2.1.1 United States

-

2.2.1.2 Canada

-

-

2.2.2 Europe

-

2.2.2.1 United Kingdom

-

2.2.2.2 Germany

-

2.2.2.3 France

-

2.2.2.4 Italy

-

-

2.2.3 Asia

-

2.2.3.1 China

-

2.2.3.2 India

-

2.2.3.3 Japan

-

2.2.3.4 Australia and New Zealand

-

-

2.2.4 Latin America

-

2.2.4.1 Mexico

-

2.2.4.2 Brazil

-

2.2.4.3 Columbia

-

-

2.2.5 Middle East and Africa

-

2.2.5.1 Saudi Arabia

-

2.2.5.2 South Africa

-

2.2.5.3 United Arab Emirates

-

-

-

PET Bottles Market Size FAQs

How big is the PET Bottles Market?

The PET Bottles Market size is expected to reach 25.18 million metric tons in 2024 and grow at a CAGR of 4.18% to reach 30.90 million metric tons by 2029.

What is the current PET Bottles Market size?

In 2024, the PET Bottles Market size is expected to reach 25.18 million metric tons.