| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Market Size (2025) | USD 11.05 Billion |

| Market Size (2030) | USD 12.95 Billion |

| CAGR (2025 - 2030) | 3.21 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Penicillin Drug Market Analysis

The Penicillin Drug Market size is estimated at USD 11.05 billion in 2025, and is expected to reach USD 12.95 billion by 2030, at a CAGR of 3.21% during the forecast period (2025-2030).

The European penicillin drug market is experiencing significant transformation through strategic manufacturing investments aimed at strengthening regional production capabilities and reducing dependence on imports. Major pharmaceutical companies are making substantial investments to expand their manufacturing facilities across Europe. For instance, in November 2022, Sandoz announced an additional investment of EUR 50 million to support increased European manufacturing capacity for finished dosage form penicillin drugs. Similarly, in June 2023, GSK invested EUR 22 million to increase antibiotic production in France, focusing on manufacturing amoxicillin and amoxicillin/clavulanic acid products.

Healthcare infrastructure development across Europe is playing a crucial role in shaping the penicillin drug market landscape. Governments are actively investing in modernizing and expanding healthcare facilities to improve patient care and access to essential medications. In April 2023, the German government approved an annual hospital construction program worth EUR 248 million, with a total investment of around EUR 455 million in hospitals for the year. This expansion of healthcare infrastructure is expected to enhance the distribution and accessibility of penicillin drugs across the region.

The market is witnessing evolving patterns in infectious disease prevalence, which directly impacts the demand for penicillin-based medications. According to data published by the Government of the United Kingdom, 52,183 cases of scarlet fever were reported in England between September 2022 and March 2023, highlighting the continued significance of bacterial infections requiring penicillin treatment. This persistent disease burden underscores the essential role of penicillin drugs in modern healthcare systems.

Supply chain resilience has emerged as a critical focus area for the European penicillin market, with stakeholders implementing various strategies to ensure consistent product availability. Pharmaceutical companies are increasingly adopting vertical integration approaches and establishing robust regional supply networks. The European Commission's support for modernizing production facilities, exemplified by their approval of EUR 28.8 million in Austrian measures to support Sandoz's penicillin production modernization in Tyrol in July 2023, demonstrates the region's commitment to strengthening its pharmaceutical manufacturing capabilities and ensuring supply security for essential medicines.

Penicillin Drug Market Trends

Increasing Burden of Infectious Diseases and Rise in Demand and Development of Generic Drugs in Europe

The rising prevalence of various bacterial infections across Europe has created a significant demand for penicillin antibiotics. According to the National Health Service (NHS) of the United Kingdom, over 800,000 hospital admissions due to urinary tract infections (UTIs) were reported in the past five years due to primary diagnosis, with more than 1.8 million hospital admissions involving UTIs between 2018-19 and 2022-23. The most affected population group was patients aged 65 and older, highlighting the growing need for effective penicillin medicines in the elderly population. Additionally, Europe has experienced several infectious disease outbreaks, such as the March 2023 outbreak of monophasic Salmonella Typhimurium infection linked to chocolate products produced in Belgium, affecting 151 cases across 11 European countries.

The burden of skin and soft tissue infections has also contributed significantly to the demand for penicillin medications. According to research published in the International Journal of Antimicrobial Agents in July 2022, acute bacterial skin and skin structure infections (ABSSSIs) are a significant health concern in Europe, with approximately 73.6% of hospitalizations for skin infections being ABSSSIs. The study revealed that 22.7% of patients required at least one additional ABSSSI-related hospitalization, while 47.1% visited emergency rooms, demonstrating the recurring nature of these infections and the sustained need for antibiotic treatments. Furthermore, according to the National Center for Infection Control of Switzerland, the combined healthcare-associated infection (HAI) prevalence was 6.1% in March 2022, with lower respiratory tract infections and surgical site infections accounting for half of all HAIs.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Research and Development Activities in the Pharmaceutical Industry

The pharmaceutical industry's commitment to research and development in antibiotics has been demonstrated through significant investments and collaborations. In July 2023, the Global Antibiotic Research & Development Partnership (GARDP) and Bugworks Research Inc. entered into a collaboration agreement to advance the development of a new broad-spectrum antibiotic compound. This initiative, supported by funding of up to USD 20 million, aims to treat infections caused by multidrug-resistant bacteria, including pneumonia, bloodstream infections, meningitis, and urinary tract infections. Additionally, in May 2023, the Government of the United Kingdom extended funding of GBP 5 million to GARDP for two years to enhance antibiotic development for drug-resistant infections identified by the World Health Organization.

The industry has also witnessed substantial investments in manufacturing capabilities and research facilities. In June 2023, GSK invested EUR 22 million to increase the production of antibiotics in France, with its Mayenne site dedicated to producing amoxicillin and amoxicillin/clavulanic acid through manufacturing and packaging various formulations. This investment strategy aims to adapt and strengthen antibiotic supply and production chains by early 2027, making them more flexible and quickly mobilized during periods of strong demand. Furthermore, in January 2023, the Antimicrobial Resistance (AMR) Research Fund made a new investment in the Swiss drugmaker BioVersys AG for developing antibiotic candidates, including treatments targeting infections caused by carbapenem-resistant Acinetobacter baumannii, demonstrating the industry's commitment to addressing emerging bacterial threats. The value of the drug industry is significantly impacted by these strategic advancements.

Segment Analysis: By Product

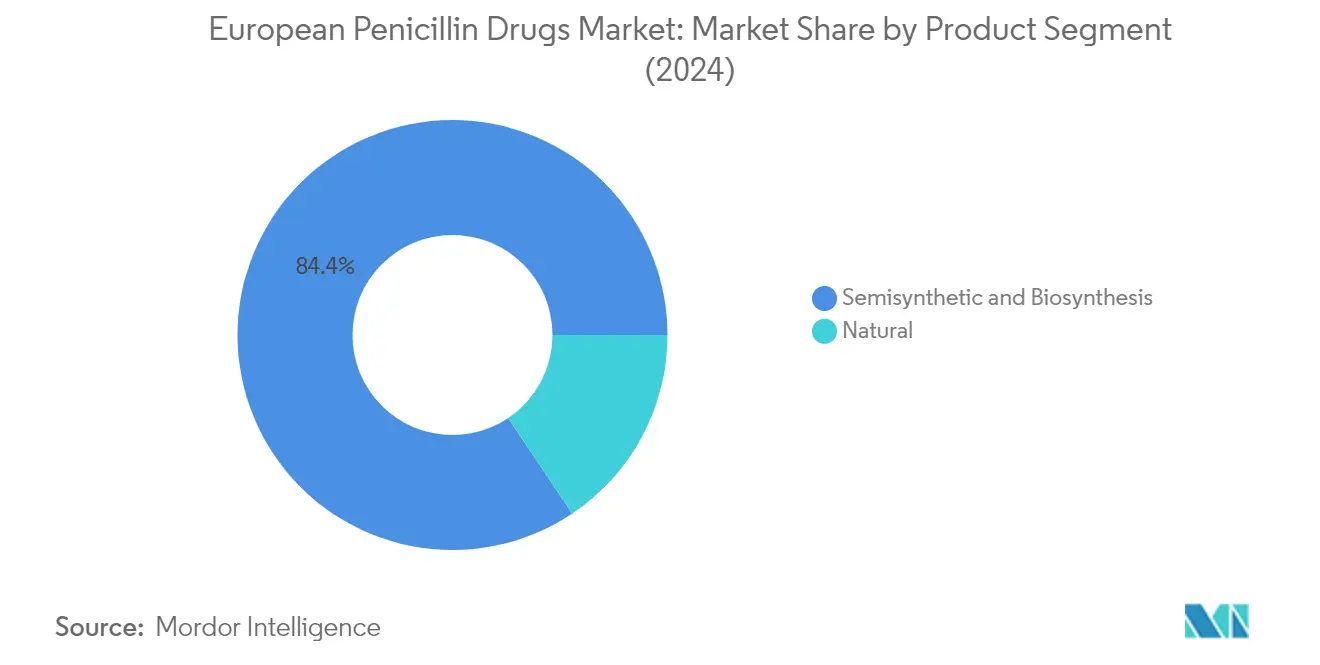

Semisynthetic & Biosynthesis Segment in European Penicillin Drugs Market

The Semisynthetic & Biosynthesis segment dominates the European penicillin drugs market, commanding approximately 84% of the market share in 2024. This segment's prominence is attributed to its diverse product portfolio, including aminopenicillin, antipseudomonal penicillin, beta-lactam and beta-lactamase inhibitors market, and penicillinase-resistant penicillin. The segment's growth is primarily driven by the increasing adoption of broad-spectrum antibiotics market and the rising prevalence of bacterial infections across Europe. Furthermore, this segment is projected to maintain its leading position with the fastest growth rate of around 3% during 2024-2029, supported by continuous research and development activities in pharmaceutical companies and the launch of novel antibiotics. The segment's growth is further bolstered by strategic investments in manufacturing facilities, such as GSK's significant investment in France to increase antibiotic production and Novartis's commitment to expanding penicillin production capabilities in Europe.

Natural Penicillin Segment in European Penicillin Drugs Market

The Natural Penicillin segment maintains a significant presence in the European penicillin drugs market, offering essential products like Penicillin G and Penicillin V. This segment's importance stems from its effectiveness against various gram-positive bacteria such as staphylococci, streptococci, and gram-negative bacteria including meningococci, Treponema, Borrelia, and Leptospira. The segment's growth is supported by its proven track record in treating severe infections and its role as a benchmark for antibiotic development. Recent comparative studies demonstrating the effectiveness and safety of natural penicillin, particularly in treating specific bacterial infections, continue to drive its adoption in clinical practice. The segment's stability is further reinforced by its cost-effectiveness and established manufacturing processes, making it an essential component of the European healthcare system's antimicrobial arsenal.

Segment Analysis: By Route of Administration

Parenteral Segment in European Penicillin Drugs Market

The parenteral segment dominates the European penicillin drugs market, commanding approximately 56% of the market share in 2024. This significant market position is attributed to the superior bioavailability and faster onset of action offered by parenteral penicillin compared to other administration routes. Parenteral penicillin demonstrates exceptional effectiveness in treating severe infections, including pyogenic infections, septic arthritis, meningitis, and surgical site infections. The segment's dominance is further strengthened by its widespread use in hospital settings for treating critical conditions and its ability to achieve therapeutic concentrations rapidly in the respiratory tract and bronchial secretions. The increasing prevalence of severe bacterial infections and the growing adoption of parenteral penicillin in European healthcare facilities continue to drive this segment's market leadership.

Oral Segment in European Penicillin Drugs Market

The oral segment in the European penicillin drugs market is projected to experience steady growth at approximately 3% CAGR from 2024 to 2029. This growth trajectory is primarily driven by the increasing prevalence of urinary tract infections (UTIs) and respiratory tract infections across Europe. The segment's expansion is further supported by various government initiatives and awareness campaigns focused on promoting appropriate antibiotic use and improving access to oral medications. The convenience of administration, patient compliance advantages, and the availability of various dosage forms such as tablets, capsules, and suspensions contribute to the segment's growth. Additionally, the rising adoption of oral penicillin products in outpatient settings and the development of new formulations with improved stability and bioavailability are expected to fuel the segment's expansion during the forecast period.

Segment Analysis: By Spectrum of Activity

Broad Spectrum Segment in Penicillin Drugs Market

The broad spectrum segment continues to dominate the European penicillin drugs market, commanding approximately 45% of the total market share in 2024. This segment's prominence is primarily attributed to the versatility and effectiveness of broad-spectrum penicillins in treating various bacterial infections, including respiratory tract infections, ear infections, urinary tract infections, and skin infections. The segment's leadership position is further strengthened by the increasing adoption of broad-spectrum antibiotics in both hospital and community settings across Europe. Looking ahead to 2024-2029, this segment is expected to maintain its growth trajectory at around 3% CAGR, driven by the rising burden of infectious diseases and the segment's crucial role in treating multiple bacterial strains simultaneously. The growth is also supported by the segment's effectiveness against both gram-positive and gram-negative bacteria, making it a preferred choice among healthcare providers for empirical treatment of infections.

Remaining Segments in Spectrum of Activity

The extended spectrum and narrow spectrum segments complete the market landscape for penicillin drugs in Europe. The extended spectrum segment holds significant importance due to its enhanced effectiveness against gram-negative bacterial infections and its crucial role in treating resistant bacterial strains. This segment is particularly valuable in hospital settings where complex infections require broader coverage. Meanwhile, the narrow spectrum segment, while smaller in market share, maintains its relevance in targeted therapy approaches where specific bacterial infections need to be addressed. This segment is particularly important in antimicrobial stewardship programs, where precise targeting of specific pathogens is preferred to minimize resistance development and optimize treatment outcomes. Both segments continue to play vital roles in providing healthcare providers with a comprehensive arsenal of treatment options for various infectious conditions.

Segment Analysis: By Distribution Channel

Hospital Pharmacies Segment in European Penicillin Drugs Market

Hospital pharmacies continue to dominate the European penicillin drugs market, commanding approximately 36% market share in 2024. This significant market position is driven by several factors including the comprehensive infrastructure of hospital pharmacies across Europe, their ability to handle complex drug dispensing requirements, and direct access to patients requiring penicillin treatments. The segment's strength is further reinforced by government initiatives supporting hospital pharmacy services, such as NHS England's investment of GBP 645 million in community pharmacy services. Additionally, the implementation of pharmacists' interventions (PI) in hospital settings has improved medication safety and optimized patient outcomes, particularly in countries like Germany where clinical pharmacists significantly contribute to medication management services. The expansion of hospital facilities across Europe, exemplified by Germany's approval of a EUR 248 million hospital construction program in 2023, has also bolstered the segment's market position.

Retail Pharmacies Segment in European Penicillin Drugs Market

The retail pharmacies segment is projected to experience the fastest growth in the European penicillin drugs market from 2024 to 2029. This growth trajectory is supported by the extensive network of retail pharmacies across Europe, with major players like Well Pharmacy operating hundreds of stores in the UK and Northern Ireland. The segment's expansion is driven by the advantages retail pharmacies offer over online channels, including personalized advice, quality customer care, and enhanced patient interaction. Retail pharmacies make particular medicines for prescriptions, supply manufacturer-made medicines, advise the public on minor illness treatments, and provide appropriate GP referrals. The growth is further supported by government policies in countries like France, where drug sales in mass-market retailing are carefully regulated to maintain continuity of care, especially in rural areas. The combination of accessibility, professional expertise, and comprehensive pharmaceutical services positions retail pharmacies for sustained growth in the penicillin drugs market.

Remaining Segments in Distribution Channel

The online pharmacies and other distribution channels segments play vital complementary roles in the European penicillin drugs market. Online pharmacies have gained prominence through platforms like AMX Holdings, Apteka.ru, and Apotea, offering convenient access to medications through digital services and home delivery options. The segment has been particularly strengthened by initiatives like the NHS Electronic Prescription Service in the UK and Spain's strategic plan to eliminate paper leaflets for hospital medications. Other distribution channels, including drug stores and chemical stores, serve as additional points of access for over-the-counter medications, though their role in penicillin distribution is more limited due to regulatory restrictions on antibiotic sales without prescriptions in most European countries.

Penicillin Drug Market Geography Segment Analysis

Penicillin Drugs Market in France

France dominates the European penicillin drugs landscape, commanding approximately 19% of the drug market share in 2024. The country's market is projected to grow at nearly 4% annually from 2024 to 2029, driven by significant government initiatives to restore domestic antibiotic production. The French government's strategic investment of EUR 160 million to support new production projects, including amoxicillin manufacturing by GSK in northwestern France, demonstrates its commitment to strengthening the local pharmaceutical infrastructure. The country's robust healthcare system, coupled with comprehensive antibiotic stewardship programs, has created a conducive environment for market growth. Furthermore, France's focus on research and development in the pharmaceutical sector, particularly in developing novel antibiotic formulations, has attracted significant investments from major pharmaceutical companies. The presence of key market players and their continued expansion of manufacturing capabilities in the region has also contributed to France's penicillin market leadership position.

Penicillin Drugs Market in Italy

Italy's penicillin drugs market demonstrates remarkable strength, particularly in the pediatric segment. The country's healthcare system places significant emphasis on appropriate antibiotic prescribing practices, with amoxicillin being the first-line treatment choice for common pediatric infections according to Italian guidelines. The robust presence of both domestic and international pharmaceutical manufacturers has established Italy as a key production hub for penicillin-based antibiotics. The country's well-developed healthcare infrastructure, combined with its strong focus on antimicrobial stewardship programs, has created a sustainable ecosystem for market growth. Additionally, Italy's strategic geographical location and strong trade relationships with other European countries have facilitated efficient distribution networks. The country's commitment to maintaining high-quality standards in pharmaceutical production, evidenced by strict regulatory compliance and continuous monitoring systems, has further strengthened its position in the European penicillin drugs market.

Penicillin Drugs Market in Spain

Spain has emerged as a crucial player in the European penicillin drugs market, supported by significant investments in manufacturing infrastructure and research capabilities. The country's strategic focus on developing its pharmaceutical sector is exemplified by Sandoz's substantial investment in expanding its penicillin production capabilities. Spain's healthcare system's emphasis on rational antibiotic use, coupled with comprehensive surveillance programs for antimicrobial resistance, has created a structured framework for market growth. The country has also made significant strides in digitalizing healthcare services, including the implementation of electronic prescription systems and online pharmacy services. The Spanish Agency for Medicines and Health Products' initiatives to modernize pharmaceutical documentation and distribution systems have further enhanced market efficiency. Moreover, Spain's strong research institutions and clinical trial infrastructure have attracted international pharmaceutical companies, fostering innovation in penicillin drug development and manufacturing.

Penicillin Drugs Market in Germany

Germany's penicillin drugs market is characterized by its strong focus on research and development, particularly in addressing antimicrobial resistance challenges. The country's robust pharmaceutical manufacturing sector, supported by advanced technology and stringent quality controls, has established it as a key producer of penicillin-based antibiotics. The German healthcare system's emphasis on evidence-based prescribing practices and comprehensive antibiotic stewardship programs has created a balanced market environment. The presence of major pharmaceutical companies and research institutions has fostered continuous innovation in antibiotic development. Furthermore, Germany's strategic initiatives, such as the German Network against Antimicrobial Resistance, have strengthened the country's position in developing new and resistance-breaking antibiotics. The nation's well-established distribution networks and healthcare infrastructure ensure efficient delivery of penicillin drugs to both hospitals and retail pharmacies.

Penicillin Drugs Market in Other Countries

The penicillin drugs market in other European countries, including the United Kingdom, Netherlands, Switzerland, Belgium, and other Nordic countries, demonstrates diverse growth patterns influenced by their respective healthcare policies and market dynamics. These countries have implemented various initiatives to combat antimicrobial resistance while ensuring adequate access to essential antibiotics. Their markets are characterized by strong regulatory frameworks, well-established healthcare systems, and increasing focus on sustainable antibiotic production. The presence of major pharmaceutical companies and research institutions in these countries continues to drive innovation in penicillin drug development. Additionally, these nations have developed robust distribution networks and healthcare infrastructure, supporting efficient delivery of penicillin drugs to various healthcare settings. Their commitment to maintaining high-quality standards in pharmaceutical production and distribution has contributed to the overall growth of the European penicillin drugs market.

Get Analysis on Important Geographic Markets

Download PDF

Penicillin Drug Industry Overview

Top Companies in Penicillin Drug Market

The European penicillin drugs market features prominent pharmaceutical companies, including Pfizer, Novartis, Sanofi, GSK, and Merck & Co., leading the competitive landscape. These companies are increasingly focusing on product innovation through research and development of novel penicillin drug formulations to combat antimicrobial resistance. Operational agility is demonstrated through strategic manufacturing partnerships and optimization of supply chain networks across Europe. Companies are making strategic moves to strengthen their market position through licensing agreements and portfolio expansion in key therapeutic areas. Geographic expansion efforts are particularly concentrated in emerging European markets, with companies establishing local manufacturing facilities and distribution networks to enhance market penetration and ensure supply chain resilience.

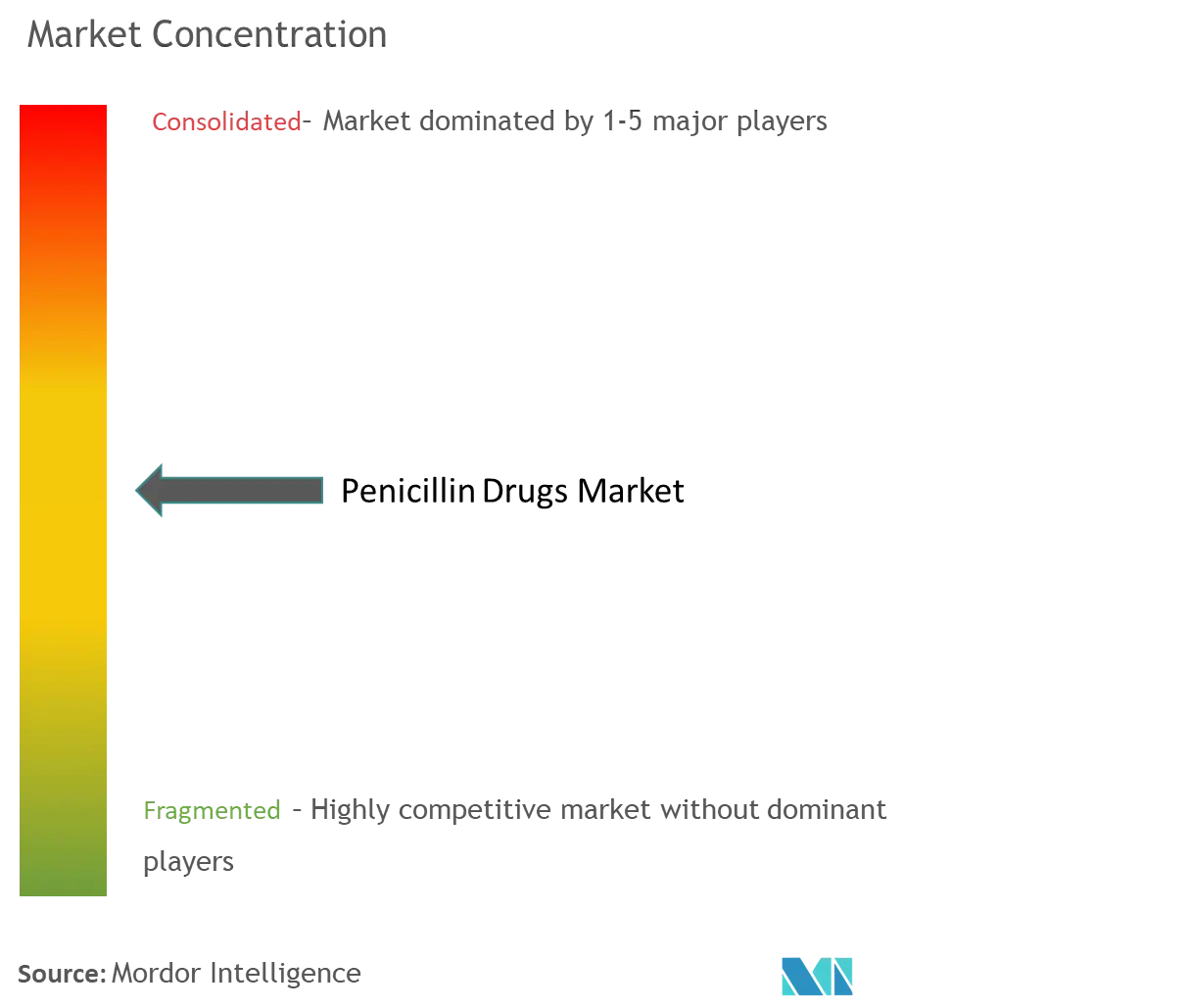

Consolidated Market with Strong Global Players

The European penicillin market is characterized by a mix of global pharmaceutical conglomerates and specialized generic manufacturers, with global players holding dominant drug market share through their established brand portfolios and extensive distribution networks. These major players leverage their substantial research and development capabilities, manufacturing infrastructure, and regulatory expertise to maintain market leadership. The market demonstrates moderate consolidation, with larger pharmaceutical companies often acquiring smaller specialized manufacturers to expand their product portfolios and geographic reach. The presence of strong regional players, particularly in markets like Germany, France, and the United Kingdom, adds to the competitive dynamics while maintaining healthy market competition.

The market has witnessed significant merger and acquisition activities, primarily driven by the need to achieve economies of scale and expand product portfolios. Global pharmaceutical companies are increasingly acquiring local manufacturers to strengthen their presence in specific European regions and gain access to established distribution networks. These strategic acquisitions also help companies overcome regulatory barriers and achieve faster market access. The trend of vertical integration is evident as companies seek to control the entire value chain from API manufacturing to final drug formulation and distribution.

Innovation and Compliance Drive Market Success

For incumbent companies to maintain and increase their market share, a focus on continuous innovation in drug formulation and delivery systems remains crucial. Companies need to invest in research and development to address emerging bacterial resistance patterns and develop more effective penicillin drugs variants. Building strong relationships with healthcare providers and maintaining high-quality standards in manufacturing are essential success factors. Additionally, incumbents must optimize their supply chain operations and maintain competitive pricing strategies while ensuring compliance with evolving regulatory requirements. Developing comprehensive antibiotic stewardship programs and engaging in sustainable manufacturing practices are becoming increasingly important for market leadership.

For contending companies looking to gain ground, focusing on niche market segments and developing specialized formulations presents significant opportunities. Success factors include building strong regulatory compliance capabilities, establishing efficient distribution networks, and developing strategic partnerships with local healthcare providers. Companies must also consider the high concentration of institutional buyers in the market and develop targeted marketing strategies accordingly. The risk of substitution from alternative antibiotics and emerging therapeutic approaches necessitates continuous innovation and differentiation in product offerings. Future success will increasingly depend on the ability to navigate complex regulatory requirements while maintaining cost competitiveness and ensuring reliable supply chains.

Penicillin Drug Market Leaders

-

Pfizer Inc.

-

Novartis AG

-

GSK plc

-

Lupin Limited

-

Sanofi SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Penicillin Drug Market News

- April 2023: Baxter International Inc. launched Zosyn (piperacillin and tazobactam) Injection in the United States. Zosyn premix is indicated for the treatment of multiple infections caused by susceptible bacteria and is available in Baxter’s proprietary single-dose Galaxy containers.

- January 2023: Juno Pharmaceuticals Canada received approval from Health Canada to import Amoxicillin powder for oral suspension pursuant to Health Canada’s exceptional importation and sale guidelines.

Penicillin Drug Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Burden of Infectious Diseases

- 4.2.2 Increasing Research and Development Activities in the Pharmaceutical Industry

- 4.2.3 Increasing Demand and Development of Generic Drugs

-

4.3 Market Restraints

- 4.3.1 Antimicrobial Resistance and Availability of Novel Antibacterials

- 4.3.2 Stringent Regulatory Framework

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value in USD)

-

5.1 By Source

- 5.1.1 Natural

- 5.1.2 Semisynthetic & Biosynthesis

- 5.1.2.1 Aminopenicillin

- 5.1.2.2 Antipseudomonal Penicillin

- 5.1.2.3 Beta-lactamase Inhibitor

- 5.1.2.4 Penicillinase-resistant Penicillin

-

5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Parenteral

-

5.3 By Spectrum of Activity

- 5.3.1 Narrow Spectrum

- 5.3.2 Broad Spectrum

- 5.3.3 Extended Spectrum

-

5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Other Distribution Channels

-

5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Pfizer, Inc.

- 6.1.2 Novartis AG

- 6.1.3 Sanofi SA.

- 6.1.4 Aenova Group

- 6.1.5 GSK plc

- 6.1.6 Merck & Co., Inc.

- 6.1.7 Teva Pharmaceuticals

- 6.1.8 Sun Pharmaceutical Industries

- 6.1.9 Lupin Limited

- 6.1.10 Cipla Limited

- 6.1.11 F. Hoffmann-La Roche AG

- 6.1.12 Wellona Pharma

- 6.1.13 AdvaCare Pharma

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Penicillin Drug Industry Segmentation

As per the scope of the report, penicillin refers to a class of antibiotics used as a drug to treat and prevent bacterial infections and diseases. Penicillin is active against several types of bacteria including Streptococcus pneumonia, Listeria, Neisseria gonorrhea, Clostridium, Peptococcus, and Peptostreptococcus. The majority of penicillins used in therapeutics are chemically synthesized from penicillins that are produced naturally.

The penicillin drug market is segmented by source (natural, semisynthetic, and biosynthesis (aminopenicillin, antipseudomonal penicillin, beta-lactamase inhibitor, and penicillinase-resistant penicillin), route of administration (oral and parenteral), spectrum of activity (narrow spectrum, broad spectrum, and extended spectrum), distribution channel (hospital pharmacies, retail pharmacies, online pharmacies, and other distribution channels), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.

| By Source | Natural | ||

| Semisynthetic & Biosynthesis | Aminopenicillin | ||

| Antipseudomonal Penicillin | |||

| Beta-lactamase Inhibitor | |||

| Penicillinase-resistant Penicillin | |||

| By Route of Administration | Oral | ||

| Parenteral | |||

| By Spectrum of Activity | Narrow Spectrum | ||

| Broad Spectrum | |||

| Extended Spectrum | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online Pharmacies | |||

| Other Distribution Channels | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Penicillin Drug Market Research FAQs

How big is the Penicillin Drug Market?

The Penicillin Drug Market size is expected to reach USD 11.05 billion in 2025 and grow at a CAGR of 3.21% to reach USD 12.95 billion by 2030.

What is the current Penicillin Drug Market size?

In 2025, the Penicillin Drug Market size is expected to reach USD 11.05 billion.

Who are the key players in Penicillin Drug Market?

Pfizer Inc., Novartis AG, GSK plc, Lupin Limited and Sanofi SA are the major companies operating in the Penicillin Drug Market.

Which is the fastest growing region in Penicillin Drug Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Penicillin Drug Market?

In 2025, the North America accounts for the largest market share in Penicillin Drug Market.

What years does this Penicillin Drug Market cover, and what was the market size in 2024?

In 2024, the Penicillin Drug Market size was estimated at USD 10.70 billion. The report covers the Penicillin Drug Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Penicillin Drug Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Penicillin Drug Market Research

Mordor Intelligence offers a comprehensive analysis of the penicillin drug market, drawing on decades of expertise in pharmaceutical industry research. Our extensive coverage includes broad spectrum antibiotics and beta lactam compounds. We provide a detailed examination of penicillin medicine development and manufacturing processes. The report explores various aspects, from the source of penicillin to the production of semi-synthetic penicillin. It also analyzes the antibiotic drug landscape and the penicillin intermediates market.

This strategic report, available as an easy-to-download PDF, provides stakeholders with crucial insights into penicillin medication trends and market dynamics. Our analysis covers the complete value chain, from 6 aminopenicillin acid production to end-user applications such as penicillin gel. The report includes detailed SAR of penicillin studies and evaluates the impact of beta lactamase inhibitors on market growth. Stakeholders gain access to comprehensive data about penicillin drugs manufacturing processes, regulatory frameworks, and competitive landscapes. This enables informed decision-making in this crucial pharmaceutical sector.