| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Market Size (2025) | USD 15.93 Billion |

| Market Size (2030) | USD 19.38 Billion |

| CAGR (2025 - 2030) | 4.00 % |

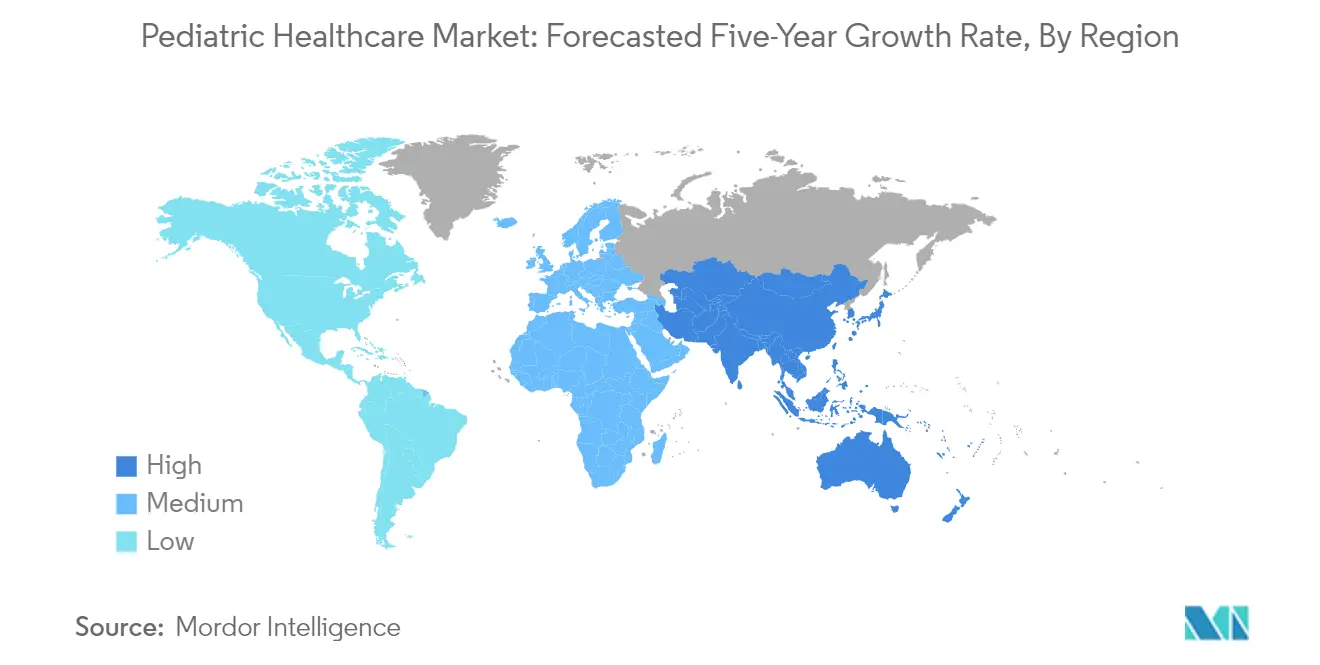

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order |

Pediatric Healthcare Market Analysis

The Pediatric Healthcare Market size is estimated at USD 15.93 billion in 2025, and is expected to reach USD 19.38 billion by 2030, at a CAGR of 4% during the forecast period (2025-2030).

The Vanishing Pediatric Infrastructure: Adapting to a New Care Reality

The pediatric healthcare market is facing a structural challenge. Only 37% of United States hospitals now offer pediatric services – down from 42% a decade ago. This decline is forcing the industry to rethink how children receive care. Healthcare systems are now exploring regional hub models where pediatric expertise is concentrated in central facilities, supported by community services and telehealth. This evolution is especially important in rural areas, where pediatric specialists have always been scarce. Progressive health systems are combining in-person and virtual care to ensure children can access specialists regardless of where they live. For stakeholders in the global pediatric health field, this represents a turning point: success will depend less on traditional hospital infrastructure and more on creating flexible, tech-enabled networks that deliver specialized care across distances while maintaining quality and patient-centered approaches. Organizations that adapt to this new distributed care model will be better positioned to serve pediatric populations effectively in this changing landscape.

The Utilization-Specialization Disconnect: Meeting High Demand with Targeted Solutions

A notable contradiction exists in today's pediatric healthcare products and services market: almost all children see doctors, yet many can't access specialized care. In 2023, 95% of children in the United States had at least one healthcare visit, showing nearly universal engagement with the healthcare system. However, this high usage masks significant gaps in access to pediatric specialists. Family doctors increasingly handle conditions that ideally require specialized knowledge, particularly for chronic issues like asthma, developmental disorders, and mental health. This gap has created a growing market for solutions that connect general care with pediatric expertise—including clinical decision support tools, remote consultation platforms, and specialized training for primary care providers. As pediatric trends evolve, organizations that develop models to address this specialization gap will gain market advantage. The opportunity isn't in competing for routine pediatric visits, but in developing solutions that enhance the quality and specialization of care during these already-occurring appointments.

The Digital Pediatric Frontier: First-Mover Advantage in an Underserved Space

While digital health has transformed many healthcare areas, the pediatric healthcare market trends show a surprising lack of innovation in solutions designed specifically for children. Industry experts note this space remains wide open—with Brenda Schmidt of Redesign Health suggesting that entrepreneurs could develop 30 pediatric tech solutions without overcrowding the market. This gap offers rare first-mover advantages in an otherwise competitive healthcare technology landscape. Several factors contribute to this untapped potential: complex regulations for pediatric products, the challenge of creating age-appropriate interfaces for different developmental stages, and specialized privacy requirements for managing children's health data. However, these barriers create defensible market positions for companies willing to navigate them. Across the pediatric industry, early entrants are focusing on condition-specific digital therapeutics, parental monitoring tools, and telehealth platforms designed specifically for younger patients. The key opportunity is clear: pediatric digital health offers strong market demand with relatively little competition—a scenario that smart healthcare investors and innovators are increasingly targeting.

Pediatric Healthcare Market Trends

The Silent Epidemic: Rising Mental Health Challenges Reshape Pediatric Care Priorities

Today's pediatric healthcare providers face a significant mental health crisis requiring specialized resources. In 2023, 16% of youth in the United States reported experiencing at least one major depressive episode, with more than 2.7 million children and adolescents living with severe major depression. This growing challenge requires healthcare systems to adopt integrated care models where mental health assessment becomes a standard part of routine pediatric visits. Providers who incorporate mental health screening tools into their standard protocols are positioning themselves as comprehensive care leaders in the competitive pediatric market.The pediatric health care landscape shows notable regional and demographic differences in disease patterns. Severe major depression rates reach nearly 20% among youth in South Dakota compared to just 5.20% in South Carolina, with substance use disorders affecting over 6% of American youth. Particularly concerning is the 16.5% prevalence of severe depression among multiracial youth, highlighting how social factors directly influence health outcomes. For healthcare organizations, these varied needs present an opportunity to develop specialized programs targeting specific conditions within demographic groups—addressing critical gaps in the pediatric healthcare market while creating new service offerings.

Beyond Band-Aids: Strategic Investments in Pediatric Research Fueling Treatment Innovations

The growing awareness of pediatric medicine among families and healthcare stakeholders is changing how care is sought and delivered. Data shows that youth with insurance coverage for mental health treatments were 11.1% more likely to receive care, demonstrating how increased awareness leads to improved healthcare utilization. This trend extends beyond mental health to all pediatric healthcare services. As parents become more informed about treatment options, providers who clearly communicate their research-backed approaches gain an advantage in today's consumer-driven healthcare environment.Industry leaders are forming strategic partnerships to advance pediatric research. The 2024 ten-year collaboration between Koninklijke Philips N.V. and Nicklaus Children's Health System illustrates this shift, creating a framework for innovation specifically for pediatric patients. These partnerships represent a change in how pediatric research progresses—moving from isolated studies toward integrated clinical-corporate collaborations that speed up implementation of new treatments. Organizations participating in these collaborative networks gain early access to emerging technologies and valuable data that can inform pediatric healthcare market trends before they become industry standards.

Smart Solutions for Small Patients: Tech-Enabled Care Elevates Pediatric Treatment Standards

Advanced diagnostic technologies optimized for pediatric use are transforming care delivery and treatment effectiveness. Philips' SmartWorkflow and SmartSpeed MR technologies reduce exam times by up to 65%, an important advancement that decreases sedation needs and improves the experience for young patients who struggle with lengthy imaging procedures. These efficiency improvements lead to earlier interventions, reduced costs, and better patient satisfaction—key advantages for pediatric healthcare providers in competitive markets. Organizations investing in these diagnostic technologies can handle more patients while delivering better care experiences that drive both referrals and retention.Treatment technologies are also seeing pediatric-focused improvements that enhance clinical workflows and patient outcomes. AI-enabled ultrasound systems like Philips' EPIQ CVx and Compact 5500CV reduce cardiac quantification time by 51% while decreasing 2D imaging exam time by 20%, particularly valuable when working with pediatric cardiac patients who may have limited cooperation. The pediatric healthcare market rewards providers who use these specialized technologies to create child-friendly environments where advanced treatment doesn't mean additional discomfort. As these technologies become more portable and non-invasive, they enable continuous care models extending beyond hospitals into homes and schools—creating new approaches that better serve chronically ill children.

Segment Analysis: By Type

Chronic Conditions: The Dominant Force in Pediatric Care

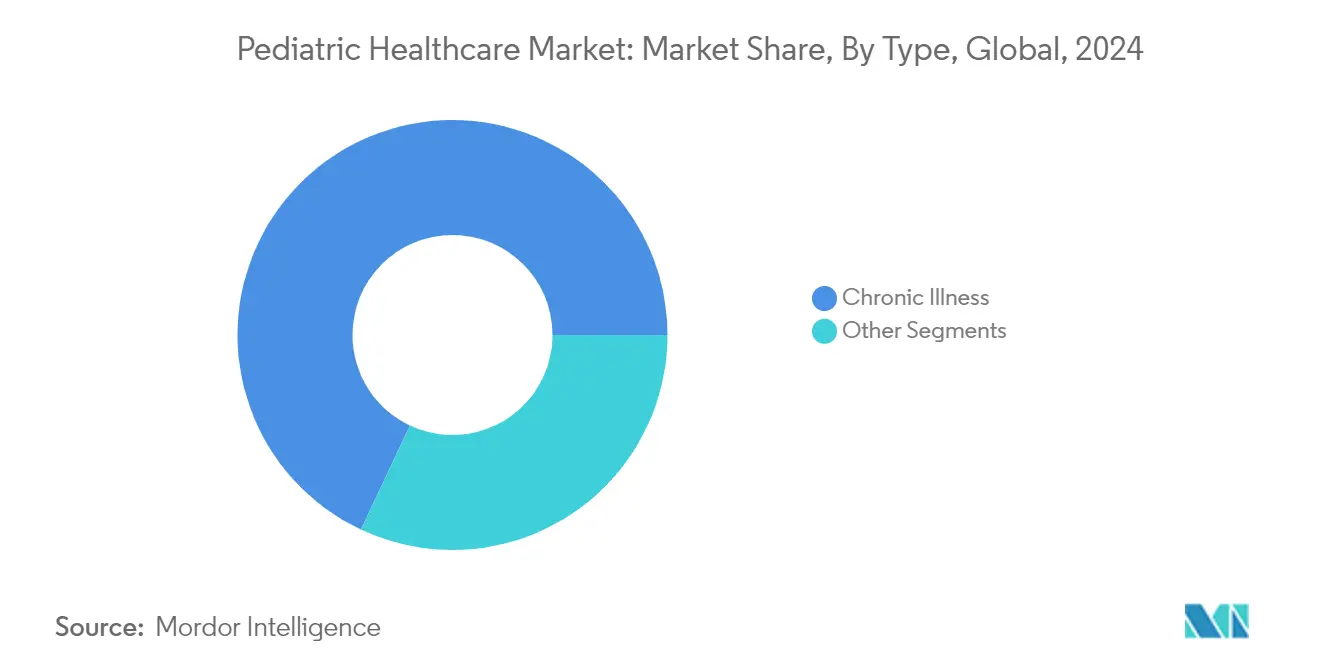

In today's pediatric healthcare market, chronic conditions have established a commanding position with a 61.2% market share while simultaneously achieving an impressive 8.9% growth rate annually. This dual dominance reflects the increasing prevalence of long-term conditions including childhood asthma, diabetes, allergies, and developmental disorders that require ongoing management rather than one-time interventions. Healthcare providers are responding with specialized equipment designed specifically for monitoring these conditions, such as pediatric stethoscopes engineered to capture higher-frequency sounds above 200 Hz for more accurate assessment of persistent respiratory and cardiac issues. The strategic implications for industry participants are clear – success in this segment demands developing integrated care systems that address the full spectrum of chronic disease management rather than isolated treatment products.

Acute Care: The Critical Response System

While representing a smaller portion of the pediatric market, acute illness management remains essential as the frontline defense against sudden health emergencies in children. This segment's critical importance is evidenced by the development of specialized emergency tools like the Broselow Pediatric Emergency Tape, standardized for children up to approximately 12 years of age and 79 lbs, which provides vital guidance on equipment sizing and medication dosing during urgent care situations. The practical reality for healthcare facilities is the necessity to maintain dual-capability systems – robust chronic disease management alongside rapid-response acute interventions. This balanced approach represents a fundamental requirement rather than an optional strategy, as institutions that excel in both areas position themselves as comprehensive care providers capable of addressing the complete spectrum of childhood health needs.

Segment Analysis: By Treatment

Vaccines: The Preventive Foundation

Preventative medicine through immunization continues as the cornerstone of the pediatric healthcare market, capturing 46.7% of the treatment segment as healthcare systems worldwide prioritize disease prevention over cure. This substantial market position reflects both clinical best practices and parental preferences for avoiding illness altogether. The effectiveness of modern vaccination programs depends on precision throughout the supply chain, with digital thermometers used for vaccine storage monitoring recommended to maintain accuracy rates of ±0.4 or better to ensure potency and efficacy. For stakeholders across the global pediatric health ecosystem, the strategic calculation is straightforward – comprehensive vaccination infrastructure delivers superior health economics by reducing downstream burden on acute and chronic care facilities, making it both a clinical and financial imperative.

Pharmaceutical Solutions: The Growth Engine

The pediatric pharmaceutical segment is experiencing remarkable acceleration at 10.4% annual growth as advancements in formulation technology and dedicated pediatric clinical trials address children's unique physiological needs. This expansion is supported by increasingly precise administration protocols, exemplified by age-appropriate equipment requirements where blood pressure cuff sizes range from 4×8 cm for newborns to 9×12 cm for older children. The message for pharmaceutical developers is both an opportunity and responsibility – companies that successfully develop child-specific drug formulations with appropriate safety profiles, palatability considerations, and flexible dosing options will capture dominant positions in this expanding segment. This represents a significant shift from historical approaches where pediatric medicine market solutions were often simply downsized adult formulations rather than purpose-built pediatric interventions.

Comprehensive Support Technologies

The diverse ecosystem of non-pharmaceutical, non-vaccine interventions represents a vital component of holistic pediatric healthcare, encompassing diagnostic equipment, therapeutic devices, digital health solutions, and specialized support services. This category benefits from continuous innovation in measurement precision, as demonstrated by pediatric stadiometers that measure recumbent length from 14 to 42 inches, ensuring accurate physical development tracking throughout childhood. Forward-thinking providers are increasingly recognizing that truly effective pediatric care extends beyond medications and vaccines to include complementary technologies and services. The most successful organizations in this space are those creating integrated solutions that address the complete spectrum of childhood health needs while simultaneously meeting value-based care metrics that satisfy both clinical requirements and economic constraints.

Geography Analysis

North America: The Powerhouse of Pediatric Healthcare Innovation

North America leads the global pediatric healthcare market thanks to strong insurance systems, advanced infrastructure, and significant R&D investments. Despite this leadership, access issues persist with about 800,000 children aged 1-5 years and 2.9 million aged 6-18 years in the United States remaining uninsured as of 2022. This gap between advanced capabilities and uneven coverage creates opportunities for companies developing affordable pediatric solutions. The key challenge for market players is addressing these coverage disparities through innovative business models and partnerships that can improve care delivery while supporting business growth. For stakeholders looking to maximize impact in this region, solutions that bridge accessibility gaps while maintaining clinical excellence will find fertile ground for development and implementation.

United States: Market Giant with Persistent Care Gaps

The United States holds the largest pediatric market share in North America, supported by extensive research and healthcare infrastructure. However, significant disparities exist, particularly along ethnic lines—approximately 12% of American Indian and Alaska Native children, 8% of Hispanic children, and 4% of white children lacked health insurance in 2022. This uneven landscape means market players should focus on developing culturally appropriate care models and partnerships with institutions serving diverse populations. The key opportunity isn't just expanding in established markets but identifying underserved demographic segments where specialized approaches can drive both social impact and business growth, especially as value-based care becomes more important in the evolving healthcare landscape.

Canada: The Fast-Emerging Frontier in Pediatric Care Delivery

Canada represents the fastest-growing pediatric healthcare market in North America, driven by investments in universal healthcare and preventive care emphasis. This growth offers important lessons for companies—particularly in how public health integration creates sustainable market opportunities. Organizations most likely to succeed here are those developing solutions that align with Canada's community-based care approach and preventive services focus. Companies should focus on aligning their products and services with Canada's long-term public health objectives to create lasting partnerships rather than short-term sales relationships. The emphasis on preventive care in this market signals a valuable direction for product development and service design that may influence broader trends in pediatric health care.

Mexico and Beyond: Diverse Markets with Untapped Potential

Mexico presents contrasting opportunities—rapid urban development alongside rural healthcare gaps creates a market requiring tailored approaches. Ongoing healthcare reforms favor providers offering affordable, scalable solutions that work within resource limitations. Unlike the US market's technology focus, Mexico's growth centers on accessible primary care and building sustainable healthcare infrastructure in underserved areas. Companies should develop hybrid models combining affordability with clinical effectiveness, which can serve as templates for other emerging markets. Solutions that can adapt across diverse infrastructure capabilities will succeed not only in Mexico but in similar markets globally, creating a blueprint for balanced pediatric healthcare delivery systems.

Europe: Balancing Tradition and Innovation in Pediatric Care

Europe's pediatric healthcare approach combines established universal coverage with leading-edge research initiatives. The region's strong position comes from solid public health systems and regulations that prioritize pediatric drug development. However, Europe faces challenges from declining birth rates alongside increased migration, creating complex service delivery issues. The pandemic revealed both strengths and weaknesses in European pediatric systems, speeding up digital health adoption while highlighting regional differences in specialty care access. Companies should develop solutions that work well with existing public health systems while addressing gaps in mental health, developmental disorders, and chronic condition management—areas where traditional systems sometimes fall short despite Europe's overall advanced healthcare infrastructure.

Germany: The Cornerstone of European Pediatric Excellence

Germany represents Europe's largest pediatric healthcare market, built on a dual public-private insurance system that provides nearly universal coverage while maintaining innovation. The country excels in developing pediatric specialties and preventive care programs but faces growing challenges in addressing children's mental health needs and integrating digital tools into traditional practices. For companies, the opportunity isn't just accessing Germany's large market but understanding how its evidence-driven approach to healthcare creates specific paths for adoption. Organizations that can demonstrate both clinical effectiveness and economic value through Germany's thorough evaluation process will succeed not only in this key market but across Europe, as German practices often influence broader European standards and pediatric healthcare market trends.

United Kingdom: Pioneering New Models of Integrated Pediatric Care

The United Kingdom stands as Europe's fastest-growing pediatric market, reflecting its bold restructuring of children's healthcare through integrated systems connecting hospital services with community support. This growth comes from substantial National Health Service (NHS) investments in children's mental health, digital infrastructure, and specialized care pathways. The UK's approach offers valuable insights for companies—particularly in how traditionally separate care areas are being connected to improve outcomes. Organizations positioned to succeed here are those developing solutions that work across multiple care settings and show measurable improvements within budget constraints. Companies shouldn't just focus on selling to the UK system but understanding how its integrated approach is reshaping expectations for paediatric healthcare services throughout Europe.

Continental Diversity: From Mediterranean Models to Nordic Innovations

Europe's other pediatric markets—France, Italy, Spain, and smaller nations—show diverse approaches reflecting distinct cultural and historical healthcare traditions. France maintains strengths in pharmaceutical innovation while facing challenges in coordinating regional services. Italy and Spain, despite budget limitations, continue developing innovative community-based models that maximize resources, especially in preventive care. Nordic countries, though smaller markets, provide valuable examples of digital health integration and outcomes-focused pediatric care. For companies, Europe's diverse approaches create opportunities to adapt solutions across different contexts—successful approaches in resource-limited Mediterranean markets may offer insights for cost-effective implementation elsewhere. The key strategy involves identifying transferable innovations that can work across Europe's varied healthcare systems while respecting each market's unique characteristics.

Asia-Pacific: The Rising Force in Pediatric Healthcare Innovation

Asia-Pacific represents the most dynamic region in pediatric healthcare market trends, combining rapid growth with unprecedented scale and diversity. The region features contrasting approaches—from Japan's technology-intensive pediatric centers to India's practical innovations designed for population-scale impact. China's expanding healthcare coverage has created new opportunities for pediatric service delivery, with approximately 2,500 general hospitals in Japan providing pediatric departments as of October 2023. The region's health challenges differ fundamentally from Western markets—infectious diseases remain important alongside rapidly rising chronic conditions. For companies, Asia-Pacific requires solutions designed specifically for its unique contexts rather than adapted Western approaches. Organizations developing scalable, affordable pediatric interventions that can function across diverse infrastructure environments will capture substantial value as regional healthcare spending continues to grow.

Middle East and Africa: Contrasting Realities in Pediatric Care Access

The Middle East and Africa region presents dramatic contrasts in pediatric healthcare—Gulf Cooperation Council (GCC) nations invest heavily in world-class pediatric facilities while much of Africa faces basic challenges in primary care access. This division creates distinct market opportunities; GCC countries increasingly focus on specialized centers for complex pediatric conditions, advanced diagnostics, and precision medicine. Meanwhile, across much of Africa, critical needs center on basic preventive services, infectious disease management, and sustainable primary care models. This regional contrast requires different business approaches. Success in GCC markets requires cutting-edge offerings aligned with ambitious healthcare transformation initiatives, while African opportunities require innovative delivery models that overcome infrastructure and resource limitations. Companies developing adaptable solutions that can be configured appropriately across this spectrum will make significant progress in this challenging but increasingly important region.

South America: Navigating Complexity in Pediatric Care Delivery

South America's pediatric healthcare landscape showcases innovative approaches despite resource constraints. The region has pioneered community-based pediatric care models that maximize impact with limited infrastructure—approaches increasingly studied globally as examples of efficient service design. Brazil leads the regional market, having built substantial pediatric specialty capacity in cities, though rural access remains challenging. The region faces a unique challenge: addressing growing chronic disease in children while continuing to fight infectious diseases—requiring careful resource allocation. In response, South American health systems have developed hybrid models combining prevention with specialized care in practical configurations. For companies, the region offers valuable lessons in creating sustainable pediatric solutions that balance clinical effectiveness with implementation realities. Organizations developing pediatric products with flexible implementation requirements, modest infrastructure needs, and clear value propositions will succeed in this challenging but innovation-rich environment.

Pediatric Healthcare Industry Overview

Innovation as the New Currency: Strategic Realignment in Pediatric Care

In the global pediatric health sector, companies are moving beyond simple market share competition, with innovation becoming the key factor in long-term success. Major players like Johnson & Johnson, Pfizer, and GlaxoSmithKline are investing heavily in pediatric-specific R&D to address treatment gaps in chronic conditions, which make up 61.2% of the market. This focus on innovation extends to healthcare institutions too - Boston Children's Hospital has maintained its top ranking in the nation for nine consecutive years by continuously advancing its care approaches and treatment methods. Companies that prioritize breakthrough solutions rather than small improvements are creating strong market positions while expanding their reach, especially in the fast-growing drugs segment with its 10.4% annual growth. The real winners are organizations developing unique technologies for precise dosing, better safety, and child-appropriate formulations - creating lasting advantages that simple market share battles can't match.

Beyond Solo Acts: The Ecosystem Advantage in Pediatric Healthcare

Today's pediatric healthcare market leaders are standing out not through individual products but by building comprehensive care ecosystems. Smart companies are creating networks through strategic partnerships, acquisitions, and platforms that address multiple aspects of patient care. We see this ecosystem approach in provider networks like the Texas-based pediatric system with over 60 locations offering primary, specialty, and urgent care services - creating a network that smaller competitors find hard to match. Similarly, pharmaceutical companies are forming alliances with digital health companies, diagnostic firms, and research institutions to develop complete solutions rather than standalone products. Companies building these integrated healthcare ecosystems gain advantages through network effects, data insights, and streamlined care coordination that isolated providers simply can't replicate - allowing them to deliver better outcomes while capturing more value across the pediatric care landscape.

The Precision Imperative: Tailored Solutions Reshaping Competitive Dynamics

The pediatric industry is experiencing a major shift as companies developing precisely targeted treatments gain advantages over those offering one-size-fits-all approaches. Market leaders are investing in genomics, biomarkers, and data analytics to create treatments tailored to children's unique needs at different developmental stages. This focus on precision is reflected in the scale of specialized institutions, such as the Fort Worth pediatric healthcare provider with over 5,800 employees delivering specialized care across multiple areas. The business implications are clear: companies developing targeted therapies for specific pediatric conditions can dominate valuable niche segments while commanding higher prices for better outcomes. Organizations that excel at collecting and analyzing pediatric-specific data gain insights that guide smarter R&D investments, better clinical trials, and more effective marketing - creating an information advantage that grows over time and directly improves market performance.

Pediatric Healthcare Market Leaders

-

GlaxoSmithKline plc

-

Johnson & Johnson

-

The Procter & Gamble Company

-

Boehringer Ingelheim

-

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Pediatric Healthcare Market News

- April 2022: Gilead opened a pediatric drug development center in Ireland. The new pediatric center out of Ireland will conduct pediatric clinical trials for seven products across 18 countries.

- February 2022: Pfizer Inc., and BioNTech initiated a rolling submission seeking to amend the Emergency Use Authorization (EUA) of the Pfizer-BioNTech COVID-19 Vaccine to include children 6 months through 4 years of age, in response to the urgent public health need in this population.

Pediatric Healthcare Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Burden of Pediatric Diseases

- 4.2.2 Increased R&D Activities and Awareness of Pediatric Medicine Among Public

- 4.2.3 Increasing Availability of Advanced Technologies To Provide Continuous Care

-

4.3 Market Restraints

- 4.3.1 Small Size of Study Population and Ethical Issues in Pediatric Research

- 4.3.2 Complications Associated with the Medicines

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Type

- 5.1.1 Chronic Illness

- 5.1.2 Acute Illness

-

5.2 By Treatment

- 5.2.1 Vaccines

- 5.2.2 Drugs

- 5.2.3 Others

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Viatris

- 6.1.3 Boehringer Ingelheim International GmbH

- 6.1.4 Eli Lilly and Company

- 6.1.5 Eisai Co.

- 6.1.6 GlaxosmithklinePlc

- 6.1.7 Gilead Sciences

- 6.1.8 Johnson & Johnson

- 6.1.9 Pfizer Inc

- 6.1.10 Sanofi S A

- 6.1.11 The Procter & Gamble Company

- 6.1.12 Novartis International AG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Pediatric Healthcare Industry Segmentation

As per the scope of this report, pediatric healthcare is a branch of medicine that deals with the medical care, development, and related diseases of infants, children, and adolescents. The pediatric healthcare market grows significantly as children often suffer from gastrointestinal, allergic, respiratory, and other chronic diseases owing to their lower immunity. The Pediatric Healthcare Market is Segmented by Type (Chronic Illness and Acute Illness), Treatment (Vaccines, Drugs, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| By Type | Chronic Illness | ||

| Acute Illness | |||

| By Treatment | Vaccines | ||

| Drugs | |||

| Others | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Pediatric Healthcare Market Research Faqs

How big is the Pediatric Healthcare Market?

The Pediatric Healthcare Market size is expected to reach USD 15.93 billion in 2025 and grow at a CAGR of 4% to reach USD 19.38 billion by 2030.

What is the current Pediatric Healthcare Market size?

In 2025, the Pediatric Healthcare Market size is expected to reach USD 15.93 billion.

Which is the fastest growing region in Pediatric Healthcare Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Pediatric Healthcare Market?

In 2025, the North America accounts for the largest market share in Pediatric Healthcare Market.

What years does this Pediatric Healthcare Market cover, and what was the market size in 2024?

In 2024, the Pediatric Healthcare Market size was estimated at USD 15.29 billion. The report covers the Pediatric Healthcare Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Pediatric Healthcare Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Pediatric Healthcare Industry Report

The pediatric healthcare market is on a trajectory of significant growth, fueled by the rising incidence of chronic and acute illnesses among children and a heightened demand for efficient treatment modalities. This growth is further bolstered by advancements in pharmaceuticals and medical devices, leading to increased demand for innovative therapies tailored for the pediatric population. With the antibiotics segment capturing a considerable market share due to the widespread prevalence of bacterial infections among children, efforts to bolster pediatric healthcare facilities globally are in full swing. North America leads this expansion, due to to its strong healthcare infrastructure, hefty R&D investments, and proactive government policies aimed at enhancing pediatric healthcare outcomes. This market's dynamism is further enriched by pediatrician companies pioneering in the field, driving innovations to cater to the health needs of children across various stages of growth. Insights from Mordor Intelligence™ highlight this market's promising outlook, underscoring the pivotal role of these companies in shaping the future of pediatric healthcare. Get a sample of this industry analysis as a free report PDF download.