| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 62.15 Billion |

| Market Size (2030) | USD 120.44 Billion |

| CAGR (2025 - 2030) | 14.15 % |

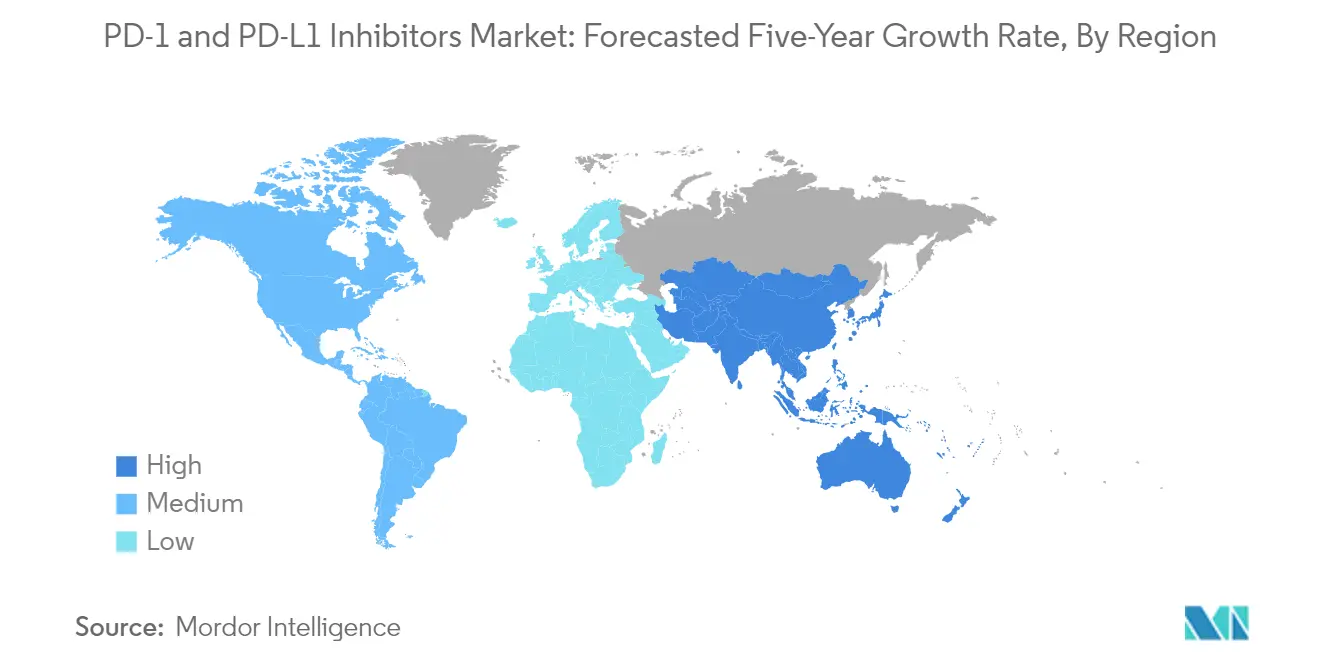

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

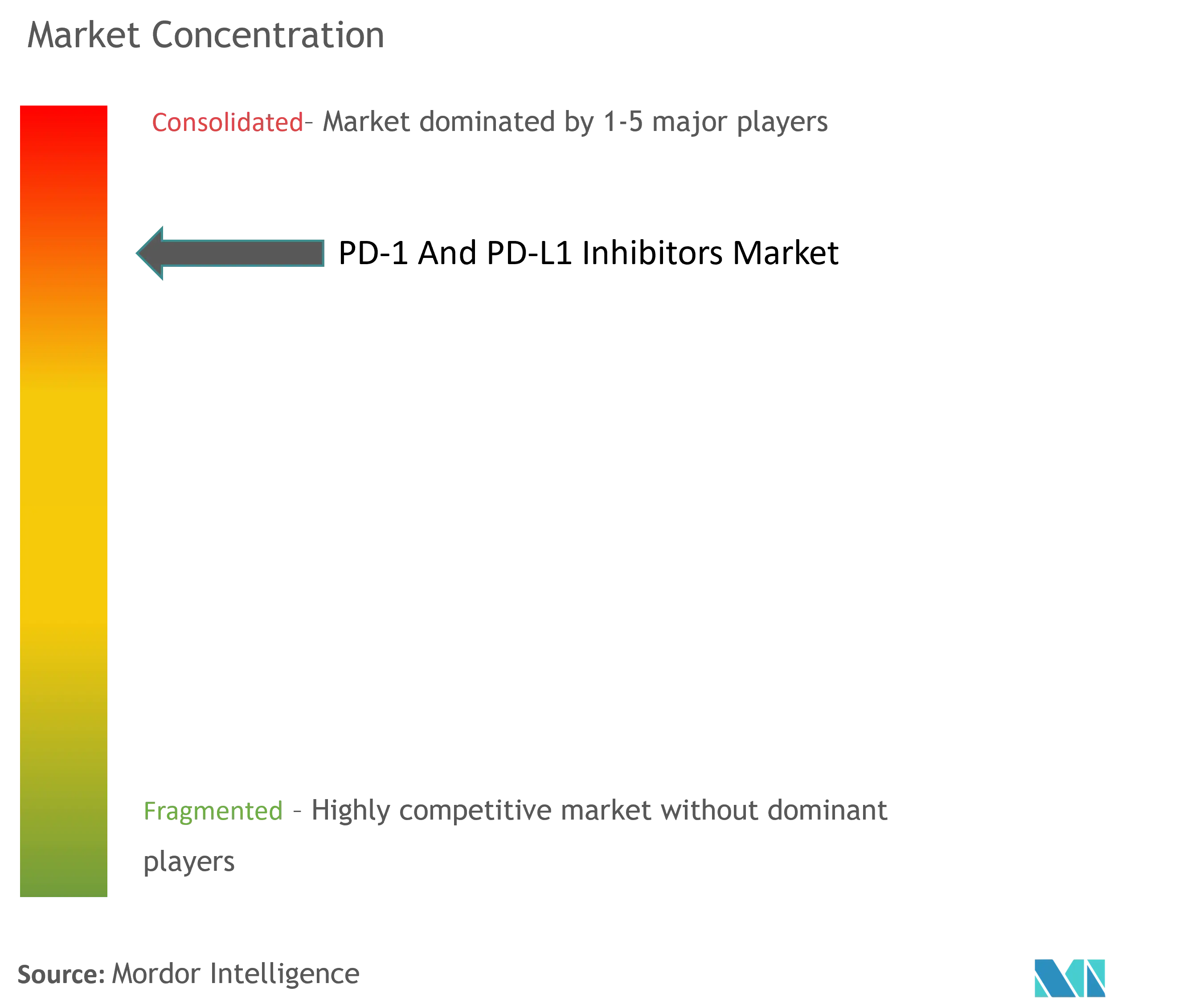

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

PD-1 And PD-L1 Inhibitors Market Analysis

The PD-1 And PD-L1 Inhibitors Market size is estimated at USD 62.15 billion in 2025, and is expected to reach USD 120.44 billion by 2030, at a CAGR of 14.15% during the forecast period (2025-2030).

The PD-1 and PD-L1 inhibitors market is experiencing significant transformation through technological advancements and innovative treatment approaches. The integration of artificial intelligence and machine learning in drug development has accelerated the discovery and optimization of new PD-1 inhibitor compounds. This evolution is evident in the expanding clinical trial landscape, with 841 clinical trials registered for PD-1 inhibitor and 606 for PD-L1 inhibitors as of June 2023. The advancement in biomarker testing and personalized medicine approaches has enabled more precise patient selection for these therapies, leading to improved treatment outcomes. Additionally, the emergence of novel combination therapies has opened new avenues for treating previously unresponsive cancer types.

Strategic collaborations and partnerships between pharmaceutical companies have become increasingly prevalent in shaping the market landscape. For instance, in April 2023, Specialised Therapeutics partnered with Akeso Inc. and CTTQ-Akeso to commercialize ANNIKO (penpulimab), an anti-PD-1 monoclonal antibody in Australia and Southeast Asia. In the same month, Enlivex Therapeutics Ltd announced a clinical partnership with BeiGene to evaluate the combination of Allocetra with tislelizumab in patients with advanced-stage solid tumors. These partnerships are crucial in expanding market reach and accelerating the development of innovative treatment solutions.

The industry has witnessed substantial progress in expanding treatment indications and improving delivery mechanisms. In February 2023, BeiGene received approval from China's NMPA for tislelizumab in combination with chemotherapy for treating gastric cancer patients with high PD-L1 expression. The focus has shifted towards developing more targeted and efficient delivery systems, including subcutaneous formulations and novel combination approaches. This evolution in treatment modalities has been accompanied by increased emphasis on reducing side effects and improving patient compliance.

The market is characterized by intensive research activities and substantial investments in clinical development. According to recent industry analysis, pharmaceutical companies are increasingly focusing on developing next-generation PD-L1 inhibitors with enhanced efficacy and safety profiles. The American Cancer Society's projection of approximately 1.9 million new cancer cases in the United States by the end of 2023 underscores the significant PD-1 market potential. This has led to accelerated development timelines and increased focus on breakthrough designations for novel therapeutic approaches, particularly in difficult-to-treat cancers and rare tumor types.

PD-1 And PD-L1 Inhibitors Market Trends

Rising Investments in R&D and Clinical Trials by Biopharmaceutical Industries

The biopharmaceutical industry has demonstrated a substantial commitment to research and development in the PD-1 and PD-L1 inhibitors space, with significant investments driving innovation and therapeutic advances. The National Institutes of Health (NIH) increased its research investment to USD 18,002 million in 2022 compared to USD 17,681 million in 2021 for research activities associated with various chronic diseases. This investment by government organizations is contributing to the rising importance of biopharmaceuticals as it has gained significant attention in disease management. According to the European Federation of Pharmaceutical Industries and Associations (EFPIA) Annual Report 2022, the research-based pharma industry in Europe invested GBP 41.5 billion in research and development activities, highlighting the global scale of R&D commitment.

The pharmaceutical industry's focus on clinical trials has intensified, with research showing that 5,683 clinical trials worldwide in 2021 explored PD-L1 inhibitors. Companies are actively pursuing strategic partnerships to accelerate research outcomes. For instance, in January 2023, NextPoint Therapeutics announced a USD 80 million Series B fundraising round to advance two of its key precision immuno-oncology programs into clinical trials. Similarly, in March 2022, Jacobi reported an R&D expenditure of RMB 421 million, representing an 83% increase over 2021, with the successful completion of phase I clinical investigation of AB-3312 and determination of recommended doses for monotherapy and combination therapy with a PD-1 inhibitor.

Understand The Key Trends Shaping This Market

Download PDF

Increased Encouragement Initiatives by the Regulatory Authorities with Favorable Approvals and Special Designations

Regulatory authorities have demonstrated strong support for PD-1 and PD-L1 inhibitors development through expedited approvals and special designations, significantly accelerating market access for innovative therapies. In 2023, several landmark approvals have reinforced this trend, including the FDA's approval of Zynyz (retifanlimab-dlwr) in March 2023 for treating adults with metastatic or recurrent locally advanced Merkel cell carcinoma. Additionally, in January 2023, the FDA approved KEYTRUDA (pembrolizumab) as adjuvant treatment following surgical resection and platinum-based chemotherapy for patients with Stage IB, II, or IIIA Non-Small Cell Lung Cancer (NSCLC), expanding treatment options for early-stage cancer patients.

The regulatory landscape continues to evolve with increasing support for combination therapies and expanded indications. For instance, in September 2022, the FDA approved durvalumab (Imfinzi) in combination with gemcitabine and cisplatin for adult patients with locally advanced or metastatic biliary tract cancer. Special designations have also played a crucial role, as evidenced by the December 2022 grant of Orphan Drug Designation to HANSIZHUANG (serplulimab) by both the European Commission and the US FDA for treating small cell lung cancer, demonstrating the global regulatory commitment to advancing innovative cancer treatments. These regulatory initiatives have created a favorable environment for continued investment and development in the PD-L1 inhibitors space.

Growing Burden of Different Cancers

The escalating global cancer burden has become a primary driver for the PD-1 non-small cell lung cancer market, with recent statistics highlighting the urgent need for effective immunotherapy solutions. According to the American Cancer Society's 2023 report, approximately 97,780 new cases of melanoma will be diagnosed in the United States in 2023, while about 81,800 adults will be diagnosed with kidney cancer. The increasing incidence of various cancer types has created a pressing demand for innovative treatment approaches, particularly in cases where traditional therapies have shown limited efficacy. The American Cancer Society also projects that approximately 80,550 persons will be diagnosed with non-Hodgkin lymphoma in 2023, including both adults and children, further emphasizing the growing cancer burden across different age groups.

The diversification of cancer types requiring treatment has led to expanded applications for PD-1 and PD-L1 inhibitors. Recent studies have demonstrated the effectiveness of these inhibitors across multiple cancer types, driving their adoption in various therapeutic contexts. For instance, according to new clinical study results published by the National Institutes of Health in August 2022, the addition of pembrolizumab (Keytruda) to chemotherapy has shown improved survival rates in patients with advanced triple-negative breast cancer compared to chemotherapy alone. This growing evidence of efficacy across different cancer types, combined with the rising cancer burden, has created a strong foundation for market expansion and continued investment in PD-1 and PD-L1 inhibitor development.

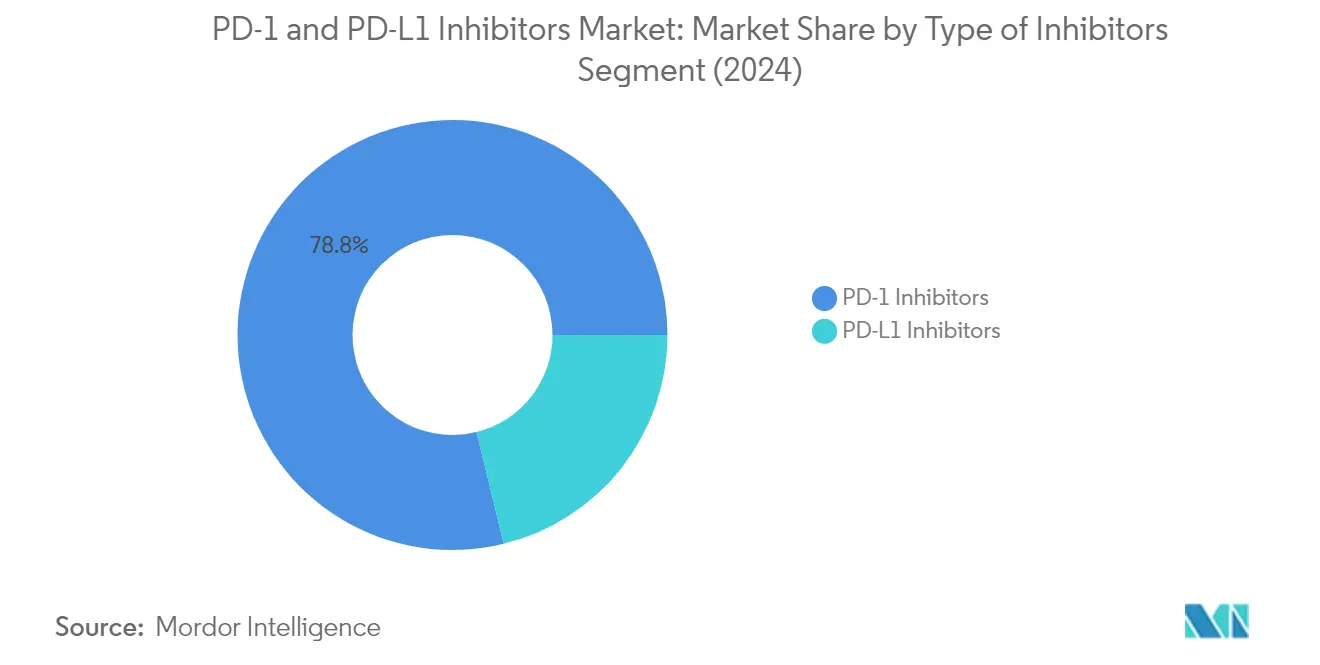

Segment Analysis: By Type of Inhibitors

PD-1 Inhibitors Segment in PD-1 and PD-L1 Inhibitors Market

The PD-1 inhibitor segment dominates the global PD-1 and PD-L1 inhibitors market, holding approximately 79% of the market share in 2024. This significant market position is attributed to the segment's proven efficacy in treating several types of cancer and its revolutionary impact on the treatment landscape. PD-1 inhibitors have demonstrated remarkable clinical benefits in multiple cancer types, particularly for patients with advanced or metastatic disease. The segment's growth is further supported by the presence of key market players and their continuous focus on research and development. These inhibitors have shown significant clinical benefits in several types of cancer and have revolutionized the treatment landscape, particularly for patients with advanced or metastatic disease. The segment is also projected to maintain its leading position with the highest growth rate of around 18% during 2024-2029, driven by increasing regulatory approvals, expanding therapeutic applications, and growing adoption in combination therapies.

PD-L1 Inhibitors Segment in PD-1 and PD-L1 Inhibitors Market

The PD-L1 inhibitors segment represents a crucial component of the market, offering a distinct mechanism of action by targeting the PD-L1 protein expressed on cancer cells and other cells in the tumor microenvironment. These inhibitors have shown promising results in various cancer types, including non-small cell lung cancer, urothelial carcinoma, triple-negative breast cancer, and head and neck squamous cell carcinoma. The segment's growth is supported by ongoing clinical trials exploring new indications and combination therapies. Key pharmaceutical companies are actively investing in research and development to enhance the efficacy of PD-L1 inhibitors and expand their applications. The segment's development is further bolstered by increasing regulatory approvals and growing adoption in various cancer treatment protocols, particularly in combination with other therapeutic approaches.

Segment Analysis: By Application

Non-small Cell Lung Cancer Segment in PD-1 and PD-L1 Inhibitors Market

The Non-small Cell Lung Cancer (NSCLC) segment dominates the PD-1 and PD-L1 inhibitors market, commanding approximately 43% of the total market share in 2024. This segment's leadership position is strengthened by several key factors, including the high efficacy of PD-1 and PD-L1 inhibitors in treating NSCLC and significant regulatory approvals. Major pharmaceutical companies have received multiple approvals for their PD-1/PD-L1 inhibitors in NSCLC treatment, such as Merck's KEYTRUDA (pembrolizumab) receiving FDA approval in January 2023 for adjuvant treatment following surgical resection and platinum-based chemotherapy for Stage IB, II, or IIIA NSCLC. The segment is also experiencing the fastest growth rate in the market, projected to expand at approximately 20% from 2024 to 2029, driven by increasing adoption of immunotherapy combinations, growing NSCLC prevalence, and continuous research and development activities focusing on expanding treatment indications.

Remaining Segments in PD-1 and PD-L1 Inhibitors Market by Application

The market's remaining segments include Melanoma, Kidney Cancer, and Hodgkin's Lymphoma, each playing crucial roles in the overall market dynamics. The Melanoma segment has established itself as a significant application area for PD-1 and PD-L1 inhibitors, with multiple approved therapies showing strong clinical outcomes. The Kidney Cancer segment continues to expand with new therapeutic combinations and treatment approaches being developed. Hodgkin's Lymphoma, while representing a smaller market share, demonstrates promising growth potential due to the high response rates of PD-1 inhibitors in treating this condition. These segments collectively contribute to the market's diversity and provide multiple growth avenues for pharmaceutical companies developing PD-1 and PD-L1 inhibitors.

Segment Analysis: By Distribution Channel

Hospital Pharmacies Segment in PD-1 and PD-L1 Inhibitors Market

Hospital pharmacies continue to dominate the PD-1 and PD-L1 inhibitors market, holding approximately 58% market share in 2024. This significant market position is primarily attributed to the high reliability of these pharmacies and the easy availability of medications within hospital settings. Hospital pharmacies play a crucial role in procuring PD-1 inhibitors from approved suppliers and manufacturers while ensuring adequate and continuous supply to meet patient needs. They are particularly valuable for inpatient management, providing quick and easy access to prescribed PD-1 inhibitors. These pharmacies work closely with healthcare providers to calculate and determine appropriate dosing based on patient characteristics such as weight, renal function, and other factors. Additionally, hospital pharmacies ensure compliance with regulatory and legal requirements related to handling, dispensing, and documentation of PD-1/PD-L1 inhibitors, maintaining accurate records of drug utilization and adverse event reporting as per regulatory guidelines.

Online Pharmacies Segment in PD-1 and PD-L1 Inhibitors Market

The online pharmacies segment is emerging as the fastest-growing distribution channel, projected to grow at approximately 21% during 2024-2029. This rapid growth is driven by the increasing adoption of digital healthcare solutions and the convenience of doorstep delivery services. Online pharmacies are becoming increasingly important in providing access to PD-1 and PD-L1 inhibitors, particularly benefiting individuals with limited mobility or those living in remote areas with restricted access to local pharmacies. These platforms are developing sophisticated systems to ensure proper handling and delivery of these critical medications while maintaining their integrity. The segment's growth is further supported by the emergence of various online portals that facilitate home delivery of cancer drugs across different regions, with proper safety and security protocols in place. Many online pharmacies are also implementing advanced patient education and support systems, providing detailed information about medication usage, potential side effects, and compliance requirements.

Remaining Segments in Distribution Channel

Retail pharmacies represent another significant distribution channel in the PD-1 and PD-L1 inhibitors market, serving as crucial community-based access points for cancer patients. These pharmacies contribute to the overall care and well-being of cancer patients by providing convenient locations for medication pickup and offering valuable patient support services. Retail pharmacies play a vital role in promoting medication adherence through reminders, refill services, and various adherence aids. They also assist patients in navigating insurance coverage and exploring financial assistance options for PD-1 or PD-L1 inhibitors. Many retail pharmacies have established collaborations with hospitals and cancer centers, enhancing their ability to serve cancer patients effectively while providing cost-related benefits and guidance on copayment assistance programs.

PD-1 And PD-L1 Inhibitors Market Geography Segment Analysis

PD-1 and PD-L1 Inhibitors Market in North America

North America represents the most significant PD-1 and PD-L1 inhibitors market globally, driven by a well-established healthcare infrastructure, substantial research and development investments, and high adoption rates of innovative cancer therapies. The United States, Canada, and Mexico comprise this region, with each country contributing uniquely to the market's growth. The presence of major pharmaceutical companies, extensive clinical trials, and favorable regulatory environments have positioned North America as a leader in the PD-1 and PD-L1 inhibitors market development and commercialization. The region benefits from advanced healthcare systems, comprehensive insurance coverage, and increasing awareness about immunotherapy treatments among healthcare providers and patients.

PD-1 and PD-L1 Inhibitors Market in the United States

The United States dominates the North American PD-1 and PD-L1 market, holding approximately 62% market share in 2024. The country's leadership position is supported by a robust research infrastructure, significant healthcare spending, and the presence of key market players. The US market benefits from favorable reimbursement policies and early access to innovative therapies. The country's strong focus on clinical research, with numerous ongoing trials for PD-1 and PD-L1 inhibitors, continues to drive market expansion. The presence of major cancer research institutions, comprehensive cancer centers, and increasing collaboration between academic institutions and pharmaceutical companies further strengthens the United States' position in the market.

PD-1 and PD-L1 Inhibitors Market in Canada

Canada emerges as the fastest-growing market in North America, with an expected growth rate of approximately 20% during 2024-2029. The country's market growth is driven by increasing cancer prevalence and a robust healthcare infrastructure. Canada's universal healthcare system facilitates better access to innovative cancer treatments, including PD-1 and PD-L1 inhibitors. The country's commitment to healthcare innovation, supported by government initiatives and research grants, continues to attract pharmaceutical investments. Canadian research institutions actively participate in global clinical trials, contributing to the development of novel cancer immunotherapies.

PD-1 and PD-L1 Inhibitors Market in Europe

Europe represents a significant market for PD-1 and PD-L1 inhibitors, characterized by advanced healthcare systems, strong research capabilities, and increasing adoption of immunotherapy treatments. The region encompasses key markets including Germany, the United Kingdom, France, Italy, and Spain, each contributing significantly to market growth. European countries benefit from well-established healthcare infrastructure, strong regulatory frameworks, and an increasing focus on personalized medicine approaches. The region's collaborative research environment and the presence of leading pharmaceutical companies drive continuous innovation in cancer immunotherapy.

PD-1 and PD-L1 Inhibitors Market in Germany

Germany leads the European market with approximately 22% market share in 2024. The country's dominant position is supported by its robust healthcare system, significant research and development investments, and a strong presence of pharmaceutical companies. Germany's leadership in clinical research and early adoption of innovative therapies contributes to its market prominence. The country's comprehensive healthcare coverage and focus on precision medicine approaches in cancer treatment further strengthen its position in the PD-1 and PD-L1 inhibitors market.

PD-1 and PD-L1 Inhibitors Market in France

France demonstrates the highest growth potential in Europe, with an anticipated growth rate of approximately 19% during 2024-2029. The country's market expansion is driven by increasing cancer research initiatives and strong government support for innovative therapies. France's commitment to healthcare excellence and investment in clinical research facilities contributes to its rapid market growth. The country's focus on developing personalized cancer treatments and strong collaboration between academic institutions and industry players positions it for continued expansion in the PD-1 and PD-L1 market.

PD-1 and PD-L1 Inhibitors Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market for PD-1 and PD-L1 inhibitors, characterized by increasing healthcare expenditure, a growing cancer burden, and improving access to innovative therapies. The region encompasses diverse markets including China, Japan, India, Australia, and South Korea, each at different stages of market development. The APAC region benefits from large patient populations, expanding healthcare infrastructure, and increasing investment in biotechnology research. Growing awareness about immunotherapy treatments and improving regulatory frameworks contribute to the region's market expansion.

PD-1 and PD-L1 Inhibitors Market in China

China emerges as the dominant force in the Asia-Pacific region's PD-1 and PD-L1 inhibitors market. The country's leadership is driven by its large patient population, increasing healthcare spending, and strong government support for biotechnology development. China's robust clinical research environment and growing domestic pharmaceutical industry contribute to its market dominance. The country's focus on developing innovative cancer treatments and improving healthcare access continues to strengthen its position in the market.

PD-1 and PD-L1 Inhibitors Market in China's Growth

China also demonstrates the highest growth potential in the Asia-Pacific region. The country's rapid market expansion is supported by increasing research and development investments, growing clinical trial activities, and improving regulatory frameworks. China's commitment to healthcare innovation and strong focus on developing domestic pharmaceutical capabilities drive its market growth. The country's expanding healthcare infrastructure and increasing adoption of innovative cancer treatments position it for continued strong growth in the PD-1 and PD-L1 inhibitors market.

PD-1 and PD-L1 Inhibitors Market in the Middle East and Africa

The Middle East and Africa region presents an emerging market for PD-1 and PD-L1 inhibitors, with varying levels of healthcare infrastructure and market maturity across different countries. The region includes key markets such as GCC countries and South Africa, with GCC emerging as both the largest and fastest-growing market in the region. The healthcare sector in this region is experiencing significant transformation, driven by increasing government investments in healthcare infrastructure and growing awareness about advanced cancer treatments. The region's focus on developing healthcare tourism and improving access to innovative therapies contributes to market growth.

PD-1 and PD-L1 Inhibitors Market in South America

South America represents an evolving market for PD-1 and PD-L1 inhibitors, characterized by improving healthcare infrastructure and an increasing focus on cancer treatment. The region includes key markets such as Brazil and Argentina, with Brazil emerging as both the largest and fastest-growing market in the region. The South American market is driven by increasing healthcare expenditure, growing cancer awareness, and improving access to innovative therapies. The region's developing healthcare infrastructure and increasing participation in clinical trials contribute to market expansion. Collaborative efforts between government agencies and pharmaceutical companies are helping to improve access to advanced cancer treatments across the region.

Get Analysis on Important Geographic Markets

Download PDF

PD-1 And PD-L1 Inhibitors Industry Overview

Top Companies in PD-1 and PD-L1 Inhibitors Market

The PD-1 and PD-L1 inhibitors market is characterized by intense innovation and strategic developments from major pharmaceutical companies, including Bristol-Myers Squibb, Merck & Co., F. Hoffmann-La Roche, GlaxoSmithKline, AstraZeneca, and others. These companies are heavily investing in research and development to expand their product portfolios and secure new therapeutic indications for their existing drugs. The market demonstrates a strong focus on clinical trials exploring combination therapies, particularly in combining PD-1 and PD-L1 inhibitors with other cancer treatments such as chemotherapy, targeted therapy, and radiation therapy. Companies are actively pursuing geographical expansion through strategic partnerships and collaborations, particularly in emerging markets. Manufacturing capabilities and distribution networks are being strengthened through substantial investments, while regulatory approvals across multiple jurisdictions remain a key priority for market players.

Consolidated Market with High Entry Barriers

The PD-1 and PD-L1 inhibitors market exhibits a highly consolidated structure dominated by large multinational pharmaceutical companies with established oncology portfolios. These market leaders possess significant advantages in terms of research capabilities, manufacturing infrastructure, and global distribution networks. The market demonstrates substantial entry barriers due to high development costs, complex regulatory requirements, and the need for extensive clinical trial data. Mergers and acquisitions activity in the sector is primarily focused on expanding therapeutic capabilities and gaining access to novel technologies or complementary product portfolios.

The competitive dynamics are shaped by the presence of strong intellectual property protection and the significant investments required for drug development and commercialization. Regional players are increasingly forming strategic partnerships with global pharmaceutical companies to enhance their market presence and access advanced technologies. The market structure favors companies with strong financial resources and established relationships with healthcare providers and research institutions. Companies are actively pursuing licensing agreements and collaborative research initiatives to share development risks and accelerate market entry for new products.

Innovation and Partnerships Drive Market Success

Success in the PD-1 and PD-L1 inhibitors market increasingly depends on developing innovative combination therapies and expanding into new indications. Companies must focus on building robust clinical evidence through comprehensive trial programs while maintaining strong relationships with healthcare providers and regulatory authorities. The ability to demonstrate superior efficacy and safety profiles compared to existing treatments remains crucial for market success. Strategic partnerships with diagnostic companies for biomarker development and patient selection are becoming increasingly important for product differentiation and market penetration.

Market players must navigate complex reimbursement landscapes and demonstrate strong health economic outcomes to secure market access. The development of companion diagnostics and personalized medicine approaches is becoming increasingly critical for success. Companies need to maintain robust supply chains and ensure manufacturing quality while managing pricing pressures from healthcare systems and competing products. Regulatory compliance and pharmacovigilance capabilities are essential for maintaining market position, while investment in real-world evidence generation helps support product value propositions. The ability to adapt to evolving treatment paradigms and integrate new technologies will be crucial for long-term success in this dynamic PD market.

PD-1 And PD-L1 Inhibitors Market Leaders

-

Bristol-Myers Squibb Company

-

Merck & Co.

-

F. Hoffmann-La Roche AG

-

Pfizer Inc.

-

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

PD-1 And PD-L1 Inhibitors Market News

- January 2024: Halozyme Therapeutics, Inc. has announced that Roche has received marketing authorization from the European Commission (EC) for Tecentriq SC (atezolizumab) co-formulated with ENHANZE, Halozyme's proprietary recombinant human hyaluronidase enzyme, rHuPH20. This approval is applicable to all approved indications of Tecentriq IV. It marks the first time that the European Union (EU) has authorized a PD-(L)1 cancer immunotherapy for subcutaneous injection.

- January 2024: Bristol Myers Squibb reported a result from the Phase 3 CheckMate-8HW trial. Opdivo (PD-1 inhibitor) and Yervoy, a dual immunotherapy combination, showed significant improvement in progression-free survival (PFS) as a first-line treatment for patients with microsatellite instability-high (MSI-H) or mismatch repair deficient (dMMR) metastatic colorectal cancer (mCRC).

PD-1 And PD-L1 Inhibitors Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Rising Investments in R&D and Clinical Trials by Bio-pharmaceutical Industries

- 4.2.2 Increased Encouragement Initiatives by the Regulatory Authorities with Favorable Approvals and Special Designations

- 4.2.3 Growing Burden of Different Cancers

-

4.3 Market Restraints

- 4.3.1 Risk of Complications Associated with the Highly Expensive Oncology Treatment

- 4.3.2 Challenges in Development with Uncertainty in Regulatory Process and High Costs of Tedious Clinical Trials

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

-

5.1 By Type of Inhibitors

- 5.1.1 PD-1 Inhibitors

- 5.1.2 PD-L1 Inhibitors

-

5.2 By Application

- 5.2.1 Hodgkins Lymphoma

- 5.2.2 Kidney Cancer

- 5.2.3 Melanoma

- 5.2.4 Non-small Cell Lung Cancer

- 5.2.5 Other Applications

-

5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United states

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Bristol-Myers Squibb Company

- 6.1.2 Merck & Co.

- 6.1.3 F. Hoffmann-La Roche AG

- 6.1.4 GSK plc

- 6.1.5 Amgen Inc.

- 6.1.6 Eli Lilly and Company

- 6.1.7 AstraZeneca PLC

- 6.1.8 BeiGene LTD

- 6.1.9 Pfizer Inc.

- 6.1.10 Regeneron Pharmaceuticals Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

PD-1 And PD-L1 Inhibitors Industry Segmentation

As per the scope of the report, programmed cell death protein 1 (PD-1) inhibitors and programmed cell death ligand 1 (PD-L1) inhibitors are a group of new checkpoint inhibitor anticancer drugs that block the activity of PD-1 and PDL1 immune checkpoint proteins present on the surface of cells. These immune checkpoint inhibitors are also active in pregnancy following tissue allografts and are emerging as a front-line treatment in immunotherapy for several types of cancer. An indication of specific staining interpretation defines tumor PD-L1 status.

The PD-1 and PD-L1 inhibitors market is segmented by type of inhibitors, application, distribution channel, and geography. By type of inhibitors, the market is segmented as PD-1 inhibitors and PD-L1 inhibitors. By application, the market is segmented as Hodgkin lymphoma, kidney cancer, melanoma, non-small cell lung cancer, and other applications. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East, Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.

| By Type of Inhibitors | PD-1 Inhibitors | ||

| PD-L1 Inhibitors | |||

| By Application | Hodgkins Lymphoma | ||

| Kidney Cancer | |||

| Melanoma | |||

| Non-small Cell Lung Cancer | |||

| Other Applications | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online Pharmacies | |||

| Geography | North America | United states | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

PD-1 And PD-L1 Inhibitors Market Research Faqs

How big is the PD-1 And PD-L1 Inhibitors Market?

The PD-1 And PD-L1 Inhibitors Market size is expected to reach USD 62.15 billion in 2025 and grow at a CAGR of 14.15% to reach USD 120.44 billion by 2030.

What is the current PD-1 And PD-L1 Inhibitors Market size?

In 2025, the PD-1 And PD-L1 Inhibitors Market size is expected to reach USD 62.15 billion.

Which is the fastest growing region in PD-1 And PD-L1 Inhibitors Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in PD-1 And PD-L1 Inhibitors Market?

In 2025, the North America accounts for the largest market share in PD-1 And PD-L1 Inhibitors Market.

What years does this PD-1 And PD-L1 Inhibitors Market cover, and what was the market size in 2024?

In 2024, the PD-1 And PD-L1 Inhibitors Market size was estimated at USD 53.36 billion. The report covers the PD-1 And PD-L1 Inhibitors Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the PD-1 And PD-L1 Inhibitors Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

PD-1 And PD-L1 Inhibitors Industry Report

Mordor Intelligence brings extensive expertise to analyzing the PD-1 and PD-L1 inhibitors market. We deliver comprehensive insights into this crucial immunotherapy sector. Our detailed research covers the entire spectrum of PD-1 and PD-L1 monoclonal antibodies. This includes breakthrough developments in PD-1 non-small cell lung cancer treatment approaches. The analysis encompasses both PD-1 inhibitor and PDL1 inhibitors technologies. It provides stakeholders with a crucial understanding of the differences between PD1 vs PDL1 therapeutic approaches.

This extensive report, available as an easy-to-download PDF, offers valuable insights into tumor immunity PD-1 inhibitors and their clinical applications. Stakeholders gain access to a detailed analysis of PD-1 and PD-L1 drug developments. This includes emerging therapeutic applications and regulatory landscapes. The report specifically examines PD-1 and PD-L1 antibody developments across major markets. It provides crucial data for pharmaceutical companies, healthcare providers, and investors seeking to understand this rapidly evolving therapeutic space.