Market Size of Pathology Devices Industry

| Study Period | 2019 - 2029 |

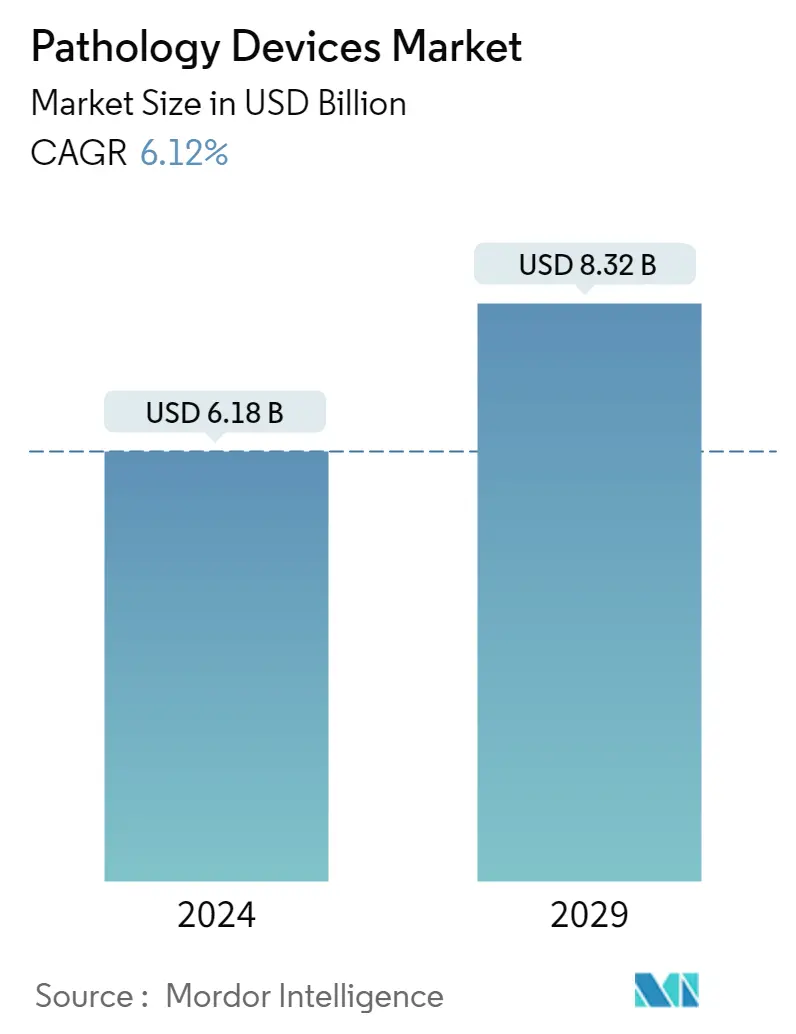

| Market Size (2024) | USD 6.18 Billion |

| Market Size (2029) | USD 8.32 Billion |

| CAGR (2024 - 2029) | 6.12 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Pathology Devices Market Analysis

The Pathology Devices Market size is estimated at USD 6.18 billion in 2024, and is expected to reach USD 8.32 billion by 2029, growing at a CAGR of 6.12% during the forecast period (2024-2029).

- The COVID-19 pandemic had a huge impact on healthcare systems around the world and caused many healthcare facilities to stop providing routine care and pathological testing, putting patients with chronic conditions, including cancer and cardiovascular disorders, at severe risk. For instance, according to an article published in International Medical Journal in January 2022, it was observed that the ratio of the number of pathology tests pre-lockdown and post-lockdown versus baseline period decreased from 1.02 to 0.53, respectively.

- However, the increased coronavirus cases among the population have increased the demand for pathological tests. For instance, as per an article published in Frontiers in Pathology in March 2022, it was found that the number of molecular microbiology tests was more than three times higher during the lockdown period. This has increased the company's focus on developing innovative pathological test kits and devices. Thus, the studied market is expected to grow and regain its full potential in the coming years.

- The increasing prevalence and burden of Alzheimer's disease, autoimmune diseases, cancer, and others around the world are driving the need for effective and advanced diagnostic tests, hence propelling the market growth. For instance, according to the 2022 statistics published by Alzheimer's Association, an estimated 6.5 million Americans age 65 and older were living with Alzheimer's dementia in 2022, and this number is projected to reach 13 million by 2050. Thus, the expected increase in the number of people suffering from Alzheimer's disease is anticipated to fuel the demand for pathology devices that helps physicians in early identifying the disease-causing dementia symptoms, thereby propelling the market growth.

- Additionally, as per the 2023 statistics published by ACS, about 24,810 malignant tumors of the brain or spinal cord (14,280 in males and 10,530 in females) are expected to be diagnosed in the United States in 2023. Thus, the high burden of brain or spinal cord tumors is anticipated to fuel the demand for radionuclide bone scintigraphy (bone scan) for detecting spinal pathologies, hence bolstering the market growth. Moreover, the rising company focus on developing technologically advanced pathological kits and devices is also contributing to the market growth. For instance, in April 2022, Sysmex Europe launched a new three-part differential system, XQ-320 XQ-Series Automated Hematology Analyzer, a robust device that brings excellence in quality to a diverse range of clinical laboratory environments with reliable technology and a new level of usability.

- Therefore, owing to the factors such as the high burden of chronic and infectious diseases and new product launches, the studied market is expected to grow over the forecast period. However, the high cost of devices and stringent regulations, as well as the lack of skilled professionals, are likely to impede the growth of pathological devices over the forecast period.

Pathology Devices Industry Segmentation

As per the scope of the report, pathology is a branch of medical science that involves the study and diagnosis of disease through the examination of surgically removed organs, tissues (biopsy samples), bodily fluids, and in some cases, the whole body (autopsy).

The pathology devices market is segmented by technology (clinical chemistry, immunoassays technology, microbiology, molecular diagnostics, and other technologies), application (drug discovery and development, disease diagnostics, forensic diagnostics, and other applications), end-user (pharmaceutical companies, diagnostic laboratories, academic institutes, and other end-users) and geography (North America, Europe, Asia-Pacific, Middle East and Africa and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD million) for the above segments.

| By Technology | |

| Clinical Chemistry | |

| Immunoassays Technology | |

| Microbiology | |

| Molecular Diagnostics | |

| Other Technologies |

| By Application | |

| Drug Discovery and Development | |

| Disease Diagnostics | |

| Forensic Diagnostics | |

| Other Applications |

| By End-User | |

| Pharmaceutical Companies | |

| Hospitals and Diagnostic Laboratories | |

| Other End-Users |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Pathology Devices Market Size Summary

The pathology devices market is poised for significant growth, driven by the increasing prevalence of chronic and infectious diseases, such as cancer and cardiovascular disorders. The demand for advanced diagnostic tests is on the rise, fueled by the need for early detection and effective management of these conditions. The market is also experiencing a surge in innovation, with companies focusing on developing technologically advanced pathological test kits and devices. This trend is expected to continue, as the healthcare sector recovers from the disruptions caused by the COVID-19 pandemic, which had initially led to a decline in routine pathological testing. The market's expansion is further supported by the growing burden of diseases like Alzheimer's and brain tumors, which necessitate the use of pathology devices for accurate diagnosis and timely intervention.

North America is anticipated to hold a substantial share of the pathology devices market, attributed to its robust healthcare infrastructure and technological advancements in diagnostic devices. The region's increasing incidence of chronic and infectious diseases is driving the demand for early detection and diagnosis, thereby boosting market growth. The proliferation of new product launches in North America is enhancing the availability of advanced diagnostic tools, further propelling the market. The competitive landscape is characterized by the presence of numerous global and local players, who are actively engaging in strategic initiatives such as product launches and collaborations to maintain their market position. As a result, the pathology devices market is expected to witness steady growth over the forecast period, supported by ongoing innovations and increasing demand for precise diagnostic solutions.

Pathology Devices Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Increasing Prevalence of Chronic and Infectious Diseases

-

1.2.2 Technological Advancements in Pathology Devices

-

1.2.3 Increasing Investment in Healthcare Infrastructure in Developing Countries

-

-

1.3 Market Restraints

-

1.3.1 High Cost of Devices

-

1.3.2 Stringent Regulations and Lack of Skilled Professionals

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD million)

-

2.1 By Technology

-

2.1.1 Clinical Chemistry

-

2.1.2 Immunoassays Technology

-

2.1.3 Microbiology

-

2.1.4 Molecular Diagnostics

-

2.1.5 Other Technologies

-

-

2.2 By Application

-

2.2.1 Drug Discovery and Development

-

2.2.2 Disease Diagnostics

-

2.2.3 Forensic Diagnostics

-

2.2.4 Other Applications

-

-

2.3 By End-User

-

2.3.1 Pharmaceutical Companies

-

2.3.2 Hospitals and Diagnostic Laboratories

-

2.3.3 Other End-Users

-

-

2.4 Geography

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

2.4.1.3 Mexico

-

-

2.4.2 Europe

-

2.4.2.1 Germany

-

2.4.2.2 United Kingdom

-

2.4.2.3 France

-

2.4.2.4 Italy

-

2.4.2.5 Spain

-

2.4.2.6 Rest of Europe

-

-

2.4.3 Asia-Pacific

-

2.4.3.1 China

-

2.4.3.2 Japan

-

2.4.3.3 India

-

2.4.3.4 Australia

-

2.4.3.5 South Korea

-

2.4.3.6 Rest of Asia-Pacific

-

-

2.4.4 Middle East and Africa

-

2.4.4.1 GCC

-

2.4.4.2 South Africa

-

2.4.4.3 Rest of Middle East and Africa

-

-

2.4.5 South America

-

2.4.5.1 Brazil

-

2.4.5.2 Argentina

-

2.4.5.3 Rest of South America

-

-

-

Pathology Devices Market Size FAQs

How big is the Pathology Devices Market?

The Pathology Devices Market size is expected to reach USD 6.18 billion in 2024 and grow at a CAGR of 6.12% to reach USD 8.32 billion by 2029.

What is the current Pathology Devices Market size?

In 2024, the Pathology Devices Market size is expected to reach USD 6.18 billion.