Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

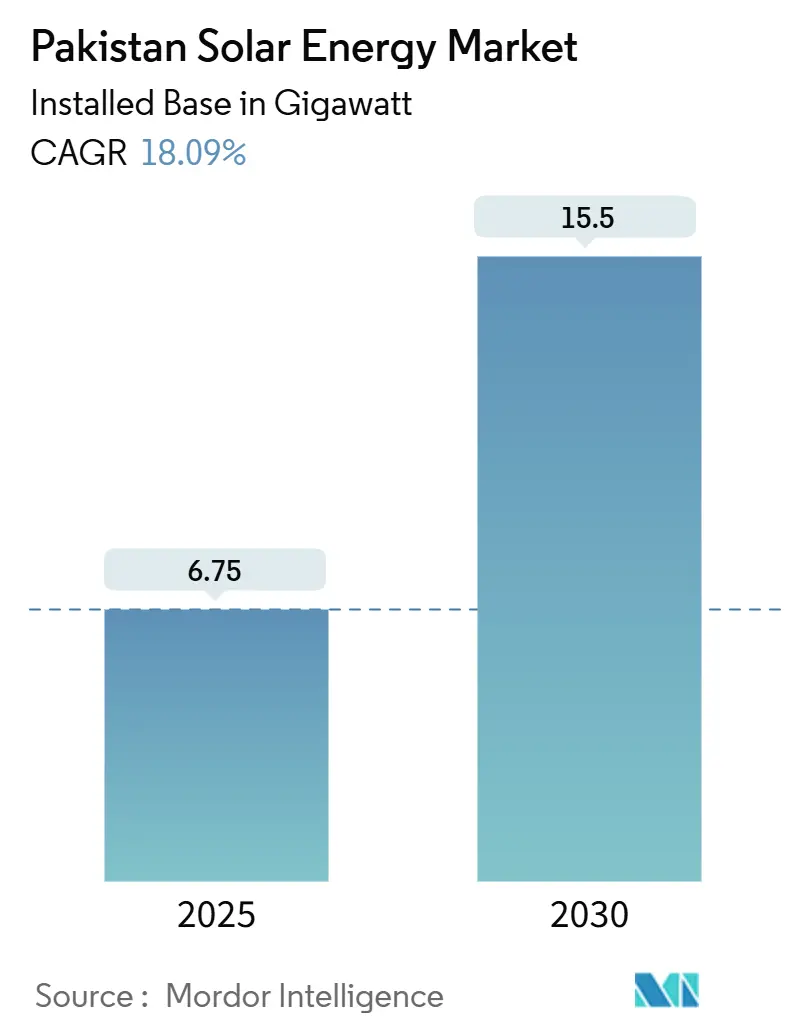

| Market Volume (2025) | 6.75 gigawatt |

| Market Volume (2030) | 15.5 gigawatt |

| Growth Rate (2025 - 2030) | 18.09% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pakistan Solar Energy Market Analysis by Mordor Intelligence

The Pakistan Solar Energy Market size in terms of installed base is expected to grow from 6.75 gigawatt in 2025 to 15.5 gigawatt by 2030, at a CAGR of 18.09% during the forecast period (2025-2030).

Plunging module prices, a cumulative 155% run-up in retail electricity tariffs since 2021, and widening access to concessional vendor financing have compressed commercial payback periods below three years, catalyzing adoption among textile mills and food processors.(1)NEPRA, “Electricity Tariff Notifications 2021-2024,” nepra.org.pkPakistan imported 16.9 GW of photovoltaic (PV) modules in 2024, a 127% year-on-year surge that vaulted the country to the world’s third-largest destination for Chinese solar exports, trailing only the United States and Brazil. Provincial free-solar-kit schemes targeting 500,000 households and corporate power-purchase agreements (PPAs) are reshaping demand patterns faster than distribution utilities can stabilize reverse power flows. Rising dependence on daytime self-generation has shaved 8-10% off grid demand in solar-dense urban feeders, forcing distribution companies (DISCOs) to socialize PKR 200 billion in stranded grid costs among non-solar consumers.

Key Report Takeaways

- By technology, solar photovoltaic captured 100% of Pakistan's solar energy market share in 2024 and is forecast to advance at an 18.1% CAGR through 2030.

- By grid type, on-grid systems held 92.5% of the Pakistan solar energy market size in 2024, whereas off-grid systems are expected to post a 25.9% CAGR to 2030.

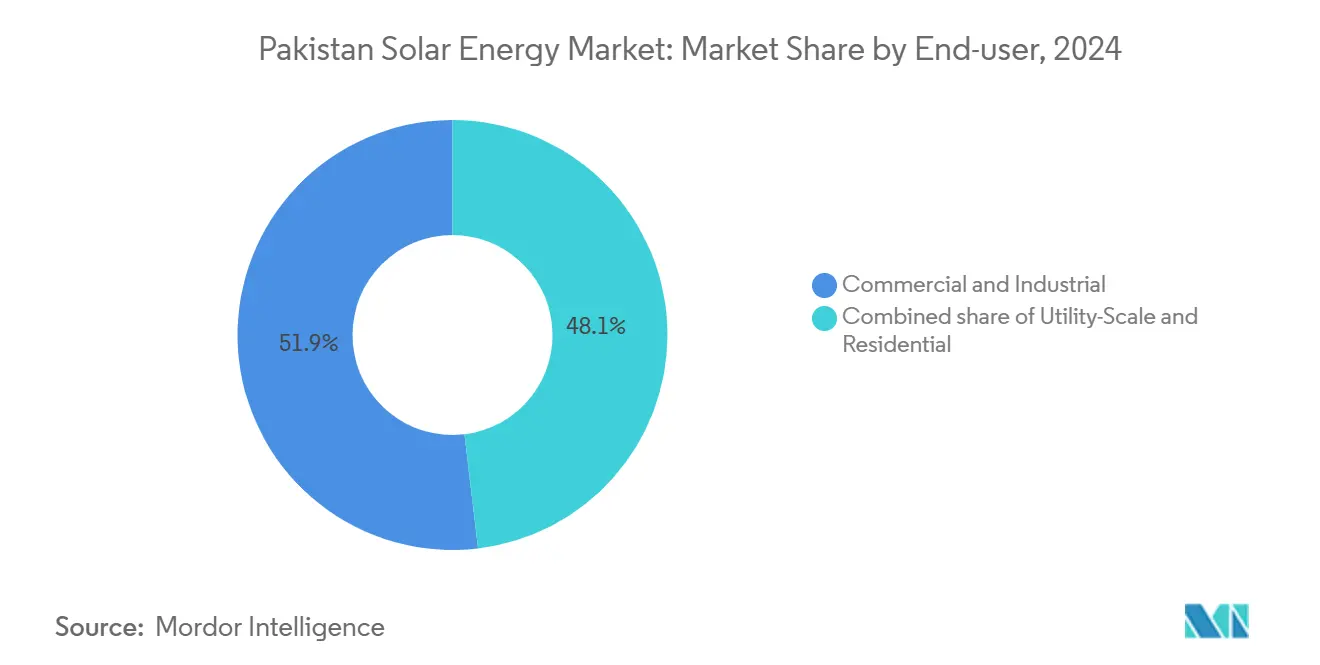

- By end user, the commercial and industrial segment commanded 51.9% of the Pakistan solar energy market share in 2024, while the residential segment is projected to expand at a 23.5% CAGR through 2030.

Pakistan Solar Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plummeting module and balance-of-system prices | +4.50% | Punjab and Sindh industrial corridors | Short term (≤ 2 years) |

| Surge in residential rooftop net-metering connections | +3.80% | Urban Punjab, Sindh, Islamabad Capital Territory | Medium term (2-4 years) |

| Corporate PPAs by export-oriented industries | +2.20% | Faisalabad, Lahore, Karachi | Medium term (2-4 years) |

| Chinese vendor financing for CPEC-aligned solar parks | +1.80% | Bahawalpur, planned Balochistan sites | Long term (≥ 4 years) |

| Falling lithium-ion prices enabling solar-plus-BESS | +1.50% | Nationwide early C&I adopters | Long term (≥ 4 years) |

| Provincial free-solar-kit schemes for low-income homes | +3.20% | Punjab, Sindh, Khyber Pakhtunkhwa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plummeting Module and Balance-of-System Prices

Module prices collapsed 60% in 2024 after Chinese manufacturers dumped surplus inventory into South Asia, dragging utility-scale levelized costs below PKR 9.8 per unit, far under the PKR 29-48 retail range in Islamabad.(2)K-Electric, “Generation Cost Comparison FY 2024,” kelectric.com.pkBulk procurement enabled EPCs to quote turnkey commercial systems at PKR 100,000–300,000 per kilowatt, down from PKR 180,000–400,000 nine months earlier, shortening payback periods for textile mills to under three years. However, slower declines in steel-intensive racking and cable pricing have squeezed local integrator margins and strengthened vertically integrated Chinese firms that fold vendor financing into supply contracts. Oversupply exceeding 200 GW worldwide is expected to keep module prices soft through 2026, yet any anti-dumping duties or further PKR depreciation would offset part of the advantage for Pakistani buyers.

Surge in Residential Rooftop Net-Metering Connections

Residential net-metering accounts rose to 283,000 by December 2024, a meteoric rise from negligible levels in 2020, as households aimed to hedge against the 155% tariff escalation since 2021. The Punjab Chief Minister’s zero-interest solar program, launched in December 2024, drew 861,000 applications within three months for 100,000 subsidized systems, revealing pent-up demand. An Economic Coordination Committee proposal to slash the buy-back rate from PKR 27 to PKR 10 per unit has triggered industry protests and legal challenges, injecting policy uncertainty that already dampens new rooftop bookings. DISCOs report an 8-10% midday demand erosion in dense feeders, spurring costly grid reinforcements to handle voltage swings and reverse power flow.

Corporate PPAs by Export-Oriented Industries

Textile exporters, which consume nearly one-third of Pakistan’s industrial electricity, now execute 10-15-year solar PPAs to lock in tariffs below PKR 15 per unit while meeting European sustainability mandates. Yellow Door Energy disclosed a 50 MW corporate portfolio in 2024 with Engro and ICI Pakistan, reflecting a growing appetite for behind-the-meter generation insulated from net-metering revisions. Nishat Mills, Interloop, and Artistic Milliners have each installed multi-megawatt systems to cut outage-driven downtime that idled production for up to eight hours daily during 2024’s peak-demand months.

Provincial Free-Solar-Kit Schemes for Low-Income Homes

Punjab earmarked PKR 12.6 billion to distribute 100,000 rooftop kits to households using fewer than 200 monthly units, targeting completion of 94,483 systems by July 2025. Sindh and Khyber Pakhtunkhwa plan a combined 300,000 kits, while Balochistan’s PKR 55 billion project will solarize 28,000 agricultural tube wells by 2027. These programs focus on regions where grid reliability hovers at 12-16 daily service hours and diesel costs hit PKR 40-60 per unit, making decentralized solar the lowest-cost alternative.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proposed cut in net-metering buy-back tariff | -2.50% | Punjab and Sindh urban feeders | Short term (≤ 2 years) |

| Grid congestion and reverse-power-flow risks | -1.80% | Lahore, Karachi, Islamabad DISCOs | Medium term (2-4 years) |

| PKR depreciation inflating imported component costs | -1.20% | Nationwide | Short term (≤ 2 years) |

| Weak local standards and counterfeit panels glut | -0.80% | Low-income residential segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proposed Cut in Net-Metering Buy-Back Tariff

The Economic Coordination Committee’s March 2025 nod to lower the buy-back rate from PKR 27 to PKR 10 per unit, plus term reduction from 10 to five years, seeks to avert PKR 545 billion in cross-subsidies by 2034.(3)ECC Approves Net-Metering Tariff Cut,” dawn.com If enforced, payback periods for typical 5 kW rooftops would stretch from four to eight years and could slow residential adoption by 30-40% through 2027. Industrial users remain shielded because direct PPAs avoid net-metering altogether.

Weak Local Standards and Counterfeit Panels Glut

The Pakistan Solar Association warned in August 2024 that low-grade modules are penetrating price-sensitive segments, threatening long-term system performance.(4) Pakistan Solar Association, “Position Paper on Module Quality,” paksolar.org Voluntary certification and lax border checks exacerbate the risk, undermining consumer confidence.

Segment Analysis

By Technology: Photovoltaic Monopoly Persists

Solar photovoltaic maintained a 100% installation footprint within the Pakistan solar energy market in 2024 and is forecast to expand at an 18.1% CAGR through 2030, leaving concentrated solar power (CSP) commercially dormant. Crystalline-silicon modules, chiefly polycrystalline and monocrystalline PERC, represent 98% of deployed wattage, driven by 18-22% conversion efficiencies and sub-USD 0.15-per-watt pricing. Pakistan imported 16.9 GW of PV modules in 2024 alone, validating the country’s status as a pivotal off-take base for excess Chinese capacity.

CSP languishes despite superior direct-normal-irradiance in Balochistan and Sindh because water-intensive steam cycles are incompatible with the regions’ arid climates and because PV CAPEX has fallen below PKR 70,000 per kilowatt. Until dry-cooled CSP costs drop by at least 40%, PV will preserve its stranglehold on the Pakistan solar energy market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Grid Type: Off-Grid Gains Momentum

On-grid systems controlled 92.5% of installed wattage in 2024 owing to lucrative net-metering and bankable industrial PPAs. However, net-metering caps and buy-back revisions are beginning to steer adopters toward self-sufficient architectures. Off-grid installations are forecast to grow at a 25.9% CAGR to 2030 as rural households, telecom towers, and agricultural tube wells bypass unreliable networks. Balochistan’s PKR 55 billion tube-well program alone will inject 28,000 standalone pumps, freeing 200-250 MW of grid capacity for factories.(5)Balochistan Government, “Solar Tube-Well Project Brief,” balochistan.gov.pk

By End User: Residential Surge Reshapes Demand

Commercial and industrial users occupied 51.9% of installed capacity in 2024, anchored by textile and food clients that hedge tariff volatility through rooftop assets. Yet the residential segment is projected to rise at a blistering 23.5% CAGR, powered by provincial subsidies and net-metering. Punjab’s zero-interest program could alone seed 1 GW of additional rooftops by 2027.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Punjab and Sindh jointly host 70-75% of the national capacity. Punjab leads with an estimated 3.5 GW, propelled by Faisalabad and Lahore textile rooftops plus the province’s expansive residential-subsidy slate. Sindh sits at roughly 2 GW, punctuated by K-Electric’s 490 MW pipeline spanning Gharo and Jhimpir, which promises PKR 3.4 billion in annual savings and will displace 400,000 tons of coal annually. Karachi’s commercial districts showcase the densest rooftop penetration, nearing 50,000 metered systems.

Balochistan and Khyber Pakhtunkhwa trail but post outsized growth rates as off-grid solar overtakes costly line extensions. Islamabad Capital Territory, though representing less than 2% of installed capacity, ranks highest on a per-capita basis thanks to affluent demographics and efficient net-metering administration. Provincial disparities in budgetary firepower, Punjab’s PKR 12.6 billion versus Balochistan’s PKR 2.5 billion, risk widening regional adoption gaps without federal equalization.

Competitive Landscape

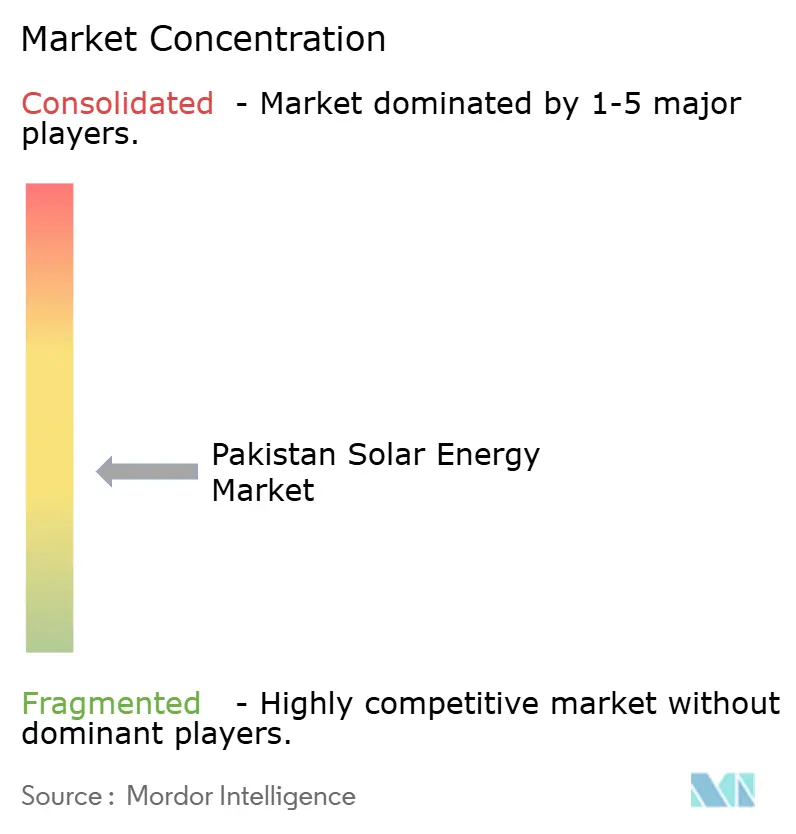

The Pakistan solar energy market is moderately fragmented. Chinese module majors, JinkoSolar, Canadian Solar, LONGi, Trina Solar, and JA Solar, collectively funnel more than 95% of imports through vendor financing tied to CPEC obligations. Local EPC specialists such as Reon Energy and Yellow Door Energy compete on speed and service, increasingly bundling finance, O&M, and monitoring. Reon disclosed a 1.5 GW pipeline in 2024 and expanded into Bangladesh, while Yellow Door’s 50 MW PPA-backed fleet underscores growth in captive C&I supply. Huawei, SMA, and Fronius dominate inverters, with Huawei’s AI-enabled FusionSolar lowering downtime by 15-20% for process-heavy factories. Rising provincial tenders featuring tariffs near PKR 9.8 per unit promise volume but compress developer margins to single-digits, foreshadowing consolidation among undercapitalized firms. Counterfeit panel inflows and optional certification regimes remain systemic risks to long-term customer trust.

Pakistan Solar Energy Industry Leaders

-

Yellow Door Energy

-

Reon Energy Ltd

-

Zonergy

-

Shams Power Ltd

-

Alpha Renewables

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: In a bid to tackle the electricity crisis and promote sustainable energy, the Khyber Pakhtunkhwa (K-P) government has rolled out a project distributing free solar kits to 130,000 low-income households. The initiative, set to unfold in two phases, will initially focus on 32,500 households.

- November 2024: Lucky Cement announced a hybrid wind-solar project through the Special Investment Facilitation Council.

- May 2024: Oracle Power, a UK-based renewable project developer, has initiated a transmission and grid interconnection study for its ambitious 1.3 GW renewable complex in southern Pakistan. Set to rise in Jhimpir village, Sindh Province, the renewable hub will feature a blend of 800 MW solar and 500 MW wind power capacity, complemented by a 450 MWh battery energy storage system (BESS).

- January 2024: Norwegian renewable energy developer Scatec started commercial operation of 150 megawatt solar PV plants in Pakistan. The solar power projects boast an annual generation capacity of 300 gigawatt hours. Scatec also signed a 25-year power purchase agreement with the Central Power Purchasing Agency of Pakistan.

Pakistan Solar Energy Market Report Scope

Solar power means using the sun's energy to produce electricity, either directly as thermal energy (heat) or indirectly through photovoltaic cells in solar panels and clear photovoltaic glass. \

The Pakistan solar energy market is segmented by technology, grid type, end-user, and component type. By technology, the market is segmented into solar photovoltaic (PV) and concentrated solar power (CSP). By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial and industrial, and residential. By component, the market is segmented into solar modules, inverters, mounting and tracking systems, balance-of-system and electricals, energy storage, and hybrid integration. For each segment, market sizing and forecasts have been done based on installed capacity.

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is solar capacity growing in Pakistan?

Installed capacity is forecast to climb from 6.75 GW in 2025 to 15.50 GW by 2030, equal to an 18.09% CAGR.

What is the largest end-user group for solar in Pakistan?

Commercial and industrial consumers held 51.9% of capacity in 2024, led by textile and food processors seeking tariff relief.

How will the proposed net-metering tariff cut affect rooftop paybacks?

If the PKR 27 to PKR 10 unit rate is enforced, residential payback periods could lengthen from four to around eight years.

Which provinces are rolling out subsidized rooftop kits?

Punjab, Sindh, and Khyber Pakhtunkhwa have collectively budgeted programs targeting roughly 400,000 low-income households.

Are battery-storage hybrids gaining traction?

Yes, falling lithium-ion prices and Pakistan’s first 350 MW solar-wind-BESS agreement indicate a pivot toward storage-integrated projects.

What share of imports do Chinese module makers hold?

Chinese brands supply more than 95% of Pakistan’s imported modules, supported by vendor financing and steep price discounts.

Page last updated on: