Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 251.3 Million |

| Market Size (2030) | USD 289.3 Million |

| Growth Rate (2025 - 2030) | 2.86% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Crop Protection Chemicals Market Analysis by Mordor Intelligence

The Pakistan Crop Protection Chemicals Market size is estimated at 251.3 million USD in 2025, and is expected to reach 289.3 million USD by 2030, growing at a CAGR of 2.86% during the forecast period (2025-2030).

Agriculture remains a cornerstone of Pakistan's economy, employing over 40% of the country's workforce and positioning the nation among the world's top 10 producers of essential crops like wheat, cotton, sugarcane, mango, dates, and Kinnow oranges. The agricultural sector's significance is further emphasized by the contribution of major crops (wheat, rice, cotton, and sugarcane), which account for approximately 4.9% of the country's GDP. Pakistan's agricultural landscape is characterized by a dual cropping system the Kharif season from April to December and the Rabi season from October to May enabling year-round cultivation and necessitating comprehensive crop protection chemicals strategies.

The crop protection chemicals market in Pakistan is experiencing a transformation driven by the adoption of modern agricultural practices and precision farming techniques. In 2022, the average pesticide consumption reached 0.4 kilograms per hectare of agricultural land, reflecting the increasing emphasis on crop protection measures. Farmers are increasingly embracing integrated pest management techniques, combining chemical and biological control methods to enhance crop yields while minimizing environmental impact. This shift towards sustainable agricultural practices is reshaping market dynamics and influencing product development strategies among manufacturers.

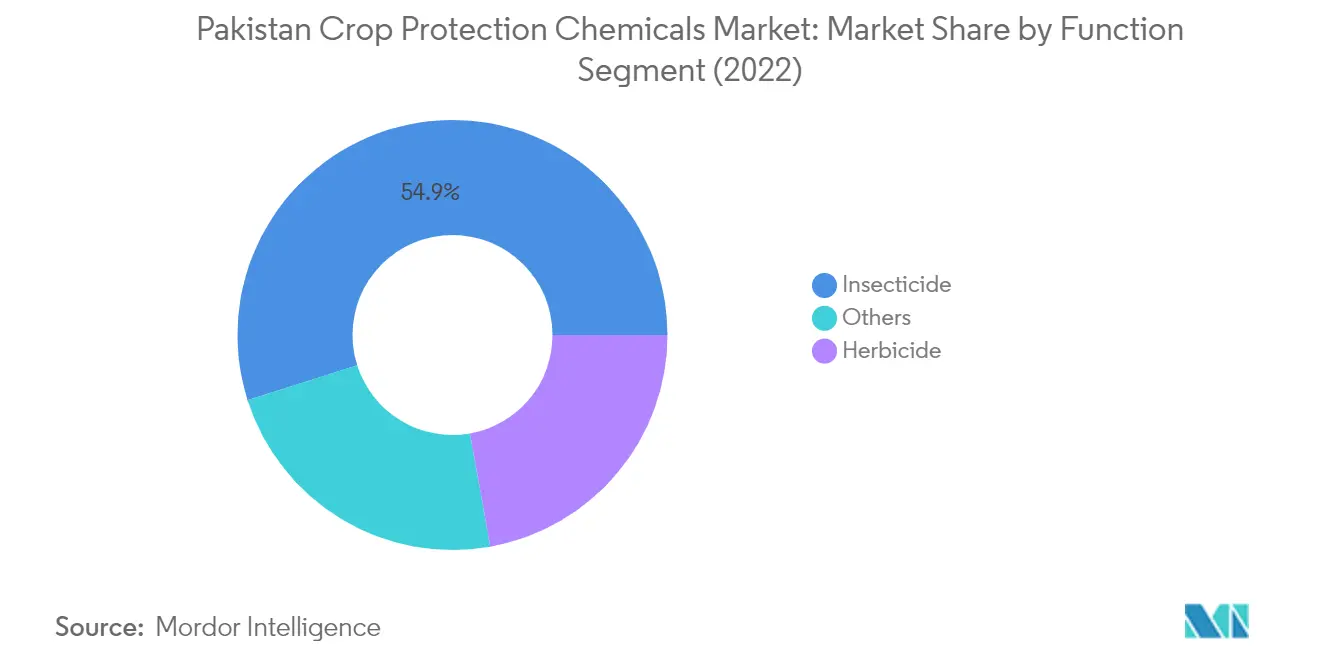

The market landscape is significantly influenced by seasonal pest challenges, with different cropping seasons facing distinct threats. The Kharif season contends primarily with pink bollworm infestations in cotton crops, while the Rabi season faces challenges from wheat aphids, fall armyworms, and whiteflies. These pest patterns have led to a specialized approach in agricultural pest control, with pesticides dominating the market at a 54.9% share in 2022, followed by herbicides at 22.2%. The industry has responded with targeted solutions for specific crop-pest combinations, leading to more efficient and effective pest management strategies.

The market is witnessing substantial technological advancement through strategic partnerships and government initiatives. In December 2023, the Asian Development Bank approved a project offering climate-friendly, technology-based solutions to improve pest control and increase crop production in Pakistan. This initiative aims to enhance data collection capabilities and implement more effective pest management strategies. The industry faces significant challenges, with weed infestation causing 20-30% of crop losses, driving the development of more effective herbicide formulations and application techniques. These developments are complemented by increasing farmer education programs and the introduction of digital farming solutions to optimize pesticide usage and improve crop yields.

Pakistan Crop Protection Chemicals Market Trends and Insights

Growing infestations by fungal diseases in major crops like wheat, rice, and cotton increased the fungicide consumption per hectare in the country

- Pakistan has a diverse range of agricultural practices and cultivates various crops across different regions. The country's climate and soil conditions support the cultivation of a wide variety of crops. Pests pose a significant threat to crop production, leading to reduced yields and potential crop failures. To combat these challenges, the country used an average of 0.4 kilograms of crop protection chemicals per hectare of agricultural land in 2022.

- Fungal diseases pose a major threat to agriculture in Pakistan, impacting crops such as wheat, rice, cotton, fruits, and vegetables. These diseases result in substantial crop losses, reduced yields, and poor-quality produce. As a consequence, farmers experience financial hardships and potential food shortages. Fungicides hold the leading position in terms of pesticide consumption, with an average consumption of 165.3 grams per hectare in 2022. This trend reflects the need to combat fungal diseases and mitigate their detrimental effects on crop production.

- Insecticides hold the second leading position in terms of pesticide consumption. In 2022, the average amount of insecticides applied per hectare was 155.3 grams. Insecticide usage in agriculture in Pakistan is prevalent due to the country's heavy reliance on agricultural practices and the need to protect crops from insect pests. Insecticides are used to control various pests that can cause damage to crops, reduce yields, and threaten food security.

- The application rate of herbicides per hectare in 2022 was 100.9 grams per hectare. This can be attributed to the growing awareness of herbicide usage as a beneficial and cost-effective method for enhancing crop yields in terms of both quantity and quality by effectively managing weed growth and minimizing labor expenses.

Understand The Key Trends Shaping This Market

Download PDF

Increased crop losses due to various pests and diseases and growing demand for pesticides for better management are boosting the prices of active ingredients

- Cypermethrin takes the lead as the primary insecticide utilized in the country, being a synthetic pyrethroid effective against a wide range of insect pests, including whiteflies, aphid hoppers, bollworms, jassids, thrips, mites, cutworms, pod borers, leaf miners, and psylla. India and China are the primary exporters of cypermethrin to Pakistan. As of 2022, the price of this active ingredient surged to USD 21,137.1 per metric ton after witnessing an increasing trend Y-o-Y. This price surge is mainly driven by the rising demand for cypermethrin in crops like sugarcane, cotton, fruits, and vegetables and its limited production capacities in the country.

- Atrazine holds a prominent position as a widely used herbicide in the country, belonging to the chlorinated herbicide of the triazine class. It serves as a pre-emergence herbicide, effectively controlling a wide range of annual grasses and some annual broadleaf weeds in crops such as maize, beans, sunflowers, and sugarcane. The active ingredient's price has consistently grown Y-o-Y due to its extensive application across different crops. As of the latest recording in 2022, the price stood at USD 13,816.0 per metric ton.

- Glyphosate takes the second spot as the most widely used herbicide, with a price standing at USD 1,144.1 per metric ton. Many farmers prefer to use this active ingredient because it is the most affordable and cost-effective solution for weed control.

- Mancozeb serves as both a curative and preventive fungicide and targets a broad spectrum of fungal diseases in cereal crops, fruits, vegetables, and pulses. With its current price standing at USD 7,767.0 per metric ton, Mancozeb ranks as one of the primary fungicide active ingredients widely employed in the country.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: Function

Insecticide Segment in Pakistan Crop Protection Chemicals Market

The insecticides segment continues to dominate the Pakistan crop protection chemicals market, accounting for approximately 55% market share in 2024. This significant market position is primarily driven by the widespread prevalence of insect pests affecting major crops in the country. Armyworms, stem borers, aphids, wheat bugs, rice weevils, rice leaf folders, and thrips are among the major insect pests causing substantial yield losses in cereal crops. The segment's dominance is particularly evident in the grains and cereals sector, where insecticides play a crucial role in protecting wheat, rice, and other staple crops. Additionally, the cotton sector, where Pakistan ranks as the fifth-largest producer globally, heavily relies on insecticides to combat pests like whitefly and pink bollworm, further solidifying the segment's market leadership.

Herbicide Segment in Pakistan Crop Protection Chemicals Market

The herbicides segment is projected to exhibit the strongest growth in the Pakistan crop protection chemicals market during 2024-2029, with an expected growth rate of approximately 4%. This robust growth trajectory is driven by the increasing challenges posed by weed infestations, which cause about 20-30% yield losses in different crops. The segment's growth is particularly notable in pulses and oilseeds cultivation, where weeds like Phalaris minor, Chenopodium album, Convolvulus arvensis, barnyard grass, wild oats, and Cyperus rotundus pose significant threats to crop yields. The growth is further supported by the rising adoption of soil treatment chemicals, where herbicides are predominantly used, accounting for a significant portion of the application methods. The segment's expansion is also influenced by Pakistan's clay soil conditions, especially in the Punjab province, which creates favorable conditions for weed growth.

Remaining Segments in Function Segmentation

The remaining segments in the Pakistan crop protection chemicals market include fungicides, molluscicides, and nematicides, each serving specific crop protection needs. Fungicides play a vital role in controlling various diseases affecting cereals, fruits, and vegetables, particularly in regions with warm temperatures that create favorable conditions for fungal pathogens. Molluscicides are essential for controlling snails and slugs, particularly in rice cultivation where golden apple snails pose significant threats. Nematicides serve a crucial function in managing microscopic worms that can cause significant damage to crops, with their application being particularly important in soil treatment processes. These segments, while smaller in market share, remain integral to the overall crop protection strategy in Pakistan's agricultural sector.

Segment Analysis: Application Mode

Foliar Segment in Pakistan Crop Protection Chemicals Market

The foliar application segment dominates the Pakistan crop protection chemicals market, accounting for approximately 52% market share in 2024. This significant market position is primarily driven by farmers increasingly adopting precision farming methods, which allow for more targeted and efficient application of pesticides. Foliar application has become particularly crucial for insecticide application, with insecticides representing the largest share of chemicals applied through this method. The method's popularity stems from its convenience and effectiveness in quickly controlling leaf-infesting pathogens when identified on the plant. Additionally, foliar application provides farmers with the flexibility to adjust application rates based on specific crop needs and pest pressure levels, making it an essential tool in modern agricultural practices.

Soil Treatment Segment in Pakistan Crop Protection Chemicals Market

The soil treatment chemicals segment is projected to exhibit the strongest growth trajectory, with an anticipated CAGR of approximately 4% during 2024-2029. This growth is primarily driven by the increasing adoption of pre-emergence herbicides and the rising awareness about soil-borne diseases among farmers. The segment's expansion is further supported by the effectiveness of soil treatment in allowing better absorption and distribution of pesticides within the soil, enabling direct interaction with pests and pathogens. The method's ability to provide longer-lasting protection and its effectiveness in controlling various soil-borne pests, diseases, and weeds makes it increasingly attractive to farmers looking for comprehensive crop protection solutions.

Remaining Segments in Application Mode

The other application modes - chemigation, seed treatment chemicals, and fumigation - each play vital roles in Pakistan's crop protection chemicals market. Chemigation has gained traction due to its ability to precisely time pesticide applications with irrigation events, making it particularly effective for systemic pesticides. Seed treatment chemicals serve as a preventive measure, protecting crops during their most vulnerable early growth stages. Fumigation, while representing a smaller share, remains crucial for stored grain protection and pre-planting soil treatment. These application methods offer farmers diverse options for protecting their crops at different growth stages and against various types of pests and diseases, contributing to a comprehensive crop protection strategy.

Segment Analysis: Crop Type

Grains & Cereals Segment in Pakistan Crop Protection Chemicals Market

The Grains & Cereals segment continues to dominate the Pakistan crop protection chemicals market, commanding approximately 52% of the total market value in 2024. This significant market share is primarily driven by the segment's crucial role in the country's food security and agricultural economy. Wheat, rice, and maize are the major crops in this segment, with wheat representing the largest share of cultivated area and production. The segment faces considerable challenges from various pests, diseases, and weeds, necessitating extensive use of crop protection chemicals, particularly insecticides which account for over 56% of chemical usage in grain crops. The Pakistani government's emphasis on enhancing agricultural productivity and ensuring food security has led to increased support for farmers in adopting modern crop protection practices, further solidifying the segment's market leadership.

Commercial Crops Segment in Pakistan Crop Protection Chemicals Market

The Commercial Crops segment is projected to exhibit the strongest growth in the Pakistan crop protection chemicals market, with an expected growth rate of approximately 3% during 2024-2029. This growth is primarily driven by the increasing importance of crops such as sugarcane, tobacco, and cotton in both domestic consumption and export earnings. The segment's expansion is supported by rising pest infestations and the growing adoption of integrated pest management techniques. Insecticides dominate the commercial crops segment, as these crops are particularly susceptible to various pests such as cotton bollworms and pink bollworms. The government's initiatives to improve agricultural productivity and promote export-oriented farming practices are expected to further boost the demand for crop protection chemicals in this segment.

Remaining Segments in Crop Type

The remaining segments in the market include Fruits & Vegetables, Pulses & Oilseeds, and Turf & Ornamental, each playing distinct roles in Pakistan's agricultural landscape. The Fruits & Vegetables segment is gaining prominence due to increasing export opportunities and growing domestic demand for high-quality produce. The Pulses & Oilseeds segment is crucial for food security and reducing dependency on imports, with particular focus on pest management and weed control. The Turf & Ornamental segment, while smaller, serves specific needs in urban landscaping and recreational facilities. These segments collectively contribute to the diverse requirements of crop care chemicals, each facing unique challenges in terms of pest management, disease control, and yield optimization.

Competitive Landscape

Top Companies in Pakistan Crop Protection Chemicals Market

The pesticide companies market in Pakistan is characterized by companies focusing on strategic initiatives to strengthen their market positions. Product innovation remains a key trend, with crop protection companies developing new formulations and active ingredients to address evolving pest challenges and resistance issues. Companies are expanding their operational footprint through partnerships and collaborations, particularly to enhance distribution networks and manufacturing capabilities. Strategic moves include joint ventures for technology sharing and market access, while expansion strategies focus on establishing new production facilities and R&D centers. The industry also witnesses significant investment in sustainable and environmentally friendly solutions, reflecting growing environmental consciousness and regulatory requirements.

Consolidated Market Led By Global Players

The Pakistani crop protection chemicals market exhibits a consolidated structure dominated by multinational pesticide companies in Pakistan with an established global presence. These major players leverage their extensive R&D capabilities, technological expertise, and robust distribution networks to maintain market leadership. Local companies, while present in the market, primarily operate as distributors or manufacturers of generic products, with limited capacity for innovation and research development. The market's consolidation is further reinforced by high entry barriers, including significant capital requirements, regulatory compliance needs, and the necessity for extensive research capabilities.

The market demonstrates active merger and acquisition activity, primarily driven by global players seeking to strengthen their presence in the region. These strategic moves often involve acquiring local distribution networks, manufacturing facilities, or smaller companies with complementary product portfolios. Vertical integration strategies are also prevalent, with companies expanding across the value chain to secure raw material supplies and enhance distribution capabilities. The competitive landscape is further shaped by strategic alliances between global and local players, combining international expertise with local market knowledge.

Innovation and Distribution Drive Market Success

For incumbent companies to maintain and expand their market share, developing innovative solutions tailored to local agricultural conditions and pest challenges is crucial. This includes investing in research and development to create new formulations, improving product efficacy, and addressing resistance issues. Building strong relationships with farmers through technical support and education programs helps create brand loyalty and market penetration. Companies must also focus on sustainable practices and environmentally friendly solutions to align with growing regulatory pressures and changing consumer preferences.

Contenders looking to gain ground in the market need to focus on developing specialized products for specific crop segments or regional requirements. Establishing strong distribution networks and partnerships with local agricultural organizations can help overcome market entry barriers. Success also depends on understanding and adapting to local farming practices, weather conditions, and pest patterns. Companies must navigate the regulatory landscape effectively while maintaining competitive pricing strategies. The ability to offer comprehensive solutions, including digital farming technologies and integrated pest management approaches, will become increasingly important for market success.

Pakistan Crop Protection Chemicals Industry Leaders

BASF SE

Bayer AG

FMC Corporation

Pakistan Agro Chemicals Private Limited

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

- August 2022: BASF and Corteva Agriscience collaborated to provide soybean farmers with the weed control of the future. By working together, BASF and Corteva aim to satisfy farmers' demand for specialized weed control solutions that are distinct from those that are currently available or being developed.

- May 2022: UPL partnered with Bayer for Spirotetramat insecticide to develop new pest management solutions. Through this long-term global data access and supply agreement with Bayer, specifically for addressing farmer demands regarding resistance management and difficult-to-control sucking pests, UPL will develop, register, and distribute new unique solutions, including Spirotetramat, using its experience in insecticides and worldwide research and development network.

Pakistan Crop Protection Chemicals Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.Function

| Fungicides |

| Herbicides |

| Insecticides |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits & Vegetables |

| Grains & Cereals |

| Pulses & Oilseeds |

| Turf & Ornamental |

| Function | Fungicides |

| Herbicides | |

| Insecticides | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits & Vegetables | |

| Grains & Cereals | |

| Pulses & Oilseeds | |

| Turf & Ornamental |

Need A Different Region or Segment?

Customize Now

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF