Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

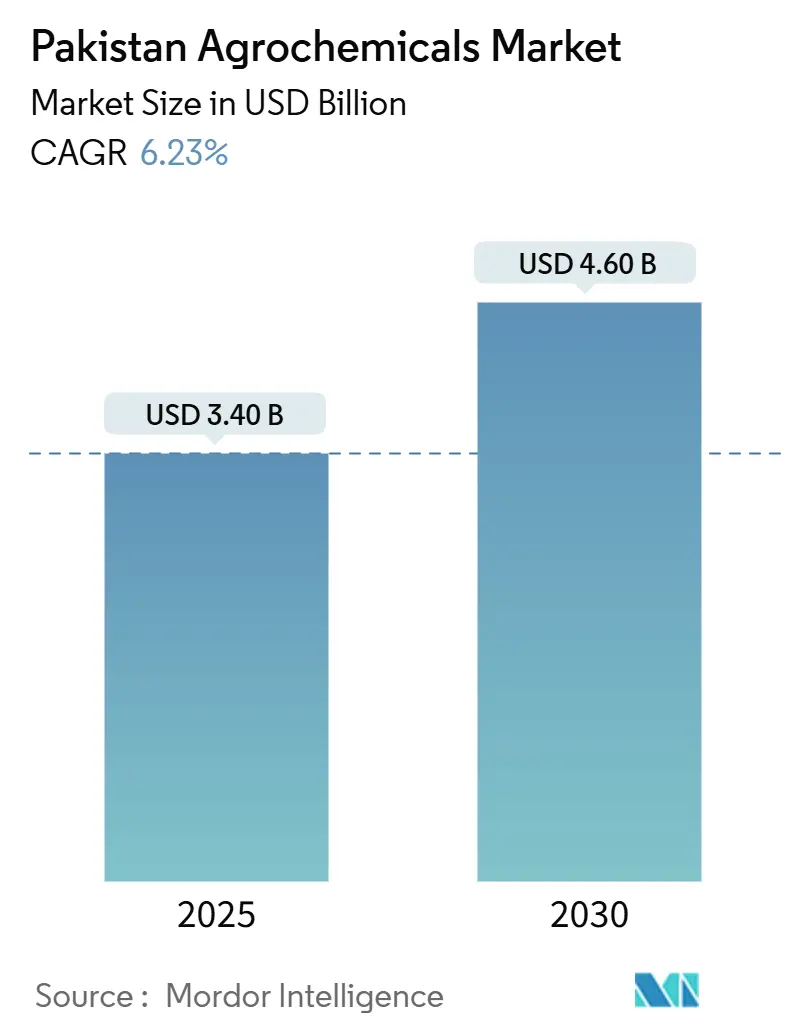

| Market Size (2025) | USD 3.40 Billion |

| Market Size (2030) | USD 4.60 Billion |

| Growth Rate (2025 - 2030) | 6.23% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pakistan Agrochemicals Market Analysis by Mordor Intelligence

The Pakistan agrochemicals market size reached USD 3.40 billion in 2025 and is advancing at a 6.23% CAGR that will lift the value to USD 4.60 billion in 2030. Changes in fertilizer usage, adoption of efficient irrigation systems, and digital agriculture platforms are transforming farming practices. Frequent pest outbreaks maintain the demand for crop protection products. Government subsidies support smallholder farmers' purchasing ability for agricultural inputs, while companies increase investments in contract farming and advisory services. For instance, in 2021, the government introduced the Kisaan Card Programme, which directly subsidizes pesticides for farmers. This program is a segment of a larger effort to dispense USD 0.061 billion in direct subsidies to farmers. Online sales channels are gaining market share from traditional retail stores by offering transparent prices and quicker delivery.

Key Report Takeaways

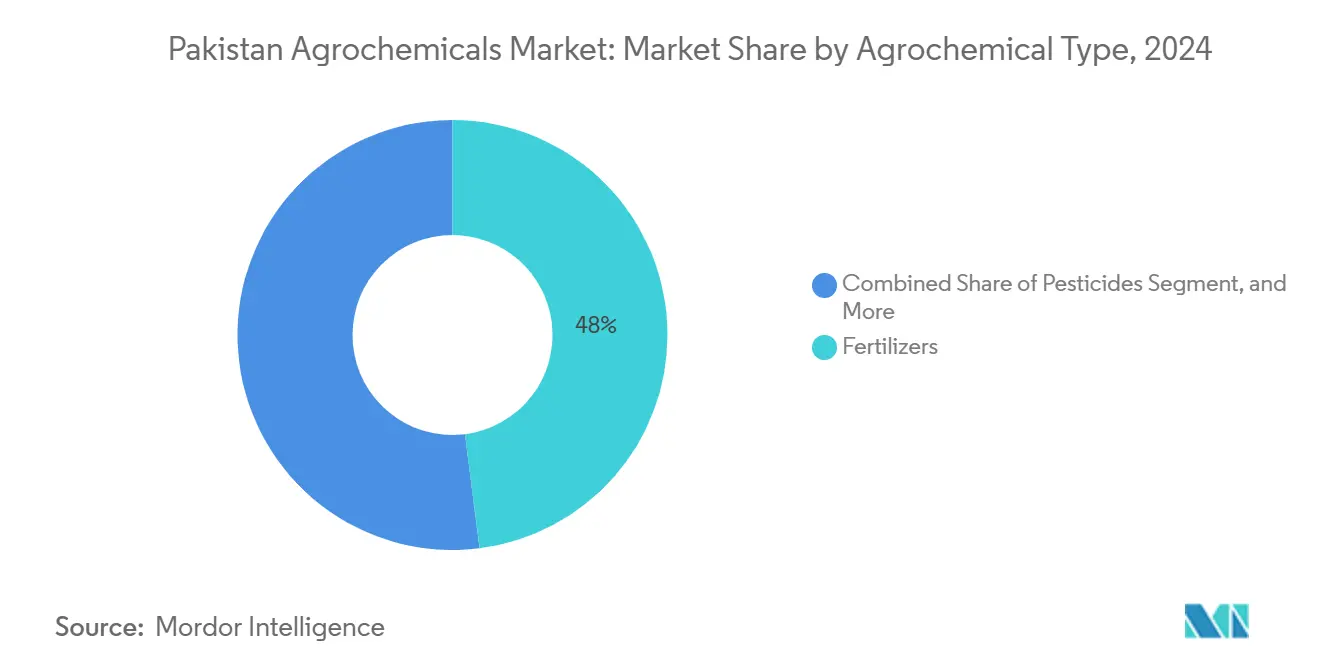

- By agrochemical type, fertilizers dominate the Pakistan agrochemicals market share, accounting for 48% in 2024, while pesticides are growing at the fastest rate, with a 6.4% CAGR through 2030.

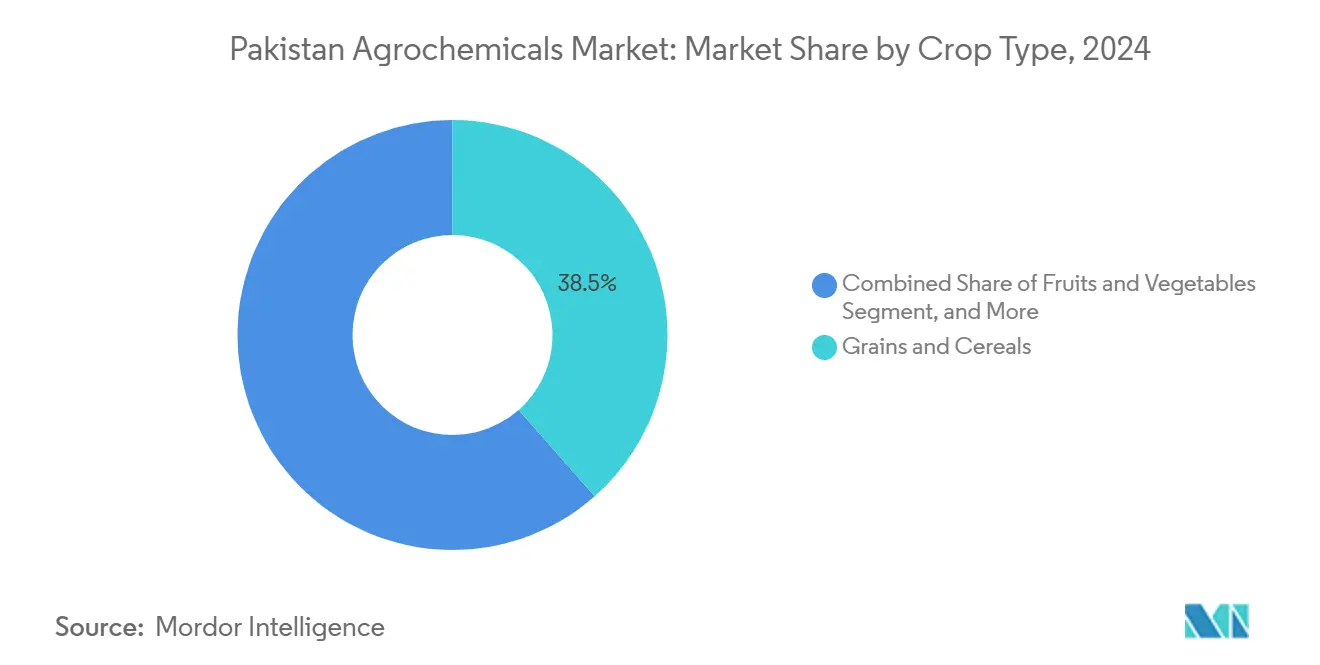

- By crop, grains and cereals accounted for a 38.5% share of the Pakistan agrochemicals market size in 2024, and fruits and vegetables are advancing at a 5.6% CAGR through 2030.

Pakistan Agrochemicals Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recurring Pest and Disease Outbreaks | +1.2% | Punjab and Sindh cotton belts | Short term (≤ 2 years) |

| Rising Food Security Pressure and the Yield Gap | +1.8% | National wheat and rice zones | Medium term (2-4 years) |

| Government Fertilizer Subsidy Realignment | +1.0% | National smallholder segments | Medium term (2-4 years) |

| Expansion of High Efficiency Irrigation Systems | +0.8% | Punjab, Sindh, and extending to Balochistan | Long term (≥ 4 years) |

| Growth of Contract Farming and Agricultural Services | +0.9% | Commercial crop areas nationwide | Medium term (2-4 years) |

| Integration of Digital Agronomy Platforms | +0.6% | Progressive districts nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recurring Pest and Disease Outbreaks

Frequent outbreaks of crop-damaging pests and diseases have increased insecticide and fungicide usage across major agricultural regions. Cotton, rice, and fruit crops have experienced significant losses, compelling farmers to implement intensive protection measures.[1]Source: U.S. Department of Commerce, “Pakistan: Demand Grows for Insecticides, Pesticides,” commerce.gov In June 2025, mango orchards in Sindh faced severe malformation and hopper infestations, while September 2023 saw whitefly attacks devastate cotton fields in Punjab. Export-related chemical residue regulations have driven manufacturers to develop precise, cleaner formulations. Extended pest breeding seasons due to higher temperatures necessitate multiple treatments, particularly in high-value orchards. These shifting dynamics are prompting greater investment in scouting technologies and predictive pest modeling to optimize spray timing. Additionally, growers are increasingly adopting rotation strategies and integrated pest management to reduce dependency on chemical interventions while maintaining crop health.

Rising Food Security Pressure and the Yield Gap

Pakistan's agricultural sector must address yield gaps to ensure food security. Wheat and rice yields remain below global standards, increasing the need for enhanced nutrient inputs and crop protection methods. Government programs promote balanced fertilization and integrated pest management through focused farmer support initiatives. Quality maintenance has become crucial as export volumes increase, particularly for rice and cotton. Farmers show increased interest in specialty nutrients like zinc and boron, demonstrating greater awareness of soil health and testing requirements. To further support productivity, agricultural extension services are expanding mobile advisory platforms that deliver region-specific guidance on input use, pest control, and irrigation scheduling directly to farmers.

Government Fertilizer Subsidy Realignment

The fertilizer subsidy system has transformed through digital platform implementation, improving targeting accuracy and reducing distribution inefficiencies. Domestic fertilizer manufacturers maintain stable production through consistent input supply. In October 2024, Pakistan's government collaborated with Engro Fertilizers to launch the UgAi app, a digital agri-commerce platform enabling farmers to purchase fertilizers directly at official prices, access satellite crop monitoring, and receive tailored recommendations. Current policies promote advanced formulations and precision agriculture methods, shifting from conventional broad application approaches. Site-specific blends and micronutrient-enhanced products have gained importance in the market. These modernization efforts support efficient nutrient utilization, higher crop yields, and lower environmental impact.

Expansion of High Efficiency Irrigation Systems

Modern irrigation technology adoption is changing agricultural water management practices. Drip and sprinkler systems demonstrate economic benefits, particularly in water-scarce areas.[2]Source: Amar Razzaq et al., “An Economic Analysis of High Efficiency Irrigation Systems in Punjab, Pakistan,” Sarhad Journal of Agriculture, researcherslinks.com These systems enable precise fertilizer and pesticide application through fertigation. Large farms are investing in advanced irrigation infrastructure, including moisture sensors and automated chemigation systems, driven by government incentives and increased water costs. This technological advancement improves input efficiency and crop productivity while minimizing waste. Farmers are integrating mobile-controlled irrigation platforms that allow real-time adjustments based on weather forecasts and soil data, further enhancing resource conservation and operational flexibility.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Environmental Compliance Costs | -0.8% | Export-oriented provinces | Short term (≤ 2 years) |

| Mounting Antimicrobial Resistance Concerns | -0.6% | Integrated crop-livestock systems | Medium term (2-4 years) |

| Export Restrictions on Key Ingredients | -0.5% | Import-dependent producers | Short term (≤ 2 years) |

| Smallholder Affordability Constraints | -0.9% | Rain-fed and marginal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Environmental Compliance Costs

Enhanced environmental regulations require pesticide companies to modify product formulations and restrict specific active ingredients. Additional compliance requirements stem from international agreements and trade protocols, particularly regarding residue limits and prohibited substances. These requirements increase operational expenses and benefit companies with established quality control systems. Testing and certification requirements challenge smaller companies, resulting in industry consolidation. The demand for environmentally safe inputs influences farming methods, with increased adoption of safer alternatives and precise application techniques.

Mounting Antimicrobial Resistance Concerns

The increasing concerns about antimicrobial resistance have led to stricter regulatory oversight in Pakistan's agrochemical market. The regulatory authorities now mandate comprehensive documentation for pesticide usage, with specific restrictions on broad-spectrum chemicals in sensitive applications.[3]Source: Khyber Pakhtunkhwa Agriculture Extension, “Plant Protection,” agriext.kp.gov.pk These regulatory requirements create compliance challenges for producers and distributors, particularly those serving export markets with strict pesticide residue standards. While the transition to responsible chemical management is necessary, it increases operational complexities and drives companies to implement targeted crop protection approaches.

Segment Analysis

By Agrochemical Type: Fertilizers Retain Scale while Pesticides Surge

Fertilizers held 48% of the Pakistan agrochemicals market size in 2024, maintaining dominance due to the nutrient requirements of wheat and rice cultivation. These crops depend on nitrogenous inputs like urea and ammonium, while phosphatic fertilizers maintain steady demand in cotton and sugarcane production. Potassium-based products are increasing in usage as soil testing reveals deficiencies. Micronutrients, particularly zinc and boron, are seeing increased adoption among farmers focused on improving yields and crop resilience.

Pesticides are experiencing the highest growth at a 6.4% CAGR, driven by increased pest challenges and export quality standards. Herbicide use is increasing in mechanized cereal farming due to labor shortages. Fungicide application is growing in fruit cultivation, especially in citrus and mango orchards, targeting exports. Plant growth regulators and spray adjuvants are seeing increased adoption alongside precision spraying equipment that enables efficient application rates.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Cereal Core, Horticulture Accelerator

Grains and cereals consumed 38.5% of the Pakistan agrochemicals market share in 2024, reflecting Pakistan's focus on wheat and rice production. These crops require substantial fertilizer and herbicide inputs, particularly in mechanized farming areas. Cotton and sugarcane maintain significant demand for phosphatic and nitrogenous fertilizers. Pulses and oilseeds are receiving increased policy support, driving demand for micronutrient blends and selective herbicides.

The fruits and vegetables segment is growing at a 5.6% CAGR, driven by export markets and domestic consumption patterns. These crops require specific fungicides and pesticides to meet quality standards. Commercial orchards are implementing professional spray services and strict harvest protocols, increasing demand for high-quality inputs. The turf and ornamental segment remains profitable despite its smaller size, supported by urban development.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Punjab leads the Pakistan agrochemicals market due to its extensive irrigated cultivation of wheat, rice, and cotton. The region's dual crop cycles create high demand for nitrogen fertilizers and require multiple pesticide applications. Sindh ranks second, where cotton and sugarcane farming face salinity and pest issues, driving consistent demand for micronutrients and insecticides. Khyber Pakhtunkhwa's high-altitude fruit and vegetable production requires specialized disease management and fertigation-compatible nutrients. Balochistan shows growth potential as canal expansion and corporate farming initiatives increase agrochemical usage.

Punjab and Sindh implement strict residue testing protocols due to their export focus, encouraging farmers to use low-residue formulations. Water accessibility influences input selection, with canal-fed areas preferring quick-release urea, while rain-fed regions use slow-release and drought-tolerant products. Climate changes affect pest patterns across provinces, extending infestation periods and increasing the need for adaptable pesticide formulations.

Central Punjab's infrastructure supports digital scouting tools and drone spraying implementation, advancing precision agriculture adoption. Northern regions' challenging terrain limits mechanization, maintaining demand for small-pack pesticides for manual application. The agricultural industrial park in Sindh improves logistics efficiency, reducing delivery times to southern farmers and expanding market reach. These geographic factors influence agrochemical distribution, adoption, and regulation throughout Pakistan.

Competitive Landscape

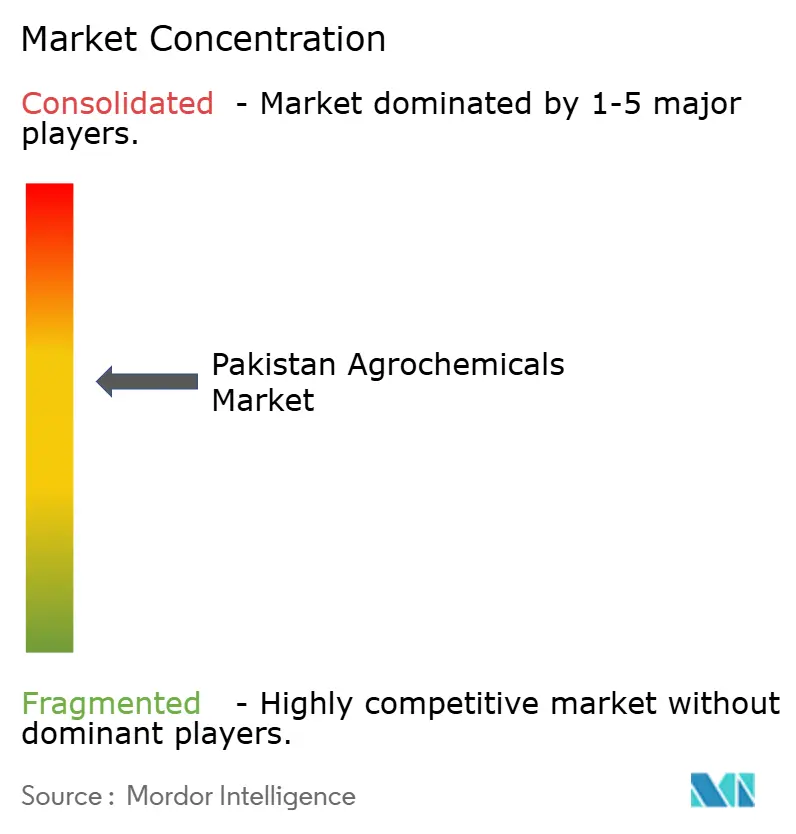

The Pakistan agrochemicals market is moderately consolidated, with five major companies controlling a substantial portion of industry revenue. Bayer AG holds a prominent position through its broad-spectrum herbicides and fungicides that meet residue compliance standards. Syngenta Group maintains a strong presence with integrated seed treatment solutions and foliar protection programs targeting commercial and export-oriented growers. UPL Limited has established its market presence through post-patent actives, while domestic companies Engro Corporation and Evyol Group are expanding from nitrogen fertilizers to micronutrient blends.

The industry shows significant movement toward vertical integration and operational expansion. Bayer AG partners with local service providers to develop drone-ready formulations for improved field application efficiency. Syngenta Group has invested in a Punjab-based residue-testing facility to support export compliance and orchard crop management. Engro Corporation is developing new product lines and distribution methods to expand its specialty inputs presence. The industry structure may shift as domestic fertilizer companies engage in merger discussions, potentially affecting capacity use and market prices.

Companies are developing reduced-risk chemical solutions to address regulatory requirements. Syngenta Group continues to expand its digital platform, providing satellite imagery and agronomic guidance that combines crop protection with precision farming. BASF SE, Corteva Agriscience, and FMC Corporation maintain market presence by introducing new technologies and stewardship programs that focus on grower relationships and regulatory compliance. These firms are also investing in localized field trials to tailor product performance to Pakistan’s diverse agro-climatic zones. Collaborative training initiatives with extension services are helping farmers adopt safer application practices and improve agrochemicals efficiency.

Pakistan Agrochemicals Industry Leaders

-

BASF SE

-

FMC Corporation

-

Syngenta Group

-

UPL Limited

-

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2024: Syngenta Group and Engro Corporation formed a partnership to enhance digital accessibility and agricultural input distribution for farmers across Pakistan. The initiative includes dedicated programs for female farmers, focusing on education and sustainable farming practices.

- April 2024: Fauji Fertilizer Company (FFC) introduced "Sona Boron DAP," the first boron-enriched DAP fertilizer in Pakistan. The product addresses micronutrient deficiencies while improving crop reproduction and soil quality in primary agricultural regions.

- May 2023: UPL Limited launched Doakda, a post-emergence selective herbicide designed specifically for rice crops in Pakistan. The product targets Leptochloa chinensis, a rapidly spreading weed that has become a major challenge for farmers across key rice-growing regions.

Pakistan Agrochemicals Market Report Scope

Pesticides are defined as commercially manufactured agrochemicals used to prevent crop destruction by pests, diseases, and weeds, thereby improving crop yield and quality. Pesticides used by farmers and large commercial growers in crops and non-crop agricultural practices are included in the market studied. The pesticides market in Pakistan is segmented by Origin (Synthetic, and Bio-based), Type (Herbicides, Insecticides, Fungicides, and Other Types), and Application (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, Turf and Ornamental Grasses, and Other Applications). The report offers the market size and forecasts in terms of Value (USD) and Volume (Metric Tons) for all the above segments.

By Agrochemical Type

| Fertilizers | Nitrogenous |

| Phosphatic | |

| Potassic | |

| Other Fertilizers (Calcium, Sulfur, Magnesium) | |

| Pesticides | Herbicides |

| Insecticides | |

| Fungicides | |

| Other Pesticides | |

| Adjuvants | |

| Plant Growth Regulators |

By Crop Type

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Commercial Cash Crops (Cotton, Sugarcane) |

| Turf and Ornamental |

| By Agrochemical Type | Fertilizers | Nitrogenous |

| Phosphatic | ||

| Potassic | ||

| Other Fertilizers (Calcium, Sulfur, Magnesium) | ||

| Pesticides | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Other Pesticides | ||

| Adjuvants | ||

| Plant Growth Regulators | ||

| By Crop Type | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Commercial Cash Crops (Cotton, Sugarcane) | ||

| Turf and Ornamental | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Pakistan agrochemicals market in 2025?

The Pakistan agrochemicals market size is at USD 3.4 billion in 2025 and is growing at a 6.23% CAGR toward USD 4.6 billion in 2030.

Which segment is growing quickest within the Pakistan agrochemicals market?

Pesticides are advancing at a 6.4% CAGR, the fastest among all major segments.

How concentrated is competition?

The Pakistan agrochemicals market exhibits moderate consolidation, with the top five companies capturing a substantial portion of industry revenue.

What policy measure supports smallholder input buying?

The Kisaan Card channels targeted subsidies directly to farmers, improving access to fertilizers and crop protection products.

Page last updated on: