Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

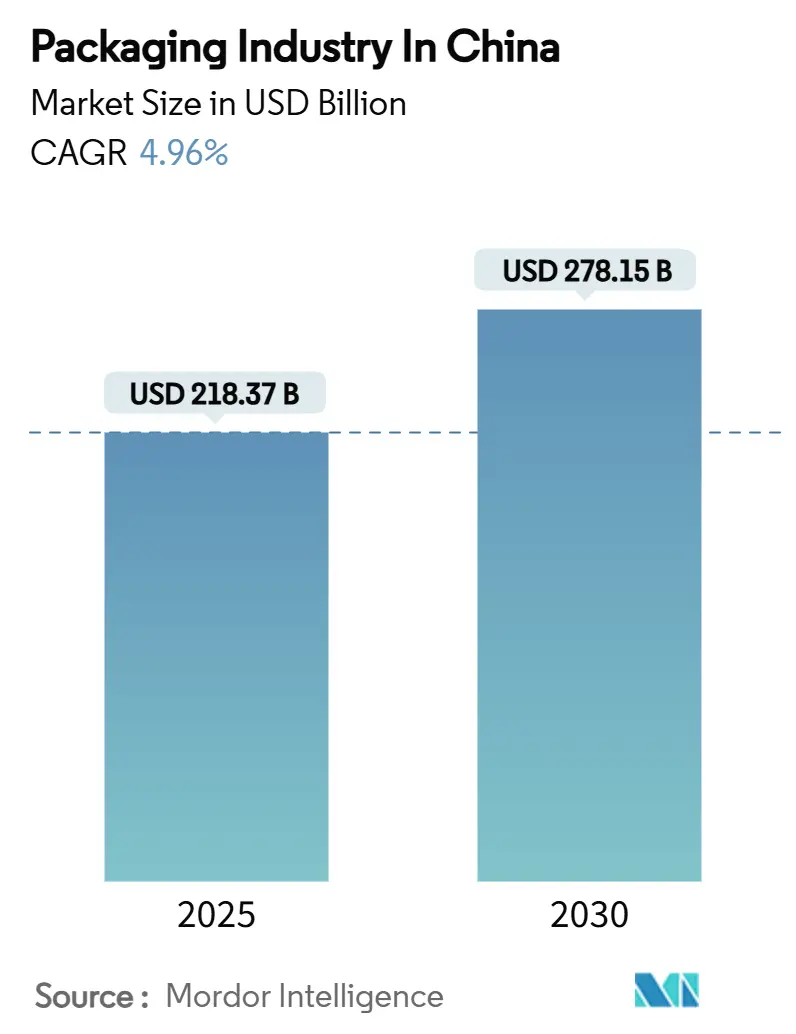

| Market Size (2025) | USD 218.37 Billion |

| Market Size (2030) | USD 278.15 Billion |

| Growth Rate (2025 - 2030) | 4.96% CAGR |

| Market Concentration | Low |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Packaging Market Analysis by Mordor Intelligence

The China packaging market is valued at USD 218.37 billion in 2025 and is forecast to reach USD 278.15 billion in 2030, reflecting a 4.96% CAGR across the review period. The China packaging market continues to expand on the back of the world’s largest e-commerce ecosystem; parcel volumes touched 175 billion units in 2024, intensifying demand for durable, automation-ready pack formats.[1]Fujian Provincial Department of Commerce, “2023 China E-commerce Market Data Report,” swt.fujian.gov.cn Mandatory express packaging standards (GB 43352-2023) are also steering the China packaging market toward low-toxicity substrates and standardised dimensions.[2]C&K Testing, “Mandatory Express Packaging Standard GB 43352-2023 Implemented,” cirs-ck.com Concurrently, large domestic producers such as Nine Dragons Paper and global majors like Amcor are leveraging scale, smart-factory investments and bio-based R&D pipelines to strengthen competitive positions. Regulatory pressure on single-use plastics, coupled with a 96.48% PET beverage recovery rate in 2025, is accelerating the shift to recycled and fibre-based formats.

Key Report Takeaways

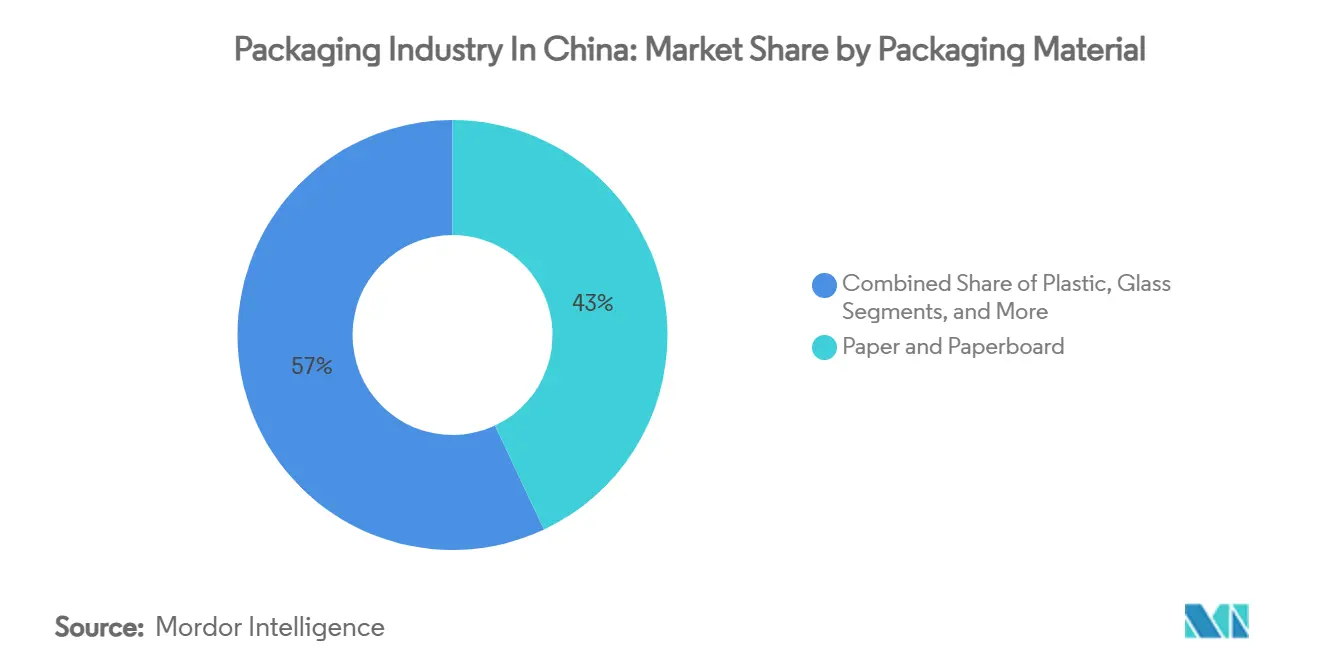

- By packaging material, Paper and Paperboard led with 43% revenue share in 2024, while Other Materials are projected to increase at a 7.21% CAGR through 2030.

- By packaging type, Primary Packaging accounted for 70% of the China packaging market size in 2024, yet Tertiary Packaging is set to expand at 6.03% CAGR over 2025-2030.

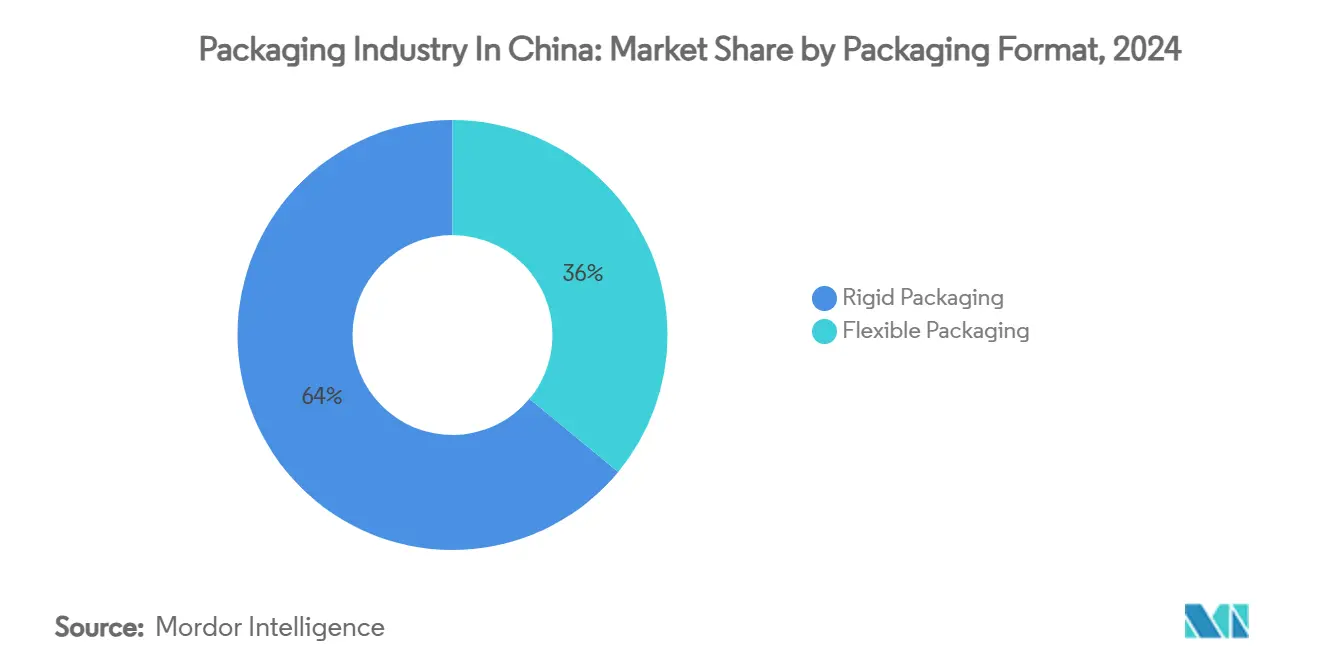

- By packaging format, Rigid Packaging held 64% China packaging market share in 2024, whereas Flexible Packaging is advancing at a 6.79% CAGR to 2030.

- By end-user industry, Food and Beverage commanded 54% of the China packaging market size in 2024; Healthcare and Pharmaceutical is forecast to grow at 7.14% CAGR during 2025-2030.

China Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth of e-commerce parcel volume | +1.8% | National, concentrated in Tier 1-2 cities | Short term (≤ 2 years) |

| Rising preference for sustainable paper-based formats | +1.2% | Global, strongest in coastal manufacturing hubs | Medium term (2-4 years) |

| Demand for convenience/RTD food packs | +0.9% | National, urban-centric adoption | Medium term (2-4 years) |

| Pharmaceutical cold-chain expansion | +0.7% | National, Beijing-Shanghai-Guangzhou corridor | Long term (≥ 4 years) |

| Smart-logistics (IoT) enabled track-and-trace packs | +0.5% | National, pilot programs in major cities | Long term (≥ 4 years) |

| Ultra-low-temperature bio-pharma packaging surge | +0.3% | National, concentrated in biotech clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of E-commerce Parcel Volume

The China packaging market is tightly linked to parcel throughput, which reached 175 billion units in 2024, driving unprecedented pressure on cushioning, tamper-evident seals and automated sorting compatibility. Fulfilment centres in Tier 1 cities now rely on AI routing systems that reduce dock-to-door lead-times by 35%, obliging converters to shorten run lengths without compromising structural integrity. Corrugated converters are investing in high-speed digital print lines that align barcodes and QR codes with logistics platforms, supporting last-mile traceability. Market participants adopting modular carton designs report double-digit reductions in void space, a priority as courier firms pivot toward volumetric pricing. These developments sustain the momentum of the China packaging market while rewarding converters able to integrate data carrier features directly into pack substrates.

Rising Preference for Sustainable Paper-Based Formats

China’s policy agenda prioritises recyclable inputs, prompting brand owners to favour fibre-based solutions across beverages, personal care and e-commerce mailers. The State Council’s eco-friendly delivery rules oblige retailers to offer in-store take-back facilities and publicly disclose packaging reduction metrics. Containerboard mills are shifting to higher-performance lightweight grades, helped by coating innovations that mitigate moisture ingress. Capacity expansions include Valmet’s OptiConcept M board line for Anhui Linping, scheduled online by end-2025 (EUR 40-60 million; USD 43-64 million). Fibre-based adoption also benefits from consumer recognition: nationwide surveys show 68% of shoppers prefer paper wrappers for online grocery deliveries when performance is comparable.

Demand for Convenience/RTD Food Packs

Retail sales of packaged foods are expected to reach 47 trillion yuan in 2025, underpinning sustained growth in aseptic cartons, stand-up pouches and microwavable trays. Ready-to-drink coffee, protein shakes and functional beverages demand oxygen-barrier laminates that extend shelf life while withstanding warehouse temperature swings. Tetra Pak’s Kunshan Development & Technology Center is re-engineering carton geometry to cut fibre use by 4% and facilitate local ink compatibility. To differentiate, brands incorporate freshness indicators calibrated for China’s cold-chain gaps; converters offering embedded time-temperature labels secure premium pricing and reinforce the growth trajectory of the China packaging market.

Pharmaceutical Cold-Chain Expansion

The pharmaceutical sector is on course to lift domestic drug spend to USD 110.97 billion by 2034, spurring specialised secondary and tertiary pack demand for biologics. Temperature-controlled parcel volumes are rising fastest along the Beijing–Shanghai–Guangzhou corridor where hospital networks centralise biologic inventory. Active thermal shippers equipped with phase-change material and data loggers safeguard payloads, meeting China’s upcoming food-contact adhesive standard GB 4806.15-2024. Biopharma customers stipulate carbon-footprint disclosures, compelling suppliers to certify recycled content in insulation panels. These dynamics cement pharma as a high-margin vertical within the China packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-ban and extended-producer-responsibility rules | -1.1% | National, stricter enforcement in major cities | Short term (≤ 2 years) |

| Volatile pulp and polymer feedstock costs | -0.8% | Global, acute impact on coastal manufacturing | Short term (≤ 2 years) |

| Patchy provincial recycling infrastructure | -0.4% | National, rural-urban infrastructure gaps | Medium term (2-4 years) |

| Reusable tote pilots eroding urban corrugated demand | -0.2% | Urban centers, logistics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastic-Ban and Extended-Producer-Responsibility Rules

China prohibits a widening list of single-use plastics in retail and courier channels, increasing compliance costs and accelerating material substitutions.[3]Circularise, “Navigating the Global Plastics Compliance Landscape,” circularise.com Producers must finance recycling systems under EPR, and the absence of uniform provincial enforcement complicates cost pass-through strategies. Brands face uncertainty over forthcoming recycled-content thresholds for PET and PP food-contact packs. Leading converters are hedging by building closed-loop paper systems; others form joint ventures with waste-management firms to secure feedstock. Until standards stabilise, capital allocation in the China packaging market skews toward retrofits rather than green-field polymer projects.

Volatile Pulp and Polymer Feedstock Costs

In 2024 China’s BPA nameplate capacity rose by 12.3% to 5.48 million tpa, depressing spot margins and triggering regional price swings that compress converter spreads. Polypropylene over-capacity similarly exerts downward price pressure, but rapid freight swings and FX volatility erode gains for flexible-film suppliers in eastern ports. Corrugators grapple with recovered-paper imports that fluctuate due to shipping disruptions. Strategic sourcing teams therefore combine futures hedging with dual-sourcing frameworks, though such measures cannot fully neutralise raw-material turbulence.

Segment Analysis

By Packaging Material: Paper Dominance Faces Bio-Innovation Challenge

Paper and Paperboard captured 43% of China packaging market share in 2024 as corrugated boxes underpinned e-commerce fulfilment and consumer confidence in fibre recyclability remained high. The segment benefits from China’s 96.48% PET beverage recycling milestone that shifts public attention to cellulose-based loops. Mill revamps are oriented toward high-strength light-weight grades, enabling shippers to meet express standard GB 43352-2023 dimensional and stacking tests. Concurrently, the China packaging market size for Paper and Paperboard is expected to rise in tandem with export-oriented corrugated demand growing at a mid-single-digit pace to 2030.

Other Materials—bio-based polymers, jute-blend films and lignin composites—record the fastest 7.21% CAGR, albeit from a low base. Academic breakthroughs reveal jute hybridisation delivering 24.42% fibre-yield gains, accelerating scale-up of moisture-resistant starch-jute liners. Lignin-bionanocomposites imbue antioxidant properties suitable for confectionery wraps, meeting demand for active packaging without synthetic additives. Investment hurdles linger—biopolymer cost parity remains elusive—but leading FMCG firms are piloting such materials, incentivised by EPR fee rebates.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Types of Packaging: Primary Leads While Tertiary Accelerates

Primary formats—cartons, bottles, blister packs—represent 70% of the China packaging market size and remain critical to product protection and shelf appeal. Food-safety expectations and QR-code traceability rules ensure persistent capital expenditure in high-speed filling lines and decoration technologies. The regulatory environment also requires tamper-proof seals for nutraceuticals, sustaining demand for multi-layer laminates.

Tertiary packaging grows at 6.03% CAGR as fulfilment centres automate palletising and cross-border e-commerce triples load-bearing requirements. Export couriers specify crush-proof, RFID-enabled pallets that feed real-time data to warehouse-management systems, creating an attractive profit pool. Market entrants offering composite pallet blocks made with recycled fibre and bio-resins shorten lead times for online retailers and reinforce the growth curve of the China packaging market.

By Packaging Format: Rigid Stability versus Flexible Innovation

Rigid formats—bottles, jars, drums—command 64% share, anchored in beverage and industrial chemicals. Lightweighting programs now shave up to 9% resin per bottle without compromising stacking performance, supporting converter margins under raw-material price volatility. Glass container manufacturers strengthen value propositions through oxygen-absorbing closures, protecting premium craft beverages.

Conversely, flexible media expand at 6.79% CAGR, supported by demand for stand-up pouches in sauces and pet food. Flexible laminates cut transport emissions by up to 70% compared with cans, a feature highlighted by marketing teams in metropolitan supermarkets. The China packaging market size for Flexible Packaging is projected to expand steadily as major CPGs switch to mono-material PE films to meet recyclability guidelines. Equipment suppliers exploit this shift by launching turret-style pouch lines capable of 220 packs per minute, catering to high-throughput snack brands.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Healthcare Surge Challenges F&B Dominance

Food and Beverage sustains a 54% revenue share, leveraging China’s massive urbanised middle class. Ready-meal and RTD beverage penetration rises alongside dual-income households, giving impetus to oxygen-barrier trays and aseptic cartons. Brands stamp QR codes onto outer sleeves to convey provenance and recycling instructions, reinforcing consumer trust.

Healthcare and Pharmaceutical grows fastest at 7.14% CAGR, catalysed by biologics demand and hospital procurement reforms. Secondary pack specifications now include tamper-evident seals and serialization mandated by the National Medical Products Administration. The China packaging market size for cold-chain vials is forecast to accelerate as mRNA vaccine trials progress to late-stage testing. Materials innovators developing recyclable insulated shippers find willing partners among speciality logistics firms, supporting circular-economy goals.

Geography Analysis

Coastal provinces anchor 73% of value-added packaging output in the China packaging market. Guangdong dominates flexible-film extrusion thanks to electronics clustering and access to Shenzhen–Hong Kong cross-border logistics. Converter density lets brand owners compress lead-times to less than three days for promotional snack launches. Adjacent Jiangsu and Zhejiang provinces form the Yangtze River Delta corridor, housing the highest concentration of multinational converters and automation vendors. Shanghai’s free-trade zones facilitate import of precision forming dies, enhancing local production sophistication. Government incentives further encourage smart-factory retrofits, making the corridor a test-bed for IoT-enabled tertiary packs.

Shandong emerges as a chemical feedstock hub with >20% share of national BPA output, giving regional converters raw-material cost advantages. Large board mills integrate captive power to counter grid volatility, ensuring stable corrugating medium supply for export-oriented SMEs. Provincial authorities co-invest in inland dry ports that link to Qingdao’s seaport, trimming transit times for agricultural exports wrapped in ventilated cartons.

Central and western regions scale rapidly as labour costs remain lower than coastal counterparts. Chengdu and Chongqing industrial parks attract beverage bottlers that in turn create anchor demand for PET preform suppliers. High-speed rail corridors reduce long-haul freight charges, allowing brand owners to base filling operations inland yet still serve eastern seaboard retailers within 48 hours. Cross-border e-commerce hubs in Guangxi and Yunnan provide new outlets for certified corrugated boxes that meet ASEAN phytosanitary rules. Such geographic diversification cushions the China packaging market against coastal wage inflation and port congestion.

Competitive Landscape

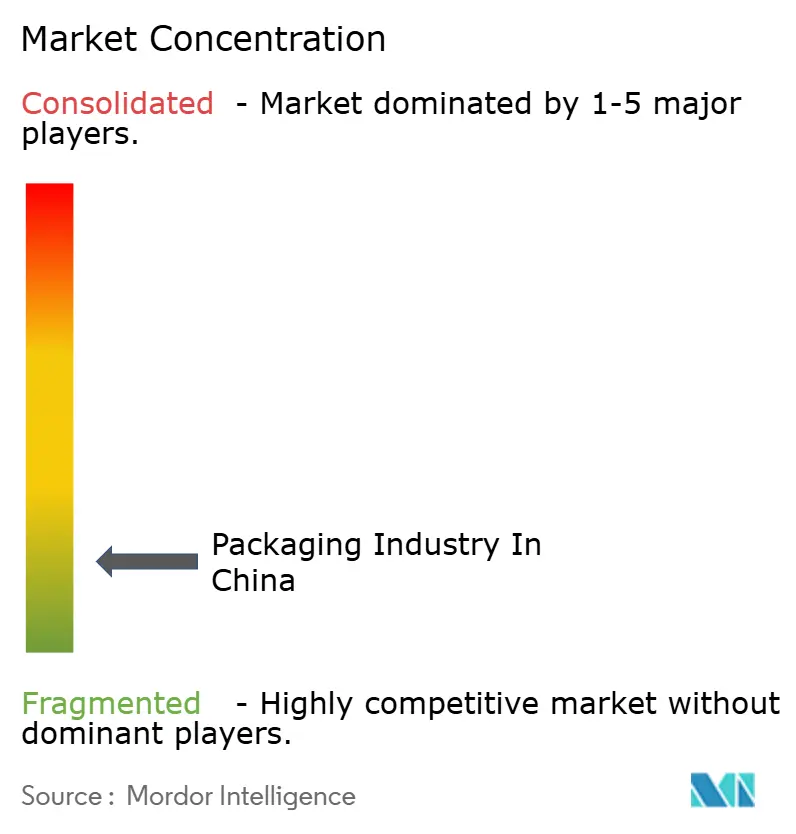

The competitive structure of the China packaging market is moderately fragmented, with the top five players controlling under 30% of revenue. Nine Dragons Paper and Lee & Man Paper dominate paper grades through integrated pulping and corrugating capacity, yielding logistics synergies that defend margins. Amcor’s 2025 merger with Berry Global creates a USD 27 billion entity that immediately lifts scale in healthcare and pet-food laminates; management targets USD 650 million cost synergies by network rationalisation. International Paper’s acquisition of DS Smith extends its foothold in lightweight corrugated, complementing China plant refurbishments designed around energy-recovery systems.

Technology investments serve as a key moat. Smurfit Westrock’s deployment of biomass boilers and AI-driven converting lines is expected to lower carbon intensity by 15% while cutting per-tonne energy spend. Domestic mid-tiers counter by adopting high-speed rotary die-cutters capable of print-to-pack in a single pass, shrinking order-to-delivery cycles for online brands. RFID deployment is another battleground; McDonald’s China and Cainiao’s partnership trims retail stock-takes from 60 minutes to 15 minutes and sets a benchmark for quick-service chains.

Strategic moves also target bio-based opportunities. Paper majors sign MOUs with agri-residue suppliers to co-process straw pulp, mitigating pulp price swings. Flexible specialists pilot mono-material pouches that comply with new recyclate protocols. Start-ups in Hangzhou focus on lignin composite masterbatch, raising series-A rounds from brand owners keen on scope-3 emission cuts. The dynamic interplay between scale, innovation and compliance sets the tempo for future consolidation within the China packaging market.

China Packaging Industry Leaders

-

Sealed Air Corporation

-

Wuxi Huatai Co.,Ltd

-

Berry Global Group, Inc.

-

Amcor Plc

-

Zhejiang Xinlei Packaging Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Smurfit Westrock reported USD 7.656 billion net sales for Q1 2025 and announced >500,000 tpa paper capacity closures in North America while commissioning a biomass boiler in Colombia to optimise global cost positioning.

- April 2025: Amcor finalised its merger with Berry Global, forecasting USD 650 million annual synergies and 12% EPS growth by 2026.

- February 2025: Shareholders of Amcor and Berry Global approved the merger, exchanging 7.25 Amcor shares for each Berry share to consolidate positions in healthcare and food-service laminates.

- October 2024: Valmet secured a EUR 40-60 million (USD 43-64 million) order to supply an OptiConcept M board line to Anhui Linping, start-up due end-2025.

China Packaging Market Report Scope

Packaging is the process of enclosing or protecting products using containers to facilitate distribution, identification, storage, promotion, and use. The packaging industry in China is showing growth trends across various end-user industries, driven by increasing urbanization, rising disposable incomes, and changing consumer preferences. Chinese packaging manufacturers are investing in innovative technologies to meet the evolving demands of both domestic and international markets. The food and beverage, e-commerce, and healthcare sectors mainly contribute to the expansion of China's packaging industry.

The packaging industry in China is segmented by type of packaging material (plastic, paper, glass, metal, and other packaging materials), type of packaging (primary packaging, secondary packaging, and tertiary packaging), and end-user industry (food and beverage, healthcare and pharmaceutical, beauty and personal care, industrial, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Packaging Material

| Plastic |

| Paper and Paperboard |

| Glass |

| Metal |

| Other Materials |

By Types of Packaging

| Primary Packaging |

| Secondary Packaging |

| Tertiary Packaging |

By Packaging Format

| Rigid Packaging |

| Flexible Packaging |

By End-user Industry

| Food and Beverages |

| Healthcare and Pharmaceutical |

| Beauty and Personal Care |

| Industrial |

| Other End-user Industries |

| By Packaging Material | Plastic |

| Paper and Paperboard | |

| Glass | |

| Metal | |

| Other Materials | |

| By Types of Packaging | Primary Packaging |

| Secondary Packaging | |

| Tertiary Packaging | |

| By Packaging Format | Rigid Packaging |

| Flexible Packaging | |

| By End-user Industry | Food and Beverages |

| Healthcare and Pharmaceutical | |

| Beauty and Personal Care | |

| Industrial | |

| Other End-user Industries |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the China packaging market?

The China packaging market stands at USD 218.37 billion in 2025 and is projected to reach USD 278.15 billion by 2030, growing at a 4.96% CAGR.

Which packaging material holds the largest share?

Paper and Paperboard leads with 43% revenue share in 2024, driven by robust e-commerce and export shipments.

Which end-user vertical is growing fastest?

Healthcare and Pharmaceutical packaging is expanding at a 7.14% CAGR, supported by biologics demand and cold-chain investments.

How are regulations shaping packaging choices in China?

Mandatory express standards and plastic-reduction rules are steering brand owners toward recyclable fibre-based formats and mono-material plastics.

What strategic benefits arise from the Amcor–Berry Global merger?

The merger creates a USD 27 billion packaging entity targeting USD 650 million cost synergies and strengthened positions in healthcare, pet-food and food-service laminates.

Why is tertiary packaging gaining momentum?

Warehouse automation and cross-border e-commerce are driving a 6.03% CAGR in tertiary packaging as brands adopt stronger, RFID-ready pallet solutions to cut damage and improve traceability.

Page last updated on: