Market Size of Oxygen Free Copper Industry

| Study Period | 2019 - 2029 |

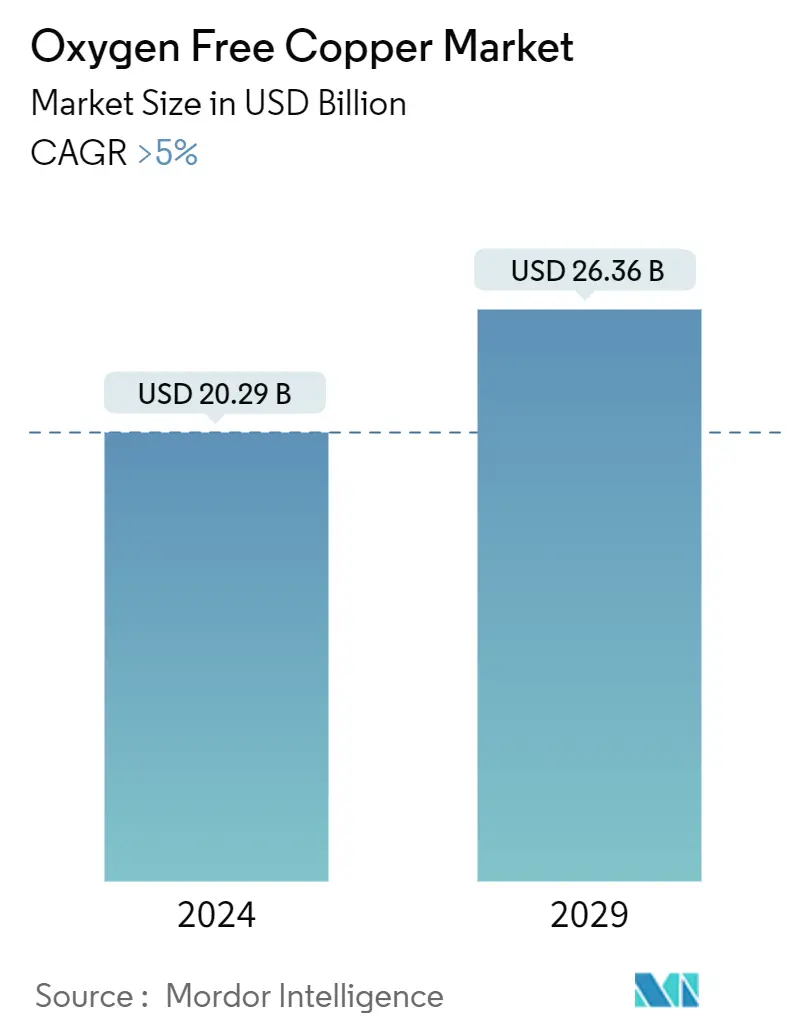

| Market Size (2024) | USD 20.29 Billion |

| Market Size (2029) | USD 26.36 Billion |

| CAGR (2024 - 2029) | > 5.00 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Oxygen Free Copper Market Analysis

The Oxygen Free Copper Market size is estimated at USD 20.29 billion in 2024, and is expected to reach USD 26.36 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The oxygen-free copper market is gaining traction due to its superior electrical conductivity and high purity, which are essential for various high-performance applications. This type of copper is particularly valued in industries where the highest levels of electrical conductivity and resistance to corrosion are critical, such as electronics, automotive, and industrial sectors. As these industries continue to advance technologically, the demand for high-purity copper with low oxygen content is increasing. This demand is especially strong in the semiconductor and automotive sectors, where oxygen-free copper plays a crucial role in enhancing the performance and reliability of components.

Advantages of Oxygen-Free Copper in High-Performance Applications

- Superior Electrical Properties: Oxygen-free copper (OFC) is renowned for its excellent electrical properties, which surpass those of standard electrolytic tough pitch (ETP) copper. Its production involves controlled processes to ensure minimal oxygen content, resulting in high conductivity and the elimination of oxide inclusions that can cause defects in the final product. This makes it the preferred material for applications where precision and reliability are paramount, such as high-frequency electronics, high-end audio equipment, and critical automotive components.

- Role in Emerging Technologies: The market for oxygen-free copper is also driven by its applications in emerging technologies. As global demand for electric vehicles (EVs) and renewable energy systems grows, the use of oxygen-free copper in these applications is expected to rise. This is due to the copper's high conductivity and thermal performance, which are essential for improving the efficiency and performance of EVs and other advanced electronic systems.

Rising Need for High-Purity Copper in Semiconductors

- Semiconductor Industry Demand: The semiconductor industry is a significant driver of the oxygen-free copper market. OFC’s high conductivity and purity are critical for the manufacturing of semiconductor devices, which require materials with minimal impurities to ensure optimal performance. The increasing complexity and miniaturization of semiconductor devices have further amplified the demand for high-quality materials like OFC. As manufacturers push the limits of technology, the need for materials that offer superior performance and reliability becomes paramount.

- Impact of Technological Advancements: Additionally, the ongoing expansion of data centers and the advent of 5G technology are fueling the demand for semiconductors, thereby indirectly boosting the need for oxygen-free copper. These applications require materials that can handle high data transfer rates and operate efficiently under demanding conditions, further solidifying the role of oxygen-free copper in the semiconductor industry.

Expanding Use of Oxygen-Free Copper in Automotive Applications

- Growth in Electric Vehicles: The automotive sector is another significant contributor to the growing demand for oxygen-free copper. As the industry shifts towards electrification, the use of OFC in electric vehicles (EVs) and hybrid electric vehicles (HEVs) is increasing. OFC is used in various automotive components, including wiring, connectors, and battery systems, where its high conductivity and resistance to corrosion are crucial for ensuring efficiency and reliability.

- Advanced Automotive Technologies: With the global push towards reducing carbon emissions, automakers are investing heavily in EVs, which require materials that can handle higher electrical loads while maintaining performance. Moreover, the focus on advanced driver-assistance systems (ADAS) and autonomous driving technologies is further driving the demand for oxygen-free copper. These systems rely on complex electronic architectures that require materials with excellent conductivity and thermal management properties, making OFC a key material in developing next-generation automotive technologies.

Oxygen Free Copper Industry Segmentation

Oxygen-free copper is a category of highly conductive wrought copper alloys that have been electrolytically optimized to minimize oxygen levels to or below 0.001 percent. Oxygen-free copper is a grade of copper that has a high level of conductivity and is virtually free from oxygen content. Oxygen-free copper is used in several applications, such as in the manufacturing of semiconductors, superconductor components, and others.

The Oxygen Free Copper Market is Segmented by Grade (CU-OF and CU-OFE), Product (Wires, Strips, Busbars and Rods, and Other Products), End-user Industry (Electrical and Electronics, Automotive, Industrial, and Other End-user Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Report Offers Market Size and Forecasts for the Oxygen-Free Copper Market in Value (USD) for all the Above Segments.

| Grade | |

| CU-OF | |

| CU-OFE |

| Product | |

| Wires | |

| Strips | |

| Busbars and Rods | |

| Other Products (Tubes and Pipes, Etc.) |

| End-user Industry | |

| Electrical and Electronics | |

| Automotive | |

| Industrial | |

| Other End-user Industries (Power Generation, Aerospace, Etc.) |

| Geography | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

Oxygen Free Copper Market Size Summary

The oxygen-free copper market is poised for significant growth, driven by its increasing demand in the semiconductor industry and its critical applications in electronics. The market, which experienced a downturn due to the COVID-19 pandemic, has rebounded to pre-pandemic levels and is expected to continue its upward trajectory. The electrical and electronics sector remains the dominant segment, with oxygen-free copper being essential in the manufacturing of semiconductors, superconductors, and high-vacuum systems. Its purity is crucial in preventing unwanted chemical reactions, making it indispensable in applications such as printed circuit boards, microwave tubes, and vacuum capacitors. The proliferation of electronic devices globally, including smartphones and smart devices, is further propelling the demand for oxygen-free copper.

The Asia-Pacific region is anticipated to be the largest and fastest-growing market for oxygen-free copper, fueled by the burgeoning demand for electronic semiconductor devices in countries like China, Japan, and India. The region's robust industrial and energy sectors, coupled with its leading position in consumer electronics production, are key contributors to this growth. China's dominance in coal-fired power generation and its substantial share in global consumer electronics production underscore the region's significance in the oxygen-free copper market. The fragmented nature of the market sees major players like Copper Braid Products, Mitsubishi Materials Corporation, and Aviva Metals actively participating, with strategic moves such as acquisitions enhancing their market positions.

Oxygen Free Copper Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Drivers

-

1.1.1 Increasing Demand from Semiconductor

-

1.1.2 Increasing Demand from Automotive Sector

-

1.1.3 Other Drivers

-

-

1.2 Restraints

-

1.2.1 High Cost of Copper

-

1.2.2 Other Restraints

-

-

1.3 Industry Value Chain Analysis

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Degree of Competition

-

-

-

2. MARKET SEGMENTATION (Market Size in Value)

-

2.1 Grade

-

2.1.1 CU-OF

-

2.1.2 CU-OFE

-

-

2.2 Product

-

2.2.1 Wires

-

2.2.2 Strips

-

2.2.3 Busbars and Rods

-

2.2.4 Other Products (Tubes and Pipes, Etc.)

-

-

2.3 End-user Industry

-

2.3.1 Electrical and Electronics

-

2.3.2 Automotive

-

2.3.3 Industrial

-

2.3.4 Other End-user Industries (Power Generation, Aerospace, Etc.)

-

-

2.4 Geography

-

2.4.1 Asia-Pacific

-

2.4.1.1 China

-

2.4.1.2 India

-

2.4.1.3 Japan

-

2.4.1.4 South Korea

-

2.4.1.5 Malaysia

-

2.4.1.6 Thailand

-

2.4.1.7 Indonesia

-

2.4.1.8 Vietnam

-

2.4.1.9 Rest of Asia-Pacific

-

-

2.4.2 North America

-

2.4.2.1 United States

-

2.4.2.2 Canada

-

2.4.2.3 Mexico

-

-

2.4.3 Europe

-

2.4.3.1 Germany

-

2.4.3.2 United Kingdom

-

2.4.3.3 France

-

2.4.3.4 Italy

-

2.4.3.5 Spain

-

2.4.3.6 NORDIC Countries

-

2.4.3.7 Turkey

-

2.4.3.8 Russia

-

2.4.3.9 Rest of Europe

-

-

2.4.4 South America

-

2.4.4.1 Brazil

-

2.4.4.2 Argentina

-

2.4.4.3 Colombia

-

2.4.4.4 Rest of South America

-

-

2.4.5 Middle-East and Africa

-

2.4.5.1 Saudi Arabia

-

2.4.5.2 South Africa

-

2.4.5.3 Nigeria

-

2.4.5.4 Qatar

-

2.4.5.5 Egypt

-

2.4.5.6 UAE

-

2.4.5.7 Rest of Middle-East and Africa

-

-

-

Oxygen Free Copper Market Size FAQs

How big is the Oxygen Free Copper Market?

The Oxygen Free Copper Market size is expected to reach USD 20.29 billion in 2024 and grow at a CAGR of greater than 5% to reach USD 26.36 billion by 2029.

What is the current Oxygen Free Copper Market size?

In 2024, the Oxygen Free Copper Market size is expected to reach USD 20.29 billion.