Osteoporosis Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

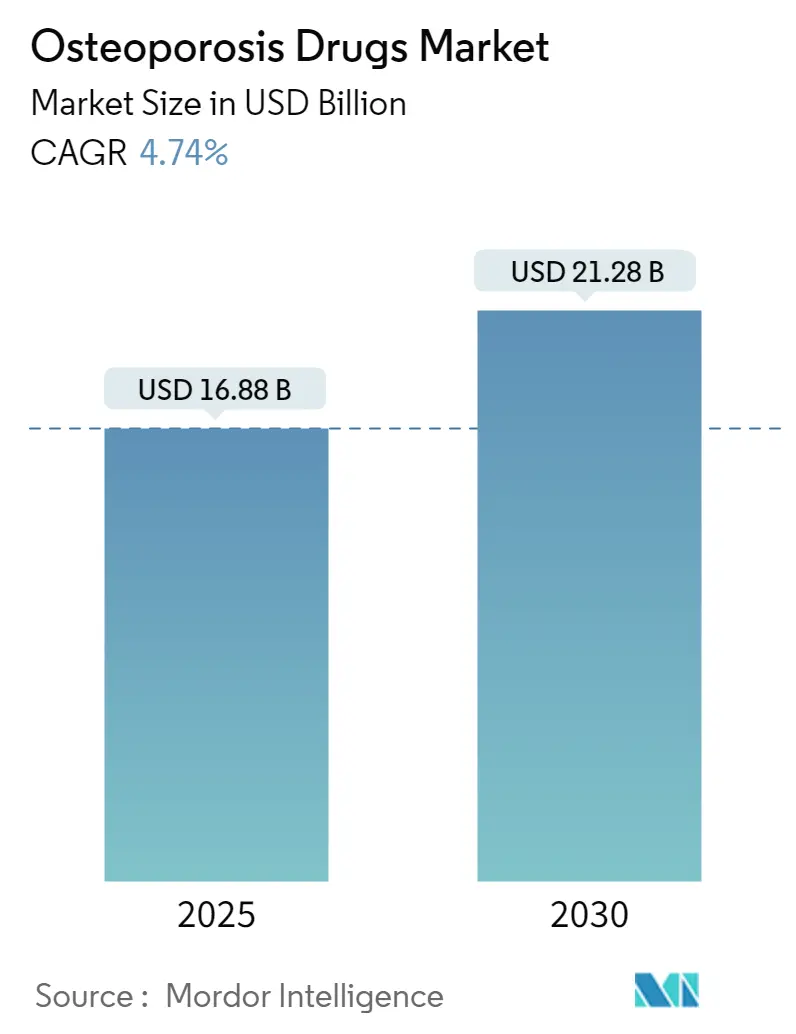

| Market Size (2025) | USD 16.88 Billion |

| Market Size (2030) | USD 21.28 Billion |

| Growth Rate (2025 - 2030) | 4.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

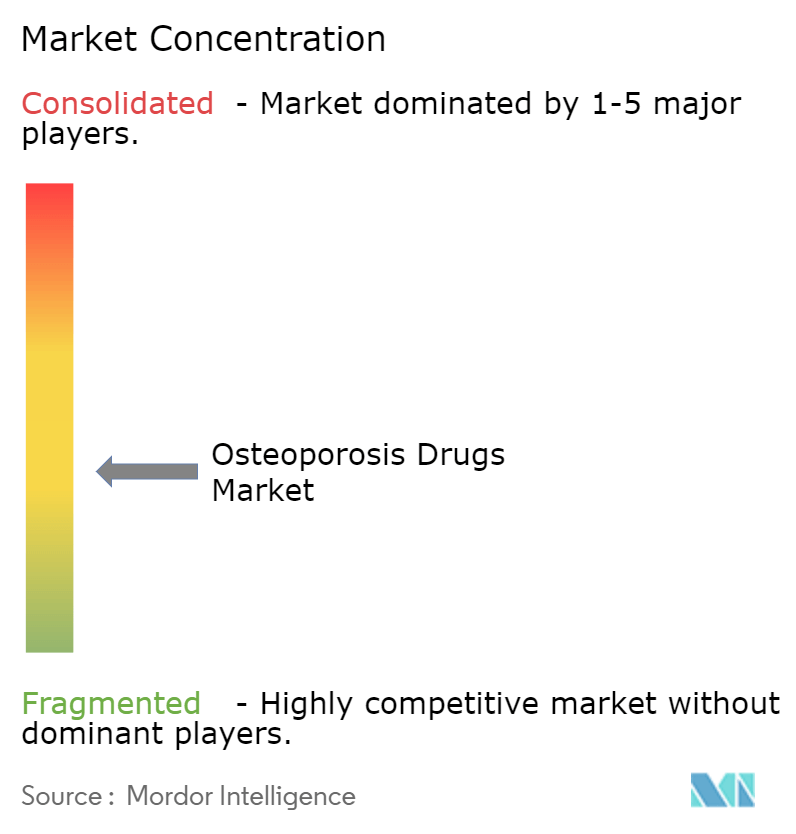

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Osteoporosis Drugs Market Analysis by Mordor Intelligence

The osteoporosis drugs market generated USD 16.88 billion in 2025 and is forecast to advance at a 4.74% CAGR to reach USD 21.28 billion by 2030. The trajectory shows a disciplined shift from low-priced bisphosphonates toward premium biologics and bone-building anabolic agents that promise faster fracture-risk reduction. Population aging, rising life expectancy, and earlier diagnosis—bolstered by opportunistic AI screening—continue to expand the treated patient pool. Reimbursement reforms that tie therapy to national fracture registries are speeding time-to-treatment, while real-world evidence pathways shorten product-approval cycles. Biosimilar launches following the denosumab patent cliff will add price competition yet simultaneously enlarge the osteoporosis drugs market by improving affordability.

Key Report Takeaways

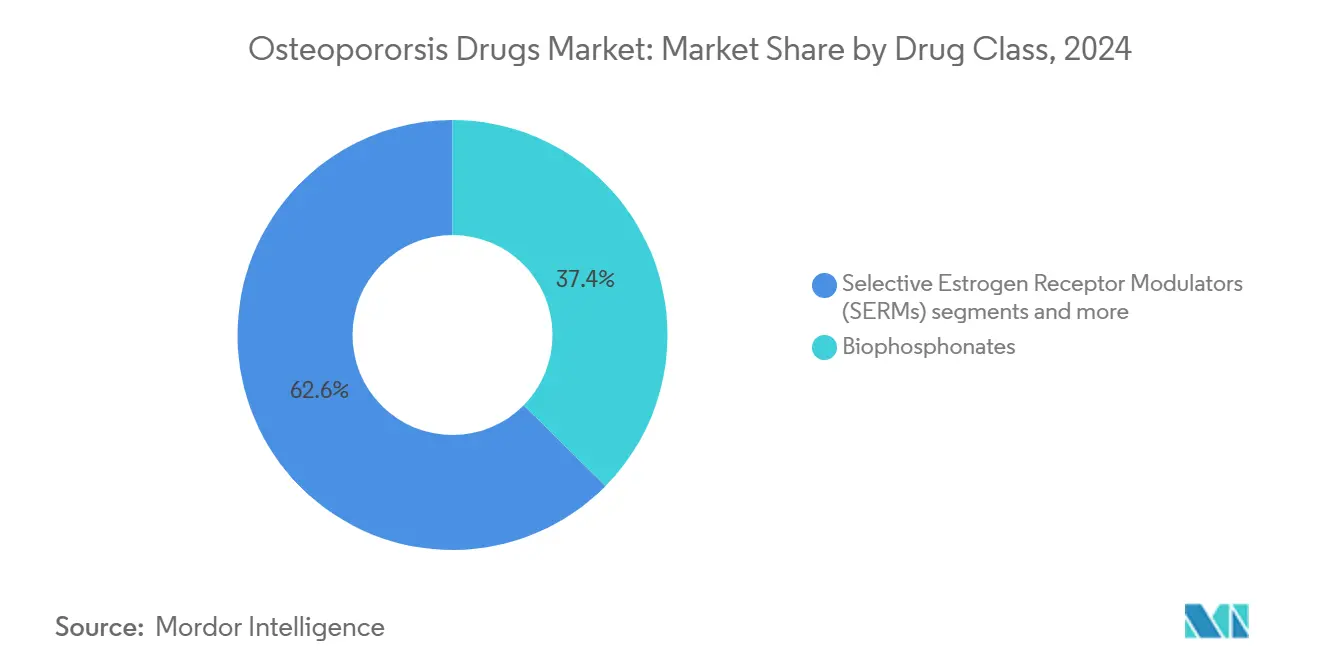

- By drug class, bisphosphonates led with 37.40% osteoporosis drugs market share in 2024; sclerostin inhibitors are projected to grow the fastest at a 5.23% CAGR to 2030.

- By route of administration, oral formulations held 65.60% of the osteoporosis drugs market size in 2024, whereas injectables are set to expand at a 5.89% CAGR through 2030.

- By distribution channel, retail pharmacies captured 47.35% revenue share in 2024; online pharmacies are forecast to record the highest 6.01% CAGR to 2030.

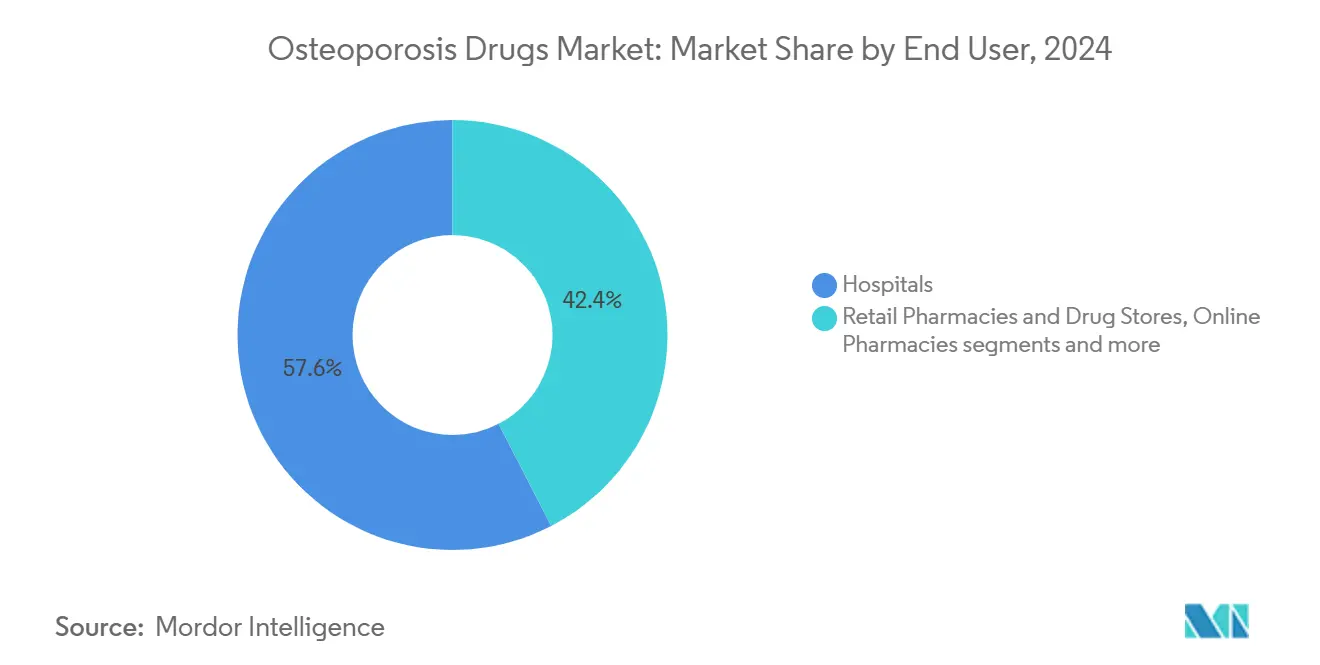

- By end user, hospitals accounted for 57.60% of the osteoporosis drugs market size in 2024, while home-care settings will advance most quickly at a 6.34% CAGR.

- By geography, North America accounted for 39.87% of the osteoporosis drugs market size in 2024, while Asia-Pacific will advance most quickly at a 7.01% CAGR.

Global Osteoporosis Drugs Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & fracture-risk burden | +1.80% | Global; highest in Japan, Germany, Italy | Long term (≥ 4 years) |

| Rising adoption of anabolic agents | +1.20% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Surge in monoclonal antibody use | +0.90% | Global, led by developed markets | Medium term (2-4 years) |

| AI-enabled primary-care fracture-risk screening | +0.60% | North America & EU, pilot programs in APAC | Short term (≤ 2 years) |

| National osteoporosis registries | +0.40% | EU, Canada, spreading to Asia-Pacific | Medium term (2-4 years) |

| microRNA-based pipelines | +0.30% | R&D hubs in United States & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Fracture-Risk Burden

Individuals aged 50 and above constitute the dominant risk group, and annual osteoporotic fractures are expected to reach 6.3 million by 2050, with Asia-Pacific carrying most of the future caseload. Hip-fracture mortality runs at 20% within 12 months, spurring demand for therapies that act quickly to rebuild bone and avert secondary fractures. In Japan, bone-density testing rates remain only 14% in rural hospitals despite 41% osteoporosis diagnoses, underscoring the diagnostic gap. Medicare spent USD 5.7 billion on fracture care for 1.8 million beneficiaries in 2016, and 80% of post-fracture patients still went untreated, highlighting cost pressures to expand access. These demographic forces cement a multi-year demand floor for every drugs class within the osteoporosis drugs market.

Rising Adoption of Anabolic Agents

Anabolic drugs such as teriparatide and abaloparatide achieve vertebral-fracture reductions of 65% and 86%, respectively, outperforming antiresorptives and attracting premium reimbursement medpagetoday.com. The FDA’s 2024 expansion of abaloparatide to treat male patients increased the addressable pool by 12% in the United States managedhealthcareexecutive.com. Sequential regimens that start with romosozumab then transition to denosumab preserve fracture-risk reductions over five years ucb.com. Japanese real-world evidence confirms that high-risk cohorts receive romosozumab with cardiovascular monitoring, signifying clinical trust despite label warnings springer.com. Stronger insurance coverage and updated guidelines legitimize the anabolic first-line approach, enriching the osteoporosis drugs market.

Surge in Monoclonal Antibody Use

Denosumab’s RANKL blockade produces fracture-risk reductions of 68% (vertebral) and 40% (hip) over three years, and 10-year data show lasting bone-density gains without new safety issues. Romosozumab complements this efficacy by stimulating formation while restricting resorption; 73% fewer new vertebral fractures emerged within 12 months of treatment start. With denosumab’s main US patent expiring in February 2025, Sandoz, Samsung Bioepis, and Celltrion have introduced interchangeable biosimilars priced 20-30% lower, broadening patient access. Although price pressure may slow revenue per script, the lower cost base can enlarge treated volumes, reinforcing overall growth for the osteoporosis drugs market.

AI-Enabled Primary-Care Fracture-Risk Screening

Deep-learning software now detects low bone mineral density on incidental foot radiographs with 89.89% accuracy and an AUC of 0.94, removing the bottleneck of scarce DXA scanners. Machine-learning algorithms that ingest demographic and lifestyle data reach AUCs of 0.848, outperforming legacy risk calculators frontiersin.org. Automated CT-based quantification captures osteoporotic cases missed by DXA, especially in patients with spinal degeneration nature.com. The XGB algorithm surpasses the Osteoporosis Self-Assessment Tool in Tibetan cohorts, indicating the need for ethnicity-specific screening models. Earlier detection shifts many patients into therapy sooner, feeding incremental demand across every segment of the osteoporosis drugs market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse effects & poor long-term compliance | -1.10% | Global; highest in elderly populations | Medium term (2-4 years) |

| Patent expiries triggering generic erosion | -0.80% | North America & EU, spreading globally | Short term (≤ 2 years) |

| Cold-chain dependency for biologics | -0.50% | Emerging markets in APAC, MEA, Latin America | Medium term (2-4 years) |

| Stringent post-marketing safety for sclerostin inhibitors | -0.40% | Global, with toughest rules in United States & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse Effects & Poor Long-Term Compliance

Average medication-possession ratios sit at only 61.9% after two years, and abrupt denosumab discontinuation triggers rebound bone resorption with a 20% higher fracture risk. Denosumab also shows hypocalcemia and dermatologic safety signals clustering in the first 30 days of use. Romosozumab carries boxed warnings for myocardial infarction and stroke; 0.8% of treated subjects experienced MI versus 0.3% on alendronate drugs.com. Bisphosphonate non-adherence still averages 23.3% in Japan despite monthly or quarterly dosing options. These compliance gaps shave growth from the osteoporosis drugs market, particularly in oral segments.

Patent Expiries Triggering Generic Erosion

The denosumab cliff in 2025 opened a USD 3.8 billion revenue pool to biosimilars, with Sandoz’s Jubbonti and Samsung Bioepis’ Ospomyv reaching U.S. shelves on May 31, 2025 under settlement terms. Romosozumab patents lapse in 2026, though method claims last to 2033, delaying full erosion. Generic alendronate already undercuts branded pricing by up to 80% while demonstrating comparable fracture-prevention efficacy. Lower prices can lift volumes but temper overall revenue expansion, especially in the osteoporosis drugs market’s mature regions.

Segment Analysis

By Drug Class: Biologics Reshape Traditional Hierarchies

Bisphosphonates retained a 37.40% osteoporosis drugs market share in 2024, yet growth slowed to less than 1% annually as payers and physicians pivoted toward higher-value options. Sclerostin inhibitors, chiefly romosozumab, exhibited the fastest 5.23% CAGR as clinicians prioritized rapid bone-formation gains for severe-risk patients. RANKL inhibitors, anchored by denosumab, remained the top-selling biologic because six-month dosing supports adherence.

Selective estrogen receptor modulators held niche roles for women unable to tolerate bisphosphonates, while parathyroid hormone analogues served as bridge therapy before antiresorptive maintenance. Pipeline attention shifted to microRNA modulators and Wnt-signaling activators that promise dual bone-building and resorption-control profiles. Declining calcitonin use, owing to questionable efficacy, shortened product life-cycles and redirected R&D budgets toward next-generation biologics that can lengthen treatment duration and sustain the osteoporosis drugs market’s value proposition.

Note: Segment shares of all individual segments available upon report purchase

By Route of Administration: Injectable Growth Accelerates

Oral drugs still composed 65.60% of 2024 revenue because of generic alendronate’s ubiquity, but injectables expanded at a 5.89% CAGR, reflecting biologic uptake. Denosumab’s twice-yearly subcutaneous dosing and romosozumab’s monthly regimen improved adherence relative to daily pills, particularly among elderly patients managing polypharmacy.

Home-health nurses and self-injection pens reduced hospital visits, while Medicare coverage for in-home injections lowered out-of-pocket costs. Intravenous zoledronic acid maintained relevance for patients seeking once-yearly dosing, yet its usage faced stiff rivalry from subcutaneous biologics. Research into hydrogel micro-depots that release anabolic peptides over 12 weeks could further tilt preferences toward minimally invasive delivery. Cold-chain logistics remained a bottleneck in emerging markets, but investment in passive shipping containers and pharmacy-grade refrigerators is narrowing the gap, unlocking new provincial sales for the osteoporosis drugs market.

By Distribution Channel: Digital Transformation Accelerates

Retail pharmacies commanded 47.35% revenue in 2024 as the primary refill point for oral bisphosphonates. Yet online and specialty pharmacies, aided by telemedicine, clocked 6.01% CAGR by automating refills, counseling, and reimbursement paperwork for high-priced biologics. Hospital pharmacies retained control over initial injectable dosing and medication teaching.

Specialty pharmacies embedded AI adherence dashboards that flag missed doses and trigger pharmacist outreach, lifting refill compliance by 11 percentage points year on year. Drug-store chains in rural locations filled a critical access niche, often partnering with tele-endocrinology hubs that prescribe anabolic starters before routing follow-up doses locally. This hybrid model smooths patient journeys and funnels incremental scripts into the osteoporosis drugs market.

By End User: Home-Care Expansion Reshapes Delivery

Hospitals contributed 57.60% of 2024 revenues owing to acute fracture management and initiation of complex regimens, while home care marked the swiftest 6.34% CAGR. Clinics offered ongoing monitoring, yet remote-monitoring wearables such as Osteoboost redirected selected osteopenia cases entirely out of bricks-and-mortar settings.

By 2025, the osteoporosis drugs market size attached to home-care patients stood at USD 3.21 billion and is set to reach USD 4.39 billion by 2030 thanks to expanded reimbursement for nurse-administered injections and digital follow-ups. Research institutes sustained their role in phase 2/3 trials, granting early access to pipeline agents under expanded-access protocols. The home-care trend promises durable volume growth as patient lifestyle preferences mesh with payer incentives to curtail hospital readmissions, reshaping end-user economics across the osteoporosis drugs market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America preserved its 39.87% revenue share in 2024, anchored by broad insurance coverage, specialty pharmacist networks, and quick uptake of newly approved agents. The Centers for Medicare & Medicaid Services added osteoporosis to its 2025 Medication Therapy Management core list, which is expected to raise adherence and push additional refills into the osteoporosis drugs market[2]Source: A. Patel et al., “Generic Alendronate in Osteoporosis,” dovepress.com . Canada’s mandatory fracture registries began linking treatment reimbursement to guideline adherence, improving first-dose capture within 90 days of index fracture.

Asia-Pacific recorded the fastest 7.01% CAGR and is projected to overtake Europe in annual treatment volumes by 2029. Japan’s universal coverage reimburses every approved osteoporosis regimen, yet under-diagnosis in rural prefectures leaves a latent cohort untapped. China’s tertiary-hospital data show denosumab usage rising 78% year on year, supported by inclusion in the 2024 National Reimbursement Drug List. India’s private-sector hospitals introduced bundled fracture-prevention packages that incorporate romosozumab starter doses, suggesting future tailwinds for the osteoporosis drugs market.

Europe remains a stable yet price-sensitive region. The European Medicines Agency now accepts real-world evidence for line-extensions, as seen in abaloparatide’s 2024 authorization based on post-marketing data. National health technology assessment bodies negotiate steep discounts—up to 25%—for biologics entering regional formularies, restraining revenue growth but widening patient access. South America and the Middle East & Africa still account for single-digit shares yet post healthy mid-single-digit CAGRs as public-sector screening programs ramp and global NGOs subsidize bisphosphonate supplies. Improved cold-chain corridors are beginning to unlock biologic penetration, seeding long-term expansion for the osteoporosis drugs market.

Competitive Landscape

The market shows moderate concentration: the top five manufacturers controlled 53% of 2024 sales. Amgen leverages 20 years of denosumab data and recently launched a digital companion app that schedules home-injection reminders. Eli Lilly capitalizes on abaloparatide’s expanded male indication and co-promotes teriparatide with generic partners to defend share ahead of next-gen anabolic entrants. UCB positions romosozumab as a first-year induction therapy before transitioning patients to antiresorptives, creating a lifecycle management moat. Novartis maintains a legacy bisphosphonate line and incubates early-stage Wnt modulators acquired via its 2024 PeakRadius acquisition.

Biosimilar makers Sandoz, Samsung Bioepis, Celltrion, and Organon orchestrated synchronized denosumab launches in mid-2025, pricing 22% below the originator yet offering white-glove specialty-pharmacy support to capture switchers quickly. Alvotech and Dr. Reddy’s plan a 2026 follow-on entrant, aiming at 15% U.S. share within three years through hospital discount contracts. Technology partnerships add competitive complexity: Henlius supplies drug substance for Organon’s global filings, and Bone Health Technologies collaborates with Kaiser Permanente to integrate Osteoboost adherence data into electronic medical records.

Differentiation increasingly hinges on care-ecosystem build-out rather than molecule alone. Players are investing in AI fracture-risk algorithms, remote densitometry devices, and real-world-evidence dashboards that satisfy regulators while reinforcing brand loyalty. Start-ups exploring microRNA anabolic therapies may offer in-licensing targets by 2028, suggesting a continual refresh cycle that keeps the osteoporosis drugs market dynamic.

Osteoporosis Drugs Industry Leaders

-

Amgen Inc.

-

Eli Lily and Company

-

F. Hoffmann La Roche

-

Merck & Co. Inc.

-

Pfizer Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Osteoboost Health launched the first FDA-cleared prescription wearable device for low bone density treatment, opening a non-drug adjunct pathway for 60 million Americans with osteopenia.

- February 2025: Celltrion received FDA clearance for interchangeable denosumab biosimilars Stoboclo and Osenvelt, slated for June 2025 launch.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the osteoporosis drugs market as all prescription pharmacologic agents, antiresorptives and anabolics, that are clinically approved to slow bone loss, build new bone, or cut fracture risk in osteoporotic patients across inpatient and outpatient settings.

Scope exclusion: Nutraceutical supplements, calcium-vitamin combinations sold as OTC, and bone-graft orthobiologics are not included in Mordor's value base.

Segmentation Overview

- By Drug Class (Value)

- Bisphosphonates

- Selective Estrogen Receptor Modulators (SERMs)

- Parathyroid Hormone Analogues

- RANK Ligand Inhibitors

- Calcitonin

- Sclerostin Inhibitors

- Others

- By Route of Administration (Value)

- Oral

- Injectable

- Intravenous

- By Distribution Channel (Value)

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- Online Pharmacies

- By End User (Value)

- Hospitals

- Clinics

- Home-care Settings

- Research Institutes

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed endocrinologists, hospital pharmacy buyers, and wholesalers across North America, Europe, and high-growth Asia-Pacific markets. Conversations clarified real-world treatment adherence, generic switch rates, and emerging biologic uptake, letting us reconcile desk findings and fine-tune country-level assumptions.

Desk Research

We start with open-access pillars such as WHO fracture databases, International Osteoporosis Foundation registries, FDA and EMA drug approval archives, UN population aging tables, and OECD Health-Stats, which together map disease burden, therapy launches, and price corridors. Financial filings, investor decks, and national drugs tender bulletins complement those macro sources with revenue splits, while paid repositories, D&B Hoovers for company sales, Dow Jones Factiva for real-time tender wins, and Questel for patent activity, anchor competitive movements. These references illustrate, not exhaust, the broad secondary pool tapped by Mordor analysts for triangulation.

Market-Sizing & Forecasting

A top-down epidemiology build, hip and vertebral fracture prevalence linked to treatment penetration and average therapy duration, creates the initial demand pool, which is then cross-checked bottom-up through sampled ex-factory ASP × volume rolls from leading manufacturers and channel checks. Key variables include aging population growth, DXA scan rates, biologic price erosion, generic entry timelines, and therapy compliance curves; each feeds a multivariate regression that projects value through 2030. Where bottom-up samples run thin, notably in low-volume African markets, adjacent country analogs and tender data are used to bridge gaps before final calibration.

Data Validation & Update Cycle

Outputs pass variance scans against historical sales trends, anomaly flags trigger re-checks with domain experts, and supervisory reviews finalize the model. We refresh every twelve months, revisiting numbers mid-cycle if safety alerts, major approvals, or reimbursement shifts materially move the needle.

Why Mordor's Osteoporosis Drugs Baseline Commands Reliability

Published estimates often differ because firms pick distinct product baskets, price bases, and forecast cadences.

Key gap drivers include whether generics are counted, if biologic rebates are netted, and how fast aging curves are applied. Our disciplined scope, annual refresh, and dual-lens modelling temper extremes, giving decision-makers a balanced anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.88 B (2025) | Mordor Intelligence | - |

| USD 15.28 B (2024) | Regional Consultancy A | Excludes generics in many emerging markets, narrowing patient coverage |

| USD 15.57 B (2025) | Global Consultancy B | Relies on epidemiology-only top-down estimates without sales cross-checks |

| USD 18.18 B (2024) | Trade Journal C | Adds nutraceuticals and orthobiologics, inflating baseline |

The comparison shows that when scope creep or insufficient validation skews numbers, outcomes swing wide. Mordor's method, rooted in verified variables and repeatable steps, delivers a dependable baseline clients can trace and trust.

Key Questions Answered in the Report

What is the current size of the osteoporosis drugs market?

The osteoporosis drugs market generated USD 16.88 billion in 2025 and is projected to reach USD 21.28 billion by 2030.

Which drug class holds the largest share?

Bisphosphonates remained the biggest category with a 37.40% osteoporosis drugs market share in 2024.

Why are anabolic agents gaining popularity?

They deliver vertebral-fracture reductions up to 86% and now receive broader reimbursement, making them attractive for high-risk patients.

How will biosimilars influence market growth?

Denosumab biosimilars priced 20-30% below the originator will expand patient access, increasing treated volumes but trimming per-patient revenue.

Which region is growing the fastest?

Asia-Pacific is advancing at a 7.01% CAGR because of rapid population aging, broader insurance coverage, and rising biologic uptake.

What role does AI play in osteoporosis care?

AI models embedded in primary care imaging detect low bone density with nearly 90% accuracy, enabling earlier intervention and reducing downstream fracture costs.

Page last updated on: