Market Trends of OSAT Industry

Communication to be the Largest Application Segment

- The semiconductor market's growth directly influences the OSAT market's development because the packaging is still at an early stage in the telecommunications value chain. The foundries can either handle the packaging themselves or contract it out. For instance, Qualcomm, a manufacturer of semiconductors and telecom equipment, contracts OSATs to handle its packaging needs.

- The communication applications primarily consist of communication chips in the telecommunication industry. Equipment such as power amplifiers (PAs), front-end modules (FEMs), and other RF and connectivity devices are major sources of demand for OSATs and OEMs. According to the Semiconductor Industry Association, about 31% of all semiconductors manufactured are used for communications, including networking equipment and smartphone radios.

- Communication applications require highly reliable packaging solutions as they are often deployed in harsh environmental conditions. In many cases, a system in package (SiP) is preferred for a large variety of communication equipment, especially in large-scale telecommunication applications.

- The smartphone market has grown significantly in hardware and software over the past few years. Despite declining global smartphone unit shipments during COVID-19, there was high penetration in many markets, including China. Sales of new smartphones are expected to regain momentum, driven by trends like biosensors, 5G smartphones, and AI features.

- The smartphone adoption rate in Asia-Pacific is expected to rise to 83% by 2025, according to GSMA. Concurrently, the mobile subscriber penetration rate is expected to reach 62% by the same year. The proliferation of 5G smartphones is also expected to significantly improve connected device density, wireless data communication bandwidth, and latency.

- Many semiconductor producers anticipate that 5G smartphones with higher silicon contents will be widely adopted worldwide. The use of semiconductor components per device will rise due to the need for 5G smartphones to have higher power efficiency, faster speeds, and more complex functionalities. In turn, the consumer electronics industry is anticipated to experience a significant increase in demand for semiconductor packaging solutions.

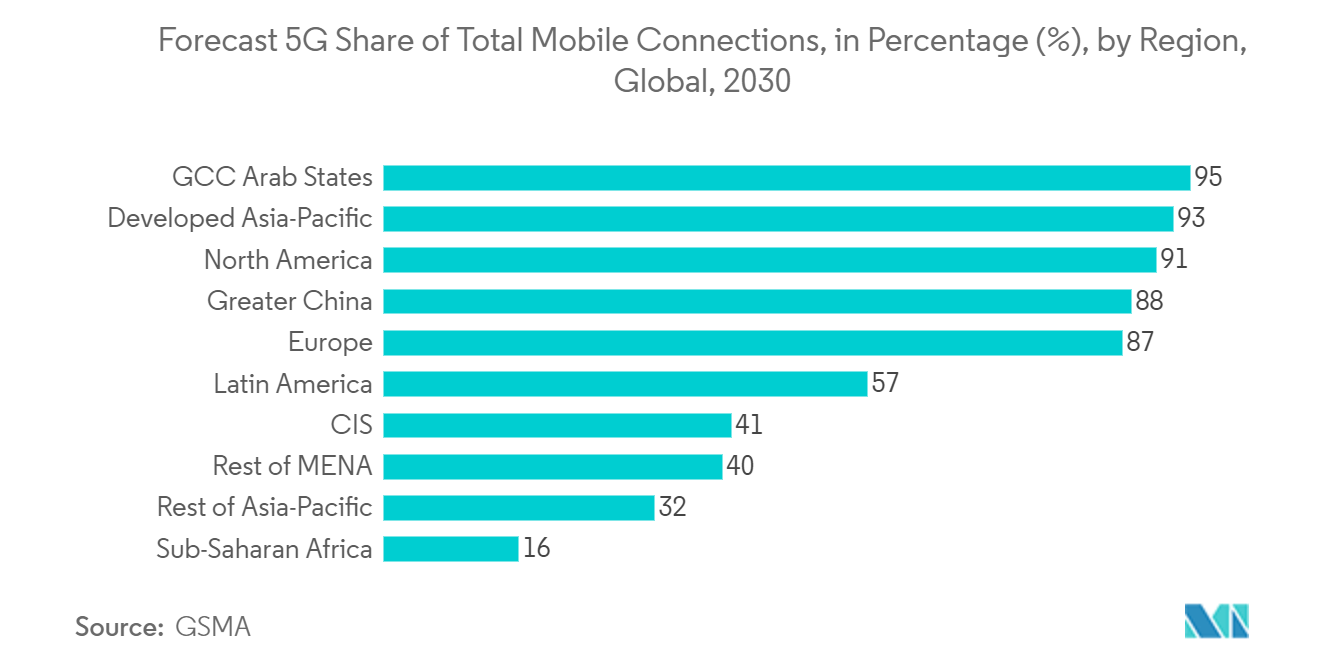

- According to the GSMA Report, around one-third of the global population is estimated to have access to 5G networks by 2025. The report also states that there will be more than 400 million 5G connections at that time, accounting for approximately 14% of all mobile connections.

- The adoption of 5G was projected to reach 17% by the end of 2023 and increase to 54% (equivalent to 5.3 billion connections) by 2030. This technological advancement is anticipated to contribute nearly USD 1 trillion to the global economy. As a result, the demand for semiconductors will enhance the market's growth.

Understand The Key Trends Shaping This Market

Download PDF

South Korea Expected to Register Significant Growth in the Market

- South Korea is one of the promising markets for global OSAT vendors. The country is also home to some prominent chip makers for the consumer electronics segment, such as Samsung and SK Hynix, making it a lucrative hub for innovation in semiconductor devices.

- The South Korean government focuses on smart manufacturing and plans to have 30,000 fully automated manufacturing companies by 2025. The government aims to achieve this by incorporating the latest automation, data exchange, and IoT technologies, which are expected to be significant drivers for OSAT services in the country.

- The country's semiconductor testing sector has grown significantly with the growth of Samsung Electronics' system semiconductor business. The semiconductor testing companies in the country, such as NEPES Ark, LB Semicon, Tesna, and Hana Micron, have been dealing with increased supplies of system semiconductors by making significant investments in necessary facilities and equipment.

- SK Hynix is constructing a base for manufacturing next-generation memory in the Wonsam town region of Yongin by investing KRW 120 trillion ( USD 90 billion). The chipmaker anticipates breaking construction on the memory manufacturing facility in 2025. SK Hynix is also the manufacturer of HBM3. The company plans to install TSV packaging production lines at its Icheon DRAM manufacturing facility. To improve its HBM competitiveness, Samsung and SK Hynix are considering adding more packaging production lines.

- Samsung has been working on replacing the 2.5D interposer integration service offered by TSMC. It seeks to lower the cost of manufacturing the through-silicon via (TSV) packaging method. Compared to SK Hynix, Samsung is a latecomer to the HBM (high bandwidth memory) market. Still, the business claims it is increasing investments in its HBM capacity and declared intentions to introduce new HBM products by 2023, opening possibilities for expanding HBMs' packaging capacity.

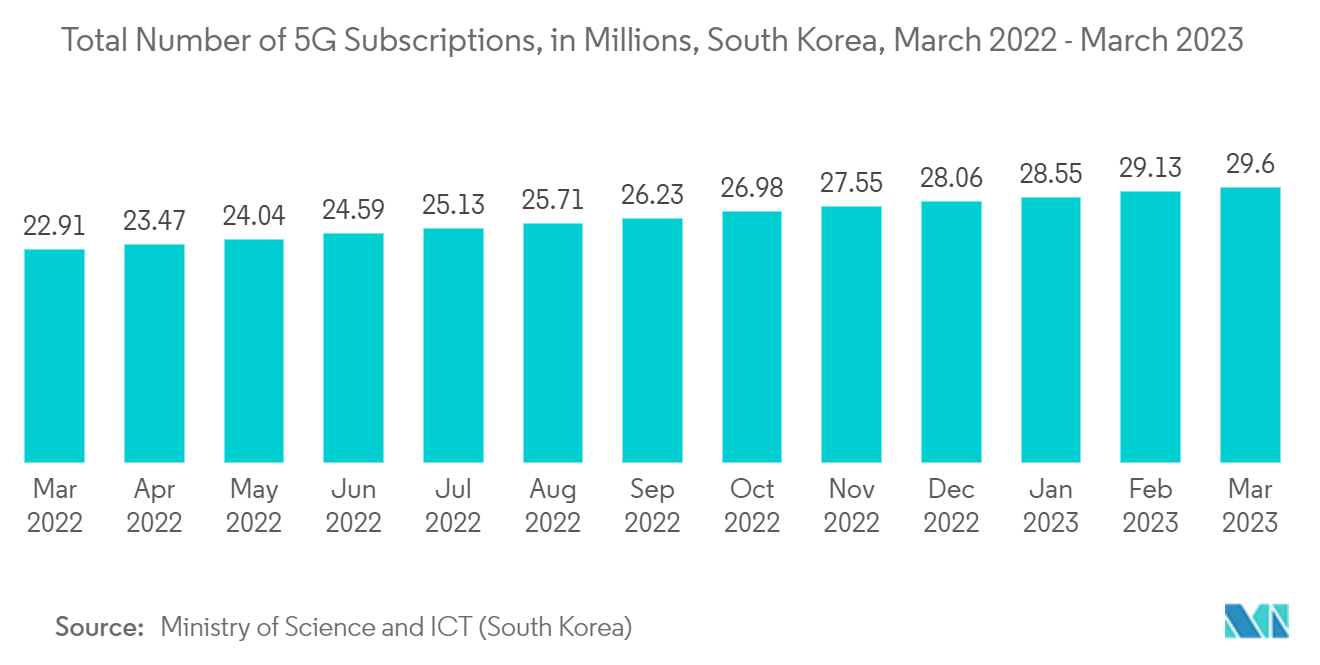

- The developments in the 5G space have also led to the growth of advanced packaging of chips. According to the Ministry of Science and ICT, as of February 2023, the country had 29.13 million 5G Subscribers, an increase of 113% compared to 13.66 million 5G subscribers in February 2021.

Get Analysis on Important Geographic Markets

Download PDF