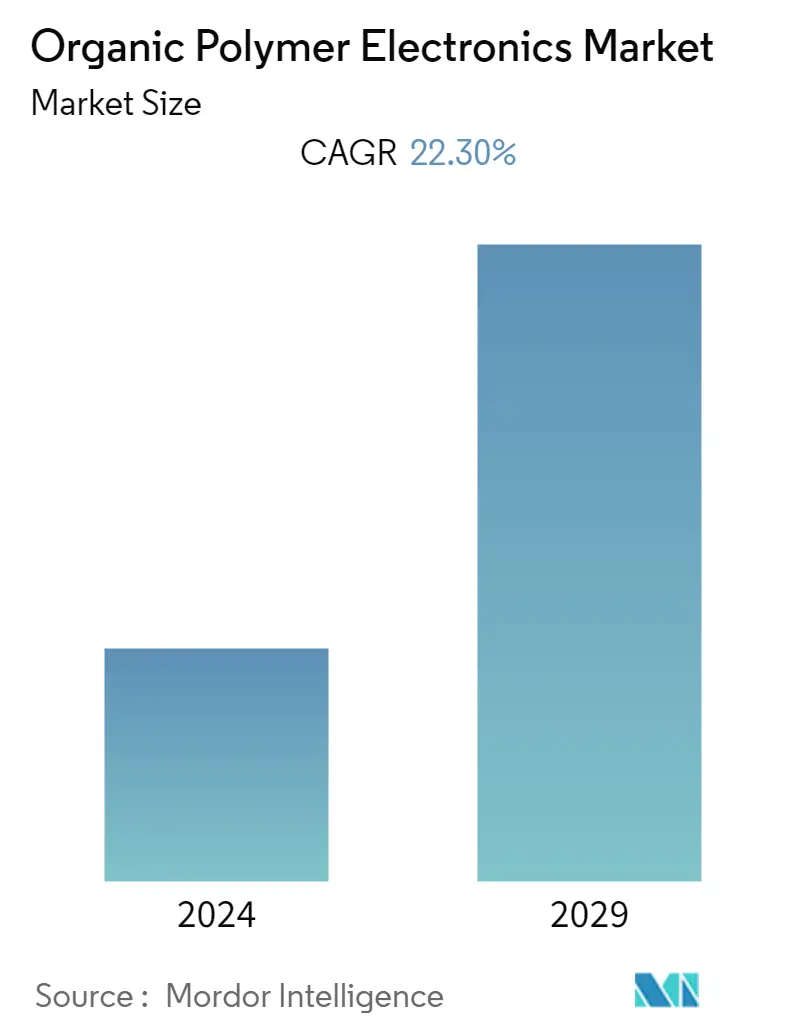

Organic Polymer Electronics Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 22.30 % |

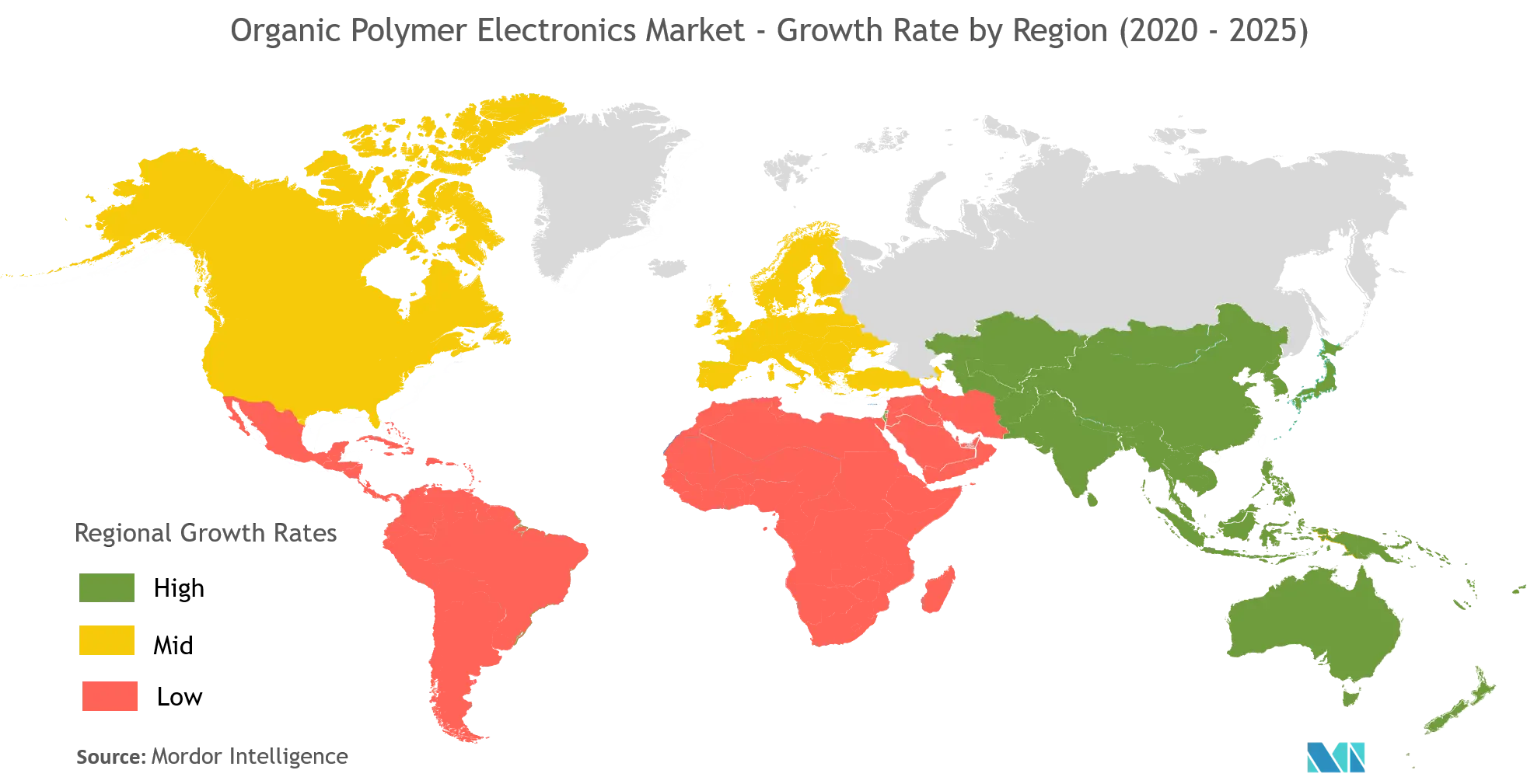

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

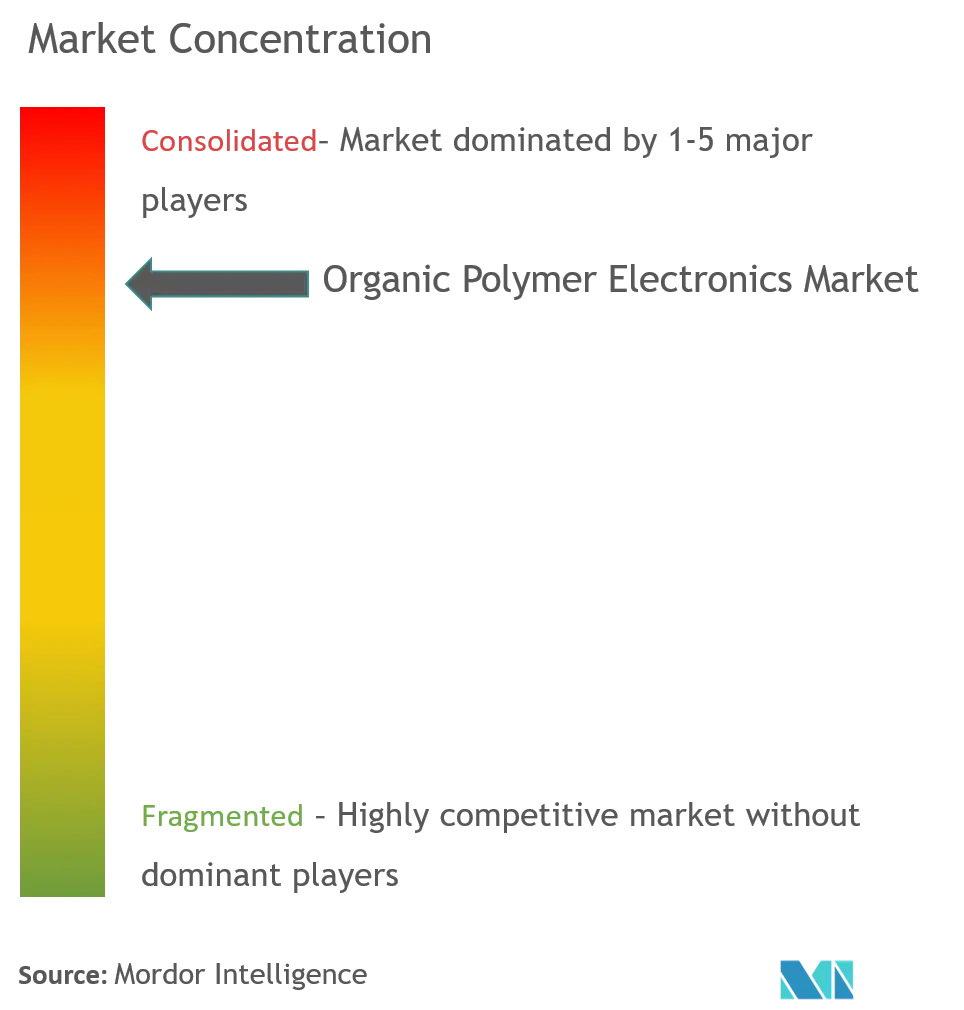

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Organic Polymer Electronics Market Analysis

The Organic Polymer Electronics Market is expected to grow at a CAGR of 22.3% over the forecast period 2020 to 2025. The devices which are made from organic polymer electronics are gradually becoming a low-cost alternative to the traditional inorganic electronic applications, due to low material utilization (use of materials that are synthesized, rather than mined from the earth) and simple processing.

- The market is majorly growing due to the rapid increase in adoption in the display industry as well as lighting, due to expanding functionality and accessibility of electronics, which traditional silicon-based electronics cannot do.

- OLEDs displays occupy a fair share of the market. In 2019, Amazon launched the first OLED TVs with FireTV in the United Kingdom, Germany, and Austria. In the United Kingdom, the company collaborated with Currys, and in Austria and Germany, they partnered with Grundig.

- Head mounted devices for augmented and virtual reality are one of the emerging applications in the display industry, since they have organic light emitting diodes as a crucial part. Apart from the gaming industry, HMDs are being used in military, medical and engineering contexts.

- Training of all types is the most potential application of AR & VR. Navy researchers are integrating AR technology into head mounted displays (HMD) to effectively provide ground deployed troops with the technology utilized by pilots.

- When it comes to electronic components, organic polymer electronics is revolutionizing small, flexible, wide-area electronic devices that can be produced at low cost in very high volumes. The demand for flexible electronic goods is required in healthcare, and government sectors.

- With advancements in wearable technology, proliferating wearable devices are being programmed to interact with the bodies and collect data. The flexible displays make sure that wearables are thin, light, robust, and comfortable for the user.

- The researchers at Leibniz Institute for Solid State and Materials Research in Germany have developed the first flexible electronic chip made of magnetic sensors and organic, polymer-based circuits. This has the potential for development in artificial electronic skins, robotics with soft materials, and biomedical science.

- Organic polymers for photovoltaic (OPV) and photodiode (OPD) are under progress nowadays. OPV solar cells can be semi-transparent, and are therefore used in the design of energy roofs that allow light to pass through.

Organic Polymer Electronics Market Trends

This section covers the major market trends shaping the Organic Polymer Electronics Market according to our research experts:

Organic Display to Witness Huge Demand

- The growing demand for enhanced displays drives the display market, organic displays such as OLED and PMOLED, augmented displays, and roll-able transparent displays. OLED technology enables efficient, bright, and thin displays and lighting panels. They are currently used in some TVs, various mobile devices, and lighting accessories. OLED displays give a more excellent image quality matched to that of LCD or Plasma displays - and can also be made transparent and flexible.

- The organic display is the largest revenue-generating segment since display devices like OLEDs find applications in laptops, tablets, TV sets, lighting, etc. Asia-Pacific is house to approximately 3/4th of the global electronics manufacturing industry, the primary application area for organic electronics. Reasons like the increasing disposable income of end-users and inclination for high-quality products influence the LCD manufacturers to invest in organic electronics.

- Display panel merchants are putting up with the demand and are launching more latest OLED displays. For instance, as of April 2020, LG Display technology will make OLED panels see-through when they are switched on. This leads to several additional applications like shop windows and offices to depict a superior user experience. In August 2019, Samsung shared plans to commence production of QD-OLED production shortly by converting its 8.5-Gen LCD lines in Asan, Korea.

- Moreover, the companies are also pitching the use of the transparent display in the aviation sector. For instance, in December 2019, LG Display’s organic light-emitting diode (OLED) panels were deployed in Boeing’s next-generation aircraft, expanding its flexible panel beyond automotive.

- Smartphones primarily drive the consumer electronics market as an application. A recent report from Mizuho Securities, in 2019, estimates the growth of OLED displays for smartphones and feature phones. Mizuho forecasts the OLED penetration to reach 29 % of the display market, growing to 80 % by 2026.

- To achieve product differentiation and competitive advantage in the market, the LCD companies have been using OLED displays in their TV sets. Due to this, the need in the OLED displays market is anticipated to grow.

APAC to Witness the Highest Growth in the Organic Polymer Electronics Market

- Asia-pacific is the fastest-growing market for the organic polymer electronics market, owing to the high growth of the consumer electronics industry. Additionally, the region has a strong foothold of vendors which adds to the growth of the market. Some of the includes Sumitomo Chemical, LG Display Co. Ltd, and Samsung Display Co. Ltd among others.

- In April 2019, Sumitomo Chemical and Zymergen signed a multi-year partnership to bring new specialty materials to the market. This collaboration between the two companies will enable the development of new materials to meet consumer trends in high-tech industries.

- The presence of the semiconductor device manufacturers and fabricators in countries such as, in Taiwan, China, Japan, and South Korea have allowed the consumer electronics companies to adopt these materials in their electronic products.

- Significant demand for smartphones and other consumer electronics devices from countries, such as India, China, the Republic of Korea, and Singapore, are encouraging many vendors to set up production establishments in the region. Investments in the smartphone segment are poised to drive the demand for OLED displays in the India.

- In January 2019, LG Display, one of the innovator of display technologies, announced to introduce OLED and LCD displays at CES 2019 in Las Vegas from January 8 to 11. LG Display plans to introduce an 88-inch 8K Crystal Sound OLED (CSO) display with an advanced 3.2.2 channel sound system embedded into the display. Samsung also launched OLED displays for IT and smartphone markets, ultra-large 8K LCDs and a 32:9 curved display.

- In the past year, 4K TVs, also known as Ultra High Definition (UHD), have been gaining traction in the Asia-Pacific from past two years, with the market upgrading the display resolutions from Full High Definition to UHD.

- Chinese panel makers are expanding their production capacities for OLED displays, putting pressures on other industry players. Samsung is closing its 8.5 generation production line in 2019 and shifting the focus to QD-OLED panels in response to the price competition. LG Display also plans to expand its OLED production capacities in China and Korea targeting large-sized TV displays

Organic Polymer Electronics Industry Overview

The Organic Polymer Electronics Market is fairly concentrated due to high entry barriers and huge initial investments. The market consists of several major players. In terms of market share, few of these players currently dominate the market. The major players in the market are, Sony Corporation, AU Optronics Corporation, Universal Display Corporation (UDC), Merck KGaA, and Novaled Gmbh among others.

- Jan 2020 - Sony Corporation announced its first TVs of 2020, and among them is the 48-inch Master Series A9S, the company's smallest 4K OLED ever. At the top of the lineup is a new 8K LCD TV, the 85- or 75-inch Sony Z8H, followed by the A8H OLED, which is available in 65-inch and 55-inch variants.

- May 2019 - Merck KGaA acquired Intermolecular Inc. for USD 1.20 per share in an all-cash transaction. Intermolecular's capabilities in rapid material screening, in combination with the R&D pipeline of Merck KGaA, is expected to foster materials innovation.

Organic Polymer Electronics Market Leaders

Sony Corporation

AU Optronics Corp

Merck KGaA

Novaled Gmbh

Universal Display Corporation (UDC)

*Disclaimer: Major Players sorted in no particular order

Organic Polymer Electronics Market Report - Table of Contents

-

1. INTRODUCTION

-

1.1 Study Assumptions and Market Definition

-

1.2 Scope of the Study

-

-

2. RESEARCH METHODOLOGY

-

3. EXECUTIVE SUMMARY

-

4. MARKET INSIGHTS

-

4.1 Market Overview (Commentary on Covid-19 Impact along with latest trends persisting in the market)

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

-

4.2.1 Bargaining Power of Suppliers

-

4.2.2 Bargaining Power of Consumers

-

4.2.3 Threat of New Entrants

-

4.2.4 Intensity of Competitive Rivalry

-

4.2.5 Threat of Substitute Products

-

-

4.3 Industry Value Chain Analysis

-

-

5. MARKET DYNAMICS

-

5.1 Market Drivers

-

5.1.1 Increase in Adoption of Augmented Reality and Virtual Reality Devices

-

5.1.2 Advancements in Wearables Technology

-

-

5.2 Market Challenges

-

5.2.1 Volatility in Raw Material Prices

-

-

-

6. BREAKDOWN BY TYPES OF MATERIALS

-

6.1 Semiconductor Materials

-

6.2 Conductive Materials

-

6.3 Dielectric Materials

-

6.4 Substrate Materials

-

6.5 Other Materials

-

-

7. MARKET SEGMENTATION

-

7.1 By Application

-

7.1.1 Organic Display

-

7.1.2 Organic Photovoltaic

-

7.1.3 OLED Lighting

-

7.1.4 Electronic Components and Integrated Systems

-

-

7.2 By End-user

-

7.2.1 Automotive

-

7.2.2 Consumer Electronics

-

7.2.3 Healthcare

-

7.2.4 Industrial Sector

-

7.2.5 Military and Defense

-

-

7.3 Geography

-

7.3.1 North America

-

7.3.2 Europe

-

7.3.3 Asia-Pacific

-

7.3.4 Rest of the World

-

-

-

8. COMPETITIVE LANDSCAPE

-

8.1 Company Profiles*

-

8.1.1 Sony Corporation

-

8.1.2 AU Optronics Corp

-

8.1.3 Merck KGaA

-

8.1.4 Novaled Gmbh

-

8.1.5 Universal Display Corporation (UDC)

-

8.1.6 FlexEnable Ltd

-

8.1.7 LG Display Co. Ltd

-

8.1.8 Samsung Display Co. Ltd

-

8.1.9 \BOE Technology Group Co. Ltd

-

8.1.10 Sumito Chemical Co. Ltd

-

-

-

9. INVESTMENT ANALYSIS

-

10. MARKET OPPORTUNITIES & FUTURE OF THE MARKET

Organic Polymer Electronics Industry Segmentation

Organic electronic devices are likely to become a low-cost alternative to the traditional inorganic electronic applications, due to low material utilization (use of materials that are synthesized, rather than mined from the earth) and simple processing. They find their uses in applications like aerospace, display manufacturing, lighting due to expanding functionality and accessibility of electronics, which traditional silicon-based electronics cannot do.

| By Application | |

| Organic Display | |

| Organic Photovoltaic | |

| OLED Lighting | |

| Electronic Components and Integrated Systems |

| By End-user | |

| Automotive | |

| Consumer Electronics | |

| Healthcare | |

| Industrial Sector | |

| Military and Defense |

| Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

Organic Polymer Electronics Market Research FAQs

What is the current Organic Polymer Electronics Market size?

The Organic Polymer Electronics Market is projected to register a CAGR of 22.30% during the forecast period (2024-2029)

Who are the key players in Organic Polymer Electronics Market?

Sony Corporation , AU Optronics Corp, Merck KGaA, Novaled Gmbh and Universal Display Corporation (UDC) are the major companies operating in the Organic Polymer Electronics Market.

Which is the fastest growing region in Organic Polymer Electronics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Organic Polymer Electronics Market?

In 2024, the North America accounts for the largest market share in Organic Polymer Electronics Market.

What years does this Organic Polymer Electronics Market cover?

The report covers the Organic Polymer Electronics Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Organic Polymer Electronics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Organic Polymer Electronics Industry Report

Statistics for the 2024 Organic Polymer Electronics market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Organic Polymer Electronics analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.