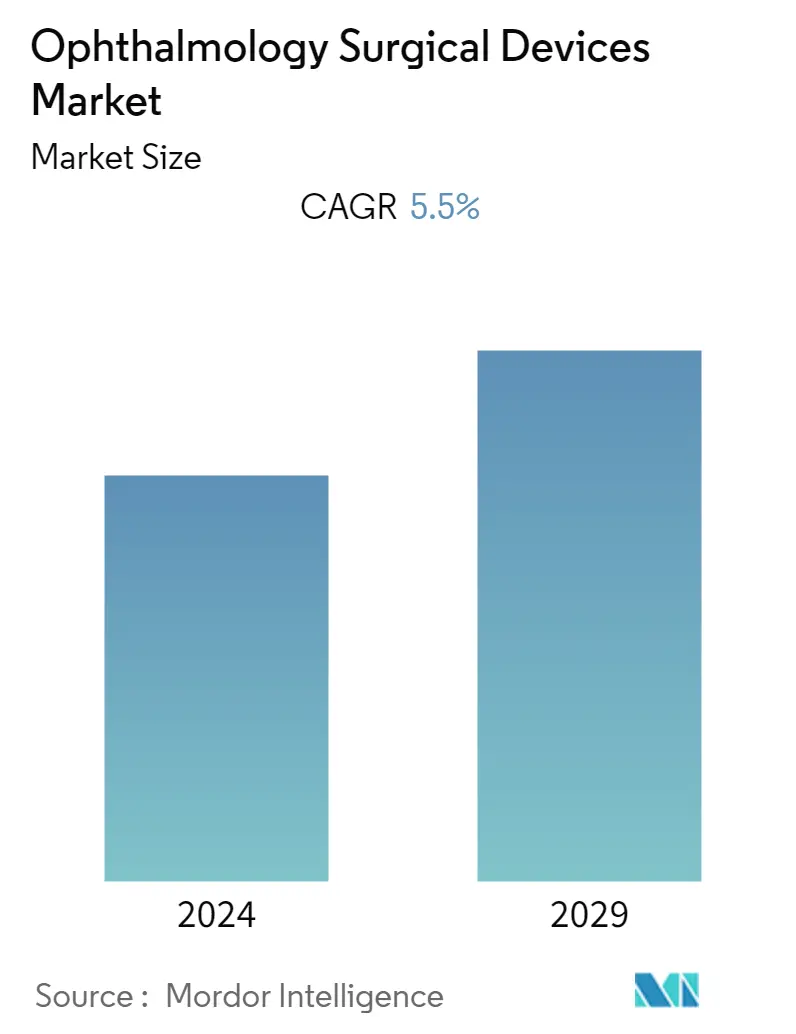

Ophthalmology Surgical Devices Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 5.50 % |

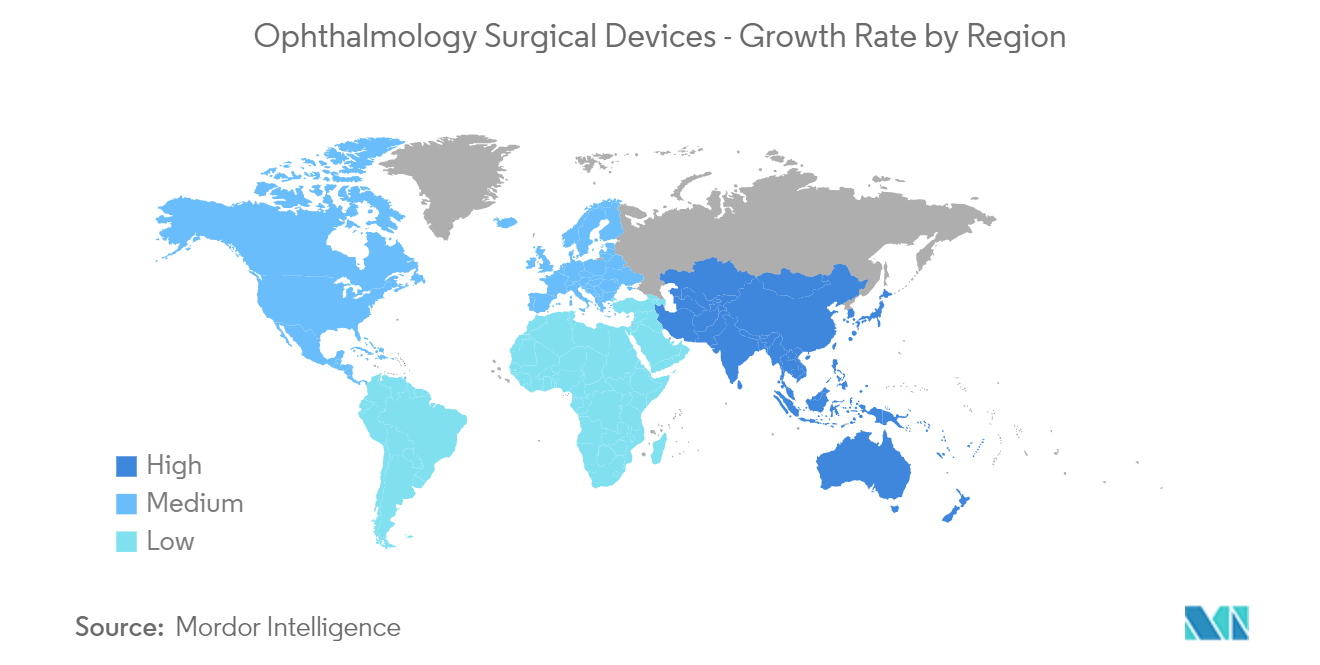

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

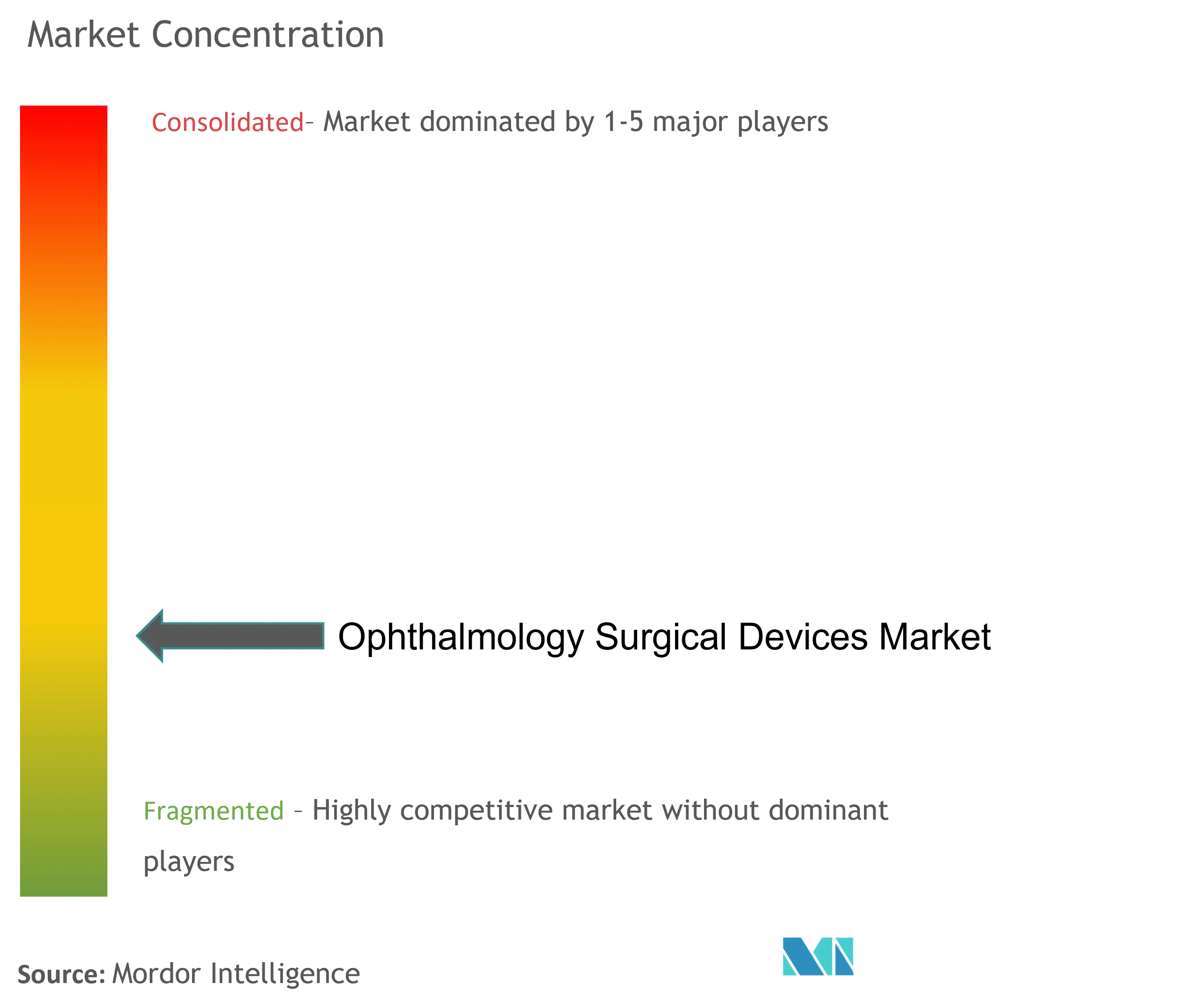

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Ophthalmology Surgical Devices Market Analysis

The ophthalmology surgical devices market studied is expected to register a CAGR of 5.5% during the forecast period.

- During the initial wave, the COVID-19 pandemic significantly impacted the ophthalmology surgical devices market, as many ophthalmic surgeries and consultations were delayed or canceled due to the global lockdown. This resulted in a substantial backlog of patients developing advanced cataracts and other eye disorders, significantly affecting the market. However, with the resumption of transport and decreasing cases of COVID-19, the market is expected to recover from the decline over the forecast period, mainly due to the increasing demand for ophthalmic surgeries worldwide.

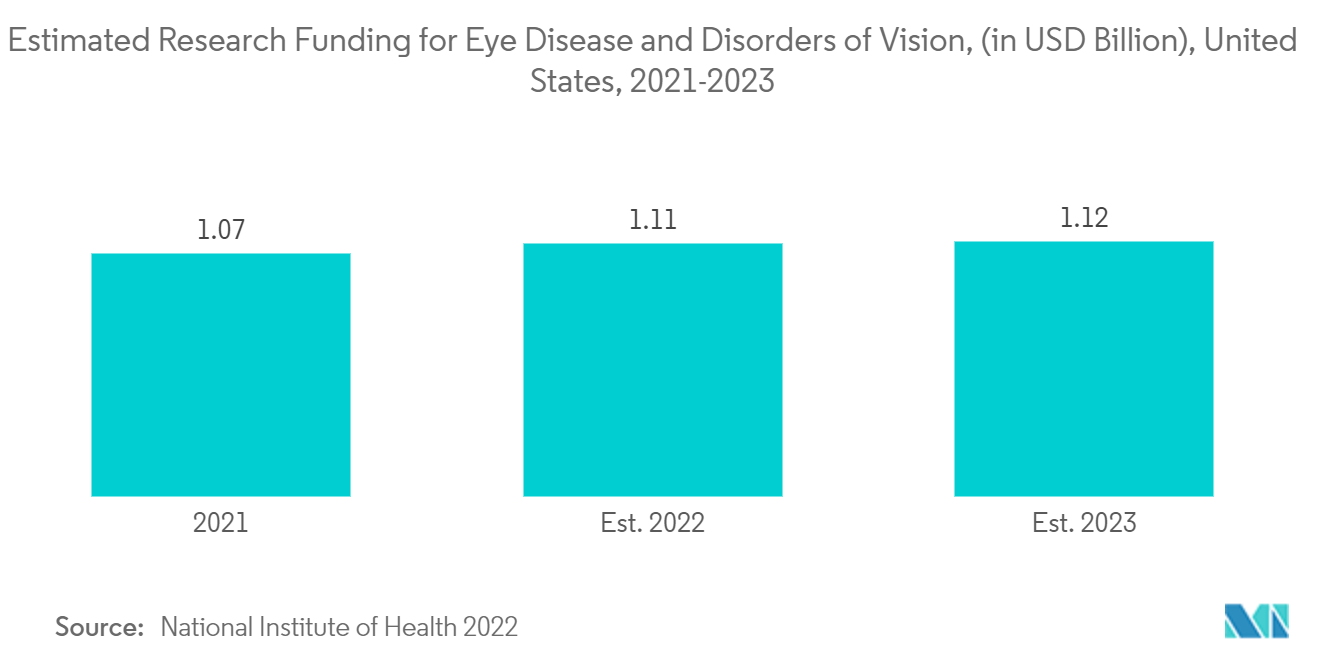

- The global prevalence of ophthalmic disorders such as glaucoma, cataract, and diabetic retinopathy primarily drives the market growth. The rise in the geriatric population results in the global burden of avoidable blindness. For example, according to the December 2022 update by the Centers for Disease Control and Prevention, vision impairment in the United States affects around 12 million people aged 40 years or above. This includes approximately 1 million who are blind and 3 million who have vision impairment even after correction. Similarly, according to the 2021 update by Macular Disease Foundation Australia, glaucoma prevalence among Australians is predicted to increase to 379,000 by 2025.

- The market growth is also fueled by advanced technologies in ophthalmology surgery devices and virtual reality options. Alcon, for instance, introduced its new Alcon Fidelis Virtual Reality (VR) Ophthalmic Surgical Simulator, a portable VR tool for cataract surgeons-in-training, which offers a high-fidelity, virtual operating room environment with haptic feedback to simulate the look and feel of cataract surgery.

- Additionally, government initiatives and support for the visually impaired population are likely to increase awareness and thereby drive market growth over the forecast period. For example, the Foundation Fighting Blindness launched a new social media campaign, #ShareYourVision, and WHO launched a new guide on eye care, Eye Care in Health Systems: Guide for Action, providing practical, step-by-step guidance to support Member States in planning and implementing integrated, people-centered eye care services.

- Despite these factors, the high cost of the devices and unfavorable reimbursement policies are likely to restrain the market growth. Nonetheless, due to the rise in eye diseases, increasing product launches, technological advancements, and government initiatives, the ophthalmology surgical devices market is expected to witness significant growth over the forecast period.

Ophthalmology Surgical Devices Market Trends

The Cataract Surgery Devices Segment is Expected to Hold a Significant Share in the Studied Market

- The segment of cataract surgery devices is projected to witness a substantial market revenue share in recent years and is expected to continue to do so over the forecast period. This growth can be attributed to several factors, including the rising number of cataract cases that require surgery, an increase in the launch of new products, and technological advancements in cataract surgery devices. It is worth noting that cataract surgery remains the primary treatment for individuals with cataracts, as it helps to restore vision.

- Moreover, the growth of this segment is expected to be driven by an increase in government initiatives aimed at supporting the population affected by cataracts. For instance, in May 2022, the Central government of India announced plans to conduct a special campaign over the next three years to clear the backlog in cataract surgeries and severe visual impairment. Such initiatives are expected to create a conducive environment for market growth.

- Additionally, the market is expected to benefit from ongoing technological advancements and product launches in ophthalmology surgery devices. For instance, in July 2021, Johnson & Johnson (J&J) Vision globally launched its phacoemulsification (phaco) system, which is designed to provide surgeons with improved efficiency and comfort during cataract surgery. Phacoemulsification, the most frequent cataract surgical approach, allows doctors to emulsify and remove the eye's internal lens when it becomes cloudy due to cataracts. Furthermore, in April 2022, Alcon released data from a clinical study supporting the use of its SmartCataract solutions for cataract surgery.

- In summary, the cataract surgery devices segment is expected to experience significant growth over the forecast period due to the rise in cataract cases, an increase in product launches, technological advancements, and government initiatives to support the cataract-affected population.

North America Anticipated to Hold a Significant Share in the Market Over the Forecast Period

- North America is anticipated to maintain a substantial market share in the ophthalmic surgical devices market during the forecast period due to various factors. Firstly, there has been a rise in the prevalence of eye diseases in the region. According to the Bright Focus Foundation's October 2022 update, more than 3 million Americans are living with glaucoma, with open-angle glaucoma affecting 2.7 million people aged 40 and above. Moreover, 3.3 million Americans aged 40 and over experience blindness or low vision, indicating a significant need for ophthalmic surgical devices in the region.

- The increase in the prevalence of eye diseases is a primary factor driving the market growth in North America. Additionally, technological advancements in ophthalmic surgery devices and product launches are contributing to the growth of the market. Government initiatives to support visually impaired populations are also expected to fuel the market's growth over the forecast period. For example, World Glaucoma Week is celebrated every year from March 6 to 12 to raise awareness about glaucoma. In 2022, the initiative aimed to "save your sight" by urging people to have regular check-ups and early diagnosis of glaucoma.

- Furthermore, market players are adopting various strategies to increase their market share, such as product launches, developments, acquisitions, collaborations, mergers, and expansions. For instance, Alcon, a company focused on eye care, completed the acquisition of Ivantis, a developer of the novel Hydrus Microstent, in January 2022. This minimally invasive glaucoma surgery (MIGS) device is designed to lower eye pressure for open-angle glaucoma patients in connection with cataract surgery.

- To sum up, North America is expected to hold a significant market share in the ophthalmic surgical devices market throughout the forecast period due to the rise in eye diseases, an increase in product launches, technological advancements, government initiatives, and market players' strategic efforts.

Ophthalmology Surgical Devices Industry Overview

The ophthalmology surgical devices market is competitive and consists of several major players. A few of the key players are developing new products with upgraded technologies to compete with the existing products trending in the market. Furthermore, key players are entering into partnerships to develop their market position globally. Some of the companies which are currently dominating the market are Bausch Health (Bausch & Lomb Incorporated), Johnson & Johnson, Topcon Corporation, Ziemer Ophthalmic Systems AG, Carl-Zeiss-Stiftung (Carl Zeiss AG), and Alcon Inc.

Ophthalmology Surgical Devices Market Leaders

-

Johnson & Johnson

-

Alcon Inc

-

Ziemer Ophthalmic Systems AG

-

Bausch Health (Bausch & Lomb Incorporated)

-

Carl-Zeiss-Stiftung (Carl Zeiss AG)

*Disclaimer: Major Players sorted in no particular order

Ophthalmology Surgical Devices Market News

- June 2022: LENSAR, Inc., a medical technology company focused on advanced femtosecond laser surgical solutions for the treatment of cataracts, received United States Food and Drug Administration (US FDA) 510(k) for its next-generation ALLY Adaptive Cataract Treatment System. ALLY is one of the first FDA-cleared platforms to enable cataract surgeons to complete the femtosecond-laser-assisted cataract surgery procedure seamlessly in a single, sterile environment.

- April 2022: Nova Eye Medical Limited, a medical technology company committed to advanced ophthalmic treatment technologies and devices, launched its next-generation canaloplasty device, iTrack Advance, in selected markets in Europe and the Asia Pacific.

Ophthalmology Surgical Devices Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Increase in Burden of Ophthalmic Diseases

4.2.2 Rise in Government Support to Control Visual Impairment and Rapid Advancements in the Ophthalmic Industry

4.3 Market Restraints

4.3.1 Higher Cost of the Ophthalmology Surgical Devices

4.3.2 Unfavorable Reimbursement Policies Pertaining to the Ophthalmic Surgery Industry

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Product

5.1.1 Refractive Surgery Devices

5.1.2 Glaucoma Surgery Devices

5.1.3 Cataract Surgery Devices

5.1.4 Other Surgical Devices

5.2 By End-User

5.2.1 Hospitals

5.2.2 Speciality Clinics

5.2.3 Ambulatory Surgical Centers

5.3 Geography

5.3.1 North America

5.3.1.1 United states

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.2 Europe

5.3.2.1 France

5.3.2.2 Germany

5.3.2.3 United Kingdom

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 South Korea

5.3.3.6 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 GCC

5.3.4.2 South Africa

5.3.4.3 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Bausch Health (Bausch & Lomb Incorporated)

6.1.2 Topcon Corporation

6.1.3 Johnson & Johnson

6.1.4 Carl-Zeiss-Stiftung (Carl Zeiss AG)

6.1.5 Alcon Inc

6.1.6 Lumenis Ltd

6.1.7 Hoya Corporation

6.1.8 Ellex Medical Laser Ltd

6.1.9 STAAR Surgical Company

6.1.10 Ziemer Ophthalmic Systems AG

6.1.11 EssilorLuxottica (Essilor)

6.1.12 Glaukos

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Ophthalmology Surgical Devices Industry Segmentation

As per the scope of the report, ophthalmology surgical devices are used in retinal, refractive, and cataract surgeries, diagnosis, and in treatment of various ophthalmic diseases such as cataract, glaucoma, and refractive error. These devices are employed majorly when the disease is not diagnosed at an early stage.

The ophthalmology surgical devices market is segmented by product (cataract surgery devices, glaucoma surgery devices, refractive surgery devices, and other surgical devices), end-user (hospitals, specialty clinics, ambulatory surgical centers), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above segments.

| By Product | |

| Refractive Surgery Devices | |

| Glaucoma Surgery Devices | |

| Cataract Surgery Devices | |

| Other Surgical Devices |

| By End-User | |

| Hospitals | |

| Speciality Clinics | |

| Ambulatory Surgical Centers |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Ophthalmology Surgical Devices Market Research FAQs

What is the current Ophthalmology Surgical Devices Market size?

The Ophthalmology Surgical Devices Market is projected to register a CAGR of 5.5% during the forecast period (2024-2029)

Who are the key players in Ophthalmology Surgical Devices Market?

Johnson & Johnson, Alcon Inc, Ziemer Ophthalmic Systems AG, Bausch Health (Bausch & Lomb Incorporated) and Carl-Zeiss-Stiftung (Carl Zeiss AG) are the major companies operating in the Ophthalmology Surgical Devices Market.

Which is the fastest growing region in Ophthalmology Surgical Devices Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Ophthalmology Surgical Devices Market?

In 2024, the North America accounts for the largest market share in Ophthalmology Surgical Devices Market.

What years does this Ophthalmology Surgical Devices Market cover?

The report covers the Ophthalmology Surgical Devices Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Ophthalmology Surgical Devices Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Corneal Surgery Devices Industry Report

Statistics for the 2024 Corneal Surgery Devices market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Corneal Surgery Devices analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Corneal Surgery Devices Market Report Snapshots