Market Size of Onshore Oil And Gas Pipeline Industry

| Study Period | 2019 - 2029 |

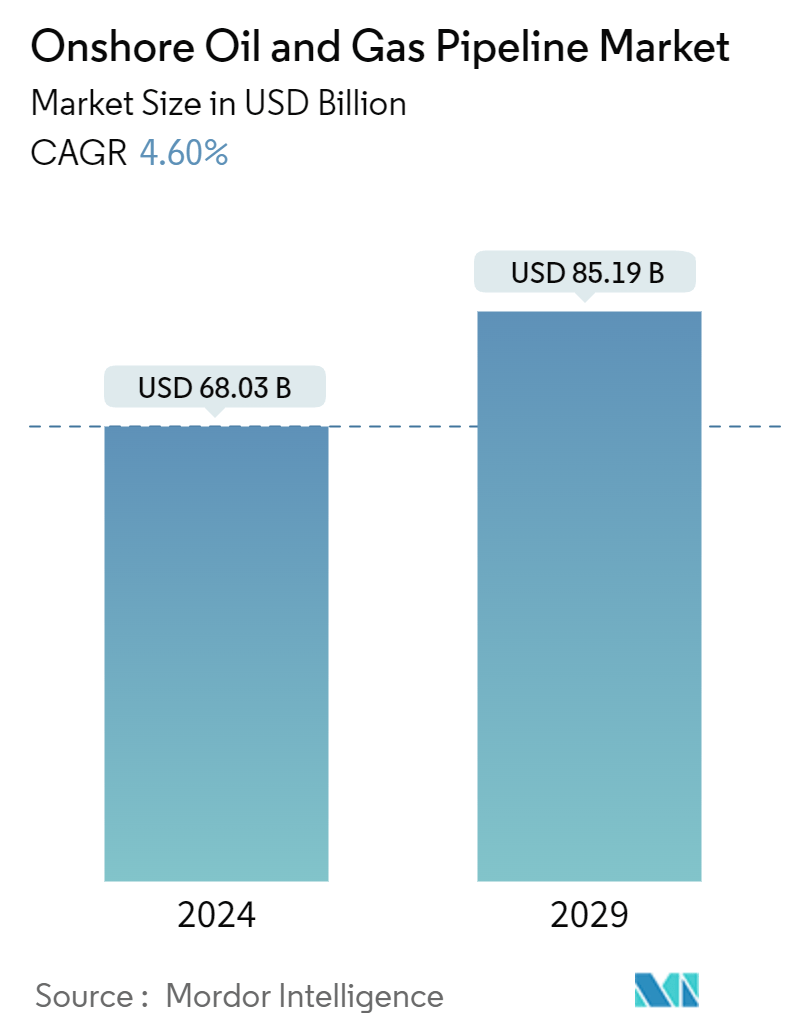

| Market Size (2024) | USD 68.03 Billion |

| Market Size (2029) | USD 85.19 Billion |

| CAGR (2024 - 2029) | 4.60 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Onshore Oil And Gas Pipeline Market Analysis

The Onshore Oil And Gas Pipeline Market size is estimated at USD 68.03 billion in 2024, and is expected to reach USD 85.19 billion by 2029, growing at a CAGR of 4.60% during the forecast period (2024-2029).

- Factors such as the availability of abundant natural gas reserves and the lower cost compared to other fossil fuel types are expected to supplement the demand for natural gas from multiple end-users, including power generation. This, in turn, is expected to boost the gas pipeline segment during the forecast period.

- However, the global shift toward renewable sources for electricity generation poses a huge threat to the oil and gas demand, which is likely to be a major challenge for the growth of onshore oil and gas pipeline installations during the forecast period.

- Nevertheless, the rise in onshore exploration and production projects is expected to create excellent opportunities for the market players in the years to come, as these projects are paving the way for the pipeline industry to grow more.

- Asia-Pacific is expected to witness significant growth during the forecast period, with the majority of the demand coming from countries like China, India, etc.

Onshore Oil And Gas Pipeline Industry Segmentation

Onshore pipelines are used in all three sectors for oil and gas transportation, i.e., upstream, downstream, and midstream. They are vulnerable to damage and, therefore, required to perform regular maintenance, repair, and overhaul of pipelines. These pipelines are mostly utilized for commercial activities such as terminals, stations, receiving facilities, refineries, retail outlets, city gas stations, and materials such as oil or gas delivered to various end-users.

The onshore oil & gas pipeline market is segmented by type and geography. By type, the market is segmented into oil pipelines and gas pipelines. The report also covers the market size and forecasts for the onshore oil & gas market across major countries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Type | |

| Oil Pipeline | |

| Gas Pipeline |

| Geography | |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

|

Onshore Oil And Gas Pipeline Market Size Summary

The onshore oil and gas pipeline market is poised for growth, driven by the increasing demand for natural gas and crude oil, particularly in the Asia-Pacific region. This growth is supported by the availability of abundant natural gas reserves and its cost-effectiveness compared to other fossil fuels, which is expected to bolster the gas pipeline segment. However, the transition towards renewable energy sources presents a significant challenge to the demand for oil and gas, potentially impacting the expansion of onshore pipeline installations. Despite these challenges, the rise in onshore exploration and production projects offers substantial opportunities for market players, as these initiatives are expected to enhance the pipeline industry's development.

The market landscape is characterized by a fragmented structure with key players such as Tenaris SA, Essar Group, Jindal SAW Ltd, Europipe GmbH, and TMK Group actively participating. Significant infrastructure developments, such as Iran's Iranian Gas Trunk Line and Australia's Barossa gas pipeline project, are set to meet the growing natural gas demand. Additionally, countries like India are investing heavily in expanding their gas pipeline infrastructure to increase the share of natural gas in their energy mix. These developments, coupled with the increasing energy consumption in emerging economies, are anticipated to drive the global onshore oil and gas pipeline market's growth during the forecast period.

Onshore Oil And Gas Pipeline Market Size - Table of Contents

-

1. MARKET OVERVIEW

-

1.1 Introduction

-

1.2 Market Size and Demand Forecast in USD billion, till 2029

-

1.3 Installed Pipeline Historic Capacity and Forecast in Kilometers, till 2029

-

1.4 Inter-Regional Pipeline Import Capacity in BSCM, till 2029

-

1.5 Inter-Regional Pipeline Export Capacity in BSCM, till 2029

-

1.6 Brent Crude Oil and Henry Hub Spot Prices Forecast, till 2029

-

1.7 Onshore CAPEX Forecast in USD billion, till 2029

-

1.8 Recent Trends and Developments

-

1.9 Government Policies and Regulations

-

1.10 Market Dynamics

-

1.10.1 Drivers

-

1.10.1.1 Availability of abundant natural gas reserves and the lower cost compared to other fossil fuel types

-

1.10.1.2 Growing investments to increase production to fulfill global demand

-

-

1.10.2 Restraints

-

1.10.2.1 The global shift toward renewable sources for electricity generation

-

-

-

1.11 Supply Chain Analysis

-

1.12 Porter's Five Forces Analysis

-

1.12.1 Bargaining Power of Suppliers

-

1.12.2 Bargaining Power of Consumers

-

1.12.3 Threat of New Entrants

-

1.12.4 Threat of Substitutes Products and Services

-

1.12.5 Intensity of Competitive Rivalry

-

-

1.13 Investment Analysis

-

-

2. MARKET SEGMENTATION

-

2.1 Type

-

2.1.1 Oil Pipeline

-

2.1.2 Gas Pipeline

-

-

2.2 Geography

-

2.2.1 North America

-

2.2.1.1 United States

-

2.2.1.2 Canada

-

2.2.1.3 Rest of North America

-

-

2.2.2 Europe

-

2.2.2.1 Norway

-

2.2.2.2 United Kingdom

-

2.2.2.3 France

-

2.2.2.4 Spain

-

2.2.2.5 NORDIC

-

2.2.2.6 Russia

-

2.2.2.7 Rest of Europe

-

-

2.2.3 Asia Pacific

-

2.2.3.1 China

-

2.2.3.2 India

-

2.2.3.3 Indonesia

-

2.2.3.4 Malaysia

-

2.2.3.5 Vietnam

-

2.2.3.6 Thailand

-

2.2.3.7 Rest of Asia Pacific

-

-

2.2.4 South America

-

2.2.4.1 Brazil

-

2.2.4.2 Argentina

-

2.2.4.3 Colombia

-

2.2.4.4 Rest of South Africa

-

-

2.2.5 Middle East and Africa

-

2.2.5.1 United Arab Emirates

-

2.2.5.2 Saudi Arabia

-

2.2.5.3 South Africa

-

2.2.5.4 Egypt

-

2.2.5.5 Nigeria

-

2.2.5.6 Qatar

-

2.2.5.7 Rest of Middle East and Africa

-

-

-

Onshore Oil And Gas Pipeline Market Size FAQs

How big is the Onshore Oil And Gas Pipeline Market?

The Onshore Oil And Gas Pipeline Market size is expected to reach USD 68.03 billion in 2024 and grow at a CAGR of 4.60% to reach USD 85.19 billion by 2029.

What is the current Onshore Oil And Gas Pipeline Market size?

In 2024, the Onshore Oil And Gas Pipeline Market size is expected to reach USD 68.03 billion.