Market Trends of Oman Oil and Gas Pipeline Industry

This section covers the major market trends shaping the Oman Oil & Gas Pipeline Market according to our research experts:

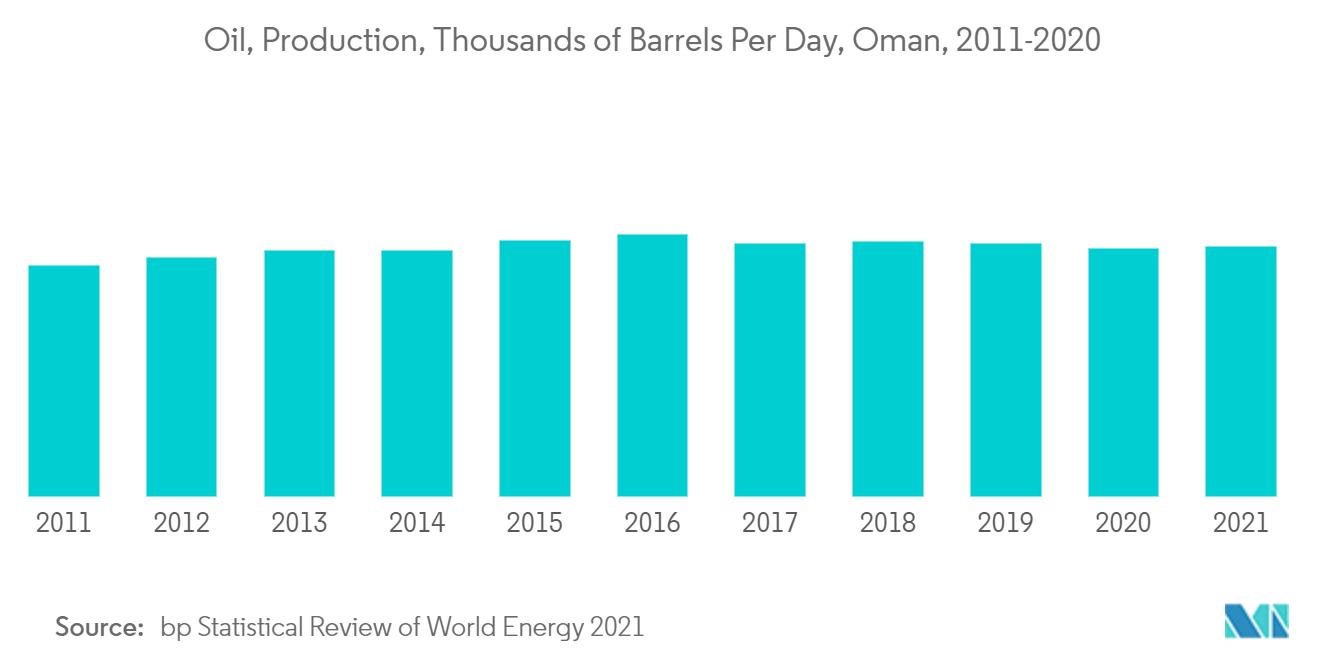

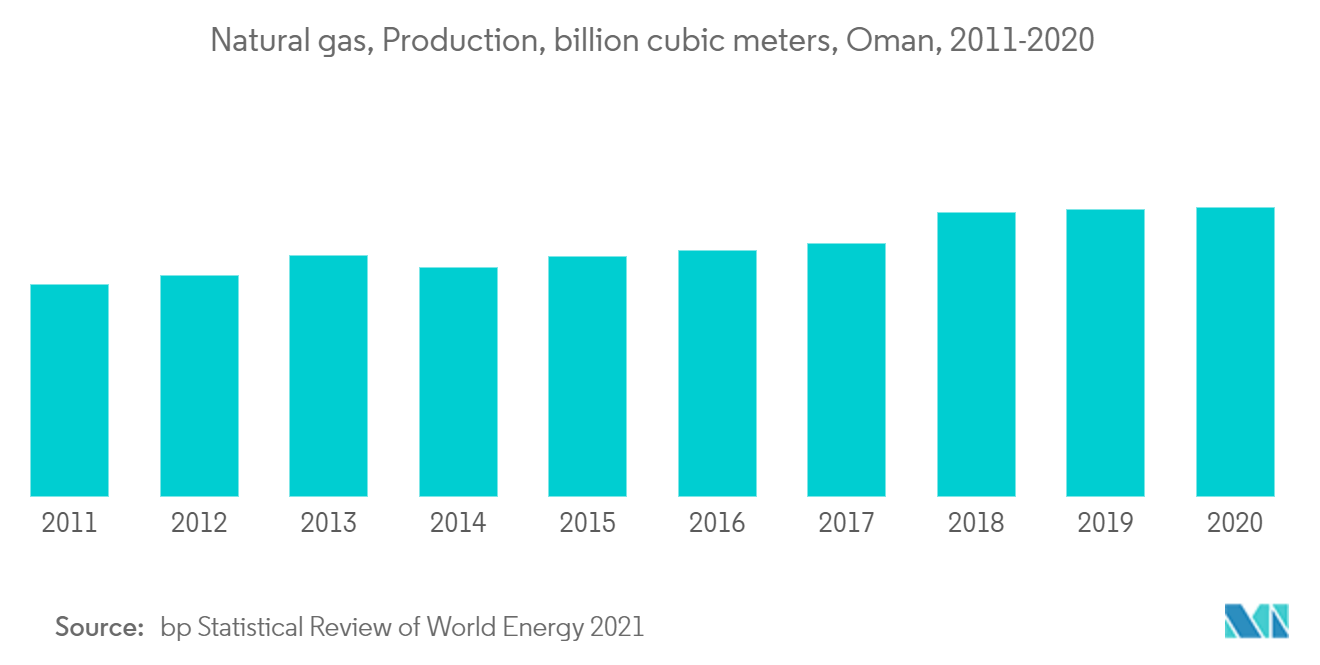

The Gas Pipeline Segment to Dominate the Market

- In Oman, natural gas production has increased from 25 billion cubic meters in 2010 to 36.9 billion cubic meters in 2020. Furthermore, natural gas consumption also increased significantly over the last decade. In 2010 the natural gas consumption was 16.4 billion cubic meters, and in 2020 it was around 25.9 billion cubic meters.

- This increased focus on natural gas production and consumption is due to higher demand for natural gas from various end-users such as residential, commercial, and industrial. This trend is expected to continue in the coming years and is anticipated to boost investment in the gas pipeline infrastructure.

- Increased awareness about the negative effects of carbon and greenhouse gas emissions on the environment as well as humans is also propelling the investment in natural gas infrastructure in Oman.

- Oil & gas companies are more focused on the exploration of natural gas in Oman. For instance, in 2010, Oman had natural gas reserves of around 0.5 trillion cubic meters, and in 2020 the natural gas reserves were 0.7 trillion cubic meters, which is approximately 40% higher than in 2010.

- Thus rising investment in natural gas infrastructure coupled with higher demand from the end-users is expected to drive the gas pipeline segment in the Oman oil and gas pipeline market in the near future.

Understand The Key Trends Shaping This Market

Download PDF

Government's Favorable Policies to Promote Oil and Gas Industry

- Oman is one of the leading oil and natural gas producers in the Middle East outside the OPEC. The oil and gas industry is a critical part of its economic performance. In 2020, the oil and gas sector accounted for 26.2% of G.D.P. Furthermore, oil and gas exports represent about 60% of Oman's merchandise exports. Moreover, Oman's government derives around 70% of its annual budget from oil and gas industry revenues in the form of taxation, and the government also has joint ownership of some of the oil and gas fields which are located in the country.

- Thus the government of Oman is focusing on the development of the oil and gas industry in the country. The state-owned Petroleum Development Oman (P.D.O.) owns most of the country's oil reserves.

- In 2019, Oman created a state energy company named OQ. The company integrates various government-owned upstream, midstream, and downstream oil and gas entities. The companies that merged include the Oman Oil Company S.A.O.C. (O.O.C.), Oman Oil Refineries & Petroleum Industries Company (Orpic), Oman Oil Company Exploration & Production (O.O.C.E.P.), Oman Gas Company (O.G.C.), Duqm Refinery & Petrochemical Industries (D.R.P.I.C.), Salalah Methanol (S.M.C.), Oman Trading International (O.T.I.), Oxo intermediates and derivatives producer OXEA, and Salalah Liquefied Petroleum Gas. Furthermore, this group owns four producing blocks, one non-producing block, and five exploration blocks in onshore and offshore fields.

- Moreover, in December 2020, the government created Energy Development Oman to represent the government's stake in P.D.O. and raise financing for oil and gas projects for future development. Furthermore, the government is also aiming to expand its downstream oil capabilities, such as refining and petrochemicals.

- The government also introduce new laws to improve the business environment and investment climate and boost foreign direct investment in the country, particularly in the oil and gas industry. A few of the laws are as follows:-

- Foreign Capital Investment Law (Sultani Decree - 50/2019) (F.C.I.L.)

- Privatisation Law (Sultani Decree - 51/2019)

- Public Private Partnership Law (Sultani Decree - 52/2019)

- Bankruptcy Law (Sultani Decree - 53/2019)

- Due to these activities and reforms by the government, the oil and gas industry is expected to witness higher demand in the near future, which, the intern, would lead to leading the oil and gas pipeline market in the forecast period.