Oman Foodservice Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 1.63 Billion |

| Market Size (2030) | USD 2.33 Billion |

| Growth Rate (2025 - 2030) | 7.42% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Oman Foodservice Market Analysis by Mordor Intelligence

The Oman foodservice market size reached USD 1.63 billion in 2025 and is projected to advance to USD 2.33 billion by 2030, reflecting a 7.42% CAGR. Steady economic diversification under Vision 2040, rapid tourism infrastructure development, and supportive fiscal incentives together underpin this upward trajectory. Growing disposable incomes, expanding urban middle-class households, and a vibrant youth demographic sustain transaction volumes across dine-in, takeaway, and delivery channels. Mandatory e-payment compliance has accelerated digital ordering, allowing operators to unlock new customer touchpoints and optimize working-capital cycles. Simultaneously, robust food security programs strengthen local supply chains, tempering price volatility and enabling health-driven menu reformulation. While rising labor, energy, and rental costs pose structural headwinds, operators equipped with technology, local sourcing strategies, and compliance agility remain well-positioned to capture incremental demand across the Oman foodservice market.

Key Report Takeaways

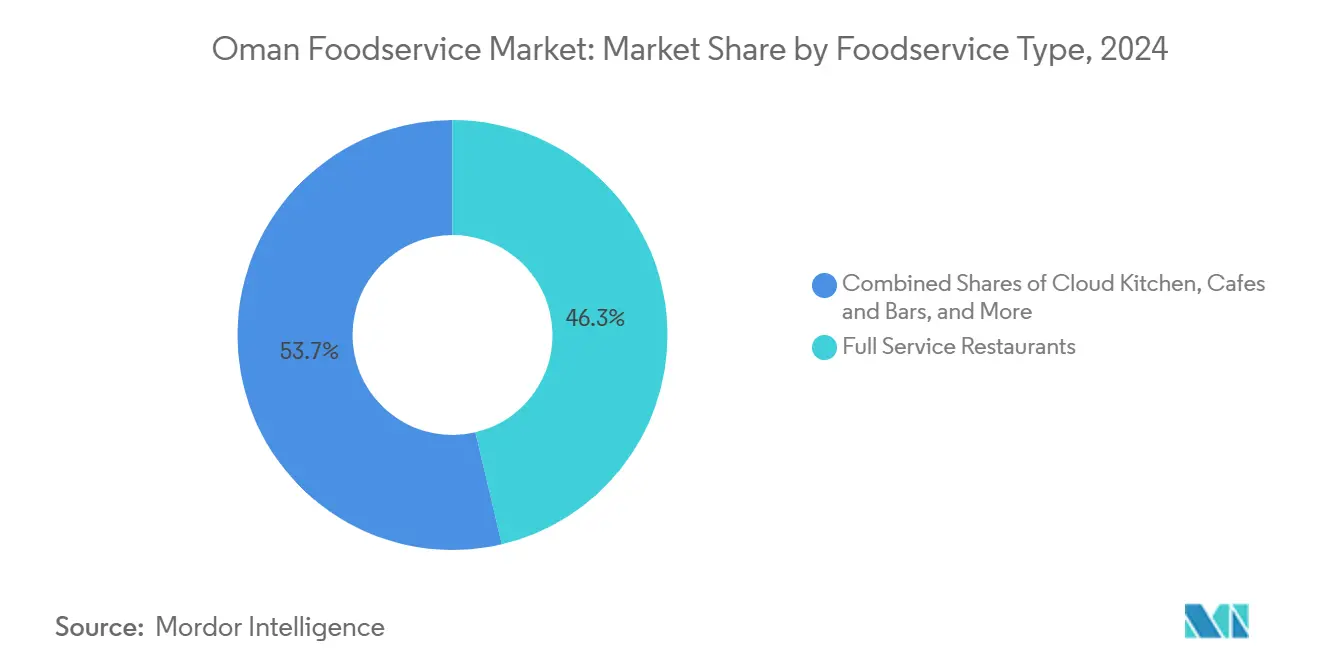

- By foodservice type, full-service restaurants led with 46.32% revenue share in 2024, whereas cloud kitchens are forecast to expand at a 17.02% CAGR through 2030.

- By outlet, independent operators held 57.25% of the Oman foodservice market share in 2024; chained outlets are advancing at an 8.55% CAGR to 2030.

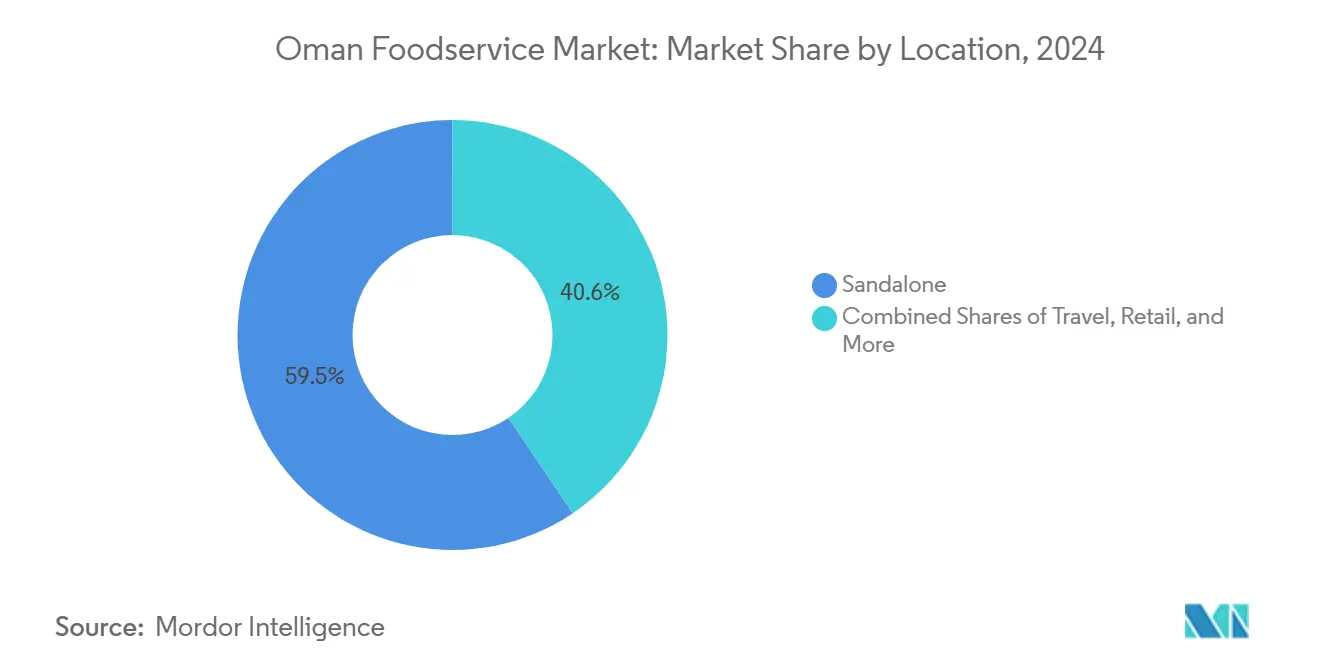

- By location, standalone venues accounted for 59.45% of the Oman foodservice market size in 2024, while travel-linked venues are growing at a 10.68% CAGR through 2030.

- By service type, dine-in commanded 68.02% of 2024 spend, yet delivery services are progressing at an 11.64% CAGR on the back of enforced e-payment adoption.

Oman Foodservice Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding tourism industry with strong government promotion of hospitality and leisure activities | +2.1% | National, concentrated in Muscat, Salalah, Nizwa | Long term (≥ 4 years) |

| Rising disposable income and urbanization | +1.8% | Urban centers: Muscat, Sohar, Sur | Medium term (2-4 years) |

| Increasing health and nutrition awareness encouraging demand for clean-label and locally sourced menu items | +1.2% | National, urban-led adoption | Medium term (2-4 years) |

| Growth of digital transformation and online food ordering | +1.5% | National, accelerated in Muscat metropolitan | Short term (≤ 2 years) |

| Introduction of government incentives, tax relief, and food security programs | +0.9% | National, special focus on agricultural regions | Long term (≥ 4 years) |

| Growing café culture and QSR growth among young consumers | +1.1% | Urban centers, mall locations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding tourism industry with strong government promotion of hospitality and leisure activities

Oman's tourism sector transformation under Vision 2040 creates unprecedented demand for foodservice establishments across multiple venue types. The government committed over OMR 3 billion (USD 7.8 billion) in tourism infrastructure investments by 2040, with major projects including the Oman Botanic Garden, Masirah Island development, and expanded cruise terminal facilities. This infrastructure expansion directly correlates with the 10.68% CAGR projected for travel-linked foodservice locations, as airports, hotels, and tourist attractions require diverse dining options. The multiplier effect extends beyond direct tourism venues, as increased visitor flows stimulate demand for standalone restaurants and delivery services in urban centers. International visitor arrivals recovery post-2024 amplifies this trend, particularly benefiting full-service restaurants that can accommodate group dining and cultural food experiences. The strategic focus on positioning Oman as a premium Middle Eastern destination necessitates elevated foodservice standards, creating opportunities for operators who can deliver authentic Omani cuisine alongside international offerings.

Growth of digital transformation and online food ordering

Oman's Ministry has implemented a mandate requiring e-payment systems in restaurants and cafés, signifying a crucial step in advancing the digital transformation of the foodservice sector. This regulatory measure eliminates cash-only operations and establishes a standardized digital payment infrastructure, fostering a more streamlined and efficient payment process. The policy has created a competitive advantage for operators adept at leveraging technology, while traditional establishments that face challenges in adopting digital systems may struggle to remain competitive. Regional players such as Talabat, along with international platforms, are now better positioned to expand their merchant networks at an accelerated pace, as the removal of regulatory barriers facilitates broader adoption of online food ordering. Furthermore, this initiative aligns with the Gulf Cooperation Council's (GCC) overarching trend toward cashless societies, enhancing Oman's foodservice sector's integration with regional digital payment ecosystems and loyalty programs. By addressing these regulatory challenges, the policy not only supports the sector's growth but also strengthens its alignment with the region's evolving digital economy.

Increasing health and nutrition awareness encouraging demand for clean-label and locally sourced menu items

Oman's Ministry of Health, through initiatives like nutrition surveys and food database updates, is responding to the rising consumer appetite for healthier dining. Backing the WHO's[1]World Health Organization, “WHO plan to eliminate industrially-produced trans-fats from global food supply,” who.int global push to eliminate trans-fats, Omani health authorities are urging foodservice operators to revamp their menus and seek alternative ingredients. This regulatory landscape favors establishments boasting clean-label credentials and locally-sourced ingredients. With Oman achieving 83% self-sufficiency in tomato production and 97% in dates, the opportunity for authentic local sourcing is evident. Beyond mere compliance, there's a palpable shift in consumer preferences, especially among urban millennials and Gen Z, who demand nutritional transparency. Quick-service restaurants are feeling the heat to diversify beyond their traditional fried offerings. In contrast, full-service venues have the chance to stand out with farm-to-table concepts, capitalizing on Oman's bolstering agricultural self-sufficiency. The interplay of health regulations and local sourcing not only meets consumer demands but also carves out a sustainable competitive edge for operators adept at weaving both into their offerings.

Introduction of government incentives, tax relief, and food security programs

The Food Security Lab 2024 has earmarked over OMR 10 million for 30 projects, representing the most extensive government initiative in Oman's food ecosystem. This program is expected to directly influence foodservice procurement and cost structures. Additionally, the Oman Investment Authority has unified Nitaj and Food Development Oman, creating a single entity aimed at strengthening the nation's food security. This consolidation is likely to improve procurement capabilities, potentially stabilizing ingredient costs for foodservice operators. The Ministry has also initiated a plantation drive, distributing over 21,000 date palm seedlings and 100,000 fruit tree seedlings, thereby expanding local sourcing options for restaurants seeking authentic Omani ingredients. Independent outlets are expected to benefit significantly by establishing direct relationships with local producers, while chained operators gain access to cost-effective alternatives to imported ingredients. Furthermore, the program's emphasis on increasing wheat production from 2,000 to over 10,000 tonnes annually aims to reduce dependence on volatile international grain markets, stabilizing costs for bakeries and pizza outlets.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High reliance on food imports | -1.4% | National, acute in urban centers | Medium term (2-4 years) |

| Rising labor costs and limited availability of skilled hospitality professionals | -1.8% | National, concentrated in hospitality zones | Short term (≤ 2 years) |

| Food price volatility and logistics challenges | -1.1% | National, supply chain dependent areas | Short term (≤ 2 years) |

| Increasing energy and rental costs in urban centers | -0.7% | Muscat, Sohar, Sur metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High reliance on food imports

Oman's significant reliance on food imports makes its foodservice sector susceptible to global price volatility and supply chain disruptions, despite government efforts to improve food security. Although Oman has achieved notable self-sufficiency rates—158% for fish, 97% for dates, and 83% for tomatoes—most processed foods, grains, and specialty ingredients still depend on imports. This dependency creates challenges, particularly for international cuisine restaurants and chain operators that require standardized ingredients to maintain menu consistency. From January 2025, the introduction of digital tax stamps on excisable beverages will increase compliance costs and may cause supply delays, as each imported beverage unit must include serialized markers. Geopolitical tensions and shipping disruptions can quickly escalate ingredient costs, forcing operators to either absorb the financial strain or pass the increases on to price-sensitive consumers. Smaller independent outlets face even greater difficulties, as they often lack the bargaining power to secure favorable import terms or maintain inventory reserves to mitigate supply shocks.

Rising labor costs and limited availability of skilled hospitality professionals

Oman's Ministry of Labour has implemented stricter Omanization requirements, mandating that every private establishment employ at least one Omani. Companies failing to comply now face doubled work permit fees. These measures are expected to significantly impact labor dynamics in the foodservice sector. Additionally, the ministry has expanded the foreign-worker prohibition list by including 30 new professions. Alongside a mandated minimum wage of OMR 325 for Omani nationals, these regulations impose dual challenges: increased labor costs and reduced hiring flexibility. Labor-intensive segments, such as full-service restaurants and large-scale catering, are particularly affected. In these areas, the preparation of specialized international cuisines may now be restricted to Omani nationals. Businesses capable of effectively training and retaining Omani employees are likely to gain a competitive advantage, while those dependent on expatriate culinary expertise may face setbacks. Furthermore, Omanization compliance is now a requirement for securing government contracts, influencing foodservice companies targeting institutional catering opportunities. With stricter inspections in place, non-compliant operators face elevated regulatory risks, potentially leading to disruptions during peak service periods.

Segment Analysis

By Foodservice Type: Cloud Kitchens Disrupt Traditional Models

In 2024, Full Service Restaurants hold a dominant 46.32% market share, highlighting Omani consumers' preference for experiential dining and family-oriented meals. On the other hand, Cloud Kitchens emerge as the fastest-growing segment, achieving an impressive 17.02% CAGR through 2030. This growth is primarily driven by mandatory e-payment compliance, which has facilitated digital ordering. The international expansion of the Omani cloud kitchen brand Hala, now operating in India, Georgia, Jordan, and Qatar, showcases the scalability of this business model. Quick Service Restaurants attract urban youth with the rise of café culture, while Café and Bars leverage the popularity of specialty coffee trends. A notable example is the recent launch of Dose Cafe at Mall of Muscat, which emphasizes its use of 100% Arabica beans and artisanal brewing techniques.

These segment trends reflect significant shifts in consumer behavior and operational strategies. Cloud kitchens' asset-light model appeals to entrepreneurs managing high commercial rents in urban areas, while their digital-first approach aligns with the government's cashless payment mandate. Full-service restaurants, while maintaining their experiential appeal, face the challenge of enhancing their digital capabilities. This is particularly crucial in tourism-heavy regions, where international visitors expect comprehensive dining experiences. The emergence of experiential venues like Muska in Muttrah, which combines artisanal cuisine with pottery classes and photography studios, demonstrates how traditional formats are adapting to stay relevant. Quick Service Restaurants must address the need to balance speed and convenience with the development of health-conscious menus, as regulatory pressures increase to eliminate trans-fats and ensure nutritional transparency.

Note: Segment shares of all individual segments available upon report purchase

By Outlet: Independent Operators Face Consolidation Pressure

In 2024, independent outlets account for 57.25% of Oman's foodservice market, highlighting the country's entrepreneurial culture and strong consumer demand for authentic local experiences. However, chained outlets are growing at a robust 8.55% CAGR, indicating a trend toward consolidation as economies of scale become essential for managing regulatory challenges and rising operational expenses. Regional chains, such as LuLu Group, continue to expand, with the recent opening of their 31st store in Al Mudhaibi, covering 40,000 square feet. This growth demonstrates how established players capitalize on procurement efficiencies and standardized operations. Similarly, international franchises are expanding rapidly, led by operators like M.H. Alshaya, which manages brands such as Starbucks, Chipotle, and Shake Shack across regional markets.

Chained operators hold a competitive edge by effectively absorbing compliance costs related to e-payment systems, Omanization policies, and the implementation of digital tax stamps. Independent outlets, while benefiting from menu flexibility, strong local sourcing relationships, and authentic cultural appeal, face increasing challenges from labor regulations that prioritize Omani employment and restrict certain roles to nationals. The Ministry of Commerce's decision to cancel 3,415 dormant commercial registrations from 1970-1999 eliminates inactive competitors and creates opportunities for active independent operators to secure prime locations. The ability of independent operators to professionalize their operations while maintaining their authentic local charm will be critical to their success in this evolving market.

By Location: Travel Venues Capitalize on Tourism Investment

In 2024, standalone locations hold a significant 59.45% market share, driven by Oman's urban development trends and increasing consumer preference for neighborhood dining. Meanwhile, travel-linked venues are experiencing robust growth, with a 10.68% CAGR. This growth aligns with the government's substantial OMR 3 billion investment in tourism infrastructure, planned through 2040. Airport expansions, new cruise terminals, and landmark projects like the Oman Botanic Garden are creating captive audiences, enabling foodservice operators to secure prime locations within transportation hubs. Leisure venues are also benefiting from mall expansions, such as the Mall of Muscat, which recently introduced specialized outlets like Bubble Lab, offering bubble tea and gelato.

Oman's location segmentation highlights its evolving urban landscape and progressive tourism strategy. Retail venues are under pressure due to changing shopping behaviors and the growth of e-commerce, while lodging-connected outlets are thriving, supported by hotel developments linked to tourism expansion. Standalone locations are focusing on differentiation by emphasizing convenience, sufficient parking, and stronger neighborhood integration. This shift is increasingly important as delivery services reduce the reliance on high foot-traffic areas. The success of travel-linked venues depends on their ability to cater to diverse international tastes while maintaining operational efficiency during peak tourism periods. However, these venues face complex regulatory challenges, needing to comply with both local foodservice regulations and the international standards expected by global travelers.

Note: Segment shares of all individual segments available upon report purchase

By Service Type: Delivery Services Transform Consumer Expectations

Dine-in services maintain 68.02% market dominance in 2024, reflecting Omani cultural preferences for social dining and family meal occasions. However, delivery services are expected to surge at an 11.64% CAGR, accelerated by mandatory e-payment compliance that has standardized digital ordering infrastructure across the market. The growth trajectory aligns with regional trends documented by Mastercard, which identified digital loyalty programs and personalized experiences as key drivers of Middle Eastern restaurant engagement. LuLu Group's e-commerce sales growth of 70% year-over-year, representing 4.5% of retail sales, demonstrates the broader digital transformation affecting food purchasing patterns Zawya.

The service type evolution reflects fundamental changes in consumer behavior and operational capabilities. Takeaway services occupy the middle ground, benefiting from consumers' desire for restaurant-quality food with the convenience and flexibility they offer. Dine-in establishments must enhance their experiential value proposition to justify the time and effort investment compared to delivery alternatives. The integration of loyalty programs, like LuLu's Happiness Loyalty with 5.5 million GCC members, creates cross-channel engagement that bridges physical and digital service modes. Delivery services face pressure to maintain food quality during transport while managing commission structures that can erode profitability. The segment's growth depends on continued investment in delivery infrastructure, cold-chain logistics, and packaging innovations that preserve food integrity during the final mile to consumers.

Geography Analysis

Oman's foodservice market demonstrates growth patterns that align with the nation's urban expansion and investments in tourism infrastructure. The Muscat metropolitan area dominates market activity, driven by high disposable incomes, a strong international business presence, and government efforts to position the capital as a regional hub for commerce and tourism. Oman's strategic location at the crossroads of Europe, Asia, and Africa offers unique opportunities for foodservice operators to cater to diverse expatriate communities and international business travelers. Government initiatives under Vision 2040, such as the OMR 3 billion tourism investment program, focus on developing key regions like Salalah for eco-tourism, Nizwa for cultural heritage, and coastal areas for cruise tourism[2]Social Protection Fund, "Oman Vision 2040 Report", www.spf.gov.om. The expansion of the Sohar industrial zone increases demand for institutional catering and quick-service options for workers, while Duqm's development as a logistics hub creates new market segments for foodservice operators.

Variations in consumer preferences and purchasing power across Oman's governorates result in distinct market dynamics. According to the World Bank data from 2024, Oman's current GDP was USD 106.94 billion[3]World Bank Open Data, " GDP-Oman", www.data.worldbank.org. Urban centers like Muscat and Sohar show greater acceptance of international cuisines and premium pricing, whereas traditional regions prefer authentic Omani and regional Arab dishes. Government agricultural initiatives, including the Al Najd Agricultural City project spanning over 54,000 acres, enhance local sourcing opportunities, benefiting restaurants that emphasize farm-to-table concepts. Coastal regions capitalize on Oman's 158% self-sufficiency in fish production to support seafood-focused establishments, while interior regions leverage 97% self-sufficiency in date production and traditional cuisine. Improved transportation infrastructure, such as road networks connecting remote areas to urban centers, is gradually extending the foodservice market's reach beyond traditional population hubs.

The geographic expansion of foodservice operations presents both opportunities and challenges shaped by government policies and infrastructure development. The Ministry of Commerce's restriction of 123 commercial activities, including mobile coffee shops and specialized food retail, to Omani nationals creates barriers for foreign operators while protecting opportunities for local entrepreneurs. However, the Capital Market Incentives Program, which reduces corporate tax rates from 15% to 5-10% for qualifying investments, encourages expansion in designated development zones. The Oman Investment Authority's USD 500 million joint fund with Turkey's OYAK focuses on agriculture and food sectors, potentially accelerating foodservice infrastructure development in emerging regions. Energy costs are a critical factor for geographic expansion, as new commercial electricity tariffs of 25 baisa per kWh impact operational economics, particularly for energy-intensive operations like large-scale kitchens and refrigeration systems.

Competitive Landscape

Top Companies in Oman Foodservice Market

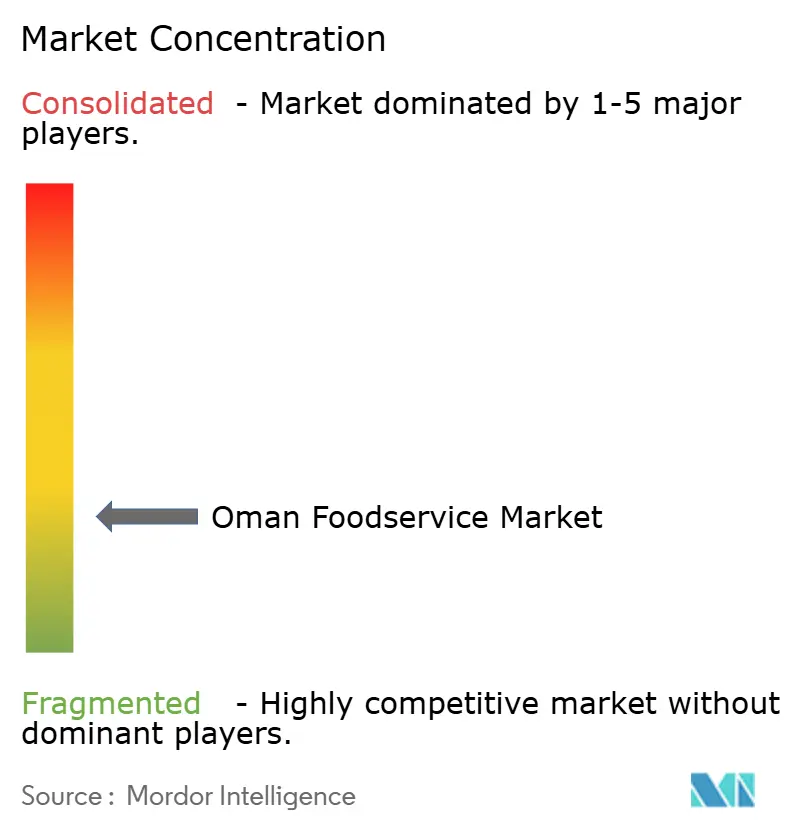

The Oman foodservice market exhibits moderate fragmentation with a concentration score of 3 out of 10, creating a competitive environment where no single player dominates, but established regional operators maintain significant advantages through scale and brand recognition. This fragmentation reflects the market's evolution from traditional family-owned establishments toward more sophisticated franchise and chain operations, while regulatory changes increasingly favor operators with robust compliance capabilities and local partnerships. The competitive dynamics are reshaping as mandatory e-payment systems eliminate cash-only operators and Omanization requirements create barriers for businesses dependent on expatriate management.

Technology adoption becomes a key differentiator, with successful operators leveraging digital ordering platforms, loyalty programs, and supply chain management systems to achieve operational efficiency and customer engagement. Strategic patterns emerge around three primary competitive approaches: regional expansion by established GCC players, international franchise development, and local entrepreneurship focused on authentic Omani cuisine. Companies like LuLu Group demonstrate the regional expansion model, opening their 31st Oman store while simultaneously expanding e-commerce capabilities that grew 70% year-over-year Times of Oman.

International franchisors like M.H. Alshaya leverage their multi-brand portfolio including Starbucks, Chipotle, and Shake Shack to capture diverse consumer segments, while local operators like the Omani-origin Hala cloud kitchen brand successfully expand internationally. White-space opportunities exist in health-focused concepts, experiential dining formats, and technology-enabled service models, particularly as government food security initiatives create new supply chain advantages for operators who can integrate local sourcing with modern foodservice delivery. The competitive landscape increasingly rewards operators who can navigate complex regulatory requirements while delivering authentic experiences that resonate with both local consumers and international visitors.

Oman Foodservice Industry Leaders

-

Al Daud Restaurants LLC

-

Americana Restaurants International PLC

-

Jawad Business Group

-

Khimji Ramdas

-

LuLu Group International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tanatan, a renowned modern Indian restaurant brand, opened a new restaurant in Oman. The restaurant offers various Indian cuisines and cocktails along with a live music experience.

- May 2025: The Lux Collective, in partnership with Adanté Realty, announced the official launch of SOCIO By The Lux Collective, the first hotel and branded residences development in Oman’s Sultan Haitham City.

- April 2025: Nobu Hospitality announced its expansion into Oman with the launch of the Nobu Hotel, Restaurant, and Residences Muscat, a major luxury mixed-use development located on Yiti Beach. The destination featured an 80-room Nobu Hotel, a signature Nobu Restaurant, a full-service spa and fitness center, multiple swimming pools, and a Nobu-style beach club, alongside a limited collection of branded residences.

- December 2024: Em Sherif made its debut in Oman with the opening of its flagship restaurant at The St. Regis Al Mouj Muscat Resort. The Muscat restaurant, led by Executive Head Chef Yasmina Hayek, offers a curated menu showcasing both traditional and contemporary dishes

Oman Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Café and Bars | By Cuisine | Bars & Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee & Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Café and Bars | By Cuisine | Bars & Pubs |

| Café | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee & Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Sandalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms