OLED Microdisplay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

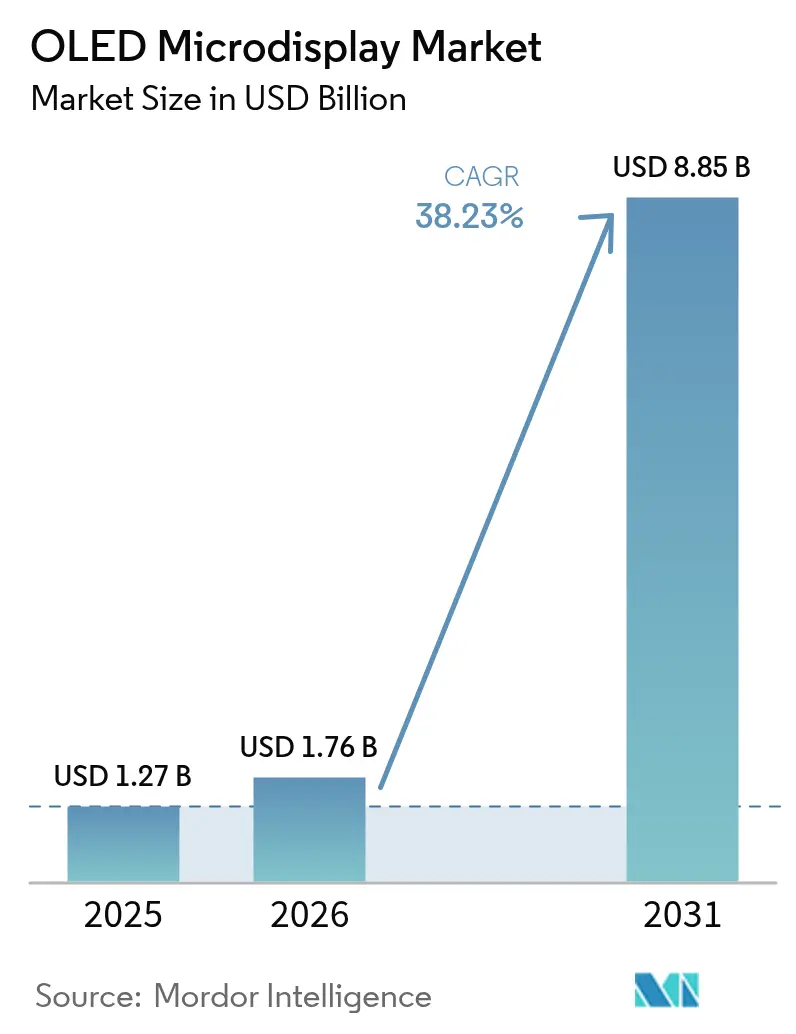

| Market Size (2026) | USD 1.76 Billion |

| Market Size (2031) | USD 8.85 Billion |

| Growth Rate (2026 - 2031) | 38.23% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

OLED Microdisplay Market Analysis by Mordor Intelligence

oled microdisplay market size in 2026 is estimated at USD 1.76 billion, growing from 2025 value of USD 1.27 billion with 2031 projections showing USD 8.85 billion, growing at 38.23% CAGR over 2026-2031. Robust demand for compact, high-resolution near-eye panels in augmented and virtual reality headsets, military helmet systems and premium automotive head-up displays is accelerating volume growth. Direct patterning and tandem-stack architectures are lifting brightness ceilings toward 60,000 nits while cutting power draw, strengthening the technology’s position against emerging MicroLED. Parallel capacity expansions at Chinese OLED-on-Silicon foundries are lowering unit costs and shortening lead times, which encourages broader consumer-electronics adoption. Strategic acquisitions—most notably Samsung Display’s 2024 purchase of eMagin—are pushing advanced process know-how into high-volume manufacturing lines, widening the performance gap with late-entry competitors

Key Report Takeaways

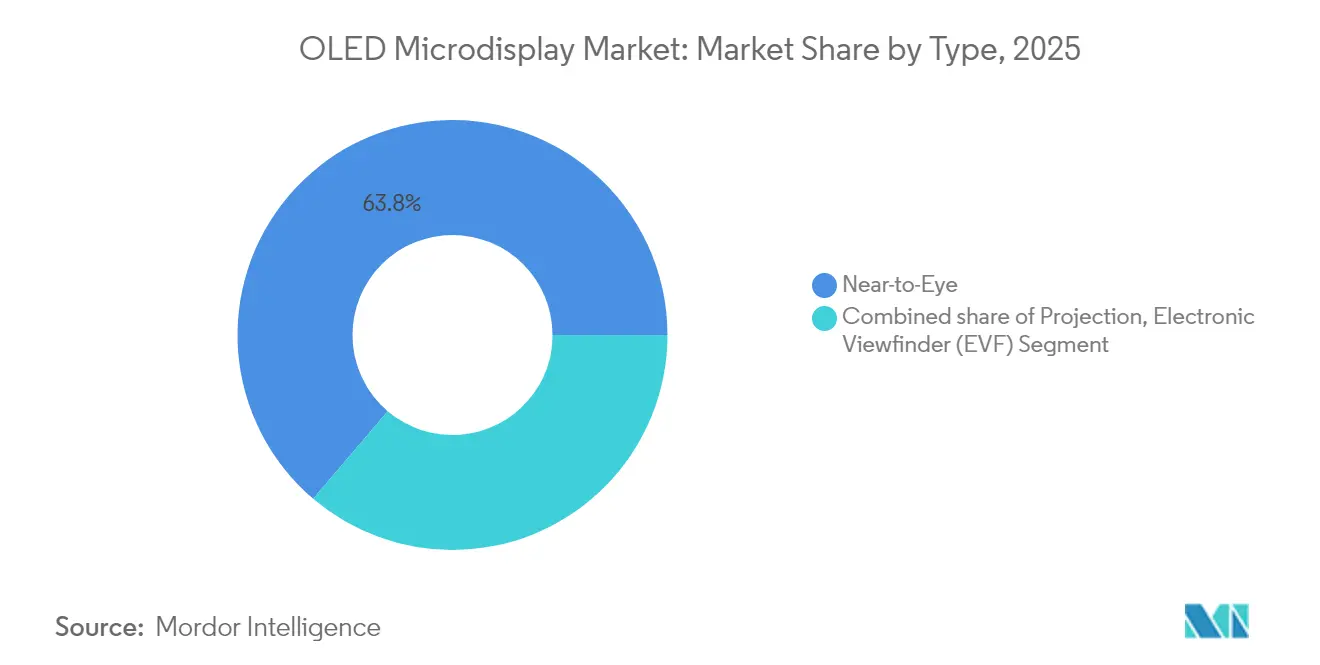

- By type, Near-to-Eye devices held 63.78% of oled microdisplay market share in 2025, while Electronic Viewfinders are projected to expand at a 40.15% CAGR through 2031.

- By technology, RGB OLED-on-Silicon led with 54.62% revenue share in 2025; the White OLED + Color Filter route is forecast to grow at 41.85% CAGR to 2031.

- By resolution, the HD (720p) tier accounted for 35.42% of the oled microdisplay market size in 2025; Above FHD (2K–4K+) is the fastest-growing tier at 40.7% CAGR.

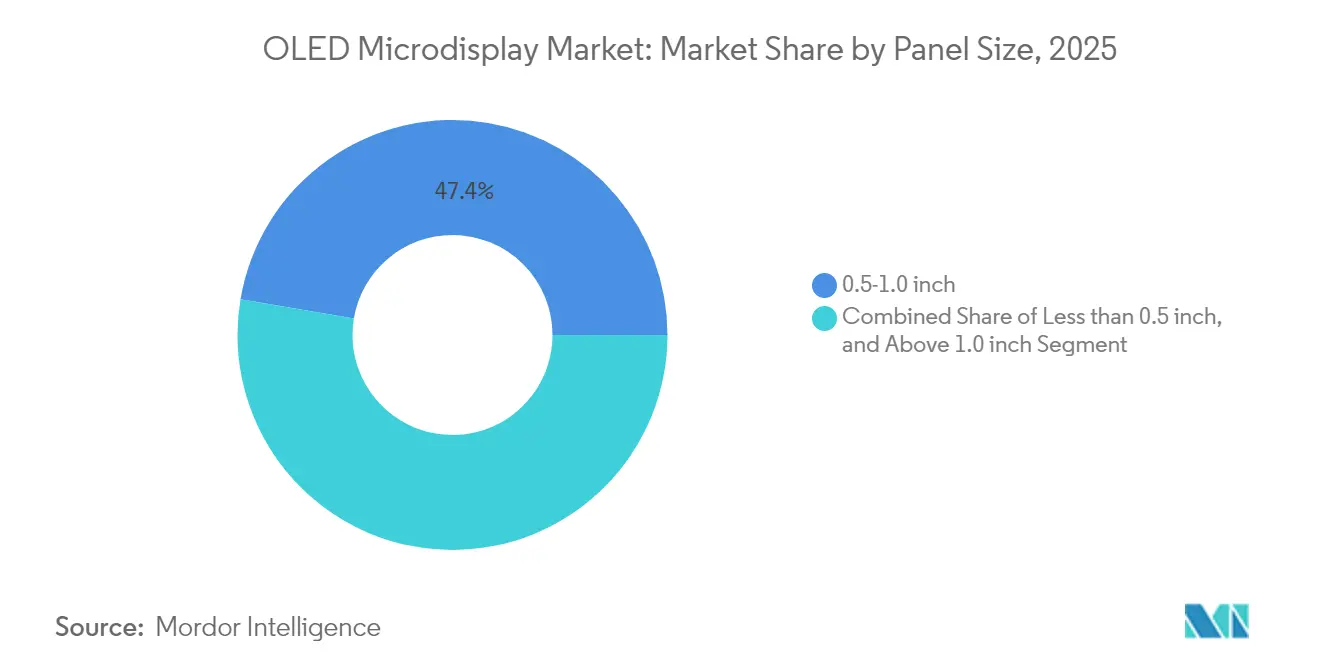

- By panel size, 0.5-1.0 inch modules commanded 47.35% share of the oled microdisplay market size in 2025, while sub-0.5 inch units are advancing at 38.05% CAGR.

- By end-user, Consumer Electronics generated 50.46% revenue in 2025; Automotive applications are set to rise at 39.7% CAGR between 2026-2031.

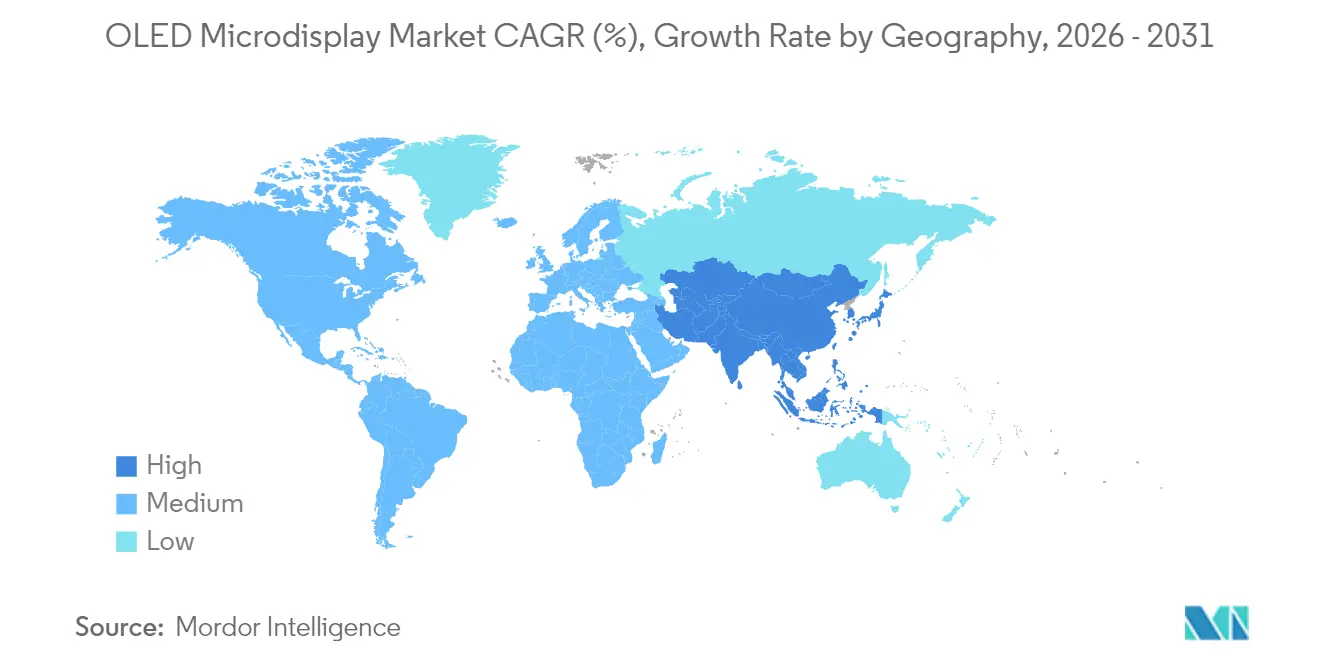

- By geography, Asia Pacific dominated with 56.64% share in 2025; the Middle East & Africa region is projected to grow at 40.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global OLED Microdisplay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of OLED-on-Silicon (OLEDoS) Capacity by Chinese Foundries | +8.5% | Asia Pacific, with spillover to North America | Medium term (2-4 years) |

| Accelerated Adoption of MicroOLED in Military Helmet-Mounted Displays across North America | +6.2% | North America | Short term (≤ 2 years) |

| Automotive OEM Integration of AR Head-Up Displays Using MicroOLED Panels in Europe | +7.8% | Europe, with spillover to North America | Medium term (2-4 years) |

| Surge in High-End Mirrorless Camera EVFs in Japan & South Korea | +5.4% | Asia Pacific | Short term (≤ 2 years) |

| Growing VC Funding for AR/VR Start-ups Focused on OLED Microdisplays in the US & Israel | +4.3% | North America, Middle East | Medium term (2-4 years) |

| Cost-Performance Advantage over MicroLED in <0.7-inch, >3,000 ppi Range | +3.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of OLED-on-Silicon Capacity by Chinese Foundries

Production ramp-ups at BOE, SeeYA and IRay Group are injecting high-volume, high-yield supply into the oled microdisplay market. Foundries are pairing pixel-dense front-planes with newly built silicon backplane lines to raise throughput and tighten process control. IRay’s dedicated backplane investment illustrates a vertical-integration push that reduces outsourcing steps, enhancing cost competitiveness.[1]Ray Group, “IRay Group To Invest In OLED Microdisplay Backplane Production Project,” iraygroup.comThese moves reposition Asia Pacific from a regional to a global supply anchor, challenging Japanese and Korean incumbents on both scale and technology leadership. Wider capacity also stabilizes pricing, encouraging consumer device OEMs to commit to long-term oled microdisplay market orders.

Accelerated Adoption in Military Helmet-Mounted Displays

North American defense programs are rapidly shifting from AMLCD to OLED microdisplays for pilot, ground-troop and night-vision optics. Kopin’s USD 7.5 million award in April 2025 underscores rising demand for ruggedized near-eye modules with superior contrast, zero-motion blur and reduced weight.[2]Kopin Corporation, “Kopin Secures USD 7.5 Million Contract for Helmet Mounted Display Systems Supporting Aircraft Pilots,” Kopin, kopin.comValidation within the F-35 platform demonstrates mission-critical reliability, prompting other programs to specify similar display architectures. Diversification into weapon sights and command-control eyewear spreads procurement risk, making military demand a stable cornerstone of the oled microdisplay market.

Automotive OEM Integration of AR Head-Up Displays

Premium European brands are embedding MicroOLED panels in wide-field head-up systems that overlay navigation and hazard alerts directly on the windshield. Projects such as DashAR show how lightweight near-eye optics can be paired with in-vehicle diagnostics to personalize driver information. Concurrent academic work on pixel-level audio generation suggests a forthcoming fusion of visual and directional sound cues within the same panel substrate. These design advances lift functional value and justify higher panel ASPs, supporting robust growth for the oled microdisplay market in automotive interiors.

Surge in High-End Mirrorless Camera EVFs

Professional photography houses in Japan and South Korea are migrating flagship mirrorless bodies from optical prisms to OLED electronic viewfinders. Real-time exposure simulation, focus peaking and HDR previews demand microdisplays with high color accuracy and fast response. Sony’s imaging group leverages its semiconductor division to co-optimize sensors and oled microdisplay panels, compressing time-to-market for feature upgrades. Rising unit volumes from camera lines offer a secondary demand pillar that balances cyclical swings in AR/VR headset shipments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Moisture-Ingress Encapsulation Challenges for OLEDoS | -3.2% | Global | Medium term (2-4 years) |

| Sub-1,000 cd/m² Brightness Ceiling versus MicroLED | -2.8% | Global | Short term (≤ 2 years) |

| Supply-Chain Concentration in Japan–China Creating Geopolitical Risk | -1.9% | Asia Pacific, North America | Medium term (2-4 years) |

| Rapid Product Obsolescence Increasing OEM Inventory Risk | -1.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Moisture-Ingress Encapsulation Challenges for OLEDoS

The persistent challenge of moisture ingress represents a significant technical barrier to widespread OLED microdisplay adoption, particularly in harsh operating environments like automotive and military applications. Unlike conventional displays, the ultra-compact form factor of microdisplays leaves minimal space for traditional encapsulation methods, creating a fundamental engineering challenge that impacts both manufacturing yield and long-term reliability. Recent innovations from Korean universities have introduced multi-functional encapsulation for fiber-based wearable OLEDs, potentially offering pathways to more robust solutions. The technical complexity of this challenge is compounded by the need for encapsulation solutions that maintain optical clarity while providing hermetic sealing—a balance that becomes increasingly difficult as pixel densities exceed 3,000 ppi. This constraint particularly impacts applications where extended operational lifetimes are expected, such as automotive displays with 10+ year service requirements, creating a competitive opportunity for companies that can develop proprietary encapsulation technologies.

Sub-1,000 cd/m² Brightness Ceiling versus MicroLED

The brightness limitations of OLED microdisplays compared to emerging MicroLED alternatives represent a critical competitive vulnerability, particularly for outdoor augmented reality applications where ambient light can overwhelm displays with insufficient luminance. This technical constraint has created a segmentation in the market, with OLED dominating indoor and controlled-lighting applications while struggling to penetrate high-brightness use cases. The competitive dynamics are evolving rapidly, however, as demonstrated by INT-Tech's breakthrough RGB OLED microdisplay achieving 60,000 nits brightness-a five-fold increase from previous generations. This advancement directly challenges the primary advantage of MicroLED technology, potentially redefining competitive boundaries between the two technologies. The brightness race has significant implications for power consumption and thermal management, with each brightness increase typically requiring disproportionate power increases unless offset by efficiency improvements. This creates a complex optimization challenge for device manufacturers, who must balance brightness requirements against battery life and thermal constraints in wearable form factors.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Near-to-Eye Dominates While EVFs Accelerate

The oled microdisplay market size for Near-to-Eye devices stood at USD 0.81 billion in 2025, equal to 63.78% of total revenue. Sustained shipments to mixed-reality headsets, training goggles and smart helmets anchor demand. Ecosystem investment from platform owners supports annual resolution and brightness upgrades, which in turn lift average selling prices and gross margins.

Electronic Viewfinders contributed a smaller base in 2025, yet their 40.15% CAGR prospect through 2031 signals ample headroom. Professional mirrorless bodies from Sony, Nikon and Canon are standardizing OLED EVFs to deliver lag-free framing and HDR previews. As camera makers streamline model cycles, panel volumes could double within three years, establishing EVFs as a strategic hedge within the oled microdisplay market.

By Resolution: Above FHD Segment Drives Premium Applications

The HD 720p tier held 35.42% of oled microdisplay market share in 2025, balancing acceptable clarity with tight power budgets for mainstream AR viewers. Growth momentum, however, lies in the Above-FHD tier where pixel densities exceed 3,000 ppi. Early 2025 samples from Samsung Display achieve 5,000 ppi and 20,000 nits peak luminance, positioning these panels for enterprise VR and military recon goggles.

A 40.7% CAGR forecast to 2031 for Above-FHD shipments will absorb much of the incremental oled microdisplay market size expansion. Higher bandwidth interfaces and low-latency drivers accompany these panels, creating ancillary silicon demand that benefits integrated suppliers.

By Technology: RGB OLED-on-Silicon Leads Market Transformation

RGB OLED-on-Silicon technology generated 54.62% revenue in 2025, reinforced by direct-patterning processes that eliminate color-filter losses and elevate brightness. Samsung’s acquisition of eMagin secures core intellectual property in this field, allowing rapid scale-up.

White OLED with color filter remains cost-efficient for wearables that prioritize size over peak luminance and is projected to outpace the broader oled microdisplay market at 41.85% CAGR. Tandem-stack research is unlocking current efficiencies above 20 cd/A, narrowing performance gaps with RGB emitters while simplifying mass production.

By Panel Size: Sub-0.5 Inch Segment Accelerates Miniaturization

The 0.5-1.0 inch bracket accounted for 47.35% of 2025 shipments and continues to suit AR spectacles and camera EVFs. Design engineers value the balance between eye-box comfort and industrial-design freedom.

Sub-0.5 inch formats are poised for 38.05% CAGR through 2031 as manufacturers push toward socially acceptable smart-glasses that resemble conventional eyewear. The oled microdisplay market size in this bracket could surpass USD 2.14 billion by 2031 if recent power-efficiency gains from Lumicore flow into high-volume lines.

By End-User: Consumer Electronics Leads While Automotive Accelerates

Consumer Electronics maintained 50.46% share in 2025 on the back of AR/VR headsets and digital imaging devices. These volumes cement baseline fab utilization, permitting aggressive cost optimization.

Automotive integrators are now the fastest-growing customers, with a 39.7% CAGR outlook linked to widescreen augmented head-up displays in electric and premium vehicles. As European OEMs finalize display specifications, multi-year sourcing agreements will create predictable pull for oled microdisplay market suppliers, diversifying revenue away from cyclical consumer cycles.

Geography Analysis

Asia Pacific commanded 56.64% of global revenue in 2025, reflecting the region’s dense network of backplane fabs, emitter suppliers and consumer-device assemblers. Ongoing capacity expansions by Samsung Display and leading Chinese foundries ensure supply continuity, while cross-border joint ventures smooth technology transfer. Government incentives in South Korea and China further lower production costs, sustaining regional leadership.

North America anchors high-specification demand, especially for defense and enterprise-XR deployments that demand ruggedized, high-brightness modules. Venture-capital funding in Silicon Valley and Boston fuels start-ups developing optics and driver ICs, which in turn elevates local sourcing of prototype displays. Defense procurement, led by programs such as the F-35 helmet upgrade, adds a stable layer to North American oled microdisplay market purchases.

Europe focuses on automotive rollouts and high-margin medical visualization. German and French tier-one suppliers work with panel makers to co-design low-latency interfaces for automotive head-up implementations. The Middle East & Africa region, although starting from a small base, is pacing at a 40.6% CAGR due to defense-modernization budgets and luxury-vehicle imports that include advanced AR-HUDs. South America remains largely consumer-oriented, with gradual opportunities arising from local camera production and burgeoning gaming communities.

Competitive Landscape

Roughly five vendors-Samsung Display, LG Display, BOE Technology, Sony Semiconductor Solutions and eMagin-collectively controlled 65% of 2024 revenue. Direct access to maskless lithography, tandem-stack emitters and proprietary backplanes forms a high barrier for late entrants. The Samsung-eMagin deal integrates cutting-edge direct patterning with world-scale OLED lines, accelerating cost reductions at resolutions above 4K.[3]eMagin Corporation, “Samsung Display Completes Acquisition of eMagin,” eMagin, emagin.com

Specialists such as Kopin and Lumicore differentiate through optical-path co-design and power-reduction algorithms, serving military, medical and industrial clients that value bespoke performance. INT-Tech’s 60,000-nits proof-of-concept panel signals that innovation is not confined to conglomerates, keeping competitive pressure high within premium tiers of the oled microdisplay market.[4]OLEDWorks, “OLEDWorks Awarded DoD Contract for High-Brightness OLED Display Development,” OLEDWorks, oledworks.com

Partnership models are proliferating. Automotive suppliers are linking with display houses to codevelop head-up optics and driver software; camera OEMs are entering long-term volume commitments to lock in capacity. The outcome is a moderate-concentration structure that rewards both scale and specialization, with ongoing M&A expected as smaller firms seek capital for pilot-line expansion.

OLED Microdisplay Industry Leaders

-

Microoled SA (Photonis Technologies SAS)

-

Yunnan Olightek Opto-electronic Technology Co. Ltd

-

Winstar Display Co. Ltd

-

Emagin Corporation

-

Kopin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Samsung Display unveiled advanced OLED technologies at Display Week 2025, including a high-resolution microdisplay with 5,000 pixels-per-inch (PPI) in a compact 1.4-inch form factor for next-generation XR devices, with peak brightness up to 20,000 nits. This breakthrough positions Samsung as a leader in high-performance microdisplays for augmented and virtual reality applications.

- May 2025: IRay Group announced a significant investment in OLED microdisplay backplane production, expanding manufacturing capacity for critical components in the OLED microdisplay supply chain. This vertical integration strategy aims to reduce dependency on external suppliers and improve production efficiency.

- April 2025: Kopin Corporation secured a USD 7.5 million contract for helmet-mounted display systems supporting aircraft pilots, highlighting the growing adoption of OLED microdisplays in military applications. This contract reinforces Kopin's position as a key supplier to defense markets.

- April 2025: Lumicore launched an upgraded OLED microdisplay, the LMC071FHDC-A, featuring 3000 nits brightness and a 50% reduction in power consumption compared to its predecessor. This advancement addresses key limitations in OLED technology, particularly for outdoor use cases.

- February 2025: VueReal secured USD 40.5 million in Series C funding to scale its MicroSolid Printing technology for advancing microLED and other micro semiconductor solutions. This investment signals growing interest in alternative microdisplay technologies that may compete with OLED in certain applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the OLED microdisplay market as the value generated from newly manufactured organic light-emitting diode microdisplays that measure below one inch in diagonal and are supplied to near-to-eye devices, projection optics, electronic viewfinders, automotive head-up displays, medical scopes, and rugged industrial wearables. According to Mordor Intelligence, module refurbishments, LCD or LCoS microdisplays, and panels larger than one inch sit outside this scope.

Scope exclusion: legacy LCD, LCoS, and emerging micro-LED microdisplays are not counted.

Segmentation Overview

-

By Type

- Near-to-Eye (NTE)

- Projection

- Electronic Viewfinder (EVF)

-

By Resolution

- SVGA and Below (≤800 × 600)

- XGA (1,024 × 768)

- HD (720p)

- Full HD (1080p)

- Above FHD (2K-4K-Plus)

-

By Technology

- RGB OLED-on-Silicon

- White OLED + Color Filter

- AMOLED on Glass

- Top-Emitting OLED

-

By Panel Size (Diagonal)

- <0.5 inch

- 0.5-1.0 inch

- >1.0 inch

-

By End-User Industry

-

Consumer Electronics

- AR/VR Headsets

- Digital Cameras and Camcorders

- Smart Wearables

-

Automotive

- AR Head-Up Displays

- Side-Mirror Replacement Displays

-

Healthcare

- Surgical and Diagnostic Wearables

- Medical Imaging Devices

-

Industrial and Enterprise

- Smart Glasses

- Machine Vision Systems

-

Aerospace and Defense

- Helmet-Mounted Displays

- Weapon and Thermal Sights

-

Law Enforcement and Security

- Night-Vision Goggles

- Body-Worn Cameras

- Others (Research and Education)

-

Consumer Electronics

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Rest of South America

-

Middle East and Africa

-

Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

Middle East

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with OLED emitter material suppliers, AR/VR headset assemblers, camera module integrators, and automotive Tier-1 HUD engineers across North America, Europe, Japan, China, and South Korea. These conversations clarified true production yields, realistic panel lifetimes, and price-volume breakpoints, filling data gaps uncovered during desk work and anchoring the model's assumptions.

Desk Research

We gathered foundational shipment and pricing cues from tier-one public sources such as the United Nations COMTRADE, the US International Trade Commission's DataWeb, the China Customs Statistics Yearbook, and patent analytics drawn through Questel. Industry guidance from bodies such as the Consumer Technology Association, the Society for Information Display, and the German VDMA provided penetration ratios for AR/VR headsets and automotive HUD fitment. Company filings, investor presentations, and press releases were mined to benchmark average selling prices and capacity ramps, while Dow Jones Factiva tracked quarterly news on capital expenditure announcements and line yield milestones. The sources quoted are illustrative; analysts consulted many others during validation.

Market-Sizing & Forecasting

Mordor analysts first reconstruct global demand through a top-down lens that links annual AR/VR headset shipments, digital camera sales, automotive HUD installations, and surgical endoscope volumes to their typical microdisplay counts and weighted ASPs. Select bottom-up checks, sampled supplier revenue roll-ups and channel inventory audits, are then overlaid to fine-tune totals. Key model variables include headset unit growth, OLED emitter efficiency progression, panel yield improvement rates, regional wage-index adjustments, and currency translation effects. A multivariate regression projects each driver five years forward, after which scenario analysis flexes adoption rates for enterprise XR and automotive HUDs to stress-test the baseline. Where bottom-up inputs are thin, gaps are bridged through averaged peer margins validated in interviews.

Data Validation & Update Cycle

Outputs run through variance filters that flag ±5 percent deviations versus historical price-volume curves and public earnings. Senior analysts review anomalies, and we re-contact respondents if swings exceed tolerance. The report refreshes annually, with an interim update triggered by major capacity announcements or new device launches. Before delivery, an analyst performs a fresh pass to ensure clients receive the latest grounded view.

Why Mordor's OLED Microdisplay Baseline Commands Reliability

Published estimates often diverge because each firm chooses a different mix of display technologies, device categories, and ASP trajectories when sizing this young market.

Key gap drivers include broader technology scope in many studies, varied headset adoption scenarios, and slower currency refresh cadences. External publications place the current-year market anywhere between USD 1.77 billion and USD 2.95 billion, yet they seldom disclose panel yield assumptions or cross-check supplier revenues, which is where Mordor's disciplined reviews add confidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.27 B (2025) | Mordor Intelligence | - |

| USD 2.21 B (2024) | Global Consultancy A | Includes prototypes and micro-LED pilots |

| USD 1.77 B (2024) | Regional Consultancy B | Uses blended LCD-OLED ASPs |

| USD 2.95 B (2024) | Trade Journal C | Counts panels up to two inches |

The comparison shows how broader scopes or blended pricing inflate valuations. By tying volumes to verified end-device production, updating currency and ASPs each quarter, and validating with supplier revenues, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the oled microdisplay market?

The market is worth USD 1.76 billion in 2026 and is tracking a 38.23% CAGR toward USD 8.85 billion by 2031.

Which application segment generates the largest revenue?

Near-to-Eye headsets account for 63.78% of 2025 revenue due to strong AR/VR headset demand.

How fast is the automotive segment expanding?

Automotive integrations, mainly AR head-up displays, are projected to grow at 39.7% CAGR between 2026-2031.

Which region dominates supply?

Asia Pacific holds 56.64% of global revenue and concentrates the majority of OLED-on-Silicon foundry capacity.

What technological hurdle most limits wider adoption?

Moisture-ingress encapsulation remains the foremost reliability challenge, trimming the forecast CAGR by an estimated 3.2%.

Who recently advanced panel brightness leadership?

INT-Tech demonstrated a direct-patterned RGB microdisplay reaching 60,000 nits, signaling rapid progress toward outdoor-readable OLED wearables.

Page last updated on: