Market Overview

| Study Period | 2021 - 2031 |

|---|---|

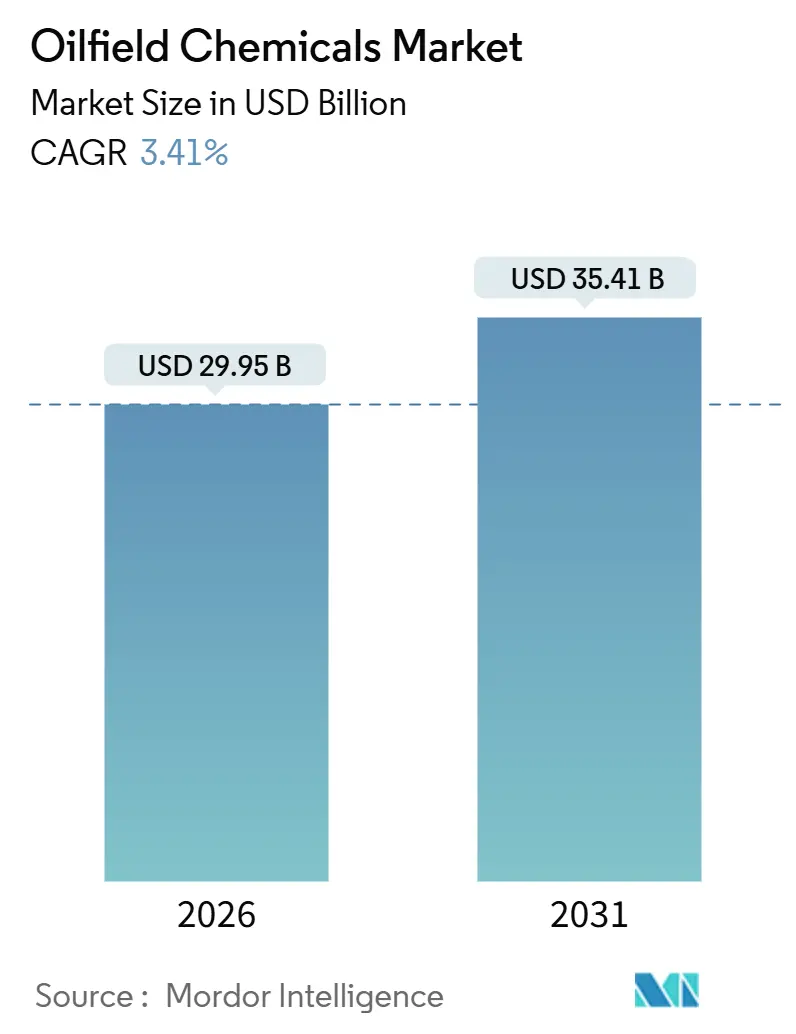

| Market Size (2026) | USD 29.95 Billion |

| Market Size (2031) | USD 35.41 Billion |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

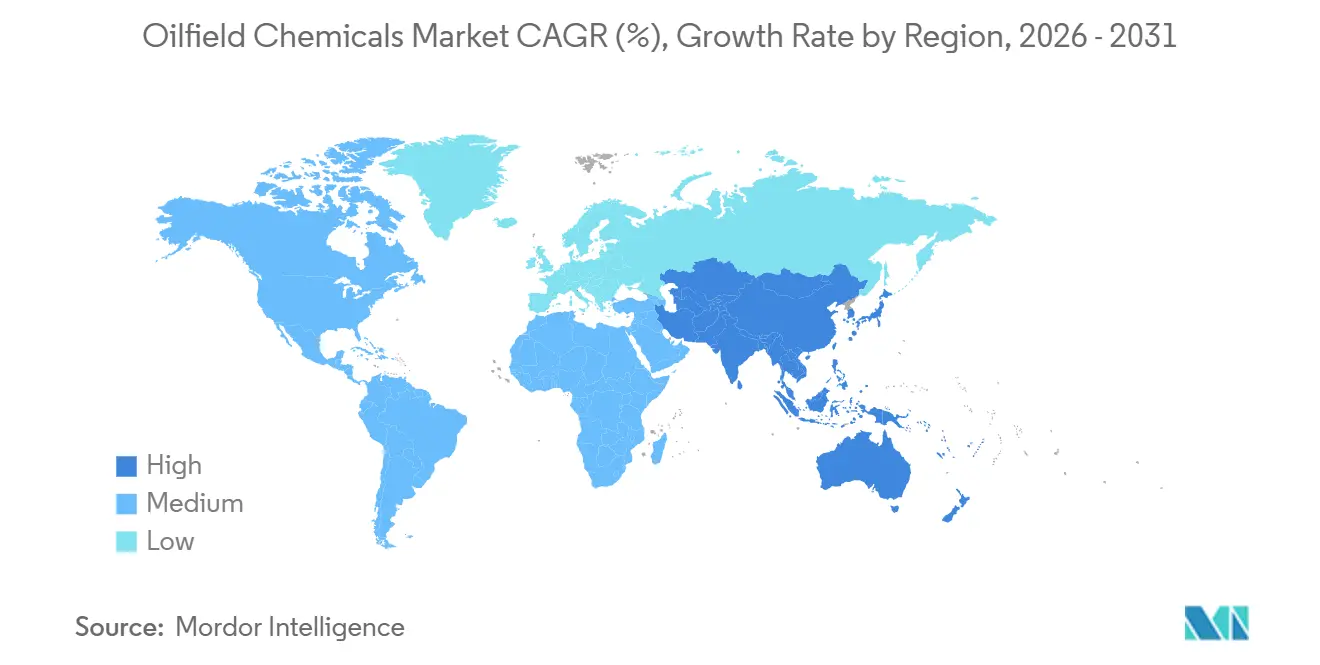

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

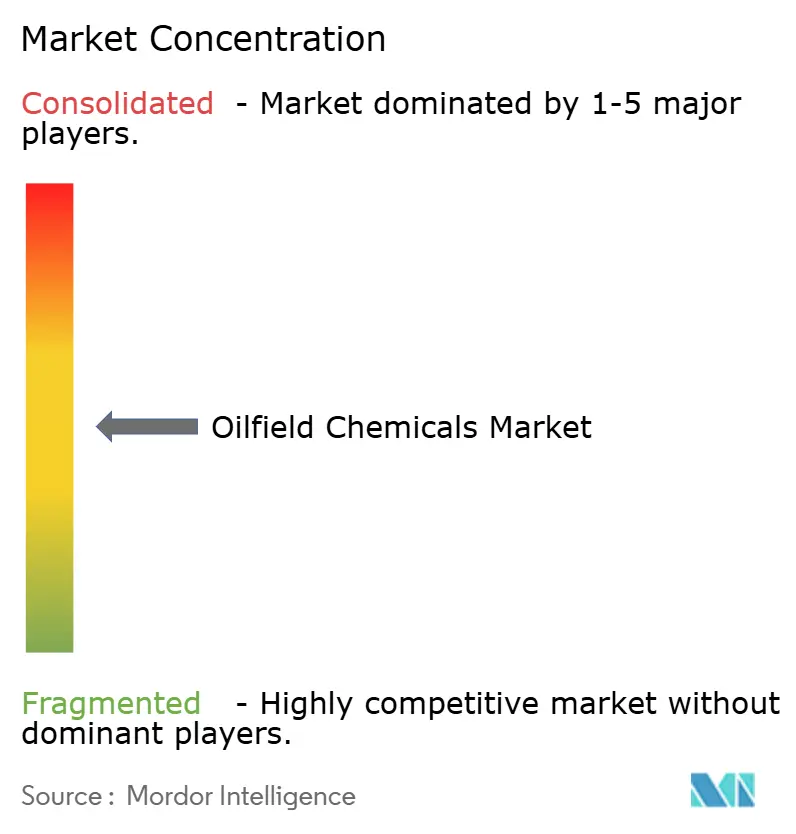

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oilfield Chemicals Market Analysis by Mordor Intelligence

The Oilfield Chemicals Market size is estimated at USD 29.95 billion in 2026, and is expected to reach USD 35.41 billion by 2031, at a CAGR of 3.41% during the forecast period (2026-2031). The oilfield chemicals market is being shaped by operators who must drill deeper, withstand hotter reservoirs, and still deliver measurable progress on decarbonization metrics. Persistent shale gas output in the United States supports demand for friction reducers even while price volatility curbs discretionary capital spending. Corrosion-control chemistries dominate value because aging tubulars in CO₂-rich and sour formations raise the cost of integrity failures. At the same time, bio-based surfactants are growing faster than conventional additives as lenders link borrowing costs to ESG disclosures. Digital dosing platforms such as SLB’s AI-enabled system and Baker Hughes’s Leucipa are tilting procurement decisions toward suppliers that couple molecules with real-time analytics.

Key Report Takeaways

- By chemical type, corrosion inhibitors led with 33.56% of the oilfield chemicals market share in 2025. However, the demand for Bio-based Surfactants is poised to grow at a CAGR of 4.82% during the forecast period (2026-2031).

- By application, well stimulation accounted for 30.18% of the oilfield chemicals market size in 2025. However, the share of Enhanced Oil Recovery is poised to grow at a CAGR of 5.50% during the forecast period (2026-2031).

- By geography, the Middle East and Africa held 28.36% of the 2025 demand, while the Asia-Pacific is forecast to grow at a 4.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oilfield Chemicals Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased shale gas exploration and production | +0.8% | North America, Argentina, China | Medium term (2-4 years) |

| Rising demand for petroleum-based fuels from transportation | +0.6% | Asia-Pacific, Middle East | Long term (≥ 4 years) |

| Expansion of deep- and ultra-deep-water projects needing advanced chemistries | +0.9% | Brazil, West Africa, Gulf of Mexico | Long term (≥ 4 years) |

| Growth in CO₂-EOR and CCUS projects requiring compatible chemicals | +0.7% | North America, Middle East, China | Medium term (2-4 years) |

| Bio-based, low-toxicity formulations tied to ESG-linked finance criteria | +0.5% | Global, fastest in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increased Shale Gas Exploration And Production

Record dry-gas volumes from the Marcellus and Haynesville basins sustained high usage of friction reducers, clay stabilizers, and biocides in 2025[1]U.S. Energy Information Administration, “Natural Gas Production Report,” eia.gov. Operators continue to extend lateral lengths, increasing stage counts and raising total chemical consumption per well even as dosage efficiencies improve. Argentina’s Vaca Muerta attracted more than USD 5 billion in upstream capital during 2024-2025, with custom slickwater systems formulated for the play’s high-temperature, high-clay profile. China’s push to commercialize Sichuan Basin shale faces water scarcity, so producers are trialing foamed and waterless fracturing fluids that cut freshwater requirements by up to 70%. Shale growth in these three regions alone underpins a sizable tranche of the oilfield chemicals market, even though per-barrel chemical intensity continues to decline in mature North American plays.

Rising Demand For Petroleum-Based Fuels From Transportation

Global liquids demand remains resilient because aviation, shipping, and long-haul trucking lack cost-competitive battery alternatives. Petrochemical integration projects in India pull additional crude volumes that require reliable flow-assurance chemistries well beyond first oil[2]Reliance Industries, “Annual Report 2025,” relianceindustries.com. National oil companies in the Middle East protect low-cost barrels, ensuring a steady call on production chemicals for corrosion, scale, and emulsion control. Even in electrifying regions, legacy fleets still anchor diesel and jet fuel demand, sustaining the oilfield chemicals market in legacy and incremental wells alike. As a result, production chemical spending grows in line with base-decline management, helping operators hold plateau rates through chemical intervention rather than fresh drilling.

Expansion Of Deep- And Ultra-Deep-Water Projects Needing Advanced Chemistries

Subsea tiebacks in water depths beyond 1,500 meters operate under extreme pressure and temperature. Petrobras awarded SLB a service contract exceeding USD 2 billion to supply high-temperature inhibitors for pre-salt carbon-dioxide-rich crudes. Chevron’s Anchor project relies on hydrate inhibitors with multiyear stability to safeguard 1,600-meter tiebacks. Discoveries offshore Nigeria and Angola require paraffin and asphaltene controls that remain effective after days of residence in umbilicals longer than 40 kilometers. Each development lifts specialty-chemical intensity per barrel, reinforcing a premium tier in the oilfield chemicals market for high-reliability products. Vendors that demonstrate proven performance in 150 °C brines command above-average margins and tighter customer lock-in.

Growth In CO₂-EOR And CCUS Projects Requiring Compatible Chemicals

Permian Basin operators injected rising volumes of captured industrial CO₂ during 2025, extending field life while sequestering emissions. Corrosion inhibitors that tolerate carbonic acid and high salinity now displace generic amine blends. Oman’s Harweel pilot scaled polymer-CO₂ hybrid floods, highlighting the need for surfactants stable in 200,000 ppm brines. China National Petroleum Corporation deployed polymer-alternating-gas schemes at Daqing, spurring demand for scale preventers that keep calcium carbonate deposition at bay when CO₂ dissolves into produced water. These projects create a sustainable niche within the oilfield chemicals market that aligns commercial recovery goals with decarbonization mandates.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global shift toward clean energy and electrification | -0.6% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Crude-price volatility curbing upstream investment | -0.5% | Global, most acute in high-cost basins | Short term (≤ 2 years) |

| PFAS or hazardous-chemical regulation tightening | -0.3% | North America, Europe, rising in Asia-Pacific | Medium term (2-4 years) |

| Raw-material supply shocks for barite and bromine | -0.4% | Import-dependent regions worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Global Shift Toward Clean Energy And Electrification

Shell has capped oil output at 2024 levels and redirects USD 15 billion each year toward low-carbon ventures. BP plans a 25% reduction in hydrocarbon production by 2030, a move that trims drilling budgets and, by extension, chemical demand. TotalEnergies earmarks 40% of capital for renewables, limiting funds for green-field wells that historically pull large volumes of stimulation chemicals. The International Energy Agency’s Net Zero scenario projects falling upstream investment beyond 2025, a structural headwind for the oilfield chemicals market. While production chemicals remain essential for existing wells, the growth ceiling is lower when fewer new wells enter the mix.

Crude-Price Volatility Curbing Upstream Investment

Brent prices swung between USD 70 and USD 90 per barrel in 2024-2025, prompting operators to defer final investment decisions on deepwater and Arctic projects. The drilled-but-uncompleted inventory in the Permian fell when companies postponed completions as prices wavered. Norway’s Equinor delayed North Sea tiebacks, and Petrobras stretched appraisal campaigns for frontier pre-salt blocks, cutting near-term chemical requisitions. During such downturns, purchasing teams often favor cost-minimization and defer premium chemistries, temporarily compressing margins in the oilfield chemicals market. Short-cycle shale remains flexible, but even here, stage counts drop when cash flow tightens.

Segment Analysis

By Chemical Type: Corrosion Control Anchors Mature-Field Economics

Corrosion inhibitors retained 33.56% of 2025 revenue, confirming that asset-integrity chemistries remain the largest slice of the oilfield chemicals market. This dominance is linked to higher water cut and acid gas content in aging assets, conditions that corrode tubulars and threaten unplanned outages. In contrast, bio-based surfactants are projected to grow at a 4.82% CAGR, the fastest pace within the portfolio, as sustainability covenants tighten, coupled with financiers rewarding environmentally preferred formulations. The oilfield chemicals market size for polymers has plateaued because operators recycle more flowback water, reducing required viscosifier loads per stage, yet polymer innovation around nanocomposite additives aims to restore growth through higher efficiency at lower dosage.

Demulsifiers are indispensable in offshore production, where crew changes and rough weather can require chemicals that maintain 95% separation efficiency without intervention. Scale, paraffin, and asphaltene inhibitors protect long tiebacks in Brazilian and West African deepwater, making them a stable subsegment even if volume growth lags high-profile categories. Nanotechnology-enhanced corrosion inhibitors have shown field results of 20% lower dosage yet improved film density, indicating room for margin expansion as these products scale. Altogether, chemical-type diversification helps suppliers cushion revenue against cyclical drilling downturns while preserving the oilfield chemicals market share lead enjoyed by corrosion-control products.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: EOR Chemistries Gain As Operators Squeeze Mature Assets

Well stimulation retained 30.18% of application revenue in 2025, sustained by North American refracturing and state-level disclosure laws that favor bio-derived friction reducers. Production chemicals remain a predictable cash flow stream because every incremental barrel from mature fields still needs demulsifiers, scale inhibitors, and corrosion control. Drilling chemicals ebb and flow with rig counts, but workover and completion additives carve out a stable niche by safeguarding wellbore productivity after initial production declines. Collectively, these dynamics keep the oilfield chemicals market balanced across lifecycle stages, cushioning suppliers against shocks in any single activity bucket.

Enhanced oil recovery is expected to increase at a 5.50% CAGR between 2026 and 2031, the highest application-level growth in the oilfield chemicals market. National oil companies in China, the Middle East, and Latin America are pumping polymers and surfactants to counter steep decline rates that threaten domestic supply security. Daqing alone invests more than USD 500 million each year on polyacrylamide, a commitment that underpins steady polymer demand regardless of volatility in drilling budgets. Offshore Brazil’s Mero field is piloting surfactant-polymer blends designed to withstand 150°C reservoir temperatures and 200,000 ppm salinity.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Middle East and Africa commanded 28.36% of global demand in 2025, anchored by Saudi Aramco’s Jafurah gas program and ADNOC’s sour-gas projects that require corrosion-resistant and hydrogen-sulfide-scavenging formulations. Kuwait and Iraq expand water-floods that push water cut above 80%, elevating demand for scale inhibitors and demulsifiers. Deepwater Nigeria and Angola developments rely on subsea injection systems and long-residence inhibitors to manage wax and hydrate risks in 40-kilometer tiebacks. The oilfield chemicals market size in the region will keep momentum as national oil companies protect low lifting-cost assets and integrate digital dosing to hit sustainability targets.

Asia-Pacific is forecast to grow at a 4.94% CAGR through 2031, thanks to China’s expanding polymer floods at Daqing and Jilin and India’s deepwater drilling in the Krishna-Godavari Basin. Indonesia and Malaysia pursue marginal-field EOR that needs tailor-made chemicals for high-water-cut, high-salinity crudes. Japan, South Korea, and Thailand import specialty additives for offshore workovers, and Vietnam attracts frontier exploration that mandates bio-based drilling fluids in ecologically sensitive zones. These projects widen the customer base and bolster the oilfield chemicals market even as regional policy moves gradually toward lower-carbon energy.

North America remains pivotal because the United States maintains crude output above 5 million barrels per day in the Permian Basin, driving large offtake of friction reducers, biocides, and scale inhibitors. Canada’s oil sands generate steady orders for demulsifiers and corrosion inhibitors suitable for cold-weather pipelines. Mexico’s shallow-water redevelopment needs cost-effective stimulation chemicals, although fiscal constraints cap growth. Europe’s North Sea faces declining production yet rising regulatory demands, pushing operators toward bio-based additives. Russia’s sector remains significant but is constrained by sanctions that limit access to Western specialty chemicals, creating room for domestic equivalents. South America’s growth continues to hinge on Brazil’s pre-salt, which awards multiyear chemical supply contracts to integrated service companies. This geographic mosaic underpins diversification of revenue streams across the oilfield chemicals market.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The oilfield chemicals market shows moderate consolidation. SLB, Halliburton, and Baker Hughes combine molecules, equipment, and data analytics to defend share against midsize challengers. Their bundled offerings let operators adopt a single-throat-to-choke model that streamlines contract management while guaranteeing uptime. Suppliers that combine robust R&D pipelines, digital tools, and regional logistics stand best placed to capture incremental value as the oilfield chemicals market shifts from price-per-gallon bidding to total-cost-of-ownership partnerships.

Oilfield Chemicals Industry Leaders

Halliburton

Baker Hughes Company

BASF

SLB

Chevron Phillips Chemical Company LLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Fineotex Chemical Limited (FCL) announced the acquisition of the CrudeChem Technologies Group, a United States-based specialty chemical manufacturer of advanced chemical fluid additives and comprehensive oilfield chemicals solutions for the global oil and gas sector.

- November 2025: Brenntag SE acquired Chem Tech Services, Inc., specializing in professional oilfield chemical solutions, boasting proprietary formulations tailored for energy sector operators in the Permian Basin, North America's top energy-producing region.

- July 2025: Versalis, the chemical arm of Eni, unveiled plans to spin off its Oilfield Chemicals division into a newly minted entity, Versalis Oilfield Solutions S.r.l. This strategic move seeks to fortify Versalis' foothold in the oilfield services arena, uniting pivotal expertise and activities under one streamlined and efficient banner.

Global Oilfield Chemicals Market Report Scope

Oilfield chemicals are a sub-class of specialty chemicals used in applications based on oil extraction, production, and refining. They are composed of petroleum sulfonate, anionic polyacrylamide, Fe-Cr lignosulfonate, and xanthan gum. The oilfield chemicals market is segmented by chemical type, application, and geography. By chemical type, the market is segmented into biocides, corrosion and scale inhibitors, demulsifiers, polymers, surfactants, and other chemical types. By application, the market is segmented into drilling and cementing, enhanced oil recovery, production, well stimulation, and workover and completion. The report also covers the size and forecasts for the oilfield chemicals market in 21 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

By Chemical Type

| Biocides |

| Corrosion Inhibitors |

| Demulsifiers |

| Polymers |

| Surfactants |

| Other Chemical Types (Scale Inhibitors, Paraffin and Asphaltene Inhibitors, etc.) |

By Application

| Drilling and Cementing |

| Production (Flow Assurance and Asset Integrity) |

| Well Stimulation |

| Enhanced Oil Recovery |

| Workover and Completion |

By Geography

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Iran | |

| Irag | |

| South Africa | |

| Algeria | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Chemical Type | Biocides | |

| Corrosion Inhibitors | ||

| Demulsifiers | ||

| Polymers | ||

| Surfactants | ||

| Other Chemical Types (Scale Inhibitors, Paraffin and Asphaltene Inhibitors, etc.) | ||

| By Application | Drilling and Cementing | |

| Production (Flow Assurance and Asset Integrity) | ||

| Well Stimulation | ||

| Enhanced Oil Recovery | ||

| Workover and Completion | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Iran | ||

| Irag | ||

| South Africa | ||

| Algeria | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the oilfield chemicals market today?

The oilfield chemicals market size reached USD 29.95 billion in 2026 and is forecast to climb to USD 35.41 billion by 2031, reflecting a 3.41% CAGR.

Which chemical type holds the largest share in this space?

Corrosion inhibitors remain the largest category, capturing 33.56% of 2025 revenue because operators prioritize asset-integrity solutions for aging wells.

Which application is growing the quickest?

Enhanced oil recovery leads growth at a 5.50% CAGR, supported by large-scale polymer and surfactant floods in China, the Middle East, and Latin America.

What region generates the most demand?

The Middle East and Africa accounted for 28.36% of global demand in 2025 due to major sour-gas and unconventional gas projects requiring specialty chemistries.

How are digital platforms influencing chemical procurement?

Systems such as SLB’s AI-driven dosing engine and Baker Hughes’s Leucipa automate injection, reduce waste by up to 20%, and create switching costs that favor integrated providers.