Market Overview

| Study Period | 2019 - 2030 |

|---|---|

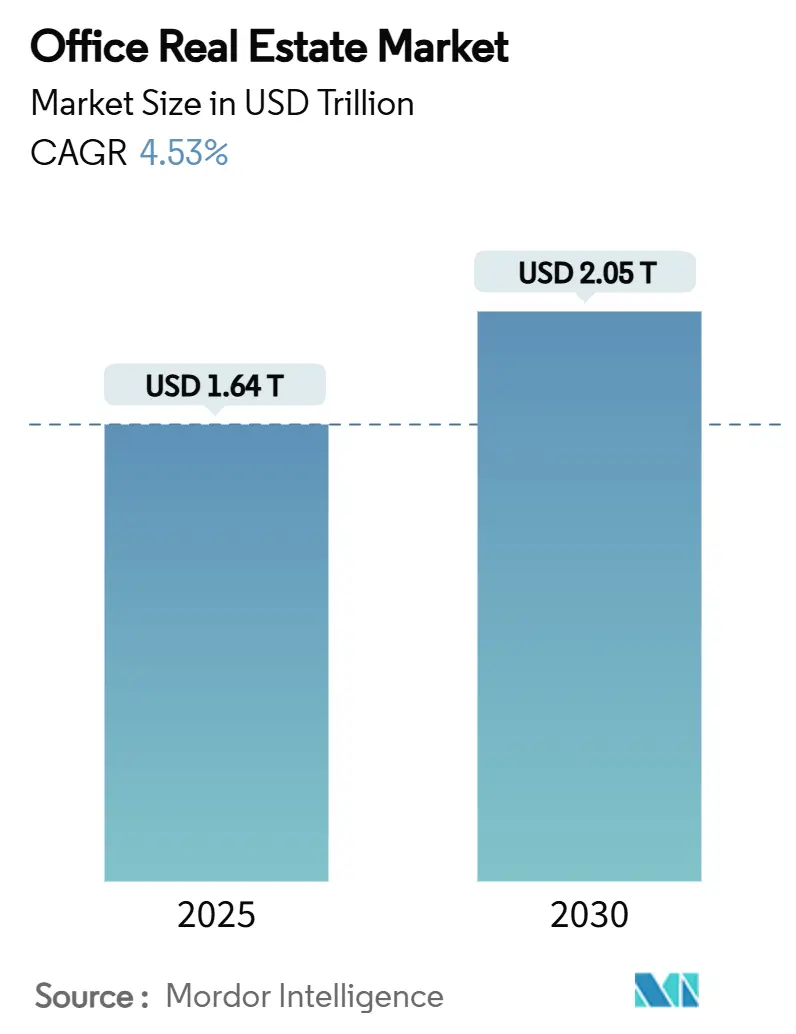

| Market Size (2025) | USD 1.64 Trillion |

| Market Size (2030) | USD 2.05 Trillion |

| Growth Rate (2025 - 2030) | 4.53% CAGR |

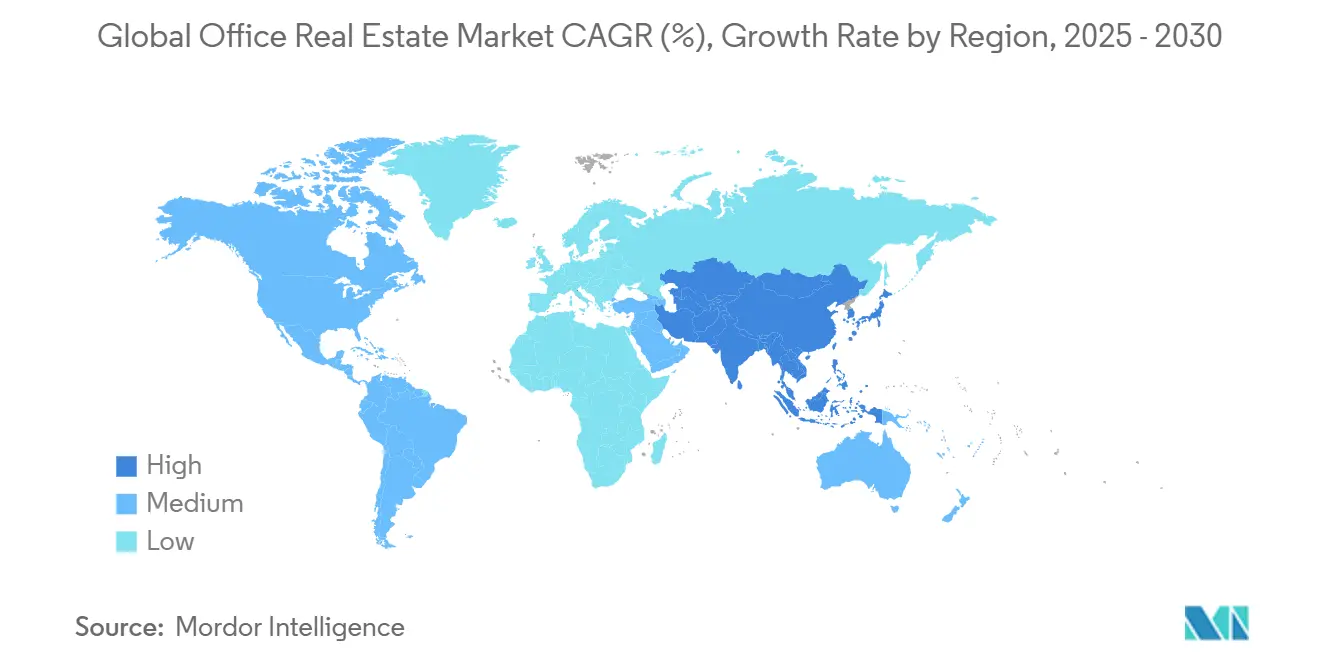

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

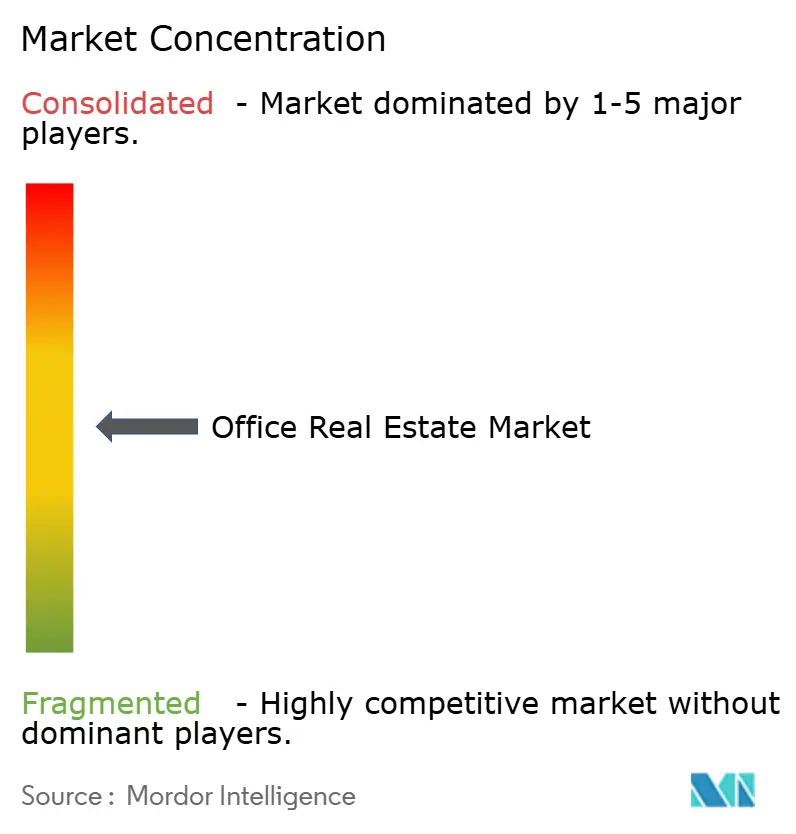

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Office Real Estate Market Analysis by Mordor Intelligence

The Office Real Estate Market size is estimated at USD 1.64 trillion in 2025, and is expected to reach USD 2.05 trillion by 2030, at a CAGR of 4.53% during the forecast period (2025-2030). The expansion reflects a sector that is reallocating capital rather than adding floor area, evidenced by a 19% nationwide vacancy rate that still accompanied four straight quarters of positive net absorption. Premium inventory is separating itself from outdated stock because new federal energy-efficiency rules require all new buildings to achieve energy consumption at least 30% below ASHRAE baselines. Investors are focusing on transit-rich trophy assets, and owners that install smart-building systems are cutting energy use by 33% while improving tenant experience[1]U.S. Department of Energy, “Building Energy Codes Program,” energy.gov. A core outcome of these trends is the shift from space-as-commodity to space-as-experience, pushing landlords to add wellness, collaboration and digital services that sustain occupancy.

Key Report Takeaways

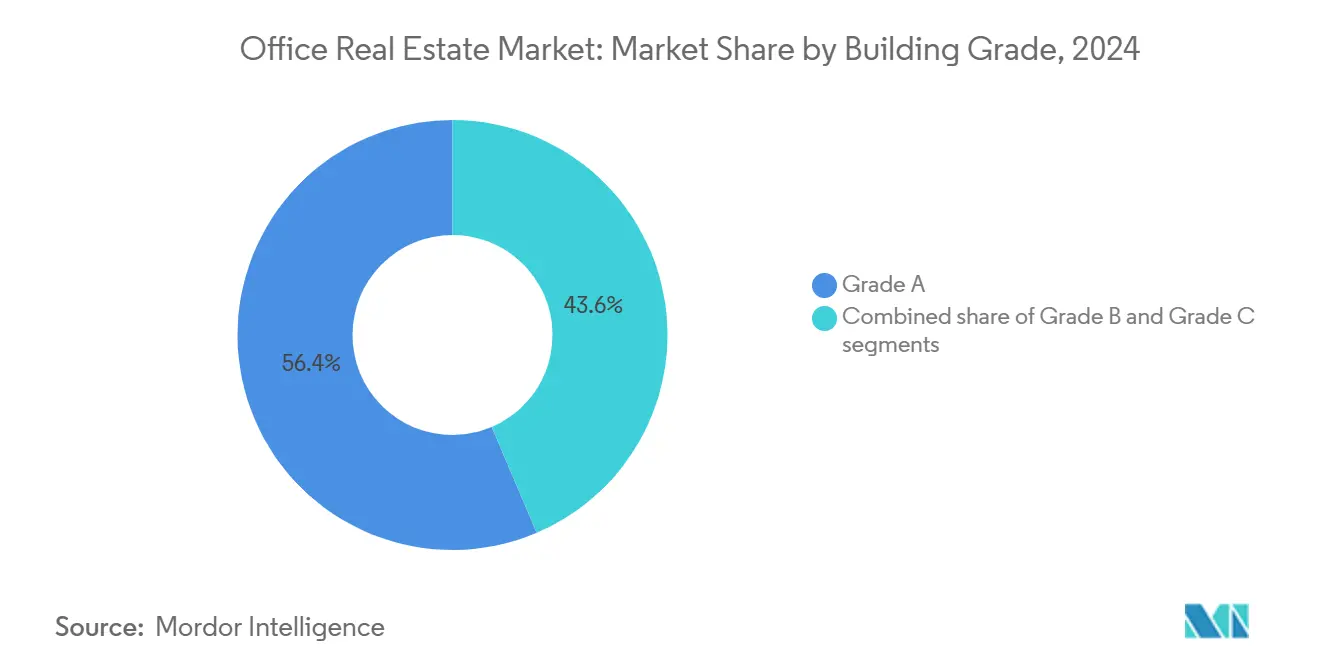

- By building grade, Grade A assets held the highest 56.4% Global office real estate market share in 2024, while Grade B is the fastest-growing at 5.03% CAGR through 2030.

- By transaction type, rental agreements dominated with 78.1% revenue share in 2024; sales transactions registered the quickest 5.19% CAGR to 2030.

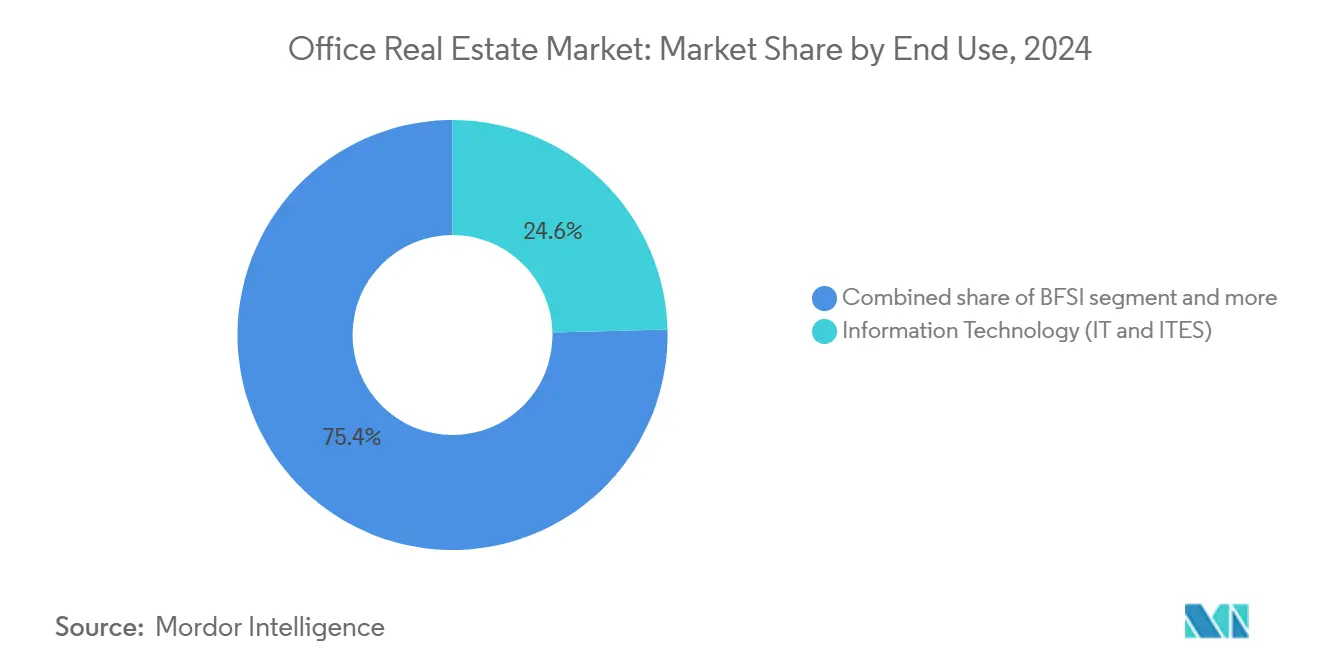

- By end use, the information technology segment accounted for 24.6% of the Global office real estate market size in 2024 and is projected to expand at a 5.30% CAGR.

- By geography, North America led with a 26.3% share of the Global office real estate market size in 2024, whereas Asia-Pacific is advancing at the highest 5.71% CAGR.

Global Office Real Estate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate ESG targets lift certified-green demand | +0.9% | Global metros | Medium term (2-4 years) |

| Hybrid work models increase demand for flexible layouts | +0.8% | North America, Europe | Medium term (2-4 years) |

| Amenity-rich, wellness-focused campuses | +0.7% | Developed markets | Medium term (2-4 years) |

| Institutional investment concentrates on core assets | +0.6% | North America, Asia-Pacific | Long term (≥4 years) |

| PropTech integration for energy and user control | +0.5% | Global tech hubs | Short term (≤2 years) |

| Urban regeneration around transit nodes | +0.4% | Asia-Pacific, US gateway cities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work Models Increase Demand for Flexible Layouts

Hybrid work adoption is prompting companies to reduce fixed desks and reshape offices into collaboration hubs. Average space per employee fell to 152 sq ft in 2024, the lowest in more than two decades. Flexible floorplates let tenants reconfigure quickly, which makes short-term leases and shared facilities more attractive. Landlords that retrofit conference rooms, plug-and-play tech and wellness zones report quicker lease-up times and lower churn. The trend is reinforcing the appeal of city-center towers that offer convenient transit as well as suburban campuses that provide green space, highlighting how flexibility affects both urban and secondary markets.

Institutional Investment Concentrates on Core Assets

Global pension funds and sovereign investors are channeling more capital into prime buildings in New York, London, Tokyo and Singapore. Such assets retain tenants even when overall vacancy remains high because they combine location, sustainability credentials and smart-building upgrades. Distressed pricing widens spreads: several funds launched USD 1 billion-plus vehicles in 2024 to acquire well-located towers below replacement cost. The strategy creates a bifurcated Global office real estate market in which core assets appreciate while obsolete stock faces either deep renovation or conversion.

Corporate ESG Targets Lift Certified-Green Demand

Companies are embedding science-based decarbonization goals in lease decisions. LEED and BREEAM labels help occupiers cut Scope 2 emissions and satisfy investor disclosures. Certified buildings show 8% higher average occupancy and attract 10%-21% valuation premiums versus non-certified peers. The premium is most pronounced in London and Paris, where green offices trade at discounts exceeding 25% and 35% respectively to conventional assets, underscoring how sustainability creates a new pricing floor.

PropTech Integration for Energy and User Control

Building owners are deploying IoT sensors, AI-enabled HVAC controls and smartphone access to manage energy and improve comfort. A Washington D.C. modernization cut energy use 33% while delivering app-based room-booking and lighting control. Operators recoup installation cost through lower utilities and higher rents, positioning PropTech not as an amenity but as a core operating requirement[2]Emma Buckland, “Smart Building Retrofits and Energy Performance,” NAIOP Research Foundation, naiop.org.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Secondary stock faces structural vacancy | -1.2% | Global secondary cities | Long term (≥4 years) |

| Lease renegotiation and space reduction | -0.9% | Major metros | Medium term (2-4 years) |

| Construction and fit-out cost escalation | -0.8% | North America, Europe | Medium term (2-4 years) |

| Macroeconomic volatility and rates | -0.6% | Leveraged markets worldwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Persistent Vacancy in Secondary and Outdated Stock

Older Class C towers lack the digital infrastructure, air quality systems and amenity mix that modern tenants require. Vacancy among those assets exceeded 25% in several US downtown submarkets in 2024. Demolition and conversion now outpace new-build deliveries for the first time in 25 years, confirming that obsolescence is structural rather than cyclical. Owners must either invest heavily or repurpose to housing, life-science labs or data centers.

Construction and Fit-Out Cost Escalation

Material price inflation, labor shortages and policy uncertainty lifted bid prices from 3.0% in Q4 2024 to 4.0% in Q1 2025. Rising interest expense compounds the hurdle, making ground-up office starts less viable. Developers pivot to phased renovations that extend building life while avoiding full-scale new construction, which constrains future supply and underpins rents for existing Grade A stock.

Segment Analysis

By Building Grade: Premium Assets Drive Differentiation

Grade A buildings captured 56.4% Global office real estate market share in 2024, underscoring investor and occupier preference for modern, adaptable space. These towers integrate high-efficiency glazing, smart sensors, and wellness-certified interiors that improve employee experience. Regulatory shifts are amplifying the advantage: all new US federal projects must meet 30% lower energy use, and many municipalities now require on-site renewable capacity. Owners who comply command longer lease terms, higher retention, and faster rent escalations[3]U.S. General Services Administration, “2025 Core Building Standards,” gsa.gov.

Grade B and Grade C assets face divergent futures. Grade B locations near transit lines will remain relevant if owners retrofit HVAC and digital services, yet older Grade C stock risks functional obsolescence and possible demolition. Premium assets are projected to post the segment-leading 5.03% CAGR, indicating the strongest growth path within the Global office real estate market through 2030.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Transaction Type: Rental Dominance with Rising Sales Interest

Rental agreements represented 78.1% of the Global office real estate market size in 2024. Corporations favor operating leases that preserve capital and keep occupancy flexible amid uncertain headcount forecasts. The structure also lets management test hybrid layouts without long-term balance-sheet exposure.

Sales transactions are accelerating at a 5.19% CAGR as investors target marked-down properties with repositioning potential. Several sovereign wealth funds purchased city-center towers at prices 20%-30% below peak values in 2024, signaling confidence that well-located assets will outperform once macro conditions stabilize. Distressed-asset pipelines in the US and Europe are expected to widen, giving deep-capital buyers an entry point into core submarkets.

By End Use: Technology Sector Leads Demand Evolution

Information technology companies accounted for 24.6% of the 2024 demand, making them the largest end-user block within the Global office real estate market. Their preference for collaboration zones, rapid reconfiguration and embedded digital infrastructure aligns closely with high-spec layouts. Tokyo and Seoul maintained vacancy below 4% on the back of tech-sector hiring, while Bengaluru recorded record net absorption among newly delivered towers. The technology segment is forecast to grow at 5.30% CAGR to 2030, the fastest among end-users, propelled by ongoing cloud, AI, and semiconductor investment cycles.

BFSI tenants remain the second-largest cohort, attracted to buildings offering high-grade security and proximity to financial districts. Professional services firms value prestigious addresses for client meetings, sustaining demand in gateway cities. Life-science and energy companies add further depth, though their requirements often lean toward specialized lab or industrial-hybrid space.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

North America retained 26.3% Global office real estate market share in 2024. The region benefits from deep capital markets, diverse industry clusters, and ongoing urban redevelopment initiatives. Vacancy levels stayed elevated in secondary towers, yet transit-oriented Grade A buildings in New York, Boston, and Toronto reported stable occupancies. Federal energy mandates are pushing owners to retrofit mechanical systems and curtain walls, extending asset life while cutting emissions. Adaptive-reuse policies, such as Chicago’s program to convert four downtown high-rises into 1,000 apartments, aim to absorb excess supply and revitalize city cores.

Asia-Pacific is projected to outpace every other region at a 5.71% CAGR, reflecting rapid urbanization, institutional capital inflows, and technology sector expansion. Singaporean, Korean, and Japanese funds deployed USD 24.56 billion during Q3 2023, nearly 70% above their 10-year average, to secure prime towers in Tokyo, Seoul, and Sydney. Vacancy is already below 4% in several districts, and government infrastructure spending supports new CBD precincts linked to mass-transit upgrades[4]Organisation for Economic Co-operation and Development, “Institutional Investment in Real Estate 2024 Report,” oecd.org.

Europe, the Middle East and Africa, and South America contribute diversified growth drivers. European capitals lead on sustainability: London and Paris green offices trade at 25%-35% premiums. Middle Eastern cities leverage economic-diversification plans while offering long-term income backed by sovereign tenants. South American markets such as São Paulo experience cyclical volatility, yet policy reforms and nearshoring trends could lift absorptions in the medium term.

Note: Segment shares of all individual segments available upon report purchase

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The office real estate market is moderately concentrated. Competition centers on the ability to deliver and manage trophy-quality assets that satisfy stringent ESG and digital-capability standards. Global listed REITs and private equity platforms combine scale, access to capital, and on-the-ground management teams. These advantages allow rapid adoption of smart-building systems and the rollout of tenant-experience apps that create seamless access, booking, and service functions.

Strategic moves highlight the flight-to-quality: a USD 1 billion joint vehicle launched in 2024 targets distressed but well-located towers in Manhattan, while a sovereign fund acquired a London skyscraper at a 28% discount to 2019 pricing, announcing an immediate USD 150 million green retrofit. Several US REITs issued sustainability-linked bonds that tie coupon step-ups to energy-use reduction and green-certification thresholds, evidencing financial innovation around ESG[5]Justin P. Davidson, “Adaptive Reuse of Obsolete Offices,” Journal of Corporate Real Estate, emerald.com.

White-space opportunities include office-to-residential conversions in oversupplied downtown submarkets, repositioning of aging stock into life-science labs and data centers, and development of amenity-rich suburban campuses that answer commute-time concerns. PropTech vendors providing AI analytics and predictive maintenance are forging partnerships with landlords, yet the service layer remains dominated by incumbent property managers able to scale solutions across multi-city portfolios.

Office Real Estate Industry Leaders

CBRE

Jones Lang LaSalle IP, Inc.

Cushman & Wakefield

Colliers

Knight Frank

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Prologis reported strong Q1 2025 results with Core FFO per diluted share rising 10.9% to USD 1.42, supported by a 94.9% average occupancy rate and 58 million sq ft of new and renewal leases signed across its global portfolio.

- February 2025: The U.S. General Services Administration (GSA) put new Core Building Standards into effect, mandating enhanced energy-performance and sustainable-design criteria for all federal buildings—benchmarks expected to influence private-sector office development.

- February 2025: King County, Washington, acquired the 15-story Dexter Horton Building for USD 36.6 million—well below its 2019 sale price—illustrating the broader repricing of downtown office assets and the public sector’s growing role in adaptive reuse.

- December 2025: EY released research showing that companies integrating hybrid-work analytics and ESG metrics into real-estate decisions are outperforming peers on occupancy efficiency and employee retention, reinforcing the demand for tech-enabled, certified-green offices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the office real estate market as the total dollar value of newly built or substantially refurbished multi-tenant buildings and single-tenant offices that are offered for lease or sale across Grade A, B, and C categories. Transactions analyzed include shell-and-core disposals as well as stabilized income-producing assets that change hands during the base year.

Scope exclusions include owner-occupied headquarters, co-working service revenue streams, and stand-alone property-management or brokerage fees, which lie outside our market boundary.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifescience, Energy, Legal)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed developers, institutional investors, corporate occupiers, and regional planners across North America, Europe, Asia-Pacific, and the Gulf. These conversations validated rent trajectories, pre-commitment ratios, and construction lead times, letting us fine-tune assumptions that pure desk work could not fully surface.

Desk Research

We began with public datasets from bodies such as the World Bank, the International Monetary Fund, and UN-DESA to anchor macro indicators that steer workplace demand. Industry-specific feeds, including MSCI Real Assets transaction logs, U.S. Census building permits, and Eurostat construction output, offered construction and investment signals. Trade associations such as NAIOP and the Royal Institution of Chartered Surveyors supplied vacancy, absorption, and cap-rate benchmarks, which our team cross-checked through Dow Jones Factiva and D&B Hoovers filings to capture developer pipelines and REIT deal flows. These sources are illustrative, not exhaustive; many additional open and proprietary references informed our desk work.

Market-Sizing & Forecasting

A top-down build paired national construction-spend series with average prime office cost per square foot, then adjusted for vacancy and pre-leasing to arrive at occupied value. Selective bottom-up tests, such as Grade A supplier roll-ups and sampled average selling price times volume checks, helped temper over- or under-shoots. Key variables include new gross leasable area completions, net absorption, average prime rent, GDP per capita growth, white-collar employment, and cap-rate shifts. A multivariate regression forecast projects each driver through 2030 and feeds a scenario matrix that covers muted, base, and expansion outlooks.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer review by a second analyst, and a senior sign-off. We revisit models annually or sooner if interest rate shocks, major policy moves, or mergers shift fundamentals, ensuring clients receive the freshest view.

Why Mordor's Office Real Estate Baseline Earns Investor Trust

Published numbers often diverge because providers pick different asset pools, pricing conventions, and refresh points.

Our disciplined scoping and yearly recalibration minimize such noise, so decision-makers can benchmark confidently.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.64 trillion (2025) | Mordor Intelligence | - |

| USD 2.10 trillion (2025) | Global Consultancy A | Counts flexible-workspace service revenue as real estate value, inflating totals |

| USD 2.50 trillion (2024) | Industry Data Firm B | Adds land-bank purchases and tenant fit-out spend, but omits resale activity |

| USD 3.40 trillion (2024) | Data Analytics Provider C | Focuses only on professionally managed assets, excluding owner-occupied stock |

Taken together, the comparison shows that Mordor's base year rests on a transparent scope, balanced inputs, and repeatable steps, giving stakeholders a dependable point of departure for strategy.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the expected size of the Global office real estate market by 2030?

The Global office real estate market size is projected to reach USD 2,048 billion by 2030.

Which building grade is performing best?

Grade A assets held 56.4% share in 2024 and are growing fastest at a 5.03% CAGR due to superior amenities and sustainability compliance.

Why are sales transactions gaining momentum if rentals dominate?

Investors are purchasing discounted towers for repositioning while occupiers keep rentals for flexibility, fuelling a 5.19% CAGR in sales volume.

Which region offers the highest growth potential?

Asia-Pacific leads with a 5.71% CAGR, driven by urbanization and technology-sector expansion.

How does ESG influence occupancy and valuations?

Certified-green offices register 8% higher occupancy and 10%-21% valuation premiums, making sustainability a core leasing criterion.

What are key risks facing landlords?

Structural vacancy in outdated stock and rising construction costs reduce returns, reinforcing the need for renovation or adaptive reuse.